3

Managing Income Tax Compliance through

Self-Assessment

Andrew Okello

March 2014

WP/14/41

© 2014 International Monetary Fund WP/14/41

IMF Working Paper

Managing Income Tax Compliance through Self-Assessment

Prepared by Andrew Okello

Authorized for distribution by Katherine Baer

March 2014

Abstract

Modern tax administrations seek to optimize tax collections while minimizing administration

costs and taxpayer compliance costs. Experience shows that voluntary compliance is best

achieved through a system of self-assessment. Many tax administrations have introduced

self-assessment principles in the income tax law but the legal authority is not being

consistently applied. They continue to rely heavily on “desk” auditing a majority of tax

returns, while risk management practices remain largely underdeveloped and/or

underutilized. There is also plenty of opportunity in many countries to enhance the design

and delivery of client-focused taxpayer service programs, and better engage with the private

sector and other stakeholders.

JEL Classification Numbers: H20, H24, H25

Keywords: income tax, tax compliance, self-assessment, risk management, Sub-Saharan

Africa

Author’s E-Mail Address: aokello@imf.org

This Working Paper should not be reported as representing the views of the IMF.

The views expressed in this Working Paper are those of the author(s) and do not necessarily

represent those of the IMF or IMF policy. Working Papers describe research in progress by the

author(s) and are published to elicit comments and to further debate.

2

Contents Page

Foreword ……………………………………………………………………………………………………………………4

I. Introduction and General Overview ……………………………………………………………………………5

A. Economic and Fiscal Context ………………………………………………………………………..5

II. Approaches to Income Tax Assessment……………………………………………………………………..9

A. Administrative Assessment System ………………………………………………………………..9

B. Self-assessment Implementation …………………………………………………………………..11

III. Status of Implementing Conditions for Effective Self-assessment………………………………16

A. Clear and Simple Tax Laws …………………………………………………………………………17

B. Service to Taxpayers …………………………………………………………………………………..19

D. Effective Collections Enforcement ……………………………………………………………….26

E. Risk-based Audit ………………………………………………………………………………………..28

F. Effective Interest and Penalty Regimes ………………………………………………………….31

G. Fair and Transparent Dispute Resolution Processes ………………………………………..32

IV. Lessons and Concluding Remarks ………………………………………………………………………….33

References ………………………………………………………………………………………………………………..36

Tables

1. Productivity indicators for the CIT and PIT (2011/12) …………………………………………………7

2. Selected MDGs indicators for selected SSA countries. …………………………………………………8

3. Self-assessment implementation in the ten SSA countries …………………………………………..12

4. Aspects of the taxpayer service function …………………………………………………………………..20

5. Common observations on TPS delivery methods. ………………………………………………………23

6. Assessment of the filing and payment function ………………………………………………………….24

7. Key features of current collection enforcement practices. ……………………………………………27

8. Key features of the current audit programs. ……………………………………………………………….29

9. Features of current interest and penalty regimes. ……………………………………………………….31

10. Dispute resolution procedures in the ten countries. …………………………………………………..32

Figures

1. Overall primary balance, excluding grants, 2002 to 2011 ……………………………………………..5

2. Tax revenue, 2001 to 2012………………………………………………………………………………………..6

3. Paying taxes ranking (out of 185 countries) ………………………………………………………………..7

3

Boxes

1. Key features of the administrative assessment system ………………………………………………….9

2. Conditions for a successful self-assessment system ……………………………………………………16

3. Modernizing taxation laws to support full income tax self-assessment …………………………18

4. Elements of a taxpayer service strategy …………………………………………………………………….21

5. Typical taxpayer service program …………………………………………………………………………….22

6. Write-off of irrecoverable tax arrears ……………………………………………………………………….28

4

FOREWORD

Modern tax administrations seek to optimize tax collections while minimizing

administration costs and taxpayer compliance costs. The most cost effective systems of

collecting taxes are those that induce the vast majority of taxpayers to meet their tax

obligations voluntarily, leaving tax officials to concentrate their efforts on those taxpayers

who do not comply. Taxpayers are more likely to comply voluntarily when the tax

administration: (1) adopts a service-oriented attitude toward taxpayers, and educates and

assists them in meeting their obligations; (2) creates strong deterrents to non-compliance

through effective audit programs and consistent use of penalties; and (3) is transparent and

seen by the public to be honest, fair, and even-handed in its administration of the tax laws.

Experience shows that voluntary compliance is best achieved through a system of self-

assessment.

