LEARNING OBJECTIVE1Describe management’s decision–

making process and incremental analysis.

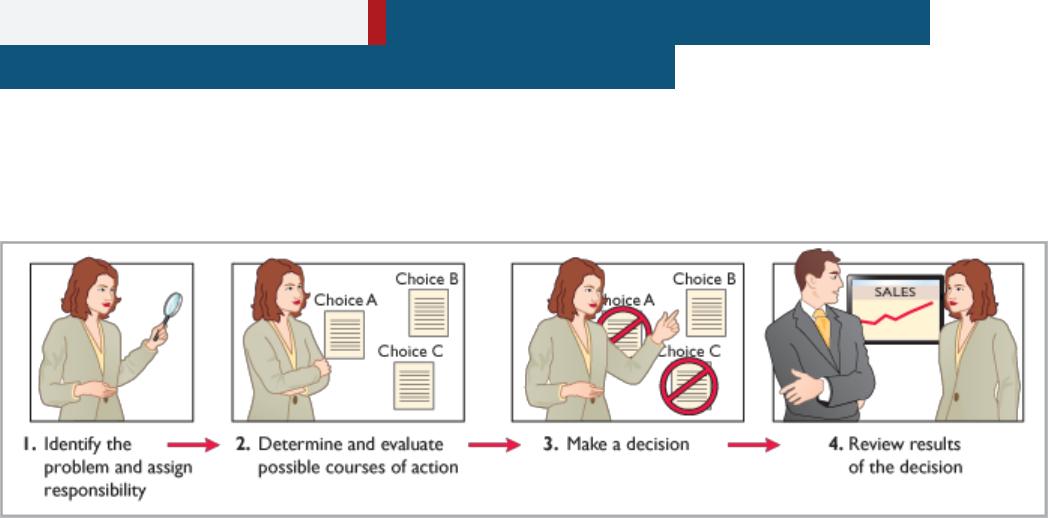

Making decisions is an important management function. Management’s decision-making

process does not always follow a set pattern because decisions vary significantly in their

scope, urgency, and importance. It is possible, though, to identify some steps that are

frequently involved in the process. These steps are shown in Illustration 21-1.

Illustration 21-1 Management’s decision-making process

Accounting’s contribution to the decision-making process occurs primarily in Steps 2 and

4—evaluating possible courses of action and reviewing results. In Step 2, for each possible

course of action, relevant revenue and cost data are provided. These show the expected

overall effect on net income. In Step 4, internal reports are prepared that review the actual

impact of the decision.

In making business decisions, management ordinarily considers both financial and

nonfinancial information. Financial information is related to revenues and costs and their

effect on the company’s overall profitability. Nonfinancial information relates to such

factors as the effect of the decision on employee turnover, the environment, or the overall

image of the company in the community. (These are considerations that we touched on in

our Chapter 15 discussion of corporate social responsibility.) Although nonfinancial

information can be as important as financial information, we will focus primarily on

financial information that is relevant to the decision.

Incremental Analysis Approach

Decisions involve a choice among alternative courses of action. Suppose you face the

personal financial decision of whether to purchase or lease a car. The financial data relate

to the cost of leasing versus the cost of purchasing. For example, leasing involves periodic

lease payments; purchasing requires “up–front” payment of the purchase price. In other

words, the financial information relevant to the decision are the data that vary in the future

among the possible alternatives. The process used to identify the financial data that change

under alternative courses of action is called incremental analysis. In some cases, you will

find that when you use incremental analysis, both costs and revenues vary. In other cases,

only costs or revenues vary.

Just as your decision to buy or lease a car affects your future financial situation, similar

decisions, on a larger scale, affect a company’s future. Incremental analysis identifies the

probable effects of those decisions on future earnings. Such analysis inevitably involves

estimates and uncertainty. Gathering data for incremental analyses may involve market

analysts, engineers, and accountants. In quantifying the data, the accountant must produce

the most reliable information available.

Alternative Terminology

Incremental analysis is also called differential analysis because the analysis focuses on

differences.

How Incremental Analysis Works

The basic approach in incremental analysis is illustrated in the following example.

