Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1111

HKICPA CODE OF ETHICS FOR

PROFESSIONAL ACCOUNTANTS

(COE)

Preface

Applicability

All members of the HKICPA.

How about a registered student?

YES!!! (signed an undertaking to observe and abide by the

Professional Accounting Ordinance and its By-Laws, and is

thus bound by the ethical requirements of the HKICPA and

subject to disciplinary proceedings)

Apparent failures by members of the Institute to comply with

the COE are liable to be enquired into by the appropriate

committee established under the authority of the Institute, and

disciplinary action may result.

2222

HKICPA CODE OF ETHICS FOR

PROFESSIONAL ACCOUNTANTS

(COE)

Fundamental Principles (Section 100)

Maintain integrity and objectivity.

Meet technical and professional standards when carrying out

professional work.

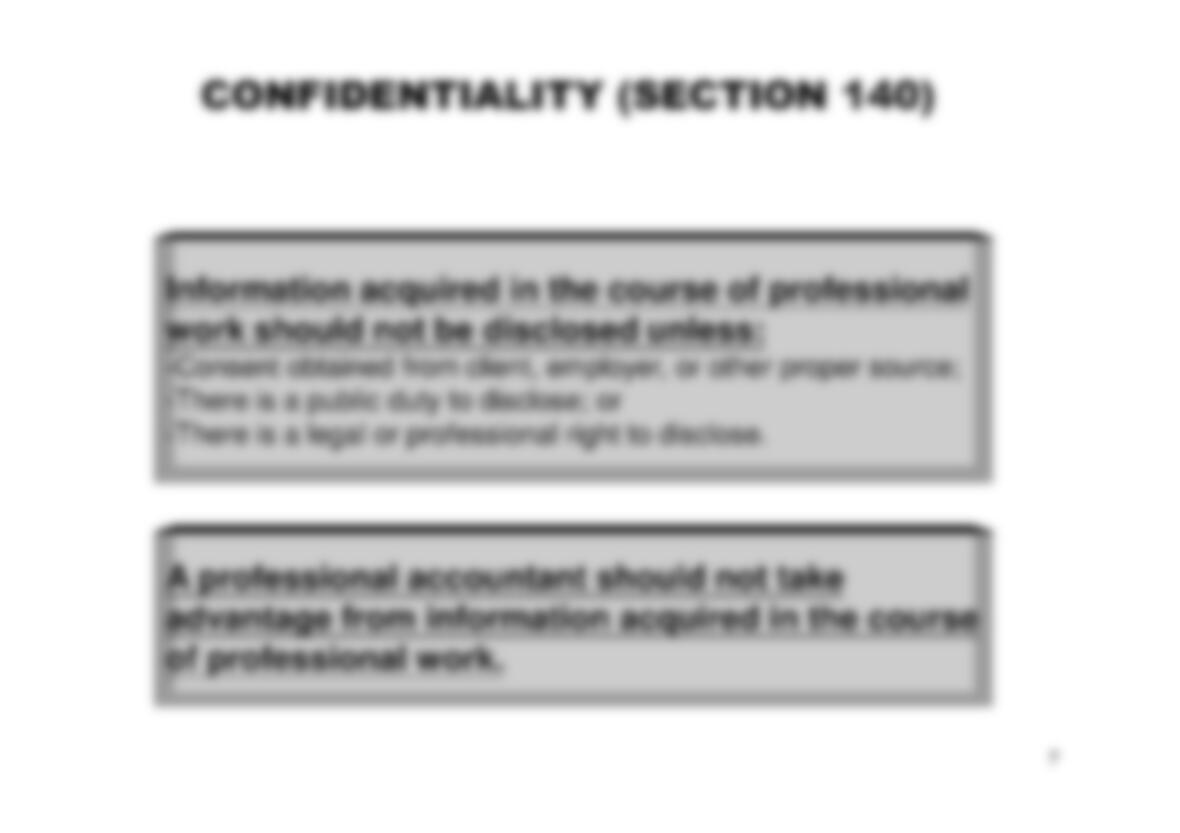

Respect the confidentiality of information acquired.

Follow ethical guidelines issued by the Institute.

