Chapter 4

Adjustments, Financial Statements, and

Financial Results

ANSWERS TO QUESTIONS

1. Adjusting entries are made at the end of the accounting period to record all

revenues and expenses that have not been recorded but belong in the current

period. These adjustments also ensure that the related accounts on the balance

sheet and income statement are up-to-date and complete.

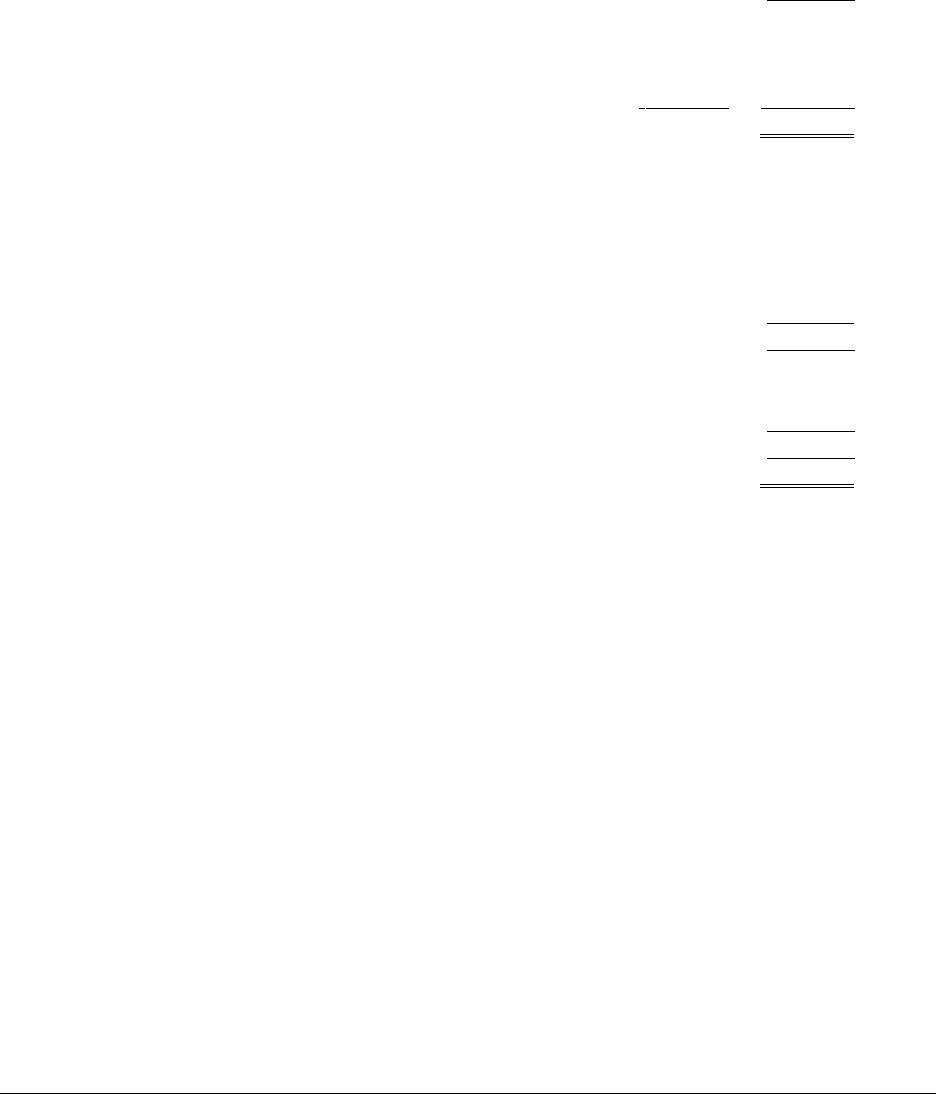

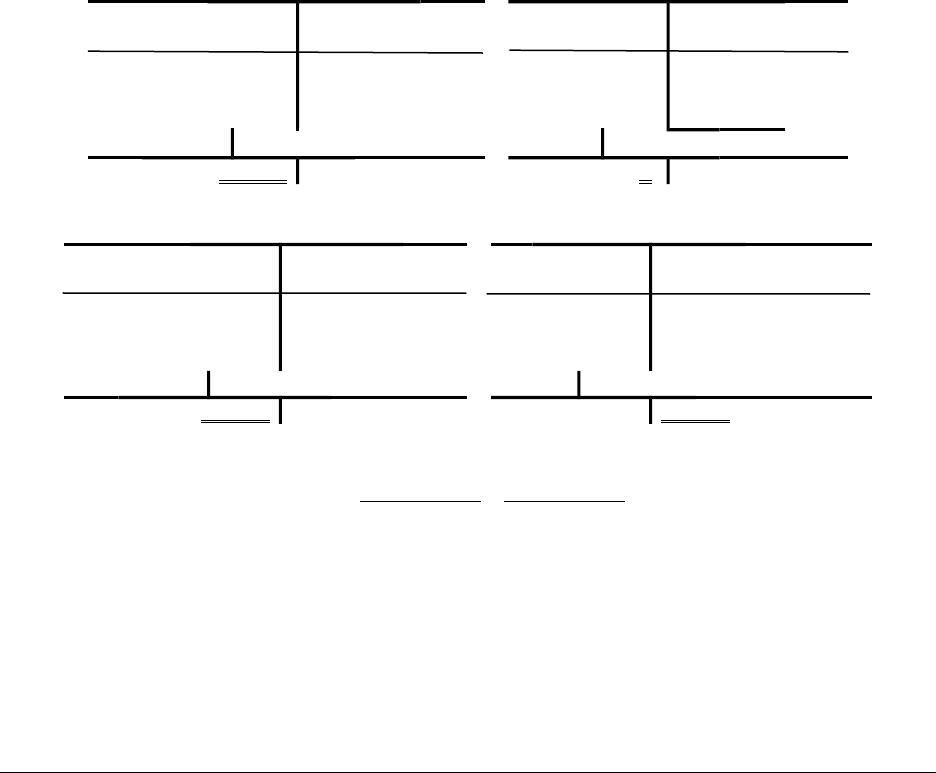

