Please see General Disclaimers on the last page of this report.

Current Environment ……………………………………………………………………………….. 1

Industry Profile ………………………………………………………………………………………. 13

Industry Trends ……………………………………………………………………………………… 14

How the Industry Operates ……………………………………………………………………. 23

Key Industry Ratios and Statistics …………………………………………………………. 27

How to Analyze a Homebuilding Company ……………………………………………. 31

Glossary …………………………………………………………………………………………………. 38

Industry References ………………………………………………………………………………. 39

Comparative Company Analysis ……………………………………………………………. 40

This issue updates the one dated July 2013.

The next update of this Survey is scheduled for July 2014.

Industry Surveys

Homebuilding

Michael Souers, Homebuilders Equity Analyst

JANUARY 2014

CONTACTS:

INQUIRIES & CLIENT RELATIONS

800.852.1641

clientrelations@

standardandpoors.com

SALES

877.219.1247

wealth@spcapitaliq.com

MEDIA

Marc Eiger

212.438.1280

marc.eiger@spcapitaliq.com

S&P CAPITAL IQ

55 Water Street

New York, NY 10041

Topics Covered by Industry Surveys

Aeros

p

ace & De

f

ense

Airlines

Alcoholic Beverages & Tobacco

Apparel & Footwear:

Retailers & Brands

Autos & Auto Parts

Banking

Biotechnology

Broadcasting, Cable & Satellite

Chemicals

Communications Equipment

Computers: Commercial Services

Computers: Consumer Services &

the Internet

Computers: Hardware

Computers: Software

Electric Utilities

Environmental & Waste Management

Financial Services: Diversi

f

ie

d

Foods & Nonalcoholic Beverages

Healthcare: Facilities

Healthcare: Life Sciences

Tools & Services

Healthcare: Managed Care

Healthcare: Pharmaceuticals

Healthcare: Products & Supplies

Heavy Equipment & Trucks

Homebuilding

Household Durables

Household Nondurables

Industrial Machinery

Insurance: Life & Health

Insurance: Property-Casualty

Investment Services

Lodging & Gaming

Metals: Industrial

Movies & Entertainment

Natural Gas Distribution

Oil & Gas: Equipment & Services

Oil & Gas: Production & Marketing

Paper & Forest Products

Publishing & Advertising

Real Estate Investment Trusts

Restaurants

Retailing: General

Retailing: Specialty

Semiconductor Equipment

Semiconductors

Supermarkets & Drugstores

Telecommunications: Wireless

Telecommunications: Wireline

Thrifts & Mortgage Finance

Transportation: Commercial

Global Industry Surveys

Airlines: Asia

Autos & Auto Parts: Europe

Banking: Europe

Food Retail: Europe

Foods & Bevera

g

es: Euro

p

e

Media: Europe

Oil & Gas: Europe

Pharmaceuticals: Euro

p

e

Telecommunications: Asia

Telecommunications: Europe

S&P Capital IQ Industry Surveys

55 Water Street, New York, NY 10041

EXECUTIVE EDITOR: EILEEN M. BOSSONG-MARTINES ASSOCIATE EDITOR: CHARLES MACVEIGH STATISTICIAN: SALLY KATHRYN NUTTALL

CLIENT SUPPORT: 1-800-523-4534.

VISIT THE S&P CAPITAL IQ WEBSITE: www.spcapitaliq.com

S&P CAPITAL IQ INDUSTRY SURVEYS (ISSN 0196-4666) is published weekly. Redistribution or reproduction in whole or in part (including inputting into a

computer) is prohibited without written permission. To learn more about Industry Surveys and the S&P Capital IQ product offering, please contact our Product

Specialist team at 1-877-219-1247 or visit getmarketscope.com. Executive and Editorial Office: S&P Capital IQ, 55 Water Street, New York, NY 10041. Officers of

