TUT Economic Research Series

Department of Finance and Economics

Tallinn University of Technology

www.tutecon.eu

Kristjan Liivamägi

Tarvo Vaarmets

Tõnn Talpsepp

TUTECON Working Paper No. WP–2014/7

Masters of the Stock Market

1

Masters of the Stock Market

Kristjan Liivamägi, Tarvo Vaarmets, Tõnn Talpsepp

1

Department of Finance and Economics, Tallinn University of Technology

Abstract

We analyze how intellectual abilities and education affect investors’ risk–adjusted returns in

the stock market. To investigate such effects, we use educational performance measured by

standardized exams and the type and specialty of a university degree obtained. The data used

covers one complete business cycle and includes detailed transactions and performance on the

national stock exchange for all Estonian individual investors along with their past educational

records from a national registry. Controlling for trading style, wealth, experience and variety

of educational characteristics, we provide empirical evidence that investors with higher

mathematical skills combined with overall high intellectual ability, have higher probability to

outperform market. We also show that investors holding higher university degrees or

specialize in certain fields achieve higher risk-adjusted return in the stock market.

Keywords: risk-adjusted performance, educational characteristics, individual investors

JEL classification: G11, I22, J24

1

We would like to thank Nasdaq OMX Tallinn Stock Exchange and Estonian Ministry of Education and Science

for providing the data and especially Kalle Viks and Marko Mölder for the cooperation. Additionally, we would

like to thank associate professor of Statistics and Econometrics Ako Sauga for assistance and seminar

participants at Tallinn University of Technology and University of Zurich.

2

1. Introduction

A superstition that the successful investor in the stock market possesses some

“magical skills” or deep insights, which are converted into money through profitable trades,

dominates in media and society. The question why some investors are more successful in the

stock market throughout the full business cycle than others has haunted the financial world for

decades but has stayed unanswered, in part because of absence of appropriate data.

Equipped with detailed transaction data from the Estonian stock exchange and

combining them with official registry-based detailed educational characteristics and results

(including high school grades and state administered standardized exam results) for all

individual investors in Estonia, we are able to assess if educational level, type of education,

other educational competencies or intellectual ability affect investors’ performance in the

stock market. We are able to consider the whole business cycle covering the years 2004-2012.

It should be noted that high school grades and exam results are available only for those whose

age does not exceed 35-40 years in 2012.

Several studies have concluded that the overall educational level is one factor affecting

the financial behavior of investors. Hong, Kubik, and Stein (2004) and Kumar (2009) show

that investors with a university degree have a higher propensity to invest in stocks compared

to less educated investors. Christiansen, Joensen, and Rangvid (2008) demonstrate that

financial decisions do not only depend on education level, but are influenced also by the type

of the education. Individuals having a university degree in economics, are more likely to

participate in the stock market and hold stocks than otherwise comparable investors.

Grinblatt, Keloharju, and Linnainmaa (2012) have provided evidence that individuals with

higher IQ are attaining better performance but they were not able to include educational

characteristics. Gottesman and Morey (2006) have demonstrated that fund managers holding

MBAs from top ranked schools exhibit superior performance, but their sample includes only

mutual fund managers. Guiso, Haliassos, and Jappelli (2003) assert that the overall education

level is affecting the financial behavior, but they have not considered how educational

characteristics influence investor’s risk-adjusted performance in the stock market. This

question has stayed unanswered, in large part because an absence of appropriate data.

We use a complete dataset from the Estonian stock market, which includes details of

all transactions made by all investors from 2004 to 2012, together with a unique dataset

obtained from the national educational registry, which includes all high school grades and

results of high school final exams. Additionally, we obtained information for all individuals’

3

educational levels, including university degrees and types of education. Combining those

unique and comprehensive datasets allows us to answer the question how high school grades

and final exams as well university degree and type of education influence investor’s behavior

in the stock market. We use data from a full business cycle to avoid biases that could arise

from using only either bull market or bear market periods and to include changes in investor’s

perceptions, trading and risk taking behavior during the 2008–2009 financial crises as noted

e.g. by Hoffmann, Post, and Pennings (2013).

The main contribution of the this paper is the first empirical documentation of

comprehensive educational characteristics, which influence investor’s risk–adjusted returns in

stock market during the full business cycle, including the bull and bear market. Christiansen,

Joensen, and Rangvid (2008) draw attention to one of the still unsolved questions – whether

economists also perform better on the stock market. Thus, the aim of the current paper is to

study whether the risk-adjusted returns of the holders of the respective university degrees are

higher than of comparable investors. In addition to looking at the investors with economics

education, we are able to compare the results of investors with a wide range of different

educational backgrounds and take into account their skills in mathematics and other subjects

by classifying investors by the results that they have obtained in state administered exams

after high school. Our hypothesis is that investors with higher state national exam result,

higher educational level, meaning bachelor, masters or doctors degree and with university

degree in economics demonstrate higher risk-adjusted performance in the stock market than

investors with no such educational characteristics.