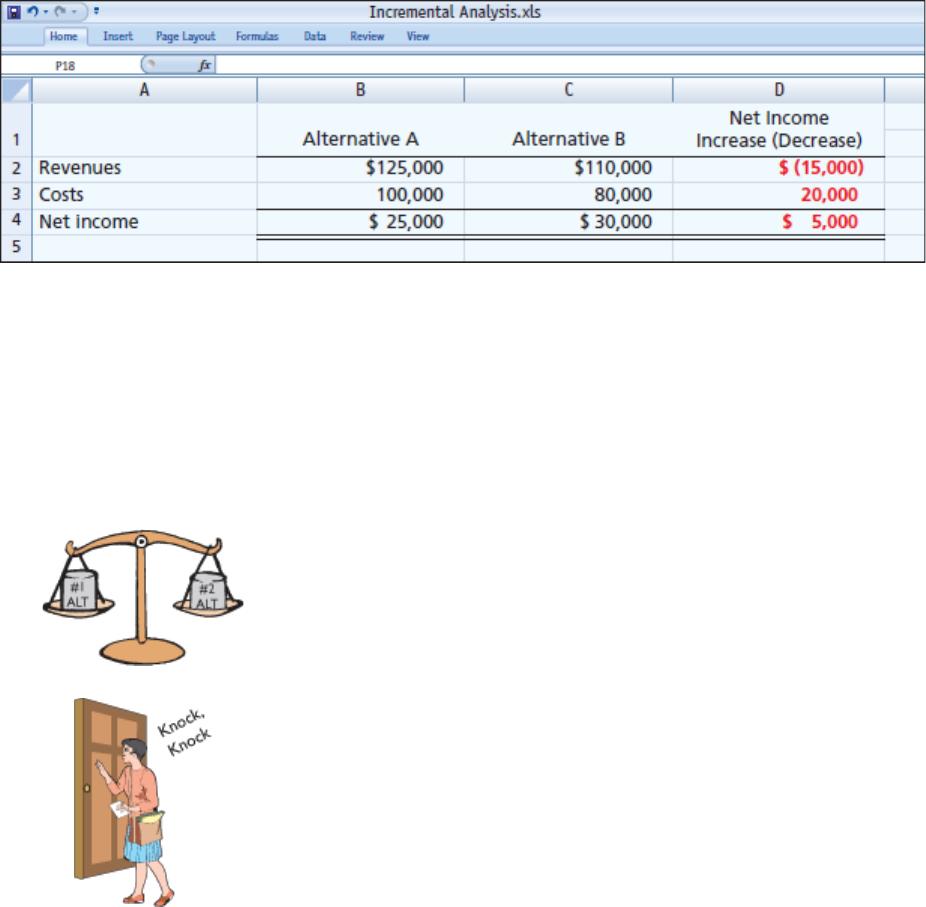

Illustration 21-2 Basic approach in incremental analysis

This example compares Alternative B with Alternative A. The net income column shows the

differences between the alternatives. In this case, incremental revenue will be $15,000 less

under Alternative B than under Alternative A. But a $20,000 incremental cost savings will

be realized.1Although income taxes are sometimes important in incremental analysis, they

are ignored in the chapter for simplicity’s sake. Thus, Alternative B will produce $5,000

more net income than Alternative A.

In the following pages, you will encounter three important cost concepts used in

incremental analysis, as defined and discussed in Illustration 21-3.

Illustration 21-3 Key cost concepts in incremental analysis

• Relevant cost In incremental analysis, the only factors

to be considered are those costs and revenues that differ

across alternatives. Those factors are called relevant

costs. Costs and revenues that do not differ across

alternatives can be ignored when trying to choose

between alternatives.

• Opportunity cost Often in choosing one course of

action, the company must give up the opportunity to

benefit from some other cource of action. For example, if

a machine is used to make one type of product, the

benefit of making another type of product with that

machine is lost. This lost benefit is reffered to

as opportunity cost.

• Sunk cost Costs that have already been incurred and

will not be changed or avoided by any present or future

decisions are referred to as sunk costs. For example, the

amount you spent in the past to purchase or repair a

laptop should have no bearing on your decision whether

to buy a new laptop. Sunk costs are not relevant costs.

