Chapter 4: Installment Sales

Revenues from Instalment sales can be recognized based on one of the following methods:

1) Recognizing revenues in full on the day of the sale.

2) Recognising revenues based on collected installments.

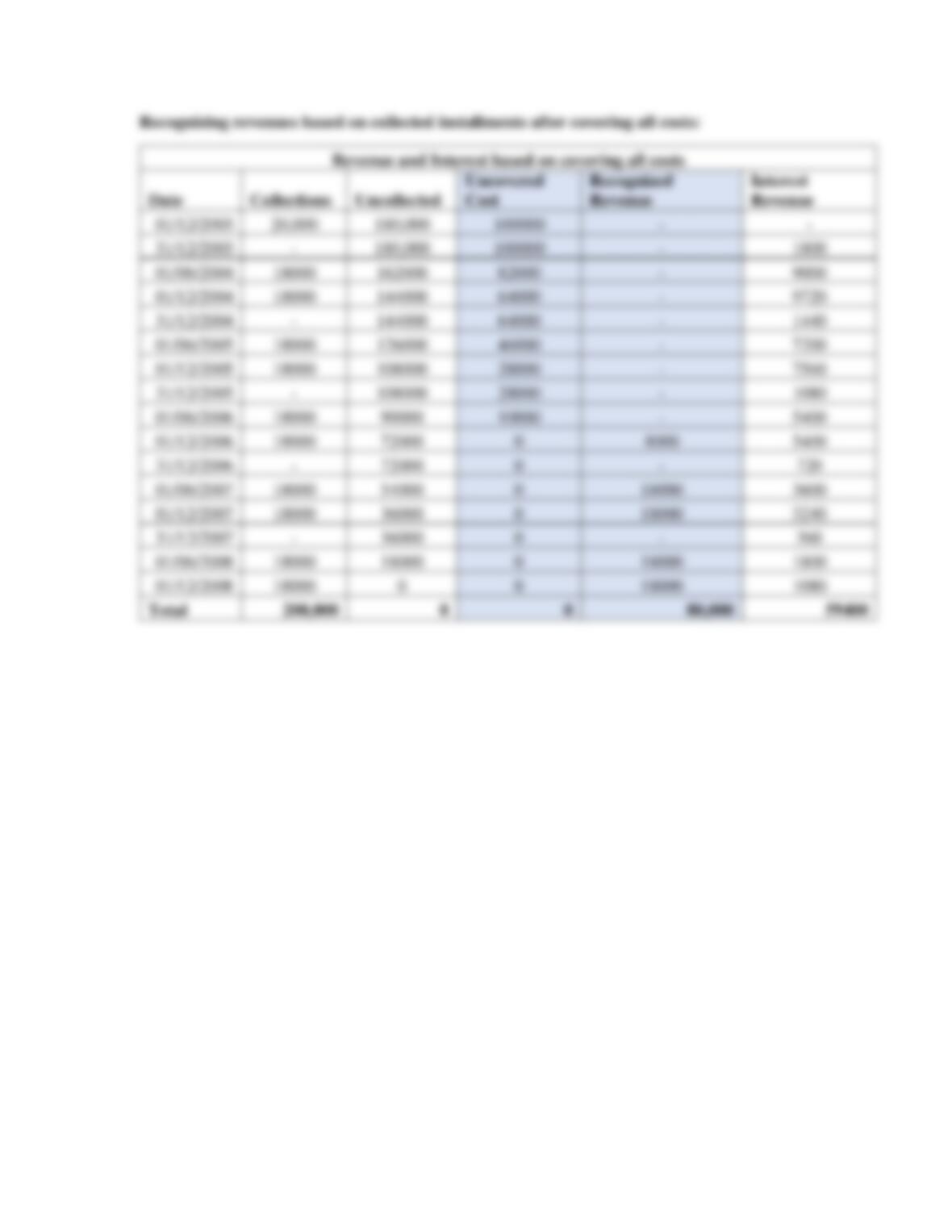

3) Recognizing revenues based on collected installments after covering all costs.

4) Recognizing revenues in full on the day of the last installment.

Example 1:

In 1/12/2008 EuroPlanes sold 520,000 to Petra Retails. Petra paid 120,000 in cash. And the

remaining balance on ten semi-annual installments. Annual intrest on uncollected amounts is

10%. Cost of sale 320,000.

Recognized Revenue = (Collections / Contract price) * Total profit

Total contract price = 520,000

Cost of sales = 320,000

Total Profit (Revenue) = 520,000 – 320,000 = 200,000

Interest Revenue = Uncollected before current collection * Interest Rate * Period

• Recognising revenues based on collected installments:

Revenue and Interest based on installments

Date

Collectio

ns

Uncollected

Recognized Revenue

Interest Revenue

01/12/200

8

120,000

520,000-

120,000=

400,000

(120,000/520,000*200,00

0)=

46,153.8

–

31/12/200

8

0

400,000

–

10%*400,000*1/1

2=

3,333.33

01/06/200

9

40,000

360,000

(40,000/520,000*200,000)

=

15,384.6

10%*400,000*5/1

2=

16,666.67

01/12/200

9

40,000

320,000

(40,000/520,000*200,000)

=

15,384.6

10%*360,000*6/1

2=

18,000

31/12/200

9

0

320,000

–

10%*320,000*1/1

2=

2,666.67

01/06/201

0

40,000

280,000

(40,000/520,000*200,000)

=

15,384.6

10%*320,000*5/1

2=

13,333.33

01/12/201

0

40,000

240,000

(40,000/520,000*200,000)

=

15,384.6

10%*280,000*6/1

2=

14,000

31/12/201

0

0

240,000

–

10%*240,000*1/1

2=

2,000

01/06/201

1

40,000

200,000

(40,000/520,000*200,000)

=

15,384.6

10%*240,000*5/12

=

10,000

01/12/201

1

40,000

160,000

(40,000/520,000*200,000)

=

15,384.6

10%*200,000*6/1

2=

10,000

31/12/201

1

0

160,000

–

10%*160,000*1/1

2=

1,333.33

01/06/201

2

40,000

120,000

(40,000/520,000*200,000)

=

15,384.6

10%*160,000*5/1

2=

6,666.67

01/12/201

2

40,000

80,000

(40,000/520,000*200,000)

=

15,384.6

10%*120,000*6/1

2=

6,000

31/12/201

2

0

80,000

–

10%*80,000*1/12

=

666.67

3

40,000

40,000

15,384.6

3,333.33

01/12/201

3

40,000

0

(40,000/520,000*200,000)

=

15,384.6

10%*40,000*6/12

=

2000