Lindsay is a student who has accrued a lot of debt over the past year.

She is so overwhelmed and doesn’t know where to begin.

PART 4 Managing Insurance

Needs

Chapter 8 Insuring Your Life

Chapter 9 Insuring Your Health

Chapter 10 Protecting Your Property

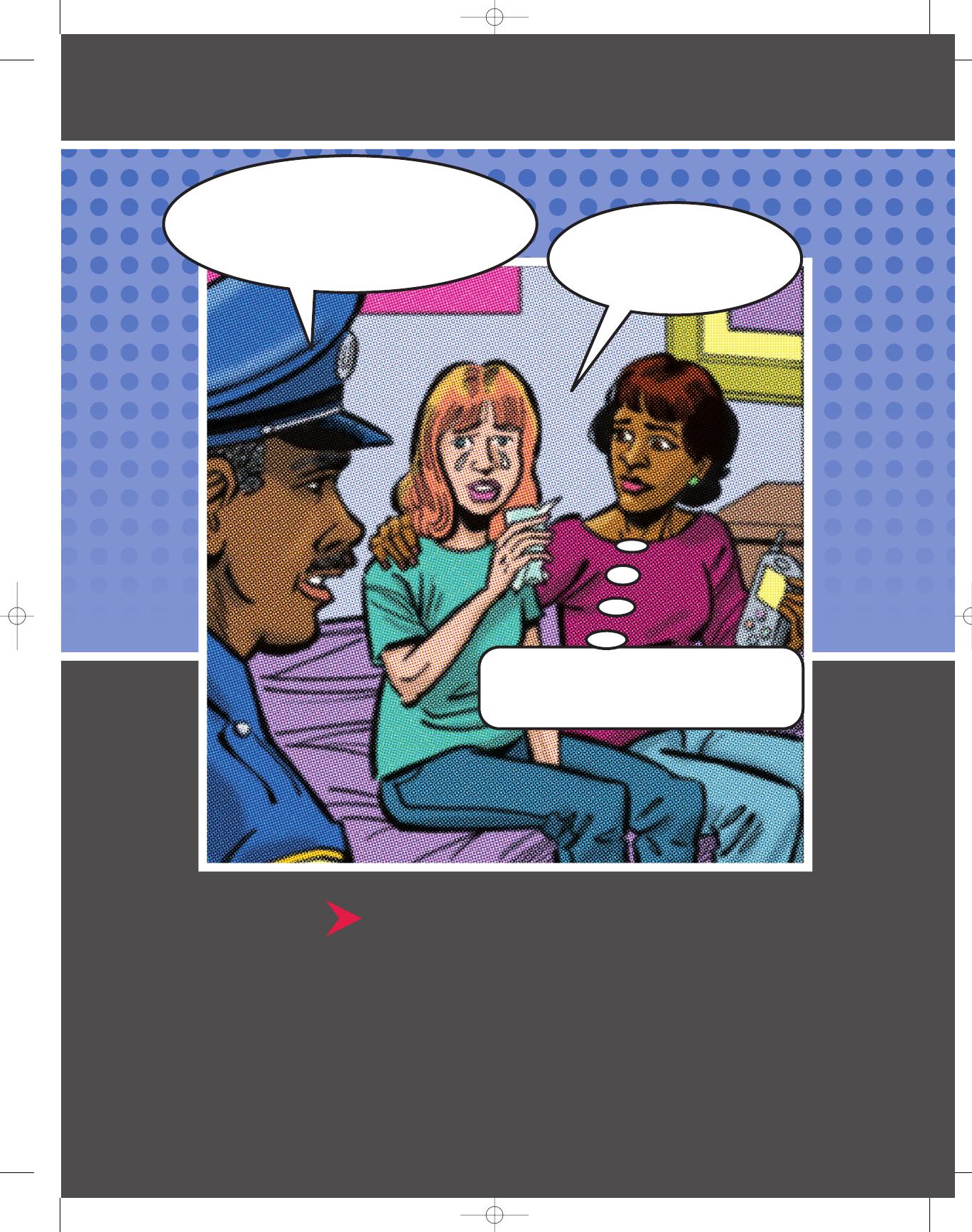

So…your computer and

your stereo were stolen…did you notice

anything else missing?…By the way,

you do have renter’s insurance,

don’t you?