3333

HKICPA CODE OF ETHICS FOR

PROFESSIONAL ACCOUNTANTS

(COE)

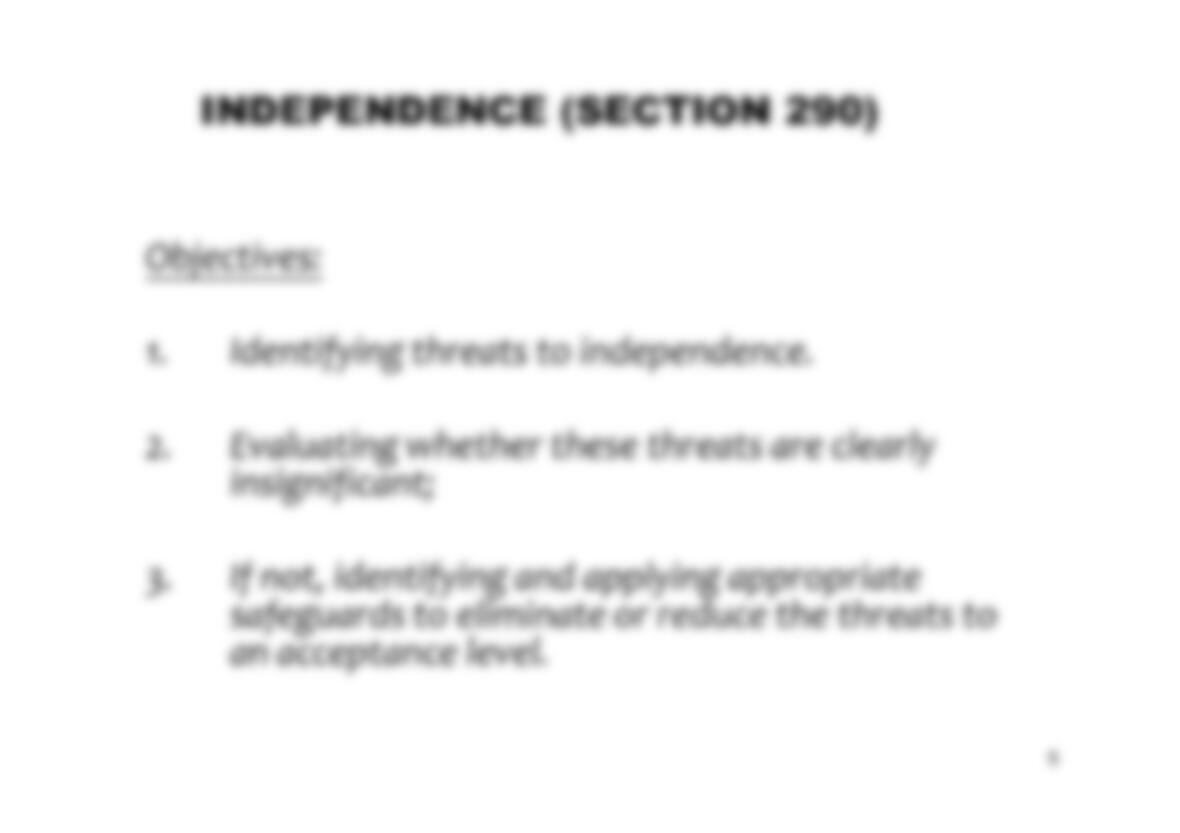

1. Independence (Section 290)

