Exam

Name___________________________________

TRUE/FALSE. Write ‘T’ if the statement is true and ‘F’ if the statement is false.

1)

Conceptually, liabilities constitute a present obligation as a result of a past event and

entail an expected future sacrifice of assets or services.

1)

2)

Under ASPE, only legal obligations are recognized.

2)

3)

A reasonable expectation on the part of a company‘s stakeholders arising from a

company‘s past practices or behaviour may constitute a constructive obligation in certain

instances.

3)

4)

A contingency may become a provision if the likelihood of the contingent event greatly

increases.

4)

5)

Under IFRS, most financial liabilities are valued at Fair Value.

5)

6)

An improvement to a company‘s credit rating under IFRS will lead to a reduction in the

carrying amount of any financial liabilities and a gain being reported in OCI.

6)

7)

Loan guarantees are only recorded if they are likely to be paid.

7)

8)

Accrued liabilities made due to routine operating expenses are not normally discounted.

8)

9)

For a small population, the best estimate for the amount of a provision that must be

recognized is the expected value of the possible outcomes.

9)

10)

Under IFRS, provisions are always recorded at their expected value.

10)

11)

For a large population, the best estimate for the amount of a provision that must be

recognized is the most likely outcome with respect to the expected value and cumulative

probabilities.

11)

12)

Under ASPE, contingent liabilities which are more likely than not, are accrued at the

lowest end of the range.

12)

13)

Contingent assets may be recorded under ASPE but not under IFRS.

13)

14)

Executory contracts seldom require a journal entry, while onerous contracts do.

14)

15)

Discounting is not required when the time value of money is immaterial or if the amount

and timing of cash flows is highly uncertain.

15)

1

16)

Financial liabilities are initially recognized at fair value and at cost, amortized cost or fair

value post-acquisition.

16)

17)

A company decides to relocate a group from a discontinued business segment to a

division with ongoing operations. The expenses incurred in doing so would qualify as a

restructuring charge.

17)

18)

Under the warranty expense approach, there should be no income statement effects for

warranty repairs performed after the year of sale (assuming that accrued warranty

expenses and expenditures equal one another).

18)

19)

Under the warranty revenue approach, there should be no income statement effects for

warranty repairs performed after the year of sale (assuming that accrued warranty

expenses and expenditures equal one another).

19)

20)

An onerous contract is one where the unavoidable costs of meeting the contract may or

may not exceed the benefits derived from the contract.

20)

21)

A lawsuit in progress wherein the defendant will probably be found guilty would likely

be accounted for as a provision.

21)

22)

Warranties provisions may arise from legal or constructive obligations.

22)

23)

Once a company has formally decided to restructure its operations, a provision must be

made for the restructuring.

23)

24)

Loyalty points are provided (accrued) for and reversed once the points are redeemed.

24)

25)

Self-insurance costs for expected losses must never be provided for.

25)

26)

Current liabilities are usually discounted.

26)

27)

A decline in value of a company‘s reporting currency relative to the foreign currency in

which it has payables will result in a foreign exchange gain on the reporting company‘s

books.

27)

28)

Adjustments to fair value relating to FVTPL liabilities will always flow through

earnings.

28)

29)

Loan guarantees must be provided for; the amount of the provision is the probability of

payout multiplied by the fair value of the loan guarantee.

29)

30)

A company may reclassify a current financial liability to a long-term one only if there is

a contractual agreement in place by the reporting date to replace the financing.

30)

2

31)

Debt issue costs may be expensed or included in the cost of the debt.

31)

32)

Normal business risks that are insured must be provided for.

32)

33)

An administrative fee pertaining to an unsuccessful loan application is to be immediately

expensed.

33)

34)

Capitalization of borrowing costs on qualifying assets will continue even if work on the

asset has temporarily ceased.

34)

35)

Accounts payable should include only obligations directly related to the primary and

continuing operations of an entity.

35)

36)

Capitalization of borrowing costs on qualifying assets is mandatory under both IFRS and

ASPE.

36)

37)

Under IFRS, a loss contingency must be credited to a liability account only if the

occurrence of the contingent event is probable and if the amount of loss can be

reasonably estimated.

37)

38)

A gain contingency will usually not be recorded in the accounts and reported in the

financial statements even though its occurrence is probable.

38)

39)

Under ASPE, disclosure in the footnotes to the financial statements is the only way to

properly report contingent losses.

39)

40)

Under IFRS, a continuity schedule must be provided for both provisions and

contingencies.

40)

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

41)

A brewing company operating in an Ontario city experiencing water shortages received

its water bill for December 2013, on December 31, 2013. The bill ($8,000) represents the

cost of water used in December to make its product. The company will not publish the

2013 financial statements until February 2014. Therefore, the adjusting entry as of

December 31, 2013 includes which of the following?

A)

cr. utilities payable $8,000

B)

cr. cash $8,000

C)

cr. utilities expense $8,000

D)

no adjusting entry needed because the bill will not be paid until January 2014

41)

3

42)

A short-term note payable may include all of the following except:

A)

Trade notes payable.

B)

Non trade notes payable.

C)

A current portion of a long-term liability.

D)

Unearned revenue.

42)

43)

Which of the following statements is correct?

A)

Under IFRS, contingencies may be accrued, but not under ASPE.

B)

Litigation for which the company will probably be found guilty would normally be

accrued as a provision.

C)

Under IFRS, content gains should be recognized if they are reasonably certain to

occur.

D)

A contingency is more likely to require an accrual than a provision.