I…I…dunno…if

anything else was stolen

yet…but…I do have

renter’s insurance…

Wow…I don’t have renter’s

insurance…I wonder how I can

get it…I better check with GJ11.

22865_08_c08_p239-271.qxd 10/5/06 12:55 PM Page 239

Insuring Your Life

CHAPTER 8 LEARNING GOALS

LG1 Explain the concept of risk and the basics of insurance

underwriting. p. 240

LG2 Discuss the primary reasons for life insurance and

identify those who need coverage. p. 242

LG3 Calculate how much life insurance you need. p. 244

LG4 Differentiate among the various types of life insurance

policies and describe their advantages and disadvantages. p. 249

LG5 Choose the best life insurance policy for your needs

at the lowest cost. p. 259

LG6 Become familiar with the key features of life insurance

policies. p. 263

8 : 240 Insuring Your Life

LG1 BASIC INSURANCE CONCEPTS

As most people discover, life is full of unexpected events that can have far-reaching con-

sequences. Your car is sideswiped on the highway and damaged beyond repair. A family

member falls ill and can no longer work. A fire or other disaster destroys your home. Your

spouse dies suddenly. Although most people don’t like to think about possibilities like this,

protecting yourself and your family against unforeseen events is part of sound financial

planning. Insurance plays a central role in providing that protection.

Auto and homeowner’s

insurance

, for example, reimburses you if your car or home are destroyed or damaged.

Life insurance

helps replace lost income if premature death occurs, providing funds so that

your loved ones can keep their home, maintain an acceptable lifestyle, pay for education,

and meet other special needs.

Hospitalization and health insurance

covers medical costs

when you get sick, and

disability insurance

protects your income while you’re ill.

All of these types of insurance are intended

to protect you and your dependents from

the financial consequences of losing assets or income when an accident, illness, or death

occurs.

By anticipating the potential risks that your assets and income could be exposed

to and weaving insurance protection into your financial plan, you lend a degree of certainty

to your financial future. We’ll begin this chapter by introducting important insurance con-

cepts such as risk and underwriting before focusing on how to make decisions regarding

life insurance. In Chapters 9, and 10, we’ll discuss other important types of insurance

including health insurance and property insurance.

22865_08_c08_p239-271.qxd 10/5/06 12:55 PM Page 240

The Concept of Risk

An important concept in any discussion of insurance is

risk.

In insurance terms, risk is defined as

uncertainty with respect to economic loss. Whenever you and your family have a financial

interest in something—whether it’s your life, health, home, car, or business—there’s a risk

of financial loss if that item is lost or damaged. Because such losses can be devastating to

your financial security, you must devise strategies for anticipating and dealing with poten-

tial risks. These strategies include risk avoidance, loss prevention and control, risk assump-

tion, and insurance.

Risk Avoidance

The simplest way to deal with risk is to avoid the act that creates it. For example, people

who are afraid they might lose everything they own because of a lawsuit resulting from an

automobile accident could avoid driving. Regarding life and health risks, avid skydivers or

bungee jumpers might want to choose another recreational activity!

Although risk avoidance can be an effective way to handle some risks, it has its

costs. People who avoid driving suffer considerable inconvenience, and the retired sky-

diver may find she now suffers

more

stress, which can lead to different types of health

risks. Risk avoidance is an attractive way to deal with risk only when the estimated cost of

avoidance is less than the estimated cost of handling it in some other way.

Loss Prevention and Control

Generally, loss prevention can be defined as any activity that reduces the probability

that a loss will occur (such as driving within the speed limit to lessen the chance of being

in a car accident). Loss control, in contrast, is any activity that lessens the severity of

loss once it occurs (such as wearing a safety belt or buying a car with air bags). Loss pre-

vention and loss control should be important parts of the risk management program of

every individual and family. In fact, insurance is a reasonable way of handling risk only

when people use effective loss prevention and control measures.