McGraw Hill Financial: Douglas L. Peterson, President, and CEO; Jack F. Callahan, Jr., Executive Vice President, Chief Financial Officer; John Berisford, Executive

Vice President, Human Resources; D. Edward Smyth, Executive Vice President, Corporate Affairs; Charles L. Teschner, Jr., Executive Vice President, Global

Strategy; and Kenneth M. Vittor, Executive Vice President and General Counsel. Information has been obtained by S&P Capital IQ INDUSTRY SURVEYS from

sources believed to be reliable. However, because of the possibility of human or mechanical error by our sources, INDUSTRY SURVEYS, or others, INDUSTRY

SURVEYS does not guarantee the accuracy, adequacy, or completeness of any information and is not responsible for any errors or omissions or for the results

obtained from the use of such information.

Copyright © 2014 Standard & Poor’s Financial Services LLC, a part of McGraw Hill Financial. All rights reserved.

STANDARD & POOR’S, S&P, S&P 500, S&P MIDCAP 400, S&P SMALLCAP 600, and S&P EUROPE 350 are registered trademarks of Standard & Poor’s Financial

Services LLC. S&P CAPITAL IQ is a trademark of Standard & Poor’s Financial Services LLC.

INDUSTRY SURVEYS HOMEBUILDING / JANUARY 2014 1

CURRENT ENVIRONMENT

Housing on the mend

The US housing market continued its recovery in 2013 after improving sharply in 2012, although it remains

weak when measured against historical averages. While the demand for multifamily homes (mostly used for

rental properties) has continued to lead the recovery, as it has over the past couple of years, demand for

single-family homes also continued to increase after rebounding sharply in 2012. Contributing to this was a

pickup in investment demand for housing, along with a dwindling amount of supply as foreclosures continue

their steady, modest decline. Prices have also continued rising into 2013, and look poised for another strong

yearly gain. That said, through September 2013, prices remained approximately 20% below their June 2006

peak. We expect the housing market to continue its recovery in 2014, but we expect the pace of improvement

to decelerate from 2013 levels. In addition, we think the recovery will be rather choppy.

We think that beyond the normal seasonal pattern for residential sales lie several challenging issues: a tight

lending market; foreclosed homes up for resale; and the hard-to-quantify shadow inventory of both bank-

owned unsold homes and underwater mortgages (i.e., mortgages that exceed their homes’ values) that might

lead to foreclosure or short sale. While we believe the publicly traded homebuilders have strong balance sheets

with ample liquidity, the rapid rise of land prices has many homebuilders remaining hesitant about

aggressively pursuing land acquisitions for new communities without seeing stronger signs of a sustainable

recovery.

Boosted by record affordability levels as a result of the actions taken by the US Federal Reserve to lower

interest rates, the S&P/Case-Shiller US 20-City Composite Home Price Index, which tracks the change in

housing prices of 20 major metropolitan areas, turned positive in June 2012. Year to date through

September 2013, the S&P/Case-Shiller US 20-City Composite Home Price Index was up 13.3% year-over-

year. The US Federal Housing Finance Agency (FHFA), an agency within the US Department of Housing