43)

44)

A firm sold $100,000 worth of goods during 2014. The firm extends warranty coverage

on these goods. Historically, warranty costs have averaged 2% of total sales. During

2014, the firm incurred $1,000 to service goods sold in 2013 and $200 to service goods

sold in 2014. What is warranty expense for 2014?

A)

$200

B)

$1,200

C)

$2,000

D)

$3,200

44)

45)

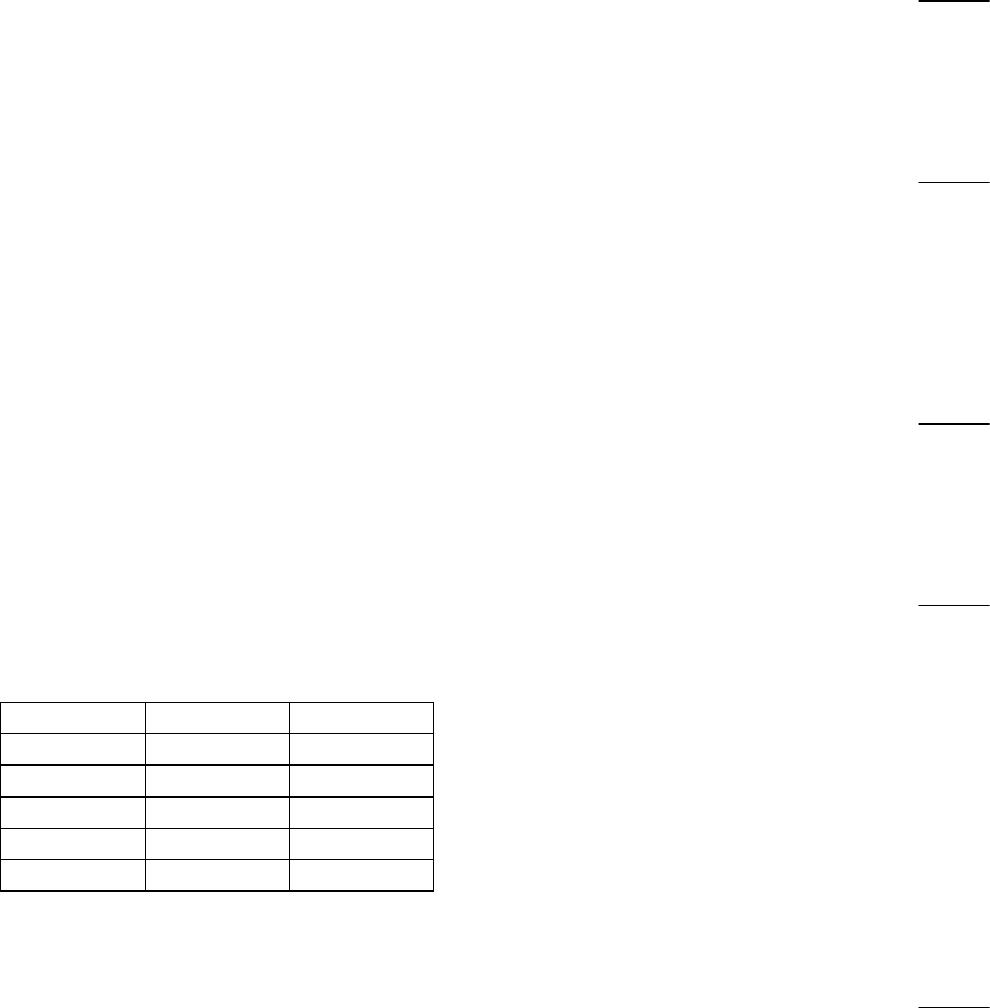

You are an investor and have just purchased a bond on July 1 which pays interest every

March 1 and September 1. When you receive your first interest cheque, you will receive

and have earned how many months interest?

Received Earned

1 6 6

2 6 2

3 2 2

4 4 4

5 6 4

A)

Choice 1

B)

Choice 2

C)

Choice 3

D)

Choice 4

E)

Choice 5

45)

46)

On November 7, 2014 local residents sued Brimley Corporation for excess chemical

emissions that caused some of them to seek medical attention. The total lawsuit is

$8,000,000. Brimley Corporation’s lawyers believe that the lawsuit will be successful

and that the amount to be paid to the residents will be $4,000,000. On its December 31,

2014 financial statements Brimley should:

A)

Accrue a provision loss of $8,000,000 with no financial statement disclosure

necessary.

B)

Accrue a provision loss of $4,000,000 and note disclose.

C)

Do nothing as the lawsuit has not yet ended.

D)

Simply disclose the details regarding the lawsuit in a note.

46)

4

47)

ABC Inc. has 50 pending lawsuits for which it may be found liable. The expected value

(sum of the probabilities of the outcomes multiplied by their respective payouts) amounts

to $100,000. However, the company‘s controller believes that the most likely outcome

will be a payout of $120,000. Which of the following statements pertaining to the accrual

of the provision is correct?

A)

There is a large population of lawsuits, so a provision of $100,000 must be accrued.

B)

There is a large population of lawsuits, so a provision of $120,000 must be accrued.

C)

There is a small population of lawsuits, so a provision of $100,000 must be accrued.

D)

There is a small population of lawsuits, so a provision of $120,000 must be accrued.

47)

48)

Which one of the following items is not a liability?

A)

Accrued estimated warranty costs

B)

Dividends payable in shares

C)

Advances from customers on contracts

D)

The portion of long-term debt due within one year

48)

49)

A company has commenced work on a non-cancellable fixed price construction contract

49)

A)