Chapter 2

The Balance Sheet

ANSWERS TO QUESTIONS

1. (a) An asset is a resource owned by a company that has measurable value

and is expected to provide future benefits.

(b) A current asset is an asset that will be used up or turned into cash within

the next 12 months.

(c) A liability is a debt or obligation arising from past transactions or events,

which the company is likely to pay, settle, or fulfill by sacrificing resources

in the future.

(d) A current liability is a debt or obligation that will be paid, settled, or

fulfilled within one year.

(e) Contributed capital includes the amount of financing (cash and sometimes

other assets) provided to the company by stockholders in exchange for

shares of stock.

(f) Retained earnings are the cumulative earnings of a company that are not

distributed to the owners and instead are reinvested in the business.

2. A transaction is an exchange or event that has a direct and measurable financial

effect on the assets, liabilities, or stockholders’ equity of a business.

Transactions include two different types of events: (1) external exchanges and

(2) internal events. The first situation (1) is exemplified by the sale of goods or

services to customers. The second situation (2) is exemplified by employees

using up the benefits of equipment owned by the company.

3. Accounts are used to accumulate and report the effects of different business

activities. Accounts are necessary to keep track of all increases and decreases

in the basic accounting equation.

4. The basic accounting equation is: Assets = Liabilities + Stockholders’ Equity.

5. Debit is the left side of a T-account and credit is the right side of a T-account. A

debit is an increase in assets or a decrease in liabilities or stockholders’ equity.

Fundamentals of Financial Accounting, 4/e 2- 1

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

A credit is the opposite – a decrease in assets or an increase in liabilities or

stockholders’ equity.

6. Transaction analysis is the process of studying a transaction to determine its

financial effect on the business in terms of the basic accounting equation:

Assets = Liabilities + Stockholders’ Equity

The two principles underlying the process are:

* Duality of effects: every transaction affects at least two accounts.

* A=L+SE; the accounting equation must remain in balance after each

transaction.

7. The accounting equalities in transaction analysis are:

(a) Assets = Liabilities + Stockholders’ Equity

(b) Debits = Credits

8. A journal entry is a method for expressing the effects of a transaction on

accounts in a debits equal credits format. The title of the account(s) to be

debited is (are) listed first. The title of the account(s) to be credited is (are) listed

underneath the debited accounts and both account title(s) and amount(s) are

indented to the right. (An optional explanation can be included on the lines

following the journal entry; this explanation is omitted in most textbook examples

and homework problems because the description of the transaction in the

textbook already provides the explanation.)

9. T-accounts are a simplified version of the ledger, which summarizes transaction

effects for each account. T-accounts show increases on the left (debit) side for

assets, which are on the left side of the accounting equation. T-accounts show

increases on the right (credit) side for liabilities and stockholders’ equity, which

are on the right side of the accounting equation. The T-account is a tool for

summarizing transaction effects for each account and determining balances.

10. The cost principle requires that assets and liabilities be recorded at their original

cost to the company.

11. Because the customer list was not purchased by her salon (it was developed

internally), her salon does not report it on the balance sheet. Knowing this, she

should be sure to advise her banker that the salon has established a loyal group

of customers that holds considerable value for generating future revenues (but is

excluded from the balance sheet for accounting reasons).

2- 2 Solutions Manual

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Authors’ Recommended Solution Time

(Time in minutes)

Mini-exercises Exercises Problems

Skills

Development

Cases*

Continuing

Case

No. Time No. Time No. Time No. Time No. Time

1 2 1 8 CP2-1 45 1 15 1 30

2 2 2 10 CP2-2 50 2 15

3 4 3 5 CP2-3 50 3 45

4 4 4 5 PA2-1 45 4 20

5 4 5 3 PA2-2 50 5 20

6 4 6 5 PA2-3 50 6 10

7 3 7 3 PB2-1 45 7 35

8 3 8 10 PB2-2 50

9 5 9 5 PB2-3 50

10 6 10 15

11 6 11 20

12 6 12 25

13 10 13 10

14 10 14 15

15 10 15 30

16 10

17 10

18 10

19 10

20 10

21 15

22 10

23 3

24 8

25 8

* Due to the nature of cases, it is very difficult to estimate the amount of time students

will need to complete them. As with any open-ended project, it is possible for students

to devote a large amount of time to these assignments. While students often benefit

from the extra effort, we find that some become frustrated by the perceived difficulty of

the task. You can reduce student frustration and anxiety by making your expectations

clear, and by offering suggestions (about how to research topics or what companies to

select). The skills developed by these cases are indicated in the table on the following

page.