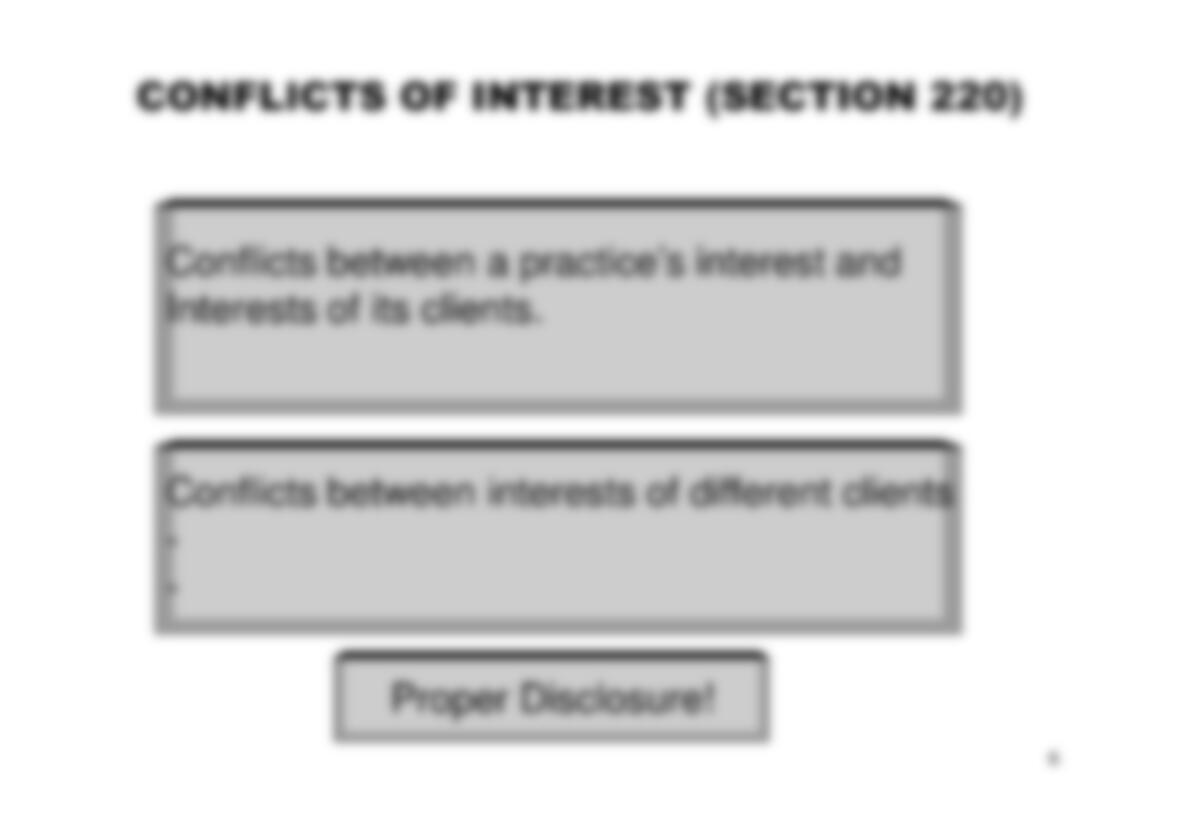

2. Conflicts of Interest (Section 220)

3. Confidentiality (Section 140)

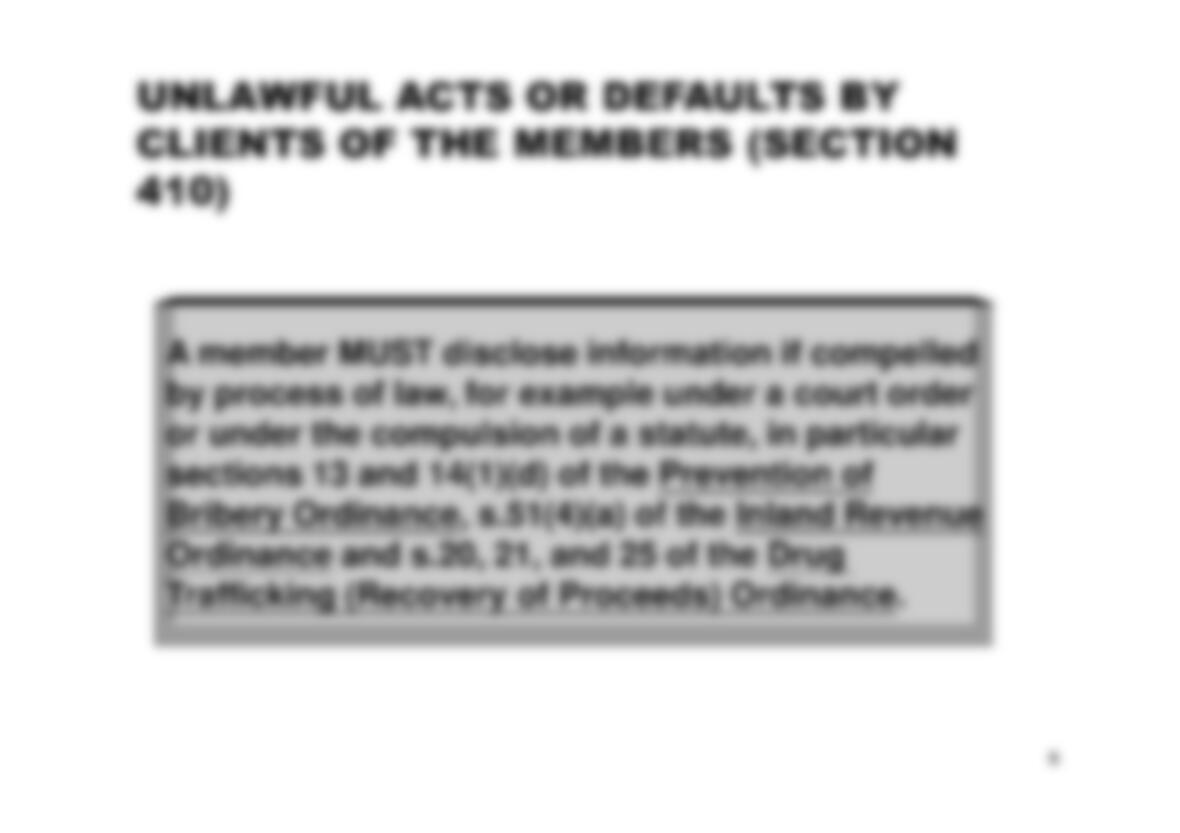