Risk Assumption

With risk assumption, you choose to accept and bear the risk of loss. Risk assumption

can be an effective way to handle many types of potentially small exposures to loss when

insurance would be too expensive. (For example, the risk of having your

Personal Financial

Planning

text stolen probably doesn’t justify buying insurance.) It’s also a reasonable

approach for dealing with very large risks that you can’t ordinarily prevent or secure insur-

ance for (nuclear holocaust, for example). Unfortunately, people often assume risks

unknowingly. They may be unaware of various exposures to loss or think that their insur-

ance policy offers adequate protection when, in fact, it doesn’t.

Insurance

An insurance policy is a contract between you (the insured) and an insurance company

(the insurer) under which the insurance company agrees to reimburse you for any losses

you suffer according to specified terms. From your perspective,

you are transferring your

risk of loss to the insurance company.

You pay a relatively small amount (the insurance

premium) in exchange for a promise from the insurance company that they’ll reimburse

you if you suffer a loss covered by the insurance policy.

Why are insurance companies willing to accept this risk? Simple. They combine

the loss experiences of large numbers of people, and, by using statistical information

known as

actuarial data

, they can estimate the risk of loss faced by the insured popu-

lation. Losses for the entire group of policyholders are thus more predictable than for

any one of the insureds individually. Insurance companies invest the amount they col-

lect from premiums and, if the amount they pay out in losses and expenses is less

than what they earn on those investments, they make a profit. Therefore, accurately

estimating the number and size of insured losses that will occur is critical for insur-

ance companies.

8 : 241

Insuring Your Life

risk avoidance To avoid

an act that would create a

risk.

loss prevention Any

activity that reduces the

probability that a loss will

occur.

loss control Any activity

that lessens the severity of

loss once it occurs.

risk assumption The

choice to accept and bear

the risk of loss.

insurance policy A con-

tract between the insured

and the insurer under which

the insurer agrees to reim-

burse the insured for any

losses suffered according to

specified terms.

underwriting The

process used by insurers to

decide who can be insured

and to determine applicable

rates they will charge for

premiums.

22865_08_c08_p239-271.qxd 10/5/06 12:55 PM Page 241

Underwriting Basics

Insurance companies take great pains to decide whom they will insure and the applicable

rates they will charge for premiums. This function is called underwriting. Underwriters

design rate-classification schedules so that people pay premiums equal with their chance

of loss. Through underwriting, insurance companies try to guard against

adverse selection

,

which happens when only high-risk clients apply for and get insurance coverage.

Underwriting directly impacts an insurance company’s chances of success. If under-

writing standards are too high, people will be unjustly denied insurance coverage, and

insurance sales will drop. On the other hand, if standards are too low, many insureds will

pay less than their fair share based upon their potential for losses, and the insurance com-

pany’s solvency may be jeopardized.

A basic problem facing insurance underwriters is how to select the best criteria for

classifying the people they insure. Because there’s no perfect relationship between avail-

able criteria and loss experience, some people invariably believe they’re being charged

more than they should be for their insurance. Insurers are always trying to improve their

underwriting capabilities in order to set premium rates that will adequately protect policy-

holders against insolvency and yet be attractive and reasonable.

Because underwriting practices and standards also vary between insurance compa-

nies, you can often save money by shopping around for the company offering the most

favorable underwriting policies for your specific characteristics and needs. To make an

effective decision about any insurance product, therefore, you need a basic understanding

of the different types of insurance available as well as insight into your own tolerance for

risk when it comes to protecting your financial assets and your family. The discussion of

life insurance that follows in this chapter, and succeeding chapters that discuss other

types of insurance, will help you accomplish these goals.

8 : 242 Insuring Your Life

underwriting the process

used by insurers to decide

who can be insured and

to determine applicable

rates they will charge for

premiums.

8-1

8-2

Discuss the role insurance plays in the financial planning process. Why is it

important to have enough life insurance?

Define (a)

risk avoidance

, (b)

loss prevention

, (c)

loss control

, (d)

risk assump-

tion

, and (e) an

insurance policy

. Explain their interrelationships, if any.