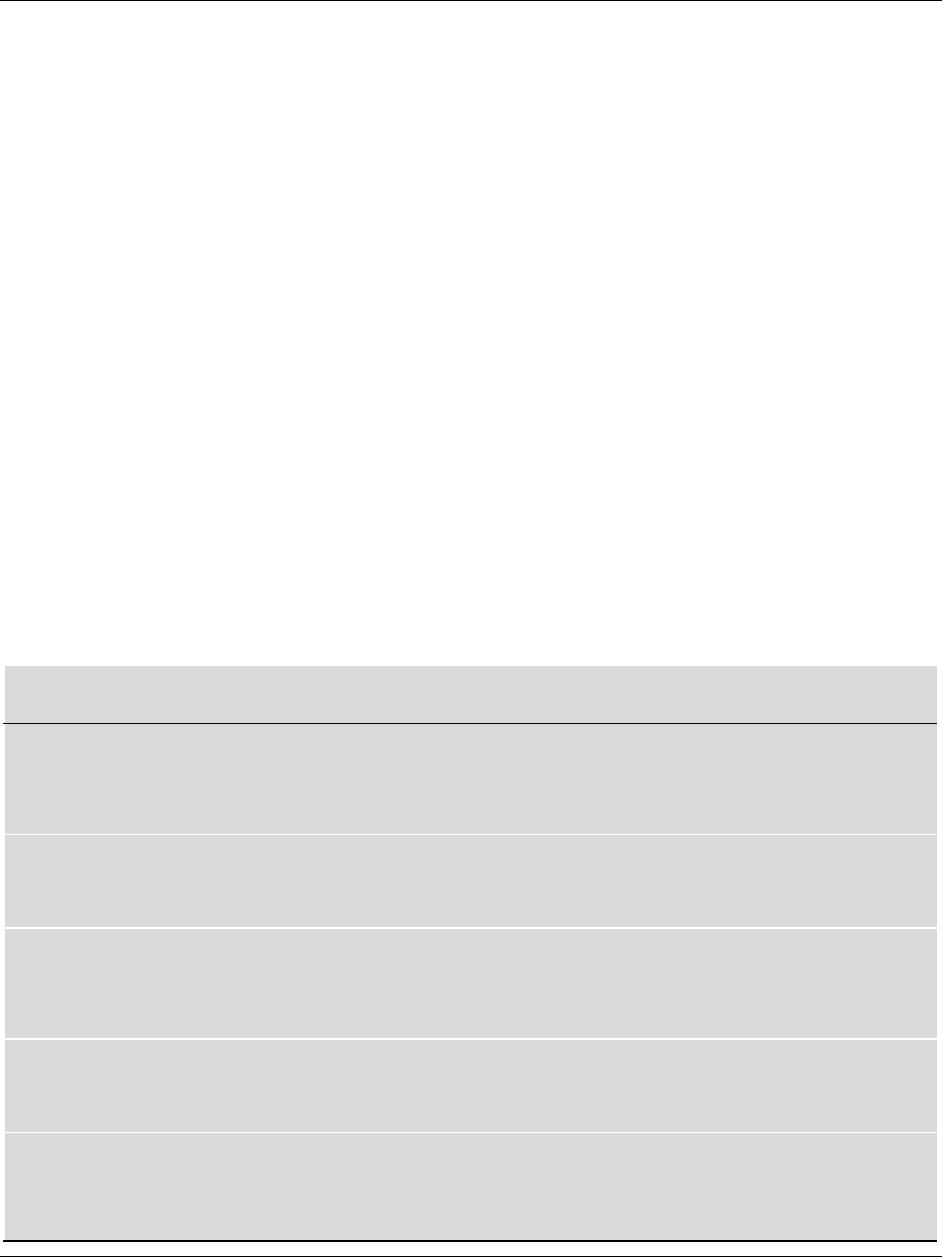

Table B14: MONTHLY

HOUSING INDUSTRY

STATISTICS

M ONT HL Y HOUSING INDUSTRY STATISTICS

—- 2012-13 RANGE —- LATEST

STATISTIC AND SOURCE HIGH LOW READING METHODOLOGY PROBLEMS OR LIMITATIONS

HOUSING STARTS

1,005,000 707,000 Aug. ’13 Seasonally adjusted annual rate. Start The seasonally adjusted annual rate varies

US Census Bureau 891,000 of construction is defined as the beginning sharply from month to month, especially in

US Dept. of Commerce of excavation f or the foundation of the the w inter, w hen actual starts are few er,

Released: Third Tuesday building. Based on a sample of the 17,000 because the multiplication factor is greater.

of follow ing month permit-issuing places in the United States. Excludes mobile homes and conversion

or rehabilitation of existing structures.