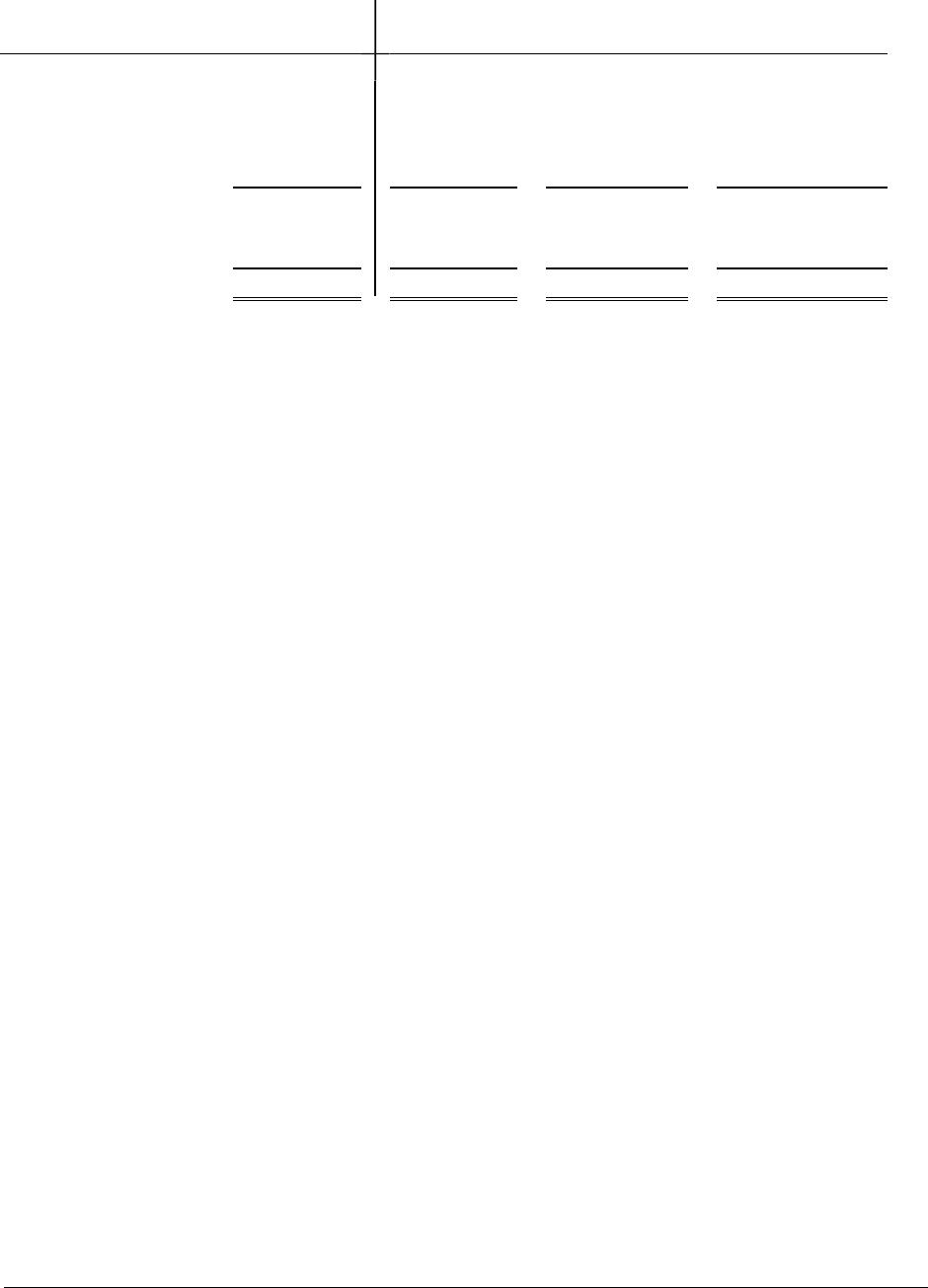

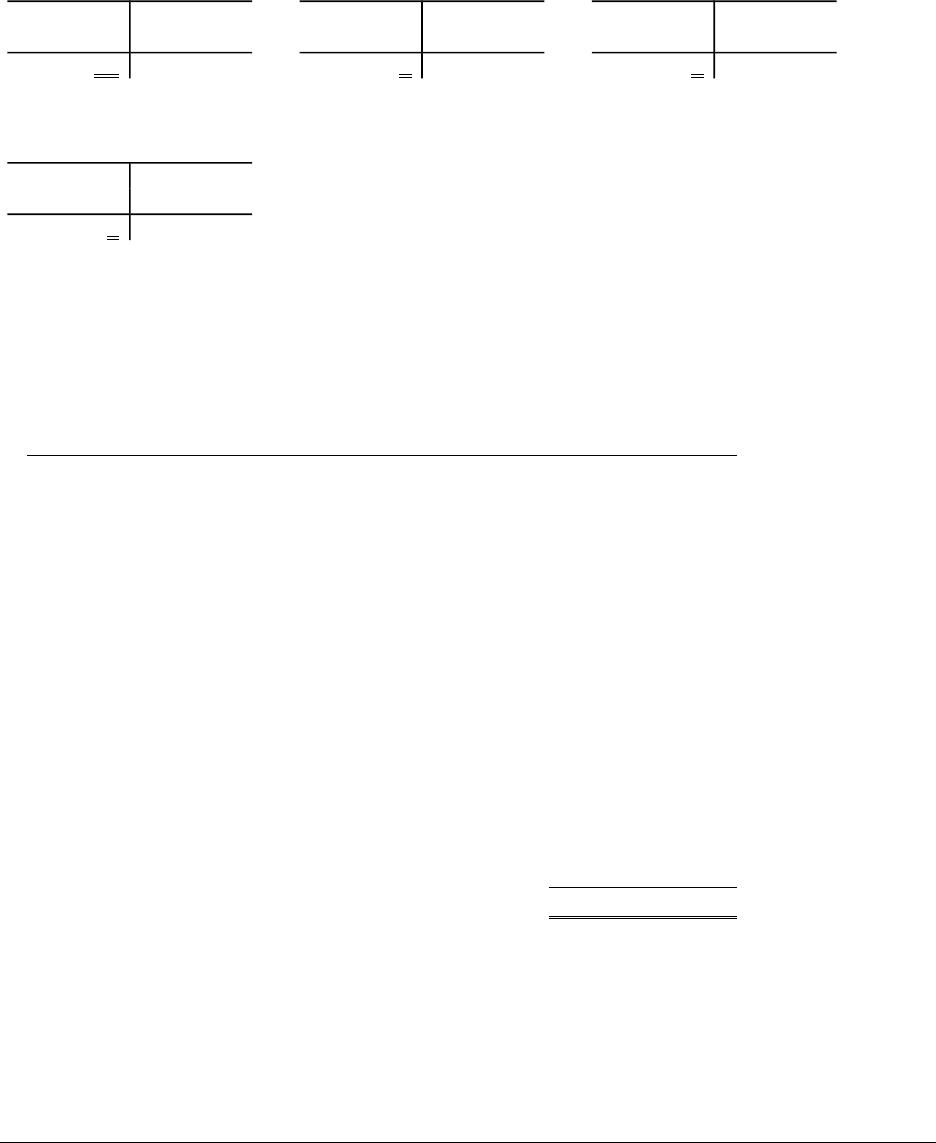

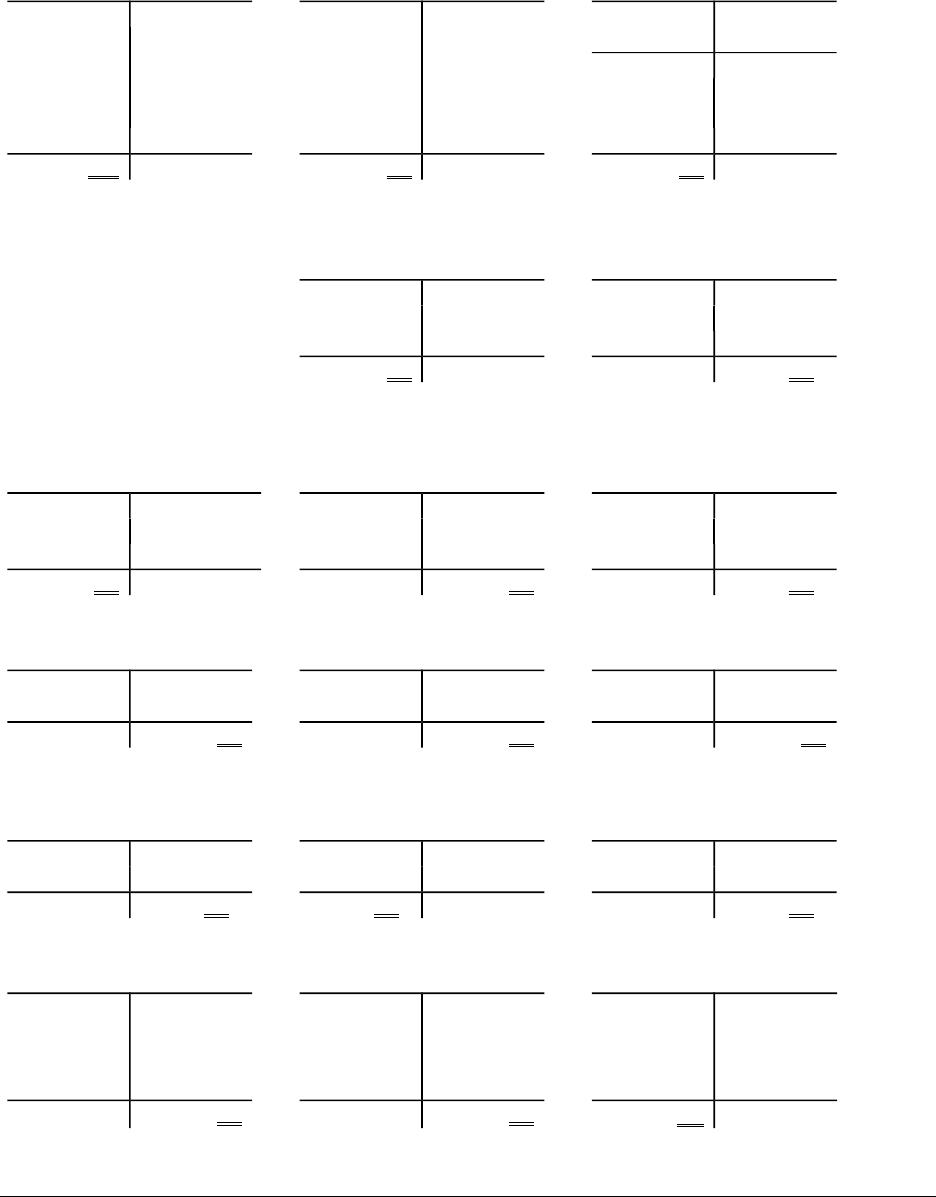

2. (a) The time period assumption states that the long life of a company can be

divided into shorter time periods. Adjustments are required by GAAP to

ensure that a company’s financial statements include all the transactions of

the given time period.

(b) The revenue recognition principle states that revenues should be recorded

when earned. Adjustments assist in recording revenues during the period in

which they are earned, rather than when cash is received.

(c) The expense recognition or “matching” principle states that expenses are

recorded when incurred to generate revenues. Adjustments ensure that the

expenses incurred during a particular period are, in fact, recorded during that

period.

3. The two different types of adjusting journal entries are:

(1) Deferral adjustments:

(a) Revenues — previously recorded liabilities that need to be adjusted at the

end of the period to reflect earned revenues (e.g., unearned revenue must be

adjusted for the portion of sales revenues earned in the current period).

(b) Expenses– previously recorded assets that need to be adjusted at the end

of the period to reflect incurred expenses (e.g., prepaid insurance must be

adjusted for the portion of insurance expense incurred in the current period).