8-3 Explain the purpose of underwriting. What are some factors underwriters

consider when evaluating a life insurance application?

EPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHEC

Concept Check

LG2 WHY BUY LIFE INSURANCE?

Life insurance planning is an important part of every successful financial plan. Its primary

purpose is to

protect your dependents from financial loss in the event of your untimely

death

. It’s an umbrella of protection for your loved ones, protecting the assets you’ve built

up during your life and providing funds to help your family reach important financial goals

even after you die.

Benefits of Life Insurance

Despite the importance of life insurance to sound financial planning, many people put off

the decision to buy, it. This happens partly because life insurance is associated with some-

thing unpleasant in many people’s minds—namely, death. People don’t like to talk about

death or the things associated with it, so they often put off considering their life insurance

needs. Life insurance is also intangible. You can’t see, smell, touch, or taste its benefits—

and those benefits mainly happen after you’ve died. However, life insurance does have

some important benefits that should not be ignored in the financial planning process:

22865_08_c08_p239-271.qxd 10/5/06 12:55 PM Page 242

•Financial protection for dependents. If your family or loved ones depend on your

income, what would happen to them after you die? Would they be able to maintain

their current lifestyle, stay in your home, or afford a college education? Life insurance

provides a financial cushion for your dependents, giving them a set amount of money

after your death that they can use for many purposes. For example, your spouse may

use your life insurance proceeds to pay off the mortgage on your home so your family

can continue living there comfortably or set aside funds for your child’s college educa-

tion. In short, the most important benefit of life insurance is providing financial protec-

tion for your dependents after your death.

•Protection from creditors. A life insurance policy can be structured so that death ben-

efits are paid directly to a named beneficiary rather than being considered as part of

your estate. This means that even if you have outstanding bills and debts at the time

of your death, creditors cannot claim the cash benefits from your life insurance policy,

providing further financial protection for your dependents.

•Tax benefits. Life insurance proceeds paid to your heirs, as a rule, aren’t subject to

state or federal income taxes. Further, if certain requirements are met, policy proceeds

can pass to named beneficiaries free of any

estate

taxes.

•Vehicle for savings. Some types of life insurance policies can serve as a savings vehi-

cle, particularly for those who are looking for safety of principal.

Variable life policies

,

which we’ll discuss later in this chapter, are more investment vehicles than they are

life insurance products. But don’t assume that all life insurance products can be con-

sidered savings instruments. As we’ll see later in this chapter, the comparison is often

inappropriate.

Just like other aspects of personal financial planning, life insurance decisions can be

made easier by following a step-by-step approach to answer the following questions:

1. Do you need life insurance?

2. If so, how much life insurance do you need?

3. Which type of life insurance is best given your financial objectives?

4. What factors should be considered in making the final purchase decision?

Do You Need Life Insurance?

The first question to ask when considering the purchase of life insurance is whether you

need it. Not everyone does. Many factors, including your personal situation and other

financial resources, play a role in determining your need for life insurance. Remember, the

major purpose of life insurance is to provide financial security for your dependents in the

event of your death. As we’ve discussed, life insurance provides other benefits, but

they’re all a distant second to this one.

Who needs life insurance? In general, life insurance should be considered if you have

dependents counting on you for financial support. Therefore, a single adult who doesn’t

have children or other relatives to support may not need life insurance at all. Children also

usually don’t require insurance on their life.

Once you marry, your life insurance requirements should be reevaluated, depending on

your spouse’s earning potential and assets—such as a house—that you want to protect.

The need for life insurance increases the most when children enter the picture, because

young families stand to suffer the greatest financial hardship from the premature death of

a parent. Even a non-wage-earning parent may require some life insurance to ensure that

children are adequately cared for if the parent dies.

As families build assets, their life insurance requirements continue to change, both in

terms of the amount of insurance needed and the type of policy necessary to meet their

financial objectives and protect their assets. Other life changes will also affect your life

insurance needs. For example, if you divorce or your spouse dies, you may need additional

life insurance to protect your children. Once your children finish school and are on their

own, the need for life insurance may drop. In later years, life insurance needs vary

depending on the availability of other financial resources, such as pensions and invest-

ments, to provide for your dependents.