Fundamentals of Financial Accounting, 4/e 2- 3

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Cas

e

Financia

l

Analysis

Research Ethical

Reasoning

Critical

Thinking Technology Writing Teamwork

1 x

2 x

3 x x x x x

4 x x x

5 x x x x

6 x x

7 x x

ANSWERS TO MINI-EXERCISES

M2-1

Debit Credit

Assets Increases Decreases

Liabilities Decreases Increases

Stockholders’ Equity Decreases Increases

M2-2

Increase Decrease

Assets Debit Credit

Liabilities Credit Debit

Stockholders’ Equity Credit Debit

M2-3 (1) D (2) C (3) A (4) I (5) F (6) B

M2-4 (1) CL (2) CL (3) CA (4) NCA (5) CA (6) SE (7) NCA

(8) CL (9) NCA (10) CL (11) SE (12) CA (13) CL

M2-5

2- 4 Solutions Manual

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Req. 1 Req. 2

Category Normal Balance

1) CA Debit

2) CL Credit

3) SE Credit

4) NCL Credit

5) CL Credit

6) NCA Debit

7) SE Credit

8) CL Credit

9) CA Debit

M2-6

Req.1 Req.2

Category Normal Balance

1) CL Credit

2) CA Debit

3) CA Debit

4) SE Credit

5) NCL Credit

6) NCA Debit

7) SE Credit

8) CL Credit

M2-7

1) Yes

2) No

3) Yes

4) No

5) No

6) Yes

M2-8

1) Yes

2) Yes

3) No – This event involves only a written promise to rent the store space. No

exchange of cash, goods, or services has occurred.

4) Yes

5) No

Fundamentals of Financial Accounting, 4/e 2- 5

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

M2-9

Assets = Liabilities + Stockholders’ Equity

a. Cash +3,940 Notes Payable

(short-term)

+3,940

b. Cash +4,630 Contributed

Capital

+4,630

c. Cash

Equipment

–200

+1,000

Notes Payable

(short-term)

+800

d. Cash

Supplies

–300

+300

e. Supplies +700 Accounts

Payable

+700

M2-10

a. dr Cash (+A)………….………….………….……………….…..….…... 3,940

cr Notes Payable (short-term) (+L)…………..…..…..….….. 3,940

b. dr Cash (+A)………….………….………….……………….…..….…... 4,630

cr Contributed Capital (+SE)………….………….…………….. 4,630

c. dr Equipment (+A)…….………….………….…..…..….….….…..…. 1,000

cr Cash (A)………..………….………….……………..….….…... 200

cr Notes Payable (short-term) (+L)…………..…..…..….….. 800

d. dr Supplies (+A)……………….………….………….………….………. 300

cr Cash (A)………..………….………….……………..….….…... 300

e. dr Supplies (+A)……………….………….………….………….………. 700

cr Accounts Payable (+L)……………..……………………….… 700

M2-11

Cash (A) Supplies (A) Equipment (A)

(a) 3,940 200 (c) (d) 300 (c) 1,000

(b) 4,630 300 (d) (e) 700

8,070 1,000 1,000

Accounts Payable (L) Notes Payable (L) Contributed Capital (SE)

700 (e) 3,940 (a) 4,630 (b)

800 (c)

700 4,740 4,630

M2-12

2- 6 Solutions Manual

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

SPOTLIGHTER INC.

Balance Sheet

At January 31, 2013

Assets Liabilities

Current Assets: Current Liabilities:

Cash $ 8,070 Accounts Payable $ 700

Supplies 1,000 Notes Payable 4,740

Total Current Assets 9,070 Total Current Liabilities 5,440

Stockholders’ Equity

Equipment 1,000 Contributed Capital 4,630

Total Assets $ 10,070

Total Liabilities & Stockholders’

Equity $10,070

M2-13

a.

dr Cash (+A) 70,000

cr Contributed Capital (+SE) 70,000

b.

dr Land (+A) 60,000

cr Cash (-A) 60,000

c.

dr Supplies (+A) 9,000

cr Accounts Payable (+L) 9,000

d.

dr Cash (+A) 25,000

cr Note Payable (long-term) (+L) 25,000

e.

