SOURCE: Courtesy of Ford Motor Company

CHAPTER Bonds and Their Valuation

8

48

Most analysts agreed that these bonds had limited

default risk. At the time, Ford held $24 billion in cash

and had earned a record $2.5 billion during the second

quarter of 1999. However, the auto industry faces some

inherent risks. When all the risk factors were balanced,

the issues all received a single-A rating. Much to the

relief of the jittery bond market, the Ford issue was well

uring the summer of 1999 the future course of

interest rates was highly uncertain. Continued

strength in the economy and growing fears of

inflation had caused interest rates to rise, and many

analysts were concerned that this trend would continue.

However, others were forecasting declining rates — they

saw no threat from inflation and were more concerned

about the economy running out of gas. Because of this

uncertainty, bond investors tended to wait on the sidelines

for some definitive economic news. At the same time,

companies tended to postpone bond issues out of fear that

nervous investors would be unwilling to purchase them.

This is exactly the situation in which Ford Motor

found itself in June 1999, when it decided to put a

large debt issue on hold. However, after just three

weeks, Ford sensed a shift in the investment climate,

and it announced plans for an $8.6 billion bond issue.

As shown in the following table, the Ford issue set a

new record, surpassing an $8 billion AT&T issue that had

taken place a few months earlier.

Ford’s $8.6 billion issue actually consisted of four

separate bonds. Ford Credit, a subsidiary that provides

customer financing, borrowed $1.0 billion dollars at a

two-year floating rate and another $1.8 billion at a

three-year floating rate. Ford Motor itself borrowed $4

billion as five-year fixed-rate debt and another $1.8

billion at a 32-year fixed rate.

FORD’S BOND

ISSUE SETS

A NEW RECORD

FORD MOTOR COMPANY

$

D

349

Top Ten U.S. Corporate Bond Financings

as of July 1999

AMOUNT

(BILLIONS

ISSUER DATE OF DOLLARS)

Ford July 9, 1999 $8.60

AT&T March 23, 1999 8.00

RJR Holdings May 12, 1989 6.11

WorldCom August 6, 1998 6.10

Sprint November 10, 1998 5.00

Assoc. Corp. of

N. America October 27, 1998 4.80

Norfolk Southern May 14, 1997 4.30

US West January 16, 1997 4.10

Conoco April 15, 1999 4.00

Charter

Communications March 12, 1999 3.58

SOURCE: Thomson Financial Securities Data, Credit Suisse

First Boston as reported in The Wall Street Journal, July 12,

1999, C1.

CHAPTER 8 ■BONDS AND THEIR VALUATION

350

Bonds are one of the most important types of securities. If you skim through The

Wall Street Journal, you will see references to a wide variety of these securities.

This variety may seem confusing, but in actuality just a few characteristics dis-

tinguish the various types of bonds.

