Case 5 – Enron Analysis

Problem 1: Company

a. Enron was an energy trading company that sold energy wholesale to other energy

companies. They also handled transportation and delivery of certain energy products,

such as natural gas, and sold energy directly to end-use consumers. Other areas of the

business included trading on products such as plastics, oil, paper, steel and broadband.

The company allowed these products to be traded online much like stocks and bonds,

and encouraged all wholesale customers to trade energy directly through their

ecommerce sites, rather than going through brokers. Enron purchased their energy

products from other companies, many of which were affiliates or subsidiaries. Enron also

traded in derivatives of energy products. This practice, also known as hedging, allows

customers to guarantee a supply of product at a guaranteed price. The company

providing the product is expecting to make money by having the price of the product

drop, while having their customer locked in at a set price for a set term. Enron pioneered

the idea of hedging using energy markets. This concept helped earn Enron the title of

most innovative company from Forbes magazine for six years in a row. Enron also

fostered the deregulation of energy markets, allowing the company to sell energy at

higher prices, which increased their revenues. Enron lobbied against increased

regulation, once deregulation created price volatility in energy markets, to keep energy

prices high. Management at Enron encouraged rule breaking and fostered an

intimidating and aggressive environment which eventually lead to the breakdown of all

ethical constraints.

b. Price Risk Management Activities were used in trading and non trading transactions. For

trading activities, Enron used the mark to market method of accounting for things like

forwards, swaps, options and energy transportation contracts. Management had to

estimate value to the best of their ability to reflect time value, over the counter quotations

and closing exchange. These were also used in non trading activities when hedging the

impact of market fluctuations on assets, liabilities, production and other commitments.

Both realized and unrealized gains from these activities are found on the income

statement in “Other Revenues”, as shown on Note 3 on page 38 of the 10K. Since the

price of energy was constantly increasing, these activities continued to be profitable – but

that profit is dependent on the energy markets. If the market drops, Enron’s mark to

market practices would cause Enron to recognize losses before they are realized. Also,

the notes do not make it clear what percentage of Other Revenues are from price risk

management activities. Enron mentions they keep reserves to cover these activities, but

does not mention amount, or where on the balance sheet these reserves can be found.

Merchant Assets and Investments – As shown in Note 4 on page 40 of the 2000 10K,

merchant investments are capital investments to other merchants in energy and

technology-related businesses, which are marked to fair market value on Enron’s

balance sheet and are either debt or equity on the merchant balance sheets. These

investments are grouped into Other Assets, and changes in these assets are shown in

Other Income on the Income Statement. Merchant Assets are investments Enron made

in other merchants’ assets, such as power plants and natural gas pipelines, and are

held by Enron through equity method investments. Some of these assets were

completely developed and built by Enron, though Note 4 says Enron does not expect

these assets to be part of Enron’s network long-term. Revenues from these assets are

shown in Equity in Earnings of Unconsolidated Equity Affiliates on the income statement.

c. From 1999 to 2000, Enron’s financial statement shows that Assets from Price Risk

Management Activities under investments more than triple, from 2,929 in 1999 to 8,988

in 2000. The same is true for Assets from Price Risk Management Activities listed under

assets which increases in value by a factor of 6. From this you can see how Other

Revenues would have raised, due to their increased activity in price risk management.

Enron’s business was split into five areas: transportation and delivery, wholesale

services, retail services, broadband and corporate activities. By far, the largest segment

is wholesale services, which made up 91% of IBIT (page 21 and page 53), and the

largest section of wholesale services is Commodity Sales and Services (page 23), which

saw a 260% increase in revenue in 2000. Enron’s commodity sales division did see a

marked increase in volume (59% according to the note on page 23), and well as new

revenues from areas such as coal, pulp and paper that were acquired in 2000. However,

they also followed the mark to market accounting principle on these commodities. This

allowed them to mark commodities they owned to fair market value, before they were

sold, allowing them to show false revenues in “Other Revenue”, as referenced in Note 1

on page 36. The notes seem to be somewhat opaque on exactly when unrealized gains

from mark-to-market are realized and where they are kept – Note 1 says that non-trading

hedging is accounted for in the account of the commodity it is hedging, so it is possible

that those mark-to-market gains could also be in the Energy and Natural Gas accounts –

what is clear is that at least some of the unrealized gains show up in Other Revenue.

On page 51 of the 10K, revenues and expenses are broken out by business segment.

While wholesale services revenue increased 253%, its depreciation, depletion and

amortization expense only increased 116%, indicating that there was not a significant

increase in assets. Without a significant increase in assets, its unlikely Enron had

increased its production to reach these revenue amounts – instead it sold the same

amount at higher prices, or sold commodities it had purchased from other producers, or

both.

Problem 2: Information for various ratios

We determined that many line items needed to be removed from the income statement to reach

quality earnings. The largest item we removed from net income was Other Revenues. As noted

on pages 36 and 40 of the 10K, other revenues are comprised of realized and unrealized gains

from Price Risk Management Activities and Merchant Assets and Investments. Some of these

revenues are unrealized so they have no business being in net income, and even the realized

gains are not what we consider high quality earnings. We also removed “Equity in Earnings of

Unconsolidated Equity Affiliates” because, according to page 40, these earnings are changes in

the value of investments in the unconsolidated equity affiliates rather than actual earnings paid

from the affiliates. There may be actual earnings, but it is unclear how much those earnings are,

or why they were treated as revenues rather than dividends or interest income. Another item we

found problematic was earnings from the issuance of stock by NTPC – a company that,

according to Enron’s 10K, is an unconsolidated equity affiliate whose assets and liabilities do

not appear on Enron’s financials. So why would a stock issuance by this company be treated as

earnings by Enron? Other notes may be found in the attached spreadsheet.

Problem 3: Profitability Analysis

a.

Ratios for the year

ended December

31, 2000

Calculated

ratio

Conclusions from ratios and discussion

of drivers of

change in each ratio