No transaction

Fundamentals of Financial Accounting, 4/e 2- 7

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

M2-14

Assets = Liabilities + Stockholders’ Equity

(a Cash + 70,000

Contributed

Capital + 70,000

(b) Cash – 60,000

Land + 60,000

(c) Supplies + 9,000

Accounts

Payable + 9,000

(d) Cash + 25,000

Note

Payable + 25,000

(e) No transaction

104,000 34,000

70,000

M2-15

a.

dr Equipment (+A) 4,000

cr Cash (-A) 4,000

b.

dr Books (+A) 7,000

cr Accounts Payable (+L) 7,000

c.

dr Cash (+A) 4,000

cr Note Payable (short-term) (+L) 4,000

d.

dr Accounts Payable (-L) 1,500

cr Cash (-A) 1,500

e.

dr Note Payable (short-term) (-L) 4,000

cr Cash (-A) 4,000

2- 8 Solutions Manual

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

M2-16

Assets = Liabilities +

Stockholders’

Equity

(a) Cash – 4,000

Equipment + 4,000

(b) Books + 7,000 Accounts Payable + 7,000

(c) Cash + 4,000 Note Payable + 4,000

(d) Cash – 1,500 Accounts Payable – 1,500

(e) Cash – 4,000 Note Payable – 4,000

5,500 5,500

M2-17

a.

dr Equipment (+A) 12,000

cr Accounts Payable (+L) 12,000

b.

dr Accounts Payable (-L) 6,000

cr Cash (-A) 6,000

c.

dr Cash (+A) 400

cr Accounts Receivable (-A) 400

d.

dr Cash (+A) 15,000

cr Contributed Capital (+SE) 15,000

e.

dr Equipment (+A) 60,000

cr Cash (-A) 10,000

cr Note Payable (+L) 50,000

Fundamentals of Financial Accounting, 4/e 2- 9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

M2-18

Assets = Liabilities + Stockholders’ Equity

(a) Equipment + 12,000

Accounts

Payable + 12,000

(b) Cash – 6,000

Accounts

Payable – 6,000

(c) Cash + 400

Accounts

Receivable – 400

(d) Cash + 15,000

Contributed

Capital + 15,000

(e) Cash – 10,000 Note Payable + 50,000

Equipment + 60,000

+ 71,000 + 56,000 + 15,000

M2-19

a.

dr Cash (+A) 50

cr Accounts Receivable (-A) 50

b.

No transaction

c.

dr Accounts Payable (-L) 2,000

cr Cash (-A) 2,000

d.

dr Note Payable (short-term) (-L) 5,000

cr Cash (-A) 5,000

e.

dr Equipment (+A) 2,200

cr Cash (-A) 1,000

cr Note Payable (short-term) (+L) 1,200

2- 10 Solutions Manual

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

M2-20

Assets = Liabilities + Stockholders’

Equity

(a) Cash + 50

Accounts Receivable – 50

(b) No transaction

(c) Cash – 2,000 Accounts Payable – 2,000

(d) Cash – 5,000

Note Payable

(short-term) – 5,000

(e) Cash – 1,000 Note Payable +1,200

Equipment + 2,200 (short-term)

– 5,800 – 5,800

M2-21

CHARLIE’S CRISPY CHICKEN

Balance Sheet

At September 30, 2013

Assets Liabilities

Current Assets Current Liabilities

Cash $ 1,800 Accounts Payable $ 2,000

Food Ingredients 400 Wages Payable 200

Supplies 1,400 Utilities Payable 300

Total Current Assets 3,600 Total Current Liabilities 2,500

Note Payable 25,000

Total Liabilities 27,500

Restaurant Booths 25,000

Kitchen Equipment 13,000 Stockholders’ Equity

Land 18,900 Contributed Capital 30,000

Retained Earnings 3,000

Total Stockholders’ Equity 33,000

Total Assets $ 60,500

Total Liabilities & Stockholders’