4. Unlawful Acts or Defaults by Clients of Members (Section 410)

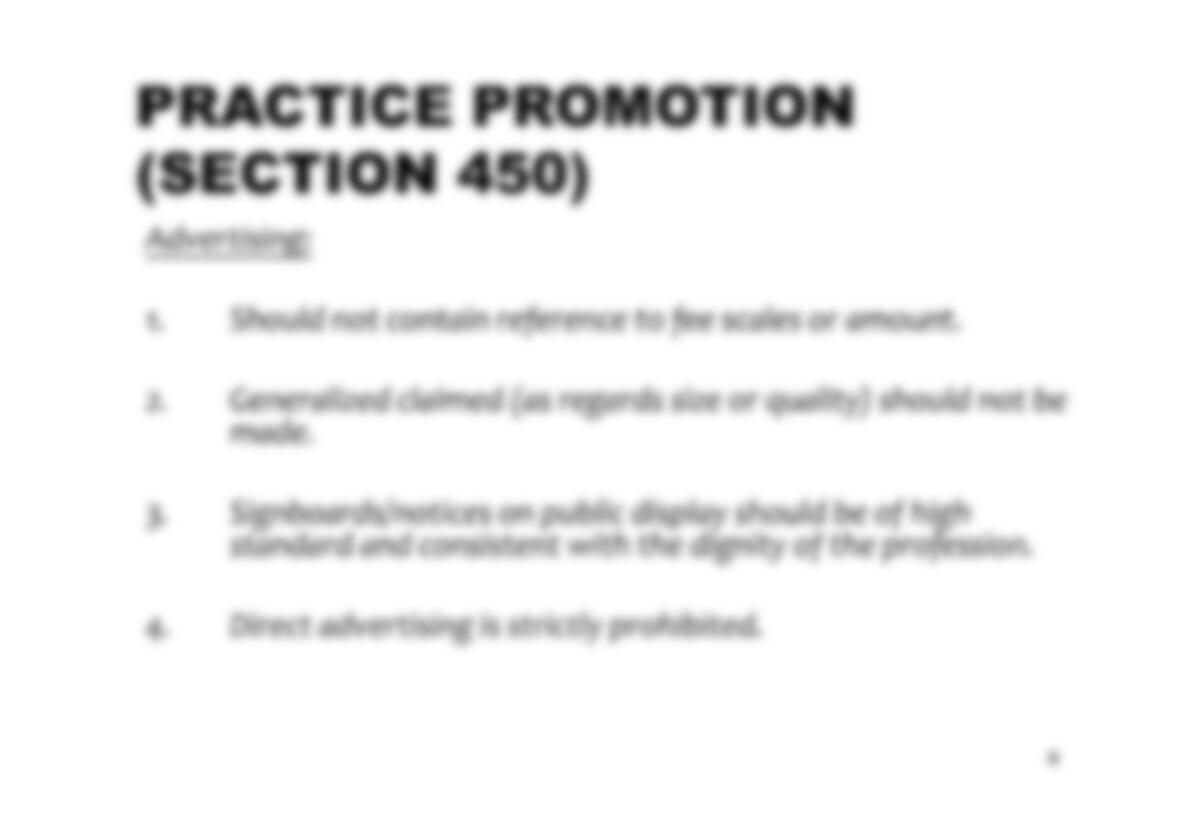

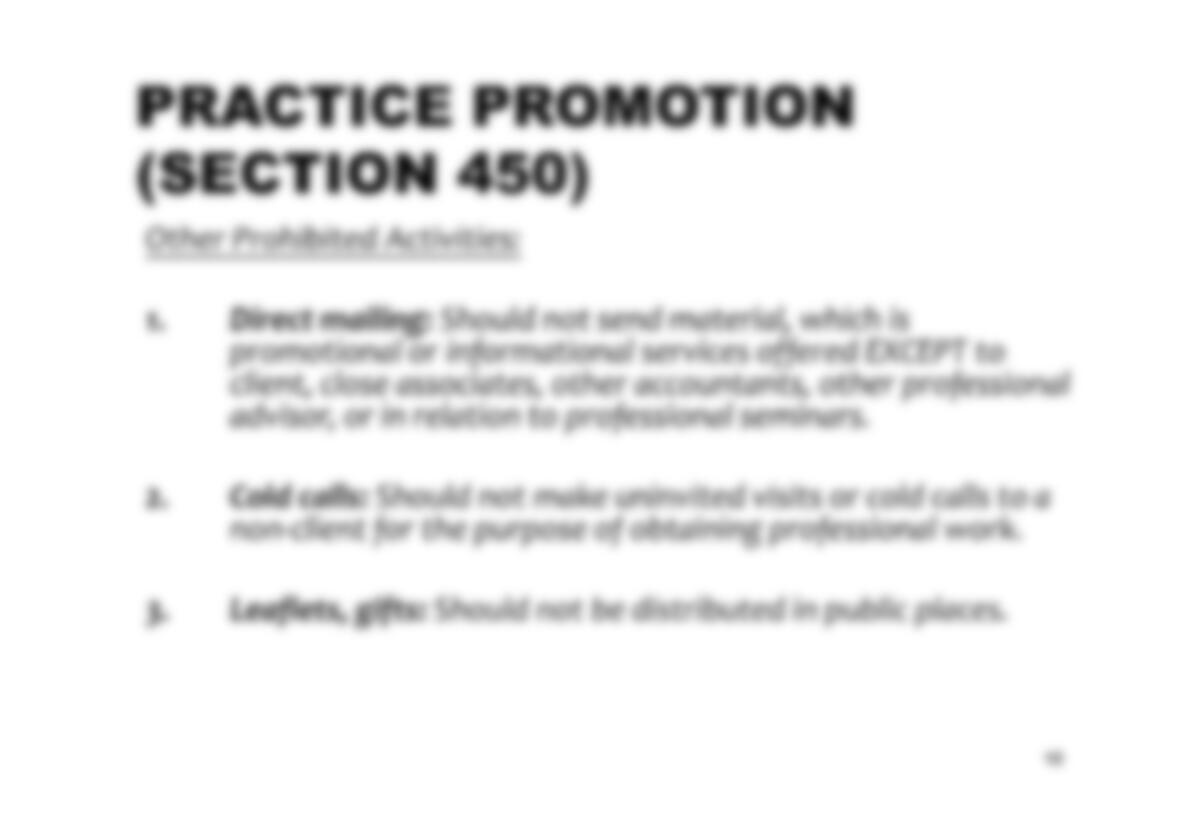