In this paper we will extend previous studies and offer empirical evidence that

investors with higher mathematical skills combined with high overall intellectual ability and a

high educational level (meaning bachelor, masters or doctors degree) are more successful in

the stock market than investors who have not proved their high intelligence in mathematics or

other high school exams or obtained a university degree. Furthermore, we present evidence

that investors with a university degree in economics achieve higher risk-adjusted returns in

stock market compared with those with no such degree. Additionally, we show that investors

holding university degree in information technology and business administration outperform

the market index and show better performance than investors with no such degree. We

demonstrate that good performance in state national exams alone is not sufficient to achieve a

high performance in stock market, but one must have also corresponding degree from

university to master the stock market. Deeper analysis of the university curriculum of those

4

subjects reveals the true reasons behind better performance and helps to explain why some

investors master stock picking and analyzing better than others.

In Section 2 the article provides information on the previous literature. In Section 3 we

discuss the data used. Section 4 offers insight into the methodology of risk-adjusted

performance measurement. In Section 5 we present empirical evidence of how national exam

results influence investor’s performance in the stock market. Additionally, we provide

evidence for risk-adjusted performance among investor’s with university degree. Furthermore

up to date empirical results of investors trading behavior and risk-adjusted performance along

with robustness tests are provided. Section 6 concludes.

2. Pervious literature

Many researchers argue that the educational level has a significant impact on financial

behavior. Nguyen and Schuessler (2012) state that a higher level of education reduces

significantly behavioral biases such as self-attribution bias, anchoring bias and

representativeness. Guiso, Haliassos, and Jappelli (2003) show that stock market participation

is strongly correlated with investor’s wealth and the level of education. Guiso and Jappelli

(2005) provide empirical evidence that financial awareness is positively correlated with

education, household resources, long-term bank relations and proxies for social interaction.

They find that an economic education increases financial awareness. Bernheim and Garrett

(2003) conclude that financial education in the workplace significantly increases the

probability of savings in general, and that households who were exposed to financial curricula

during high school have higher savings rates than others. Kaustia and Torstila (2011) show

that besides educational factors also values such as political views, determine stock market

participation. They find that left-wing voters and politicians are less likely to invest in stocks.

Overall, the educational environment where prospective investors spend a lot of time is an

important factor influencing investment decisions and choice to participate in stock market.

Vaarmets, Liivamägi, and Talpsepp (2014) show that higher education and intellectual

abilities increase the probability of stock market participation.

Research by Barnea, Cronqvist, and Siegel (2010) seeks to tie most of the work done

in behavioral finance together, arguing that many factors influencing our financial behavior

are in turn affected by our genetics. They use data of Swedish identical and fraternal twins to

show that our financial behavior is greatly determined already before we are born. This means

5

the genetic factor influences our stock market decisions. In addition they show that family

environment does also have a significant effect on the investment behavior of young

individuals, but this effect disappears (unless the twins stay in frequent contact) as an

individual gains her own experiences. Latter is consistent with the view that our social life

impacts our stock market participation. Reason may be that learning from friends and

neighbors probably reduces fixed participation costs as emphasized by Hong, Kubik, and

Stein (2004).

Additionally, we can find several researches concentrating on different factors

influencing investor behavior and performance is the stock market. For example Kumar

(2009) finds that investors with lower income and lower education level are more likely to

choose lottery-type stocks or gamble in the stock market. Stock market gamblers are also

rather younger and unemployed. Their portfolio performance is usually worse than average.

This is consistent also with evidences that financial decisions are influenced by age – older

investors outperform younger investors. Additionally female investors tend to experience

better performance than male investors as they hold stocks longer and trade less noted by e.g.

Barber and Odean (2001) and Talpsepp (2010).

Barber and Odean (2007) provide evidences that individual investors tend to buy

stocks, which grab their attention through unusual events. They are net buyers on high volume

days, following both extremely negative and extremely positive one-day returns, and when

stocks are in the news. Still, this kind of behavior does not generate superior returns and

institutional investors seems to know that, because they do not display attention-driven

buying. Odean (1998) has also focused on the influence of trading frequency to the stock

performance and found that most investors do not benefit from active trading. On average, the

stocks investors buy subsequently underperform those they sell. In addition most active

traders underperform those who trade less (Barber and Odean (2000)). Furthermore there are

also evidences that foreign investor and investors with the larger portfolio (sophisticated,

institutional investors) do better in stock market than domestic investors and investors with

small portfolio (less sophisticated, households). Sophisticated institutional foreign investors

tend to hold winners and sell losers, while less sophisticated domestic households tend to do

the opposite as found by Grinblatt and Keloharju (2000). This view is shared by Talpsepp

(2011). Grinblatt and Keloharju (2001) find that investors are reluctant to realize losses and

that past returns and historical price patterns affect trading. Feng and Seasholes (2005) added

trading experience to their research and proved that more sophisticated and more experienced

investors are less influenced by the disposition effect and therefore act more rational.