Equity $60,500

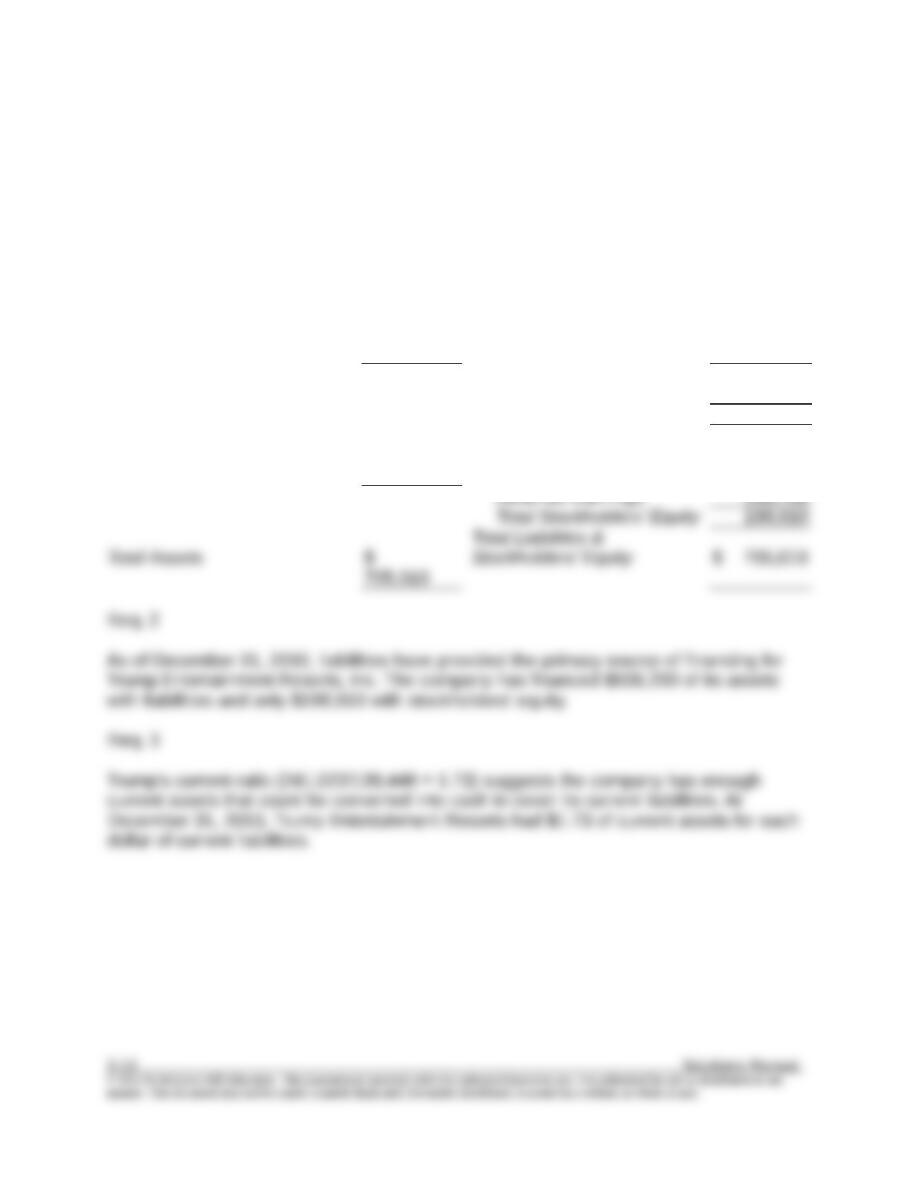

CCC’s current ratio (3,600/2,500 = 1.44) suggests the company has enough current

assets that could be converted into cash to cover its current liabilities. At September

30, CCC had $1.44 of current assets for each dollar of current liabilities.

Fundamentals of Financial Accounting, 4/e 2- 11

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

M2-22

Req. 1

TRUMP ENTERTAINMENT RESORTS, INC.

Balance Sheet

At December 31, 2010

(in thousands)

Assets Liabilities

Current Assets Current Liabilities

Cash $

85,585

Accounts Payable $ 40,862

Accounts Receivable 26,094 Salaries Payable 24,338

Other Current Assets 129,343 Other Current Liabilities 74,248

Total Current Assets 241,022 Total Current Liabilities 139,448

Long-term Note Payable 366,752

Total Liabilities 506,200

Stockholders’ Equity

Equipment 463,988 Contributed Capital 11