This paper reviews the key issues in income tax compliance and taxpayer self-

assessment1 in 10 SSA countries.2 The objective is to identify common implementation

gaps and challenges, and draw broad lessons for tax administrations that plan to implement,

or are in the process of strengthening income tax compliance through self-assessment. The

findings also have implications for the design of tax administration reform programs and for

technical assistance intended to help these countries better manage income tax compliance

through effective self-assessment systems.3 Overall, the review suggests that all countries

have introduced self-assessment principles in the income tax law but the legal authority is not

being consistently applied. Many countries, though at different stages, continue to rely

heavily on “desk” auditing all or a majority of income tax returns, while risk management

practices remain largely underdeveloped and/or underutilized. Overall, there is plenty of

opportunity in all the countries reviewed to enhance the design and delivery of client-focused

taxpayer service (TPS) programs, change the attitude of tax officials, enhance trust in

taxpayers and engage with the private sector and other stakeholders in a mutually beneficial

manner. Also, much work is still needed to strengthen and implement selective risk based ex-

post controls.

1 While discussions in this paper are limited to income tax administration, the general principles and the key

issues cut across, and are applicable to all taxes, including the VAT, excises taxes, and customs duties.

2 Botswana, Ghana, Kenya, Lesotho, Liberia, Malawi, Nigeria, Rwanda, Tanzania, and Zambia. They are

English-speaking Sub-Sahara African countries representing three geographical blocks (East, West and South)

and are currently at various stages of implementing income tax self-assessment. Some were early adopters of

income tax self-assessment (in the 1990s) while others are still in the early stages of implementation. Further

some have implemented universal self-assessment while others are implementing self-assessment only for

certain types of tax or taxpayers.

3 This is a qualitative study that has been developed through a review of recent FAD technical assistance reports

and IMF and other research on this topic.

5

I. INTRODUCTION AND GENERAL OVERVIEW

A. Economic and Fiscal Context

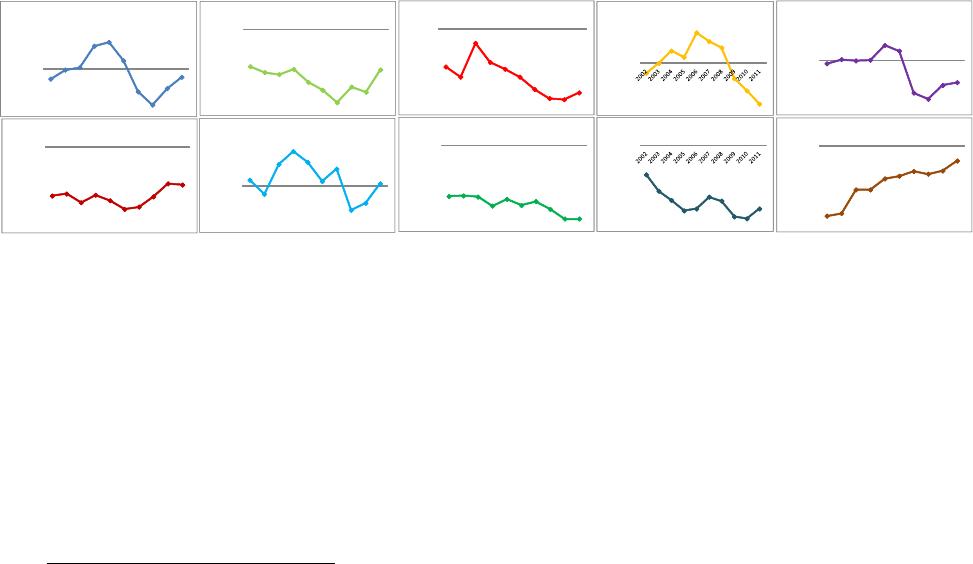

1. The majority of the countries under review face serious fiscal challenges. Although

most SSA countries have rebounded from the Great Recession, many of them have been slow

in rebuilding fiscal positions that weakened during the downturn. Central government

revenue, for example, currently falls short of expenditures by unsustainable margins in most

countries (except Botswana, Nigeria, and Zambia)—Figure 1. A number of these countries

(e.g., Liberia, Malawi, Rwanda, and Tanzania) therefore continue to rely very heavily on

donor financing, which is, by its nature, volatile. Against this backdrop, and assuming that

growth remains robust as envisaged, the policy implication is that fast-growing economies

will be required to rebuild fiscal and external buffers, without unduly affecting key social and

capital spending. Overall, most low-income countries and fragile states need to strengthen

domestic fiscal positions by improving revenue bases, to meet investment needs and avoid

risks from unpredictable aid flows (IMF, REO, 2013).