BUILDING PERMITS

1,005,000 714,000 Aug. ’13 Seasonally adjusted annual rate. Permits are generally a leading indicator of

US Census Bureau 926,000 Permits are issued in areas covering housing starts. How ever, not all permits are

US Dept. of Commerce approximately 92% of all US housing used, and a long time may elapse betw een

Released: Third Tuesday construction. permit issuance and completion of

of follow ing month construction.

NEW SINGLE– FAMILY

458,000 338,000 Aug. ’13 Seasonally adjusted annual rate. Based on Month-to-month changes are sometimes

HOME SALES

421,000 an estimate of the actual number of new irregular, but less so than for those of

US Census Bureau homes sold during the month. A sale is housing starts and building permits.

US Dept. of Commerce assumed to occur w hen a buyer signs a Excludes mobile home sales. Sales are

Released: 4-5 w eeks contract or makes a deposit. often a leading indicator of future building

after end of month permits and housing starts.

AVG. NEW- HOME PRICE

$337,000 $265,700 Aug. ’13 The prices of homes included in the sample Indicates not only the direction or actual

Fed. Home Loan Bank Bd. $318,900 are totaled and divided by the number of level of home prices, but also the mix of

Released: First Tuesday homes to arrive at a simple average. homes sold. When luxury homes are selling

of follow ing month w ell, it rises quickly; and w hen low er-cost

home sales predominate, it falls sharply.

MEDIAN P RICE

$279,300 $221,700 Aug. ’13 This statistic is derived from a nationw ide This gives a better indication of the

OF A NEW HOME

$254,600 sample of home prices. direction and level of home prices in

US Dept. of Commerc e general. No real “national” home market

Released: 1-month lag exists, how ever; home prices vary

dramatically from one part of the country to

the next.

2 HOMEBUILDING / JANUARY 2014 INDUSTRY SURVEYS

and Urban Development, tracks only the prices of homes backed by mortgages sold or guaranteed by the

Federal National Mortgage Association (Fannie Mae) and Federal Home Loan Mortgage Corp. (Freddie

Mac), and excludes new-home sales. In the third quarter of 2013, the FHFA’s house price index improved

8.4%, year over year, marking the ninth straight quarter of positive changes in home prices after 20 straight

quarterly declines.

MACROECONOMIC CHALLENGES

Despite the fact that the housing market is recovering from recent lows, the US continues to face various

challenges at the macroeconomic level, including high unemployment, significant shadow inventory of

homes, consumers’ limited access to capital from mortgage lenders, and psychological factors.

Unemployment remains high

In October 2013, nonfarm payroll growth accelerated from the previous month, adding 204,000 new jobs

(versus 163,000 in September). However, this pace of job growth is only about what is needed to keep up

with population growth. The private sector added 212,000 new jobs in October 2013, with continued growth

in professional and business services, leisure and hospitality sectors, manufacturing and healthcare services,

and retail trade sectors. Over the past 12 months, payroll growth has averaged 194,000 per month. While

this growth is solid, it is still shy of what would be expected during an economic growth cycle. In our

opinion, a sustained recovery in housing cannot occur without stronger improvement in the labor force.

The unemployment rate increased marginally to 7.3% for October 2013 from 7.2% in the prior month,

largely attributable to the federal government’s partial shutdown. On a year-over-year basis, the

unemployment rate has fallen from the 7.9% rate in October 2012. However, in our view, this decline in

the unemployment rate has much more to do with people completely dropping out of the labor force (about

3.1 million over the past year) than it does with any meaningful improvement in the job market. To better

illustrate this, we note that the labor force participation rate fell to 62.8% in October 2013, the lowest rate

in 35 years (from 63.8% in October 2012), while the employment-to-population ratio dropped to 58.3%

(from 58.7% last October). These ratios are at levels not seen since the early 1980s, when single-income

families were far more prevalent. We think these metrics more accurately reflect the health of the labor force

than does the official U-3 unemployment rate. As of December 2013, Standard & Poor’s Economics (which

operates separately from S&P Capital IQ) was projecting a 7.5% unemployment rate for 2013 after an

8.1% average rate in 2012. For 2014, it expected the unemployment rate to decline to 6.9%.