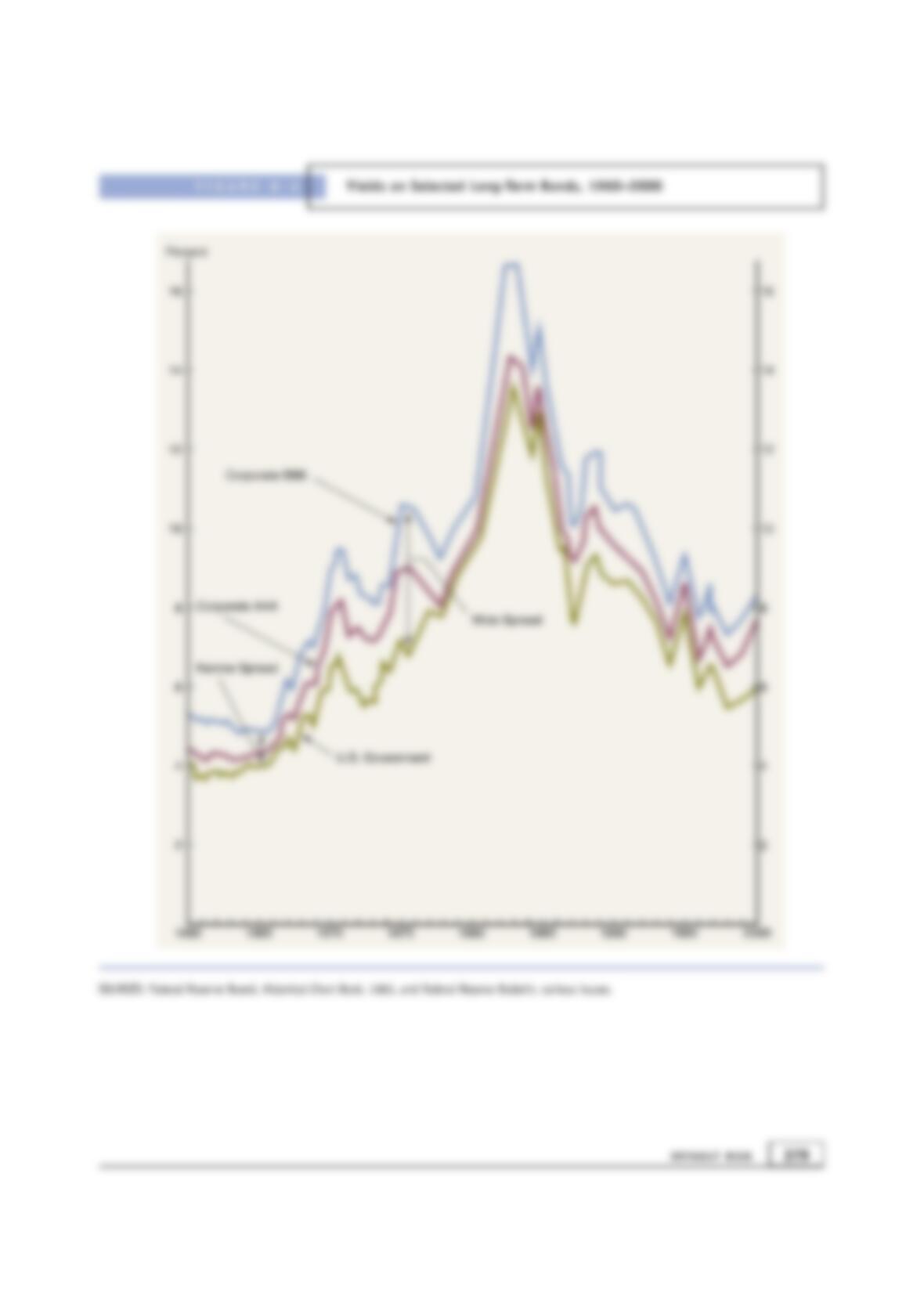

While bonds are often viewed as relatively safe investments, one can certainly

lose money on them. Indeed, “riskless” long-term U.S. Treasury bonds have de-

clined in value three of the last seven years. Note, though, that it is also possi-

ble to rack up impressive gains in the bond market. Long-term government bonds

provided a total return of nearly 16 percent in 1997 and more than 30 percent in

1995.

In this chapter, we will discuss the types of bonds companies and government

agencies issue, the terms that are contained in bond contracts, the types of risks

to which both bond investors and issuers are exposed, and procedures for deter-

mining the values of and rates of return on bonds. ■

bonds outstanding will decrease, forcing many Treasury

investors into the corporate bond market, where they

will look for investment-grade issues by companies such

as Ford.

Already anticipating this demand, Ford is planning

to regularly issue large blocks of debt in the global

market. Seeing Ford’s success, less than one month

after the Ford issue, Wal-Mart entered the list of top

ten U.S. corporate bond financings with a new $5

billion issue. Other large companies have subsequently

followed suit. ■

SOURCE: Gregory Zuckerman, “Ford’s Record Issue May Drive

Imitators,” The Wall Street Journal, July 12, 1999, C1.

received. Dave Cosper, Ford Credit’s Treasurer, said

“There was a lot of excitement, and demand exceeded

our expectations.”