Figure 1. Overall primary balance, excluding grants, 2002 to 2011

Source: IMF World Economic Outlook (WEO) database

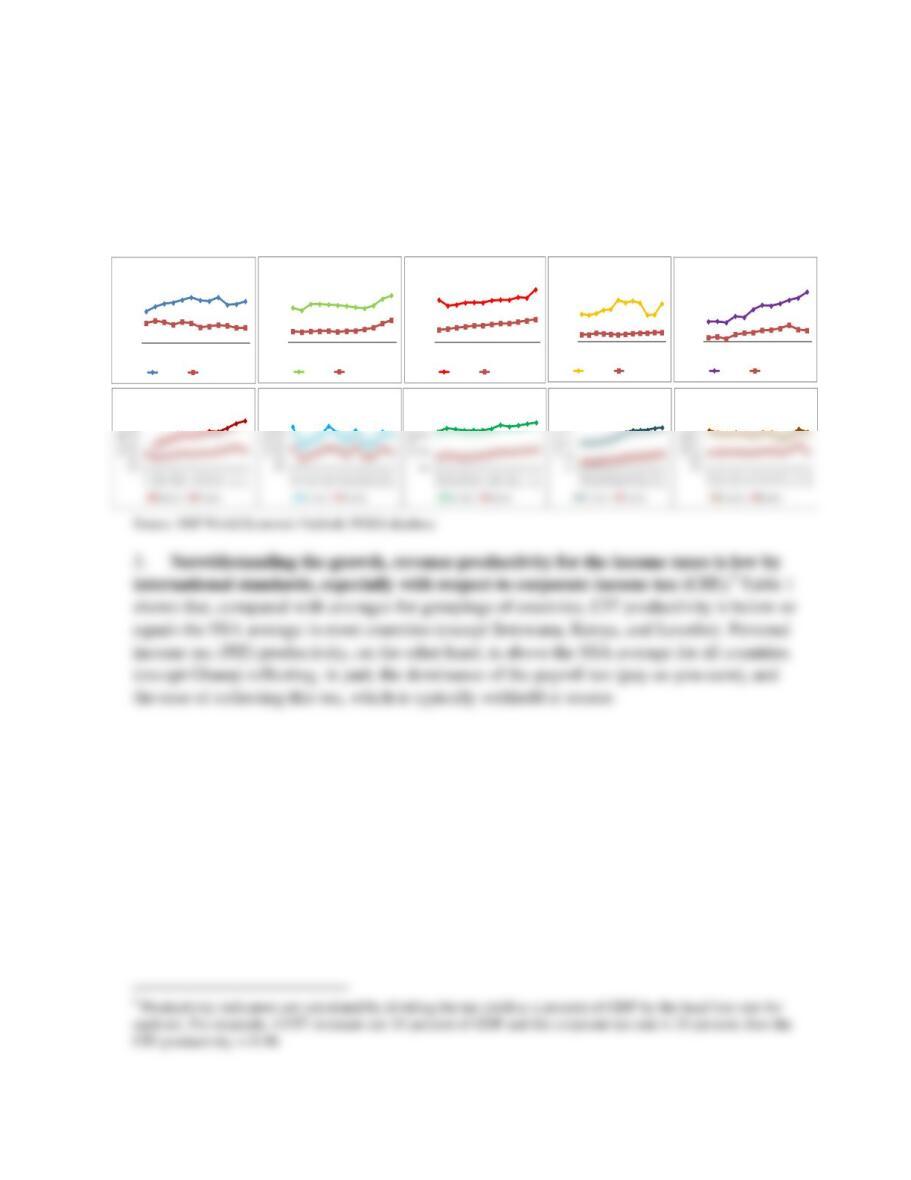

2. Tax revenue is very low compared with international standards. Figure 2 shows

total central government tax revenue performance in the 10 countries. In 9 of the countries

(Lesotho is excluded as it is an outlier),4 total central government tax revenue averaged about

16.9 percent of GDP during the period 2008 to 2010.5 This is relatively weak in comparison

with international standards. During the same period, the comparator figure in advanced

countries (the 32-member countries of the Organization for Economic Cooperation and

Development (OECD) is 25.4 percent (IaDB, 2013)—these countries also collect, on average,

an additional 10 percentage points of GDP in social contributions, bringing their tax-to–GDP

4 Receipts from the South African Customs Union (SACU), a common revenue pool that is allocated to member countries

based upon a formula), account for over 60 percent of total tax revenue in Lesotho.

5 Kenya, Liberia, Malawi, and Tanzania stand out as countries that have successfully strived to increase the tax–to-GDP ratio

over the 10-year period, 2002 to 2011.

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Botswana

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Ghana

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Kenya

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

% of GDP

Lesotho

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Liberia

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Malawi

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Nigeria

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Rwanda

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

% of GDP

Tanzania

-15.0%

-10.0%

-5.0%

0.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

% of GDP

Zambia

6

ratio to about 35 percent. Income tax is an important source of government revenue but there

is still much potential from this source. It currently accounts for over 7 percent of GDP in

seven countries as indicated in Figure 2. It has also been consistently on a growth trajectory

in recent years in many of the countries under review.

Figure 2. Tax revenue, 2001 to 2012

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

% of GDP

Botswana

Tax revenue

Income tax

0.0%

5.0%

10.0%

15.0%

20.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

% of GDP

Ghana

Tax revenue

Income tax

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

% of GDP

Kenya

Tax revenue

Income tax

0.0%

20.0%

40.0%

60.0%

80.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

% of GDP

Lesotho

Tax revenue

Income tax

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

% of GDP

Liberia

Tax revenue

Income tax

25.0%

Malawi

25.0%

Nigeria

15.0%

Rwanda

20.0%

Tanzania

25.0%

Zambia