8 : 243

Insuring Your Life

HEC

22865_08_c08_p239-271.qxd 10/5/06 12:55 PM Page 243

LG3 HOW MUCH LIFE INSURANCE IS RIGHT FOR YOU?

After deciding that life insurance makes sense for your particular situation, you’ll need to

make more decisions to find the life insurance product that best fits your needs. First, you

must determine how much life insurance you need for adequate coverage. Buying too

much life insurance can be costly; buying too little may prove disastrous. To avoid these

problems, you can use one of two methods to estimate how much insurance is neces-

sary: the

multiple-of-earnings method

and the

needs analysis method

.

The multiple-of-earnings method takes your gross annual earnings and multiplies

it by some selected (often arbitrary) number to arrive at an estimate of adequate life insur-

ance coverage. The rule of thumb used by many insurance agents is that your insurance

coverage should be equal to 5 to 10 times your current income. For example, if you cur-

rently earn $70,000 a year, using the multiple-of-earnings method you’d need between

$350,000 and $700,000 worth of life insurance. Although simple to use, the multiple-of-

earnings method fails to fully recognize the financial obligations and resources of the indi-

vidual and his or her family. Therefore, the multiple-of-earnings method should be used

only to roughly approximate life insurance needs.

A more detailed approach is the needs analysis method. The needs analysis

method considers both the financial obligations and financial resources of the insured and