(2) Accrual adjustments:

(a) Revenues — revenues that have been earned by the end of the accounting

period, but will be collected in a future accounting period (e.g., recording

interest receivable for interest earned but not yet collected).

(b) Expenses — expenses that have been incurred by the end of the accounting

period, but will be paid in a future accounting period (e.g., recording an

accrued liability for utilities used during the period but which have not yet been

paid).

Fundamentals of Financial Accounting, 4/e 4- 1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

4. Adjusting entries have no effect on cash. For unearned revenues and

prepayments, cash was received or paid at some point in the past. For accruals,

cash will be received or paid in a future accounting period. At the time of the

adjusting entry, no cash is received or paid.

5. A contra-asset is an account related to an asset that is an offset or reduction to the

asset’s balance. Accumulated Depreciation is a contra-account to the equipment

and buildings accounts.

6. Depreciation expense is reported on the income statement. It indicates the amount

of depreciation for the current period. Accumulated depreciation is reported on the

balance sheet (as a contra-asset). It indicates the total depreciation, which has

accumulated from the date the asset was acquired to the date of the balance sheet.

7. An adjusted trial balance is a list of the individual accounts, usually in financial

statement order, with their adjusted debit or credit balances. It is used to provide a

check on the equality of the debits and credits.

8.

Assets = Liabilities + Stockholders’ Equity

De

c

31

Cash

Prepaid Rent 9,000

+9,000 =

Jan

31

Prepaid Rent 3,000 =Rent

Expense (+E) 3,000

Fe

b

28

Prepaid Rent 3,000

=

Rent

Expense (+E) 3,000

Ma

r

31

Prepaid Rent 3,000

=

Rent

Expense (+E) 3,000

9. Balance sheet accounts at January 31:

Prepaid rent $6,000

Income statement accounts for period ended January 31:

Rent expense $3,000

4- 2 Solutions Manual

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

10.

12/31 dr Prepaid Rent (+A)………………………………………. 9,000

cr Cash (A)……………………………………………. 9,000

1/31 dr Rent Expense (+E, SE)…………………………….. 3,000

cr Prepaid Rent (A)………………………………… 3,000

2/28 dr Rent Expense (+E, SE)…………………………….. 3,000

cr Prepaid Rent (A)………………………………… 3,000

3/31 dr Rent Expense (+E, SE)…………………………….. 3,000

cr Prepaid Rent (A)………………………………… 3,000

11. (a) Income statement: Revenues Expenses = Net Income

(b) Balance sheet: Assets = Liabilities + Stockholders’ Equity

(c) Statement of retained earnings: Beginning Retained Earnings + Net Income

Dividends Declared = Ending Retained Earnings

12. The net income from the income statement is included on the statement of retained

earnings to determine the ending retained earnings balance, which is then reported

on the balance sheet as a stockholders’ equity account.

13. Closing journal entries are made at the end of the accounting period to transfer the

balances in the temporary accounts to retained earnings. The closing journal

entries reduce the revenue, expense, and dividends declared accounts to a zero

balance so that they can be used for the accumulation process during the next

period. Closing entries must be entered into the system through the journal and

posted to the ledger accounts to state properly the temporary and permanent

account balances (i.e., zero balances in the temporary accounts).

14. Permanent accounts are balance sheet accounts (for assets, liabilities, and

stockholders’ equity accounts). These accounts are not closed at the end of

each period.

Temporary accounts include all income statement accounts (for revenues and

expenses) and the Dividends Declared account. These accounts are used to

track results of only the current period, so they are closed (into Retained

Earnings) at the end of each year.

Fundamentals of Financial Accounting, 4/e 4- 3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

15. The income statement accounts are closed at the end of the accounting period

because, in effect, they are temporary sub-accounts to retained earnings (i.e., a

part of stockholders’ equity). They are used only for accumulation during the

accounting period. When the period ends, these accumulated accounts must be

transferred (closed) to retained earnings. The closing process serves:

(1) to correctly state retained earnings, and

(2) to clear out the balances of the temporary accounts for the year just ended, so

that these sub-accounts can be used again during the next period for

accumulation and classification purposes.

Balance sheet accounts are not closed at the end of the period because they

reflect permanent accumulated balances of assets, liabilities, and stockholders’

equity. Permanent accounts show the business’s financial position at the end of

the period and are the beginning amounts for the next period.

16. Dividends declared is a stockholders’ equity account that reduces the overall value

of stockholders’ equity. It functions as a temporary account that is closed to