5. Practice Promotion (Section 450)

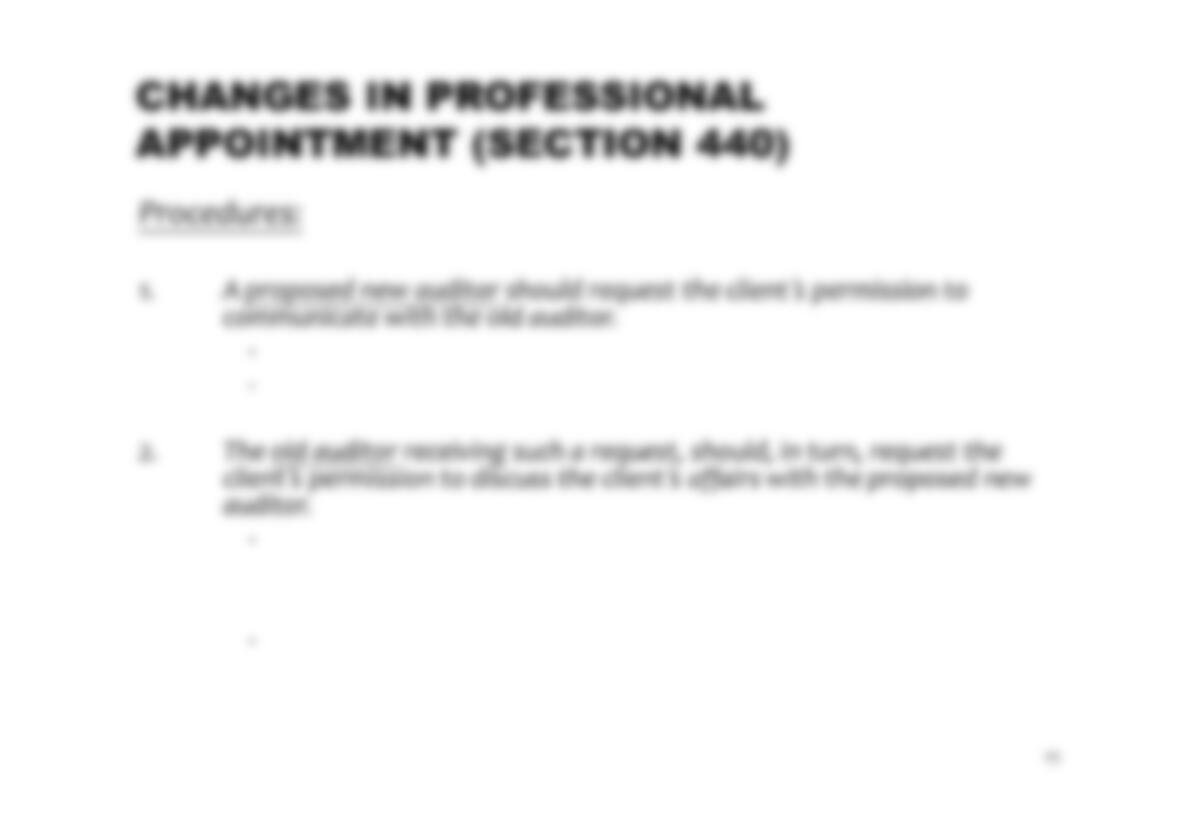

6. Changes in Professional Appointment (Section 440)