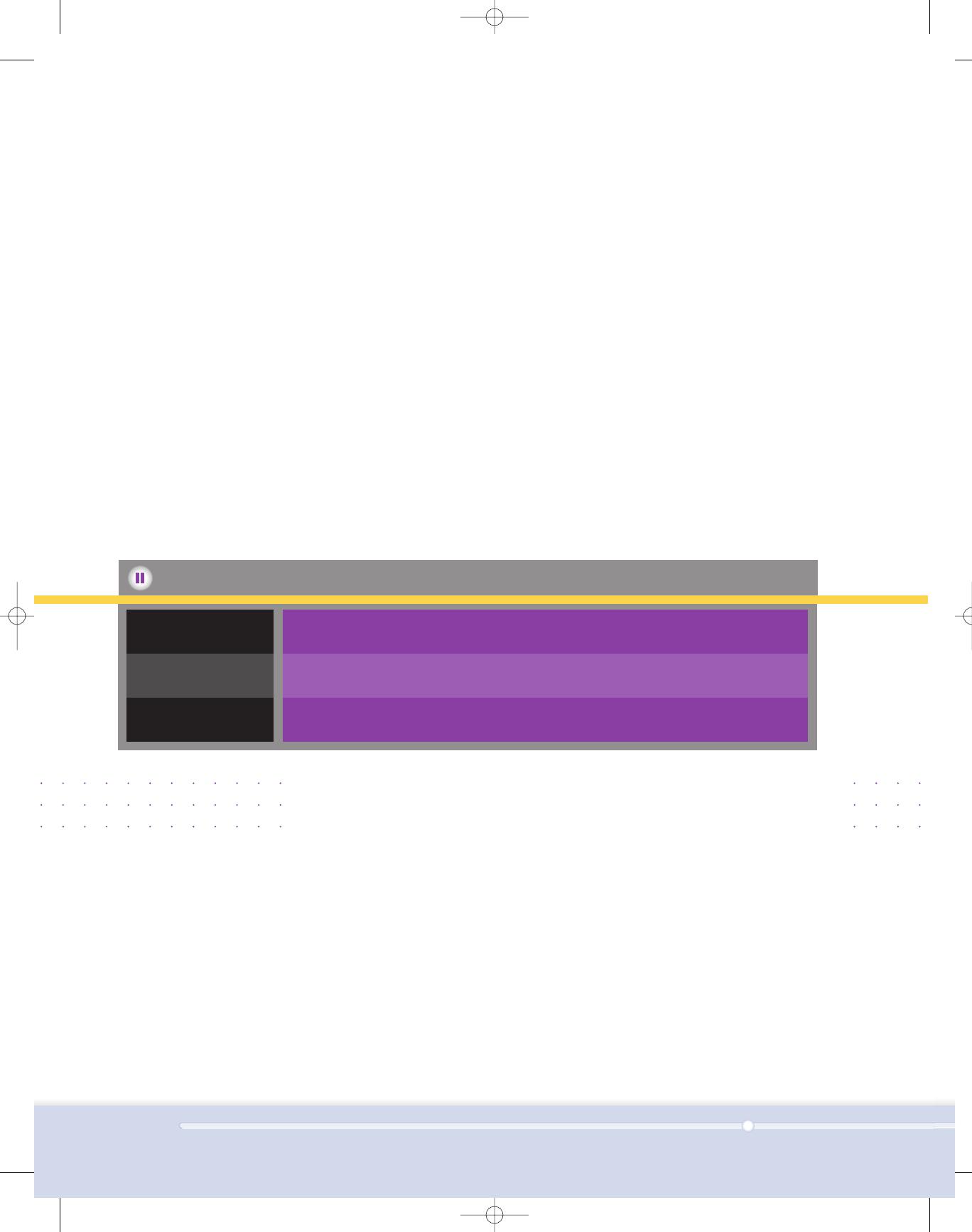

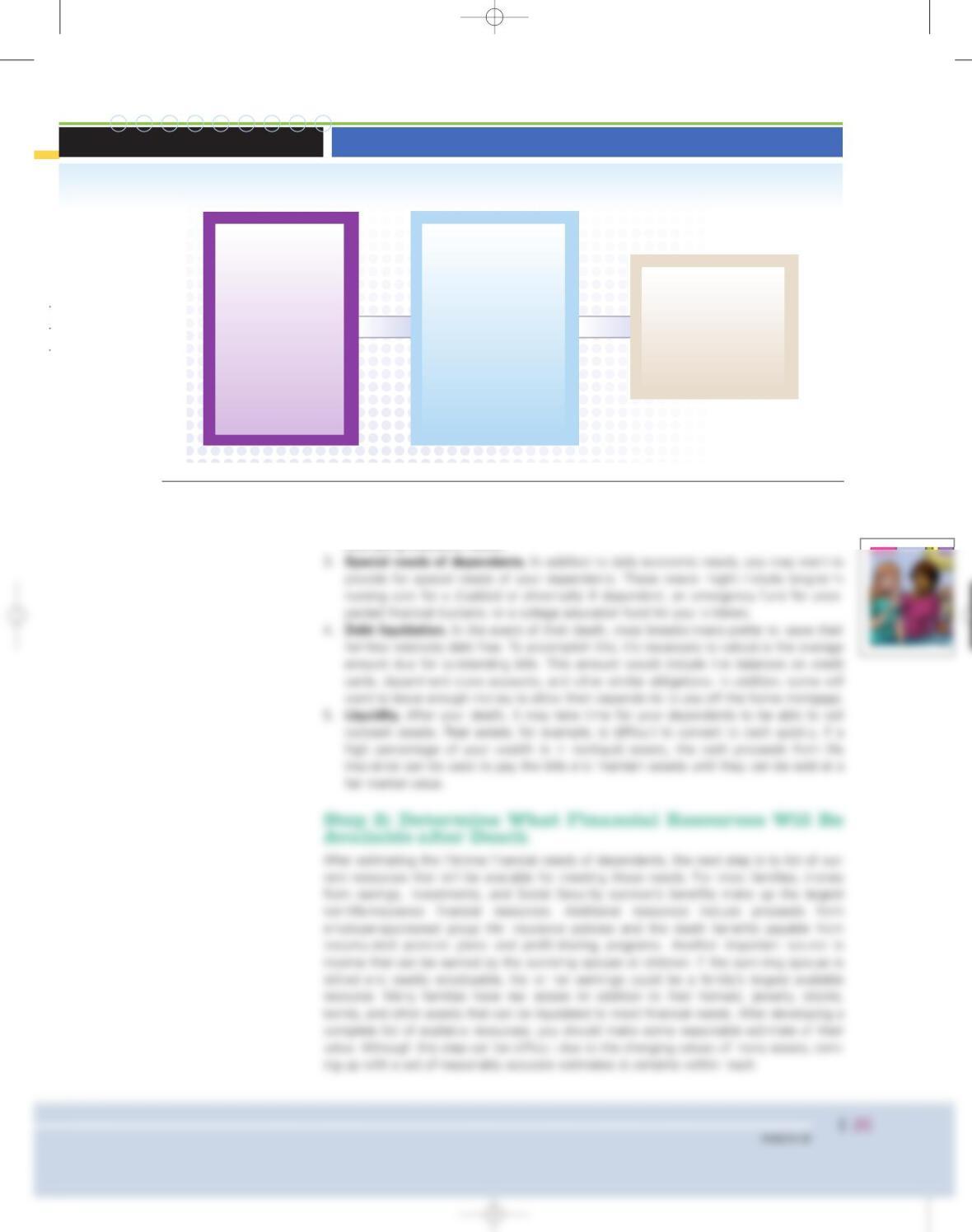

his or her dependents. This method involves three steps, as shown in Exhibit 8.1:

1. Estimate the total economic resources needed if the individual were to die.

2. Determine all financial resources that would be available after death, including existing

life insurance and pension plan death benefits.

3. Subtract available resources from the amount needed to calculate how much additional

life insurance is required.

Step 1: Assess Your Family’s Total Economic Needs

The first question the needs analysis method asks is:

What financial resources will my sur-

vivors need should I die tomorrow

? You should consider the following five items in

answering this question:

1. Income needed to maintain an adequate lifestyle. If you died, how much money

would your dependents need each month in order to live a comfortable life? Estimate

this amount by looking at your family’s current monthly budget, including expenses for

housing costs, utilities, food, clothing, and medical and dental needs. Other expenses

to consider include property taxes, insurance, recreation and travel, and savings. Try to

take into account that the amount needed may change over time. For example, once

children are grown, monthly household expenses should decrease substantially but the

surviving spouse may still need monthly support. Therefore, the survivor’s life

expectancy and the income they’ll require may also need to be considered.

2. Extra expenses if the income producer dies. These expenses include funeral costs

and any expenses that might be incurred to replace services you currently provide. For

example, a mother who doesn’t work outside of the home still provides childcare,

cooking, cleaning, and other services. If she were to die or have to return to work,