Recent job growth is not constructive for household formation

We believe the key to a sustainable housing recovery is household formation. Population growth can

certainly help household formation, but is likely to average only 1% annually, the average over the past

decade. Therefore, in our opinion, the key to household formation lies with the labor market, as quality

jobs will give more people the ability to afford new homes.

In terms of job growth, things look fairly good to us on the surface. Since the trough of the labor market in

December 2009, approximately 5.5 million jobs have been created through October 2013. However, as

discussed earlier, though the official unemployment rate has dropped from its October 2009 peak, much of

the improvement has come from people dropping out of the labor force. Making matters worse is that the

quality of jobs has been poor and not conducive to increased household formation.

Some of that weakness is reflected in wage growth, which has averaged only about 2% since late 2009. Of

greater concern is that the jobs created have been part-time jobs, as companies remain reluctant to hire full-

time staff. In fact, nearly 60% of the jobs created since the trough of the labor market pay less than $14 per

hour. Another statistic that we found to be extremely representative of the poor job quality is that all of the

5.5 million jobs created between December 2009 and October 2013 have gone either to workers aged 16–

24 or to those aged 55 and older (there are net 21,000 fewer workers in the 25–54 age range). Given the

makeup of the labor force in this country, with nearly two-thirds of workers in the 25–54 age cohort, the

amount of new job creation in the young and older cohorts is even more peculiar. Regardless of the reasons

behind this, job growth remains weak for the age cohort (25–54) that typically drives new housing demand.

INDUSTRY SURVEYS HOMEBUILDING / JANUARY 2014 3

“Shadow” inventory and foreclosure concerns

The inventory of existing homes for sale in October 2013 declined 1.8% sequentially to 2.13 million, which

represented a 5.0-month supply at the existing sales pace, up from the 4.9-month supply in September,

according to the National Association of Realtors (NAR). The months of supply has fallen considerably

from the 9.5 months reported in June 2011 and has been declining from a recent peak of 11.0 months in

November 2008, a level that hadn’t been seen since 1982’s all-time record of 11.5 months. In each year

from 2000 to 2005, inventories of existing homes for sale averaged less than 5.0 months’ supply. (The

“normal” level is considered to be about six months of supply.) By this measure, it would appear that

supply is extremely constricted and that further house price appreciation is very likely. However, that might

not necessarily be the case.

Despite this decline, the number of months’ supply does not take into account the “shadow” inventory that

banks are holding on their books. [Shadow inventory is defined as real estate owned by banks and mortgage

companies due to foreclosures and other actions (such as deeds in lieu of foreclosure), as well as real estate

that is at least 90 days delinquent.] According to the latest available data from CoreLogic, a market and

business research company, the shadow inventory stood at 1.9 million homes as of July 2013 (which equals

about 3.7 months’ supply). The 1.9 million figure included 874,000 seriously delinquent units and 661,000

in some stage of foreclosure, with the remaining 318,000 units being real estate owned (REO) by lenders.

While the shadow inventory is down 22% from the 2.4 million units in July 2012, it remains approximately

five times the amount of inventory at the peak of the housing bubble in mid-2006. CoreLogic postulates

that shadow inventory of over one month’s supply remains an obstacle to the improving housing markets as

it exerts downward pressure on prices. In addition, if we count homeowners who are 30 days or more

delinquent on their mortgage payment, the numbers rise further. According to Lender Processing Services, a

leading provider of mortgage and consumer loan processing services, 4.4 million mortgages were 30 or

more days delinquent or in foreclosure as of October 2013.