Incremental analysis sometimes involves changes that at first glance might seem contrary

to your intuition. For example, sometimes variable costs do not change under the

alternative courses of action. Also, sometimes fixed costs do change. For example, direct

labor, normally a variable cost, is not an incremental cost in deciding between two new

factory machines if each asset requires the same amount of direct labor. In contrast, rent

expense, normally a fixed cost, is an incremental cost in a decision whether to continue

occupancy of a building or to purchase or lease a new building.

It is also important to understand that the approaches to incremental analysis

discussed in this chapter do not take into consideration the time value of money.

That is, amounts to be paid or received in future years are not discounted for the cost of

interest. Time value of money is addressed in Chapter 26 and Appendix G.

Service Company InsightAmerican Express

That Letter from AmEx Might Not Be a Bill

No doubt every one of you has received an invitation from a credit card company to open a new

account—some of you have probably received three in one day. But how many of you have received

an offer of $300 to close out your credit card account? American Express decided to offer some of

its customers $300 if they would give back their credit card. You could receive the $300 even if you

hadn’t paid off your balance yet, as long as you agreed to give up your credit card.

Source: Aparajita Saha-Bubna and Lauren Pollock, “AmEx Offers Some Holders $300 to Pay and Leave,” Wall Street Journal

Online (February 23, 2009).

What are the relevant costs that American Express would need to know in order to determine to

whom to make this offer?

Qualitative Factors

In this chapter, we focus primarily on the quantitative factors that affect a decision—those

attributes that can be easily expressed in terms of numbers or dollars. However, many of

the decisions involving incremental analysis have important qualitative features. Though

not easily measured, they should not be ignored.

Consider, for example, the potential effects of the make-or-buy decision or of the decision

to eliminate a line of business on existing employees and the community in which the plant

is located. The cost savings that may be obtained from outsourcing or from eliminating a

plant should be weighed against these qualitative attributes. One example would be the

cost of lost morale that might result. Al “Chainsaw” Dunlap was a so–called “turnaround”

artist who went into many companies, identified inefficiencies (using incremental analysis

techniques), and tried to correct these problems to improve corporate profitability. Along

the way, he laid off thousands of employees at numerous companies. As head of Sunbeam,

it was Al Dunlap who lost his job because his Draconian approach failed to improve

Sunbeam’s profitability. It was reported that Sunbeam’s employees openly rejoiced for

days after his departure. Clearly, qualitative factors can matter.

Relationship of Incremental Analysis and Activity-Based

Costing

In Chapter 18, we noted that many companies have shifted to activity-based costing to

allocate overhead costs to products. The primary reason for using activity-based costing is

that it results in a more accurate allocation of overhead. The concepts presented in this

chapter are completely consistent with the use of activity-based costing. In fact, activity-

based costing results in better identification of relevant costs and, therefore, better

incremental analysis.

Types of Incremental Analysis

A number of different types of decisions involve incremental analysis. The more common types

of decisions are whether to:

1. Accept an order at a special price.

2. Make or buy component parts or finished products.

3. Sell products or process them further.

4. Repair, retain, or replace equipment.

5. Eliminate an unprofitable business segment or product.

We consider each of these types of decisions in the following pages.