these services might have to be replaced using the family’s income. Because such

8 : 244 Insuring Your Life

multiple-of-earnings

method A method of deter-

mining the amount of life

insurance coverage needed

by multiplying gross annual

earnings by some selected

number.

needs analysis method

A method of determining the

amount of life insurance

coverage needed by consid-

ering a person’s financial

obligations and available

financial resources in addi-

tion to life insurance.

8-4

8-5

Discuss some benefits of life insurance in addition to protecting family

members financially after the primary wage earner’s death.

Explain the circumstances under which a single college graduate would or

would not need life insurance. What life-cycle events would change this initial

evaluation, and how might they affect his or her life insurance needs?

EPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHECK • CONCEPT CHEC

Concept Check

22865_08_c08_p239-271.qxd 10/5/06 12:55 PM Page 244

expenses can stretch a family budget to the breaking point, include them when you’re

HEC

EXHIBIT 8.1 How Much Life Insurance Do You Need?

The needs analysis method uses three steps to estimate life insurance needs.

equalsminus

Step 2:

Determine what

financial resources will

be available after death

Step 1:

Assess your family’s

total economic needs

Step 3:

Amount of additional

life insurance required

to protect your family

Income needed to

maintain an

adequate lifestyle

Extra expenses if the

income producer dies

Special needs of

dependents

Debt liquidation

Liquidity

Savings and invest-

ments Income from

Social Security survivor

benefits; surviving

spouse’s annual

income; other annual

pensions and profit

sharing programs.

Other life insurance

Other resources.

22865_08_c08_p239-271.qxd 10/5/06 12:55 PM Page 245