Foreclosures in 2013 continued with the declining trend seen in 2011 and 2012, according to RealtyTrac, a

web-based firm that tracks and markets foreclosed homes. In October 2013, foreclosure filings were reported

on 133,919 properties, a 2% increase from September 2013, but a 28% drop from October 2012. In 2012,

foreclosure filings totaled 2,304,941 on 1,836,634 properties, a 3% decline from filings in 2011, and a 36%

decline from the peak of 2.9 million filings set in 2010. We expect foreclosure activity to flatten out in late

2013 before resuming a gradual decline in 2014, with improving home prices and job growth offsetting

some of the foreclosure backlog in judicial states (as discussed in more detail later in this section).

Lending standards remain tight

The Federal Reserve has tried to provide stimulus to the US housing market by lowering the federal funds

rate to just over 0%, which in turn has helped reduce the 30-year, fixed-rate mortgage rate. However, with

the Federal Reserve hinting that it might taper off its latest quantitative easing program, interest rates have

risen over the past several months. The 30-year, fixed-rate mortgage rose to 4.29% for the week ending

November 27, 2013. This is up from the 3.35% average in December 2012 and from the record low of

3.31% set in November 2012.

While low rates have provided a modest boost in demand from prospective homebuyers, continued tight

bank lending practices have mitigated the effort. While it became common practice in the last decade to

purchase a house with a down payment of 5% or less, banks in today’s environment are often asking

homebuyers for a 20% down payment. In addition, banks are requiring higher Fair Isaac Credit

Organization (FICO) scores in order for prospective homebuyers to qualify for a mortgage.

While current lending standards may be tight compared with the recent housing boom years of the 2000s,

when no-money-down home purchases were rampant (with lenders even allowing prospective homebuyers

with poor credit to do this), we believe credit is still much looser than it was pre-1980, when a 20% down

payment was the standard. We don’t expect more than just minor loosening in bank lending standards in

2013 without some sort of political intervention.

4 HOMEBUILDING / JANUARY 2014 INDUSTRY SURVEYS

Psychological factors

Homebuilders often say that an important building block for a housing recovery is buyers’ confidence.

Confidence has been yo-yoing over the past few years. In 2011, it reached a temporary high of 72.0 in

February, according to the Conference Board’s Consumer Confidence Index (CCI), before dropping to 40.9

in October. Confidence perked up again in early 2012, hitting 71.6 in February, suggesting that consumers

were becoming more positive despite rising gasoline prices. However, the index declined to 61.3 in August

2012. Driven by slight improvement in economic data, the CCI rose to 73.1 in October 2012, its highest

level since February 2008 and a sharp contrast to its year-earlier level. This improvement didn’t last long,

however, as the index declined over the last two months of 2012, ending at 66.7 in December.

Heading into 2013, the index dropped significantly to 58.4 in January, but started to rise over the next

several months, reaching a yearly high of 82.1 in June. Since June, confidence declined all the way back

down to 70.4 in November, which we attribute to concerns related to the labor market, questions

surrounding the implementation of the Affordable Care Act, and disgust with the government following its

recent shutdown. Although the November figure is significantly higher than the historic low posted in

February 2009 (when it stood at 25.3), it still represents confidence levels synonymous with recessions:

consumer confidence averages 71 during recessions and 102 in economic expansions.

In our view, despite some relief from gas prices, worries about federal budget issues, anemic wage growth,

and higher taxes continue to stunt consumer confidence. According to the NAR, the Housing Affordability

Index reached a record high of 193.9 in 2012, up from its earlier record of 186.4 in 2011. Although homes

reached record affordability levels in 2012, we believe buyer confidence remains low, as homeowners have

been scarred by the breadth and depth of the housing market decline. We think the psychological outlook is

gradually improving, but is still an impediment to recovery.

Further, households are nervous at this time, in our view, and they are having trouble paying their existing

or new mortgage. According to CoreLogic, 7.1 million residential properties with a mortgage (around

14.5% of the total) were underwater at the end of the second quarter of 2013—that is, the total owed on

the mortgage exceeds the home’s appraised value. This is lower than the 9.6 million residential properties

with a mortgage (around 19.7% of the total) that were underwater at the end of the first quarter of 2013.