According to Dhar and Zhu (2006) the wealth is also connected to the investor behavior –

wealthier individuals tend to be less influenced by the disposition effect.

While previous researchers have used indirect measure of sophistication, Grinblatt,

Keloharju, and Linnainmaa (2012) have proved that directly measured IQ really does

influence trading behavior and portfolio performance. Investors with higher IQ have better

stock-picking skills and market timing; therefore their portfolios are also experiencing better

performance. Gottesman and Morey (2006) proved that fund managers who hold MBAs from

schools ranked in the top 30 of the Business Week rankings of MBA programs exhibit

performance superior to the performance of both managers without MBA degrees and

managers holding MBAs from unranked programs. Additionally, they conclude that other

education variables, such as whether the manager attained a CFA designation or holds either a

non-MBA masters-level graduate degree or Ph.D., are generally unrelated to mutual fund

performance. We on the other hand provide a clear empirical evidence that individual

investors holding a bachelor, masters or doctoral degree achieve higher risk-adjusted returns

in the stock market then investors with no such degree.

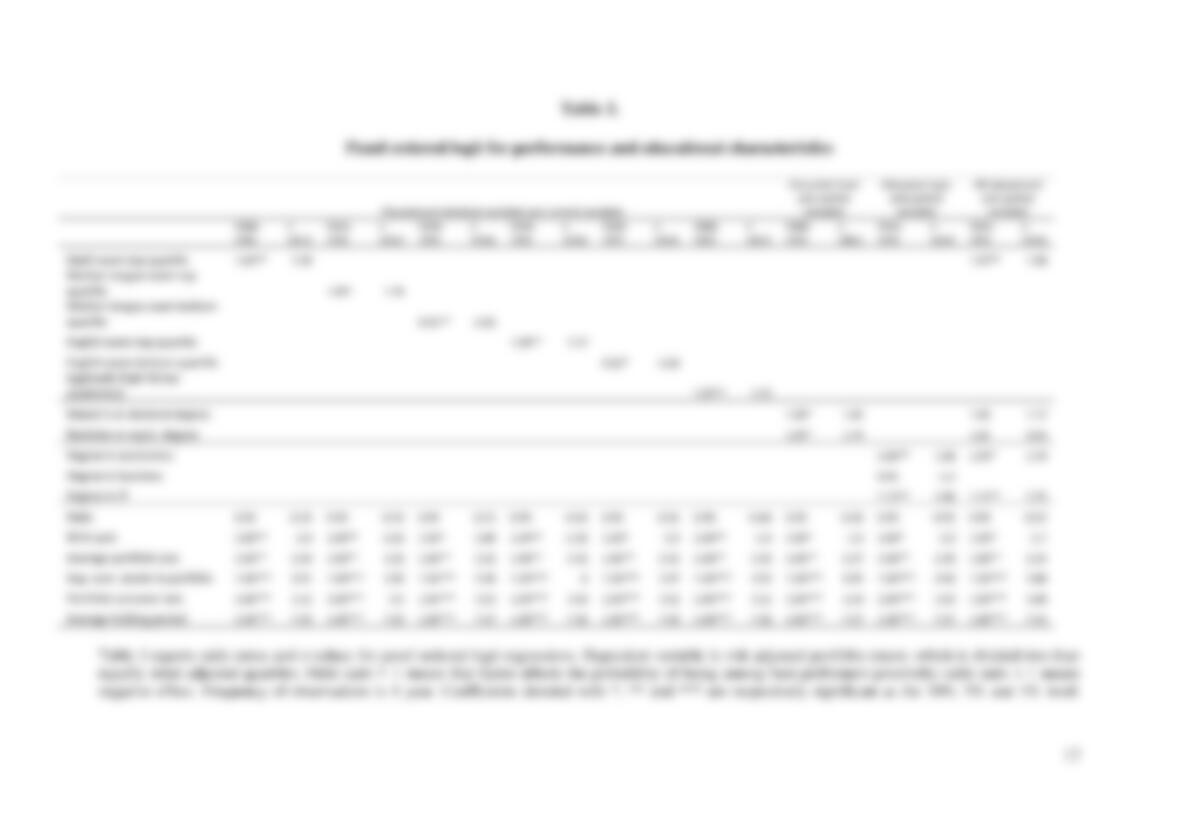

3. Data