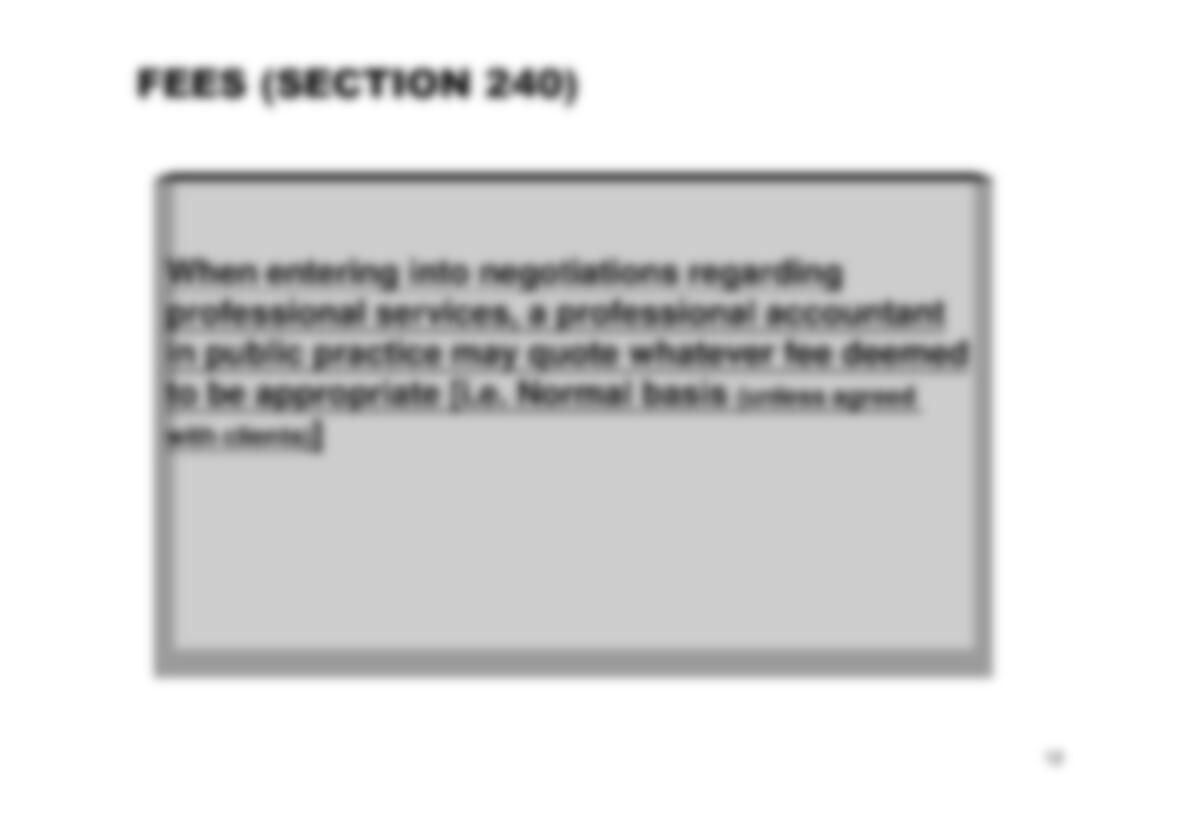

7. Fees (Section 240)

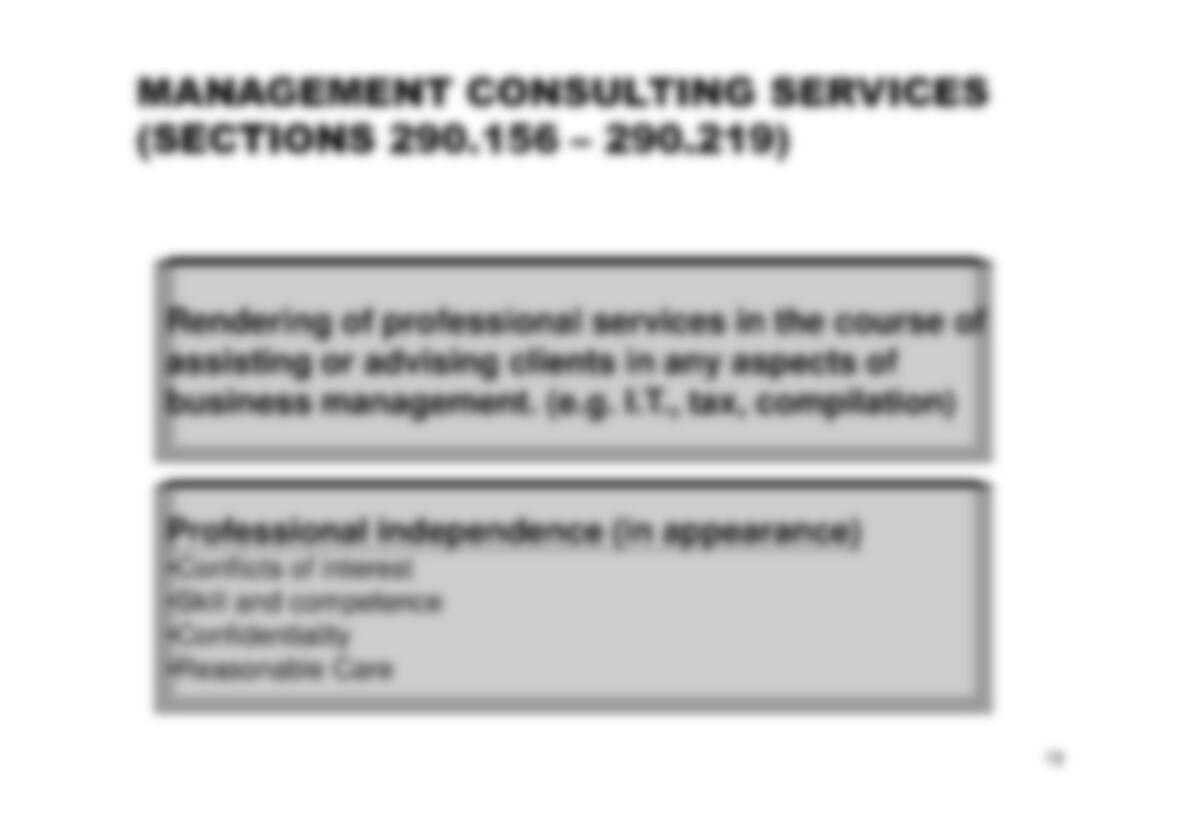

8. Management Consulting Services (Sections 290.156 –290.219)

INDEPENDENCE (SECTION 290)

Independence of mind (Independence in fact)Independence of mind (Independence in fact)

--