The response to the Ford offering revealed that

investors had a strong appetite for large bond issues

with strong credit ratings. Larger issues are more liquid

than smaller ones, and liquidity is particularly important

to bond investors when the direction of the overall

market is highly uncertain.

Interestingly, large investment-grade issues by well-

known companies such as Ford are also helping to fill

the vacuum created by the reduction in Treasury debt.

The Federal government is forecasting future budget

surpluses, and it plans to use a portion of the surplus to

reduce its outstanding debt. As this occurs, Treasury

351

WHO ISSUES BONDS?

A bond is a long-term contract under which a borrower agrees to make pay-

ments of interest and principal, on specific dates, to the holders of the bond.

For example, on January 3, 2002, Allied Food Products borrowed $50 million

by issuing $50 million of bonds. For convenience, we assume that Allied sold

50,000 individual bonds for $1,000 each. Actually, it could have sold one $50

million bond, 10 bonds with a $5 million face value, or any other combination

that totals to $50 million. In any event, Allied received the $50 million, and in

exchange it promised to make annual interest payments and to repay the $50

million on a specified maturity date.

Investors have many choices when investing in bonds, but bonds are classi-

fied into four main types: Treasury, corporate, municipal, and foreign. Each

type differs with respect to expected return and degree of risk.

Treasury bonds, sometimes referred to as government bonds, are issued by

the federal government.

1

It is reasonable to assume that the federal government

will make good on its promised payments, so these bonds have no default risk.

However, Treasury bond prices decline when interest rates rise, so they are not

free of all risks.

Corporate bonds, as the name implies, are issued by corporations. Unlike

Tr e a s u r y b o n d s , c o r p o r a t e b o n d s a r e e x p o s e d t o d e f a u l t r i s k — i f t h e i s s u i n g

company gets into trouble, it may be unable to make the promised interest and

principal payments. Different corporate bonds have different levels of default

risk, depending on the issuing company’s characteristics and on the terms of the

specific bond. Default risk is often referred to as “credit risk,” and, as we saw in

Chapter 5, the larger the default or credit risk, the higher the interest rate the

issuer must pay.

Municipal bonds, or “munis,” are issued by state and local governments.

Like corporate bonds, munis have default risk. However, munis offer one major

advantage over all other bonds: As we discussed in Chapter 2, the interest

earned on most municipal bonds is exempt from federal taxes and also from

state taxes if the holder is a resident of the issuing state. Consequently, munic-

ipal bonds carry interest rates that are considerably lower than those on corpo-

rate bonds with the same default risk.

Foreign bonds are issued by foreign governments or foreign corporations.

Foreign corporate bonds are, of course, exposed to default risk, and so are some

foreign government bonds. An additional risk exists if the bonds are denomi-

nated in a currency other than that of the investor’s home currency. For exam-

ple, if you purchase corporate bonds denominated in Japanese yen, you will lose

money — even if the company does not default on its bonds — if the Japanese

yen falls relative to the dollar.

WHO ISSUES BONDS?

Bond

A long-term debt instrument.

1

The U.S. Treasury actually calls its debt issues “bills,” “notes,” or “bonds.” T-bills generally have

maturities of 1 year or less at the time of issue, notes generally have original maturities of 2 to 7 years,

and bond maturities extend out to 30 years. There are technical differences between bills, notes, and

bonds, but they are not important for our purposes, so we generally call all Treasury securities

“bonds.” Note too that a 30-year T-bond at the time of issue becomes a 1-year bond 29 years later.

Treasury Bonds

Bonds issued by the federal

government, sometimes referred

to as government bonds.

Corporate Bonds

Bonds issued by corporations.

Municipal Bonds

Bonds issued by state and local

governments.

Foreign Bonds

Bonds issued by either

foreign governments or

foreign corporations.

CHAPTER 8 ■BONDS AND THEIR VALUATION

352

KEY CHARACTERISTICS OF BONDS

Although all bonds have some common characteristics, they do not always

have the same contractual features. For example, most corporate bonds have

provisions for early repayment (call features), but these provisions can be quite

different for different bonds. Differences in contractual provisions, and in the

underlying strength of the companies backing the bonds, lead to major differ-

ences in bonds’ risks, prices, and expected returns. To understand bonds, it is

important that you understand the following terms.

PAR VALUE

The par value is the stated face value of the bond; for illustrative purposes we

generally assume a par value of $1,000, although any multiple of $1,000 (for ex-

ample, $5,000) can be used. The par value generally represents the amount of

money the firm borrows and promises to repay on the maturity date.

COUPON INTEREST RATE

Allied’s bonds require the company to pay a fixed number of dollars of interest

each year (or, more typically, each six months). When this coupon payment,

as it is called, is divided by the par value, the result is the coupon interest rate.

For example, Allied’s bonds have a $1,000 par value, and they pay $100 in in-

terest each year. The bond’s coupon interest is $100, so its coupon interest rate

is $100/$1,000 !10 percent. The $100 is the yearly “rent” on the $1,000 loan.

This payment, which is fixed at the time the bond is issued, remains in force

during the life of the bond.

2

Typ ic al ly , a t t he ti me a bo nd is is su ed , i ts co up on

payment is set at a level that will enable the bond to be issued at or near its par

Par Value

The face value of a bond.

Coupon Payment

The specified number of dollars of

interest paid each period,

generally each six months.

Coupon Interest Rate

The stated annual interest rate on

a bond.

2

Incidentally, some time ago bonds literally had a number of small (1/2- by 2-inch), dated coupons

attached to them, and on each interest payment date, the owner would clip off the coupon for that

date and either cash it at his or her bank or mail it to the company’s paying agent, who would then

mail back a check for the interest. A 30-year, semiannual bond would start with 60 coupons,

whereas a 5-year annual payment bond would start with only 5 coupons. Today, new bonds must

be registered — no physical coupons are involved, and interest checks are mailed automatically to

the registered owners of the bonds. Even so, people continue to use the terms coupon and coupon in-

terest rate when discussing registered bonds.

SELF-TEST QUESTIONS

What is a bond?

What are the four main types of bonds?

Why are U.S. Treasury bonds not riskless?

To what types of risk are investors of foreign bonds exposed?

An excellent site for

information on many types

of bonds is Bonds Online,

which can be found at

http://www.

bondsonline.com.The site has a great

deal of information about corporates,

municipals, treasuries, and bond funds.

It includes free bond searches, through

which the user specifies the attributes

desired in a bond and then the search

returns the publicly traded bonds

meeting the criteria. The site also

includes a downloadable bond calculator

and an excellent glossary of bond

terminology.

353

value. Consequently, most of our examples and problems throughout this text

will focus on bonds with fixed coupon rates.

In some cases, however, a bond’s coupon payment will vary over time. These

floating rate bonds work as follows. The coupon rate is set for, say, the initial

six-month period, after which it is adjusted every six months based on some

market rate. Some corporate issues are tied to the Treasury bond rate, while

other issues are tied to other rates. Many additional provisions can be included

in floating rate issues. For example, some are convertible to fixed rate debt,

whereas others have upper and lower limits (“caps” and “floors”) on how high

or low the rate can go.

Floating rate debt is popular with investors who are worried about the risk of

rising interest rates, since the interest paid increases whenever market rates rise.