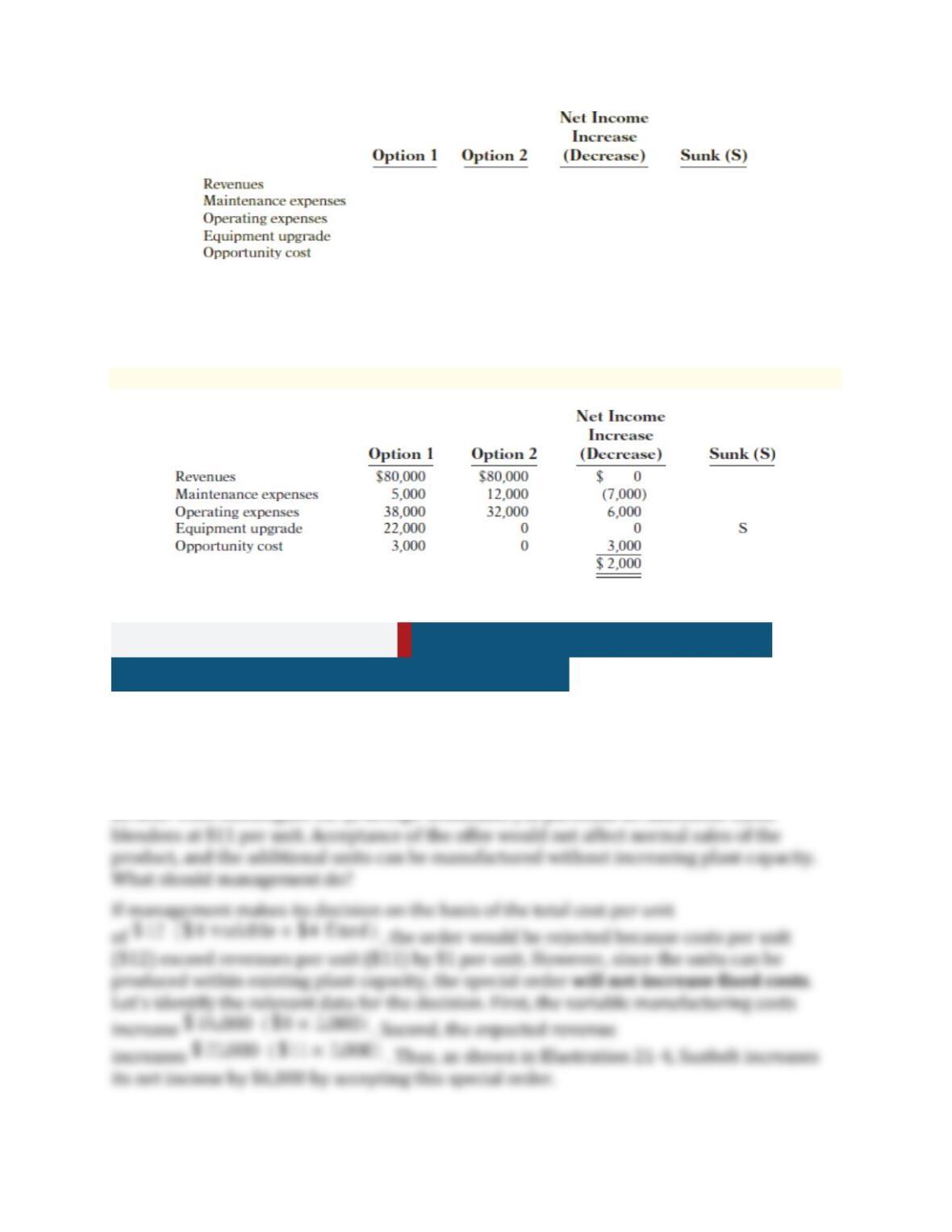

DO IT!1Incremental Analysis

Owen T Corporation is comparing two different options. The company currently follows

Option 1, with revenues of $80,000 per year, maintenance expenses of $5,000 per year, and

operating expenses of $38,000 per year. Option 2 provides revenues of $80,000 per year,

maintenance expenses of $12,000 per year, and operating expenses of $32,000 per year.

Option 1 employs a piece of equipment that was upgraded 2 years ago at a cost of $22,000.

If Option 2 is chosen, it will free up resources that will increase revenues by $3,000.

Complete the following table to show the change in income from choosing Option 2 versus

Option 1. Designate any sunk costs with an “S.”

Action Plan

• ✓Past costs that cannot be changed are sunk costs.

• ✓Benefits lost by choosing one option over another are opportunity costs.

Solution

LEARNING OBJECTIVE2Analyze the relevant costs in

accepting an order at a special price.

Sometimes a company has an opportunity to obtain additional business if it is willing to

make a price concession to a specific customer. To illustrate, assume that Sunbelt Company

produces 100,000 Smoothie blenders per month, which is 80% of plant capacity. Variable

manufacturing costs are $8 per unit. Fixed manufacturing costs are $400,000, or $4 per

unit. The Smoothie blenders are normally sold directly to retailers at $20 each. Sunbelt has