Chapter 2 – Problem 28 – LO.3,4 Scott and Laura are married and will file a joint tax return. Laura has a sole proprietorship (not a

“specified services” business) that generates qualified business income of $300,000. The proprietorship pays W–2 wages of

$40,000 and holds property with an unadjusted basis of $10,000. Scott is employed by a local school district. Their taxable

income before the QBI deduction is $386,600 (this is also their modified taxable income).

– Determine Scott and Laura’s QBI deduction, taxable income, and tax liability for 2020.

– After providing you the original information in the problem, Scott finds out that he will be receiving a $6,000 bonus in

December 2020 (increasing their taxable income before the QBI deduction by this amount). Redetermine Scott and

Laura’s QBI deduction, taxable income, and tax liability for 2020.

– What is the marginal tax rate on Scott’s bonus?

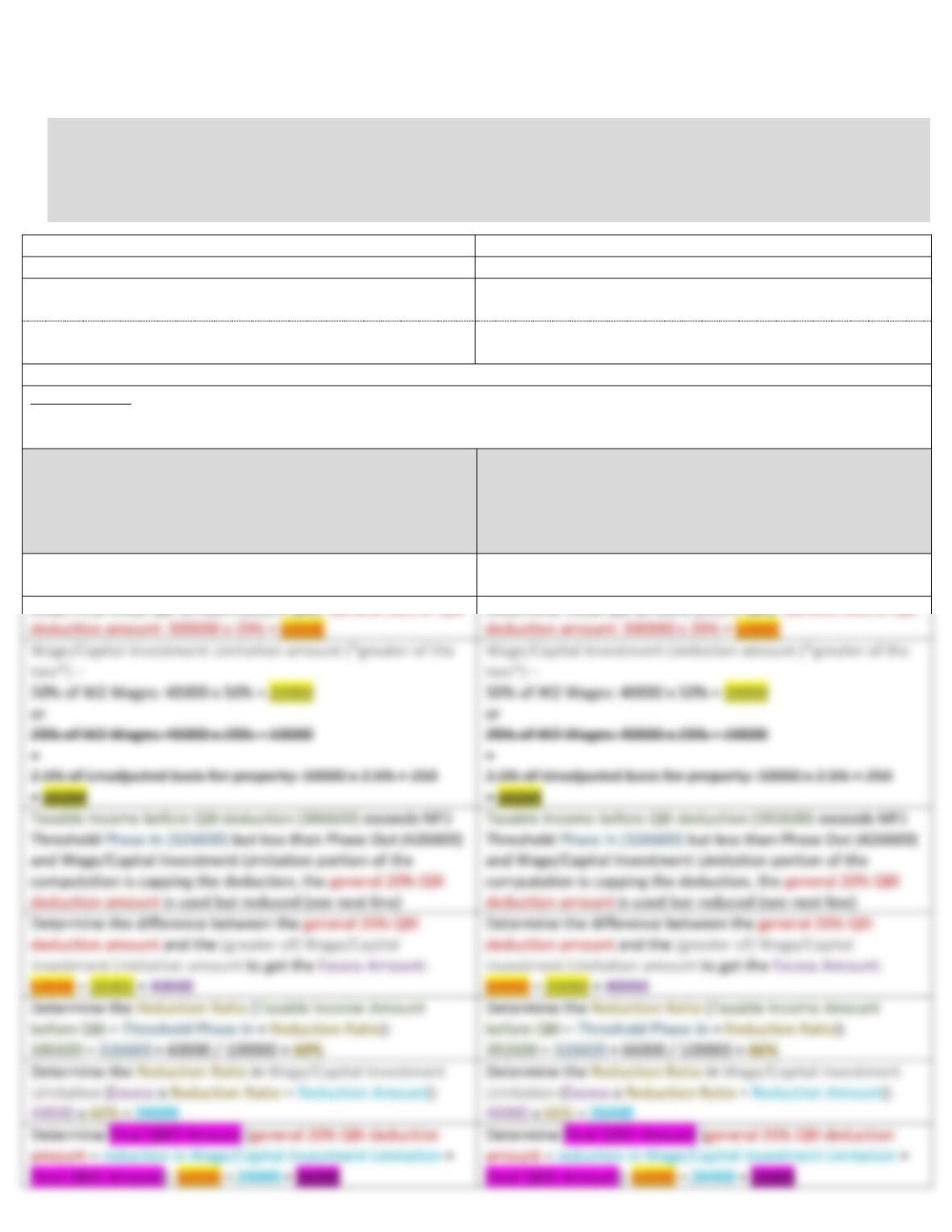

Taxable Income before QBI deduction

386600

Initial QBI Amount

300000

Wage/Capital Investment Limitation

– W2 Wages

40000

Wage/Capital Investment Limitation

– Unadjusted basis for property

10000

Is the QTB ‘specified service’ business? No

MFJ Threshold

Phase In: 326600

Phase Out: 426600

– Determine Scott and Laura’s QBI deduction, taxable income,

and tax liability for 2020.

– After providing you the original information in the problem,

Scott finds out that he will be receiving a $6,000 bonus in

December 2020 (increasing their taxable income before the

QBI deduction by this amount). Redetermine Scott and Laura’s

QBI deduction, taxable income, and tax liability for 2020.

Modified Taxable Income: 386600 x 20% = 77320 no great

than this amount

Modified Taxable Income: 386600 + 6000 = 392600 x 20% =

78520 no great than this amount

Determine Initial QBI amount (20% x QBI): General 20% of QBI

Determine Initial QBI amount (20% x QBI): General 20% of QBI

+

2.5% of Unadjusted basis for property: 10000 x 2.5% = 250

+

2.5% of Unadjusted basis for property: 10000 x 2.5% = 250

Determine the difference between the general 20% QBI

Determine the difference between the general 20% QBI

Determine the Reduction Ratio (Taxable Income Amount

Determine the Reduction Ratio (Taxable Income Amount

Determine the Reduction Ratio in Wage/Capital Investment

Determine the Reduction Ratio in Wage/Capital Investment