This causes the market value of the debt to be stabilized, and it also provides in-

stitutional buyers such as banks with income that is better geared to their own

obligations. Banks’ deposit costs rise with interest rates, so the income on float-

ing rate loans that they have made rises at the same time their deposit costs are

rising. The savings and loan industry was virtually destroyed as a result of their

practice of making fixed rate mortgage loans but borrowing on floating rate

terms. If you are earning 6 percent but paying 10 percent—which they were—

you soon go bankrupt—which they did.

Moreover, floating rate debt appeals to corporations that want to issue long-

term debt without committing themselves to paying an historically high interest

rate for the entire life of the loan.

Some bonds pay no coupons at all, but are offered at a substantial discount

below their par values and hence provide capital appreciation rather than inter-

est income. These securities are called zero coupon bonds (“zeros”). Other

bonds pay some coupon interest, but not enough to be issued at par. In general,

any bond originally offered at a price significantly below its par value is called

an original issue discount (OID) bond. Corporations first used zeros in a

major way in 1981. In recent years IBM, Alcoa, JCPenney, ITT, Cities Service,

GMAC, Lockheed Martin, and even the U.S. Treasury have used zeros to raise

billions of dollars. Some of the details associated with issuing or investing in

zero coupon bonds are discussed more fully in Appendix 8A.

MATURITY DATE

Bonds generally have a specified maturity date on which the par value must be

repaid. Allied’s bonds, which were issued on January 3, 2002, will mature on

January 2, 2017; thus, they had a 15-year maturity at the time they were issued.

Most bonds have original maturities (the maturity at the time the bond is is-

sued) ranging from 10 to 40 years, but any maturity is legally permissible.

3

Of

course, the effective maturity of a bond declines each year after it has been is-

sued. Thus, Allied’s bonds had a 15-year original maturity, but in 2003, a year

later, they will have a 14-year maturity, and so on.

KEY CHARACTERISTICS OF BONDS

Zero Coupon Bond

A bond that pays no annual

interest but is sold at a discount

below par, thus providing

compensation to investors in the

form of capital appreciation.

Original Issue Discount Bond

Any bond originally offered at a

price below its par value.

Maturity Date

A specified date on which the par

value of a bond must be repaid.

Original Maturity

The number of years to maturity

at the time a bond is issued.

3

In July 1993, Walt Disney Co., attempting to lock in a low interest rate, issued the first 100-year

bonds to be sold by any borrower in modern times. Soon after, Coca-Cola became the second com-

pany to stretch the meaning of “long-term bond” by selling $150 million worth of 100-year bonds.

Floating Rate Bond

A bond whose interest rate

fluctuates with shifts in the

general level of interest rates.

CALL PROVISIONS

Most corporate bonds contain a call provision, which gives the issuing corpo-

ration the right to call the bonds for redemption.

4

The call provision generally

states that the company must pay the bondholders an amount greater than the

par value if they are called. The additional sum, which is termed a call premium,

is often set equal to one year’s interest if the bonds are called during the first

year, and the premium declines at a constant rate of INT/N each year there-

after, where INT !annual interest and N !original maturity in years. For ex-

ample, the call premium on a $1,000 par value, 10-year, 10 percent bond would

generally be $100 if it were called during the first year, $90 during the second

year (calculated by reducing the $100, or 10 percent, premium by one-tenth),

and so on. However, bonds are often not callable until several years (generally

5 to 10) after they were issued. This is known as a deferred call, and the bonds

are said to have call protection.

Suppose a company sold bonds when interest rates were relatively high. Pro-

vided the issue is callable, the company could sell a new issue of low-yielding

securities if and when interest rates drop. It could then use the proceeds of the

new issue to retire the high-rate issue and thus reduce its interest expense. This

process is called a refunding operation.

The call privilege is valuable to the firm but potentially detrimental to the

investor, especially if the bonds were issued in a period when interest rates were

cyclically high. Accordingly, the interest rate on a new issue of callable bonds

Call Provision

A provision in a bond contract

that gives the issuer the right to

redeem the bonds under specified

terms prior to the normal

maturity date.