Though the drop in the underwater mortgage numbers is indicative of some progress, Zillow, an online real

estate database, paints an even less sanguine picture: in the third quarter of 2013, it estimated that 21% of

homes—around 10.8 million households—were underwater on their mortgages. Whether the percentage for

underwater mortgages is 15% or 21%, it is still fairly high, and exemplifies the damage that the housing

boom (and subsequent bust) created.

FORECLOSURES CONTINUE TO DECLINE

Foreclosed homes are becoming much less of a drag on housing. Data from RealtyTrac show that

foreclosure starts hit a seven-year low in the third quarter of 2013. According to the firm’s U.S. Foreclosure

Market Report for the third quarter of 2013, there were 376,931 properties with foreclosure filings for

default notices, scheduled auctions, and bank repossessions, down 7% from the second quarter of 2013 and

down nearly 29% from the third quarter of 2012. In its Year-end 2012 U.S. Foreclosure Market Report, the

firm noted that there were 1,836,634 properties with foreclosure filings in 2012, a 3% decrease from 2011,

and nearly a 36% decline from 2010.

However, not all states are showing declines in foreclosures. According to RealtyTrac, foreclosure activity in

the first quarter of 2013 (latest available) increased 6% in all 26 states that use judicial process for foreclosure,

while foreclosure activity dropped 44% in the 24 states that use non-judicial foreclosure process. We think

this is due to the timeline it takes for foreclosures to be completed in judicial states, averaging over three

years from start to completion in states like New York. As a result, we think it will take another year or so

before much of the backlogged foreclosures clear the market in judicial states, while non-judicial states

should continue to see declines in foreclosure activity. In its year-end 2012 report, RealtyTrac noted that it

expected foreclosure activity to pick up in 2013. In line with its expectations, foreclosure activity in judicial

process states increased at the beginning of 2013, as lenders attempted to catch up with backlogs. The firm

also noted that non-judicial process states would likely see an increase towards the end of the year as

lenders process deferred foreclosures.

According to RealtyTrac, Florida reported the highest foreclosure rate (one in every 104 housing units) in

the first quarter of 2013, followed by Nevada (one in every 115 housing units), Illinois (one in every 147),

Ohio (one in every 188), and Georgia (one in every 200). Other states ranked among the nation’s top 10

with the highest foreclosure rates were Arizona (one in every 202), Washington (one in every 220),

Maryland and South Carolina (each with one in every 254), and California (one in every 266).

HOMEBUILDERS MORE AGGRESSIVE IN ACQUIRING LAND, BUT REMAIN RELATIVELY CAUTIOUS

Land acquisition activity is picking up strength among homebuilders, though many remain somewhat

cautious. Most have raised significant cash to get through the housing downturn. They continue to

recalibrate their operations, products, and pricing to contend with weak buyer demand, changing housing

preferences, and competition from foreclosed homes that are being re-marketed for sale. In our opinion,

many of the largest publicly traded homebuilders are ready to take advantage of potential land acquisitions,

although the all-clear sign of a housing market recovery has yet to occur, in our opinion.

We believe that most of the largest publicly traded companies are strong enough from a liquidity standpoint

to rebound in a housing market recovery and gain market share from the smaller private builders that have

limited access to funds (which come mostly from banks that have tightened their lending practices). Some of

these large builders have cash equivalents and unused bank line-of-credit facilities exceeding $1 billion, with

no major debt outstanding maturing in the next year. In our view, homebuilders have been very smart to

reduce debt and extend debt maturities.

The key industry drivers for a housing recovery include an increase in buyers’ confidence, strengthening

demand for new homes, a reduction in oversupply of new and existing homes available for sale, shorter time

periods for homebuyers to sell their current homes, and credit availability for those households that qualify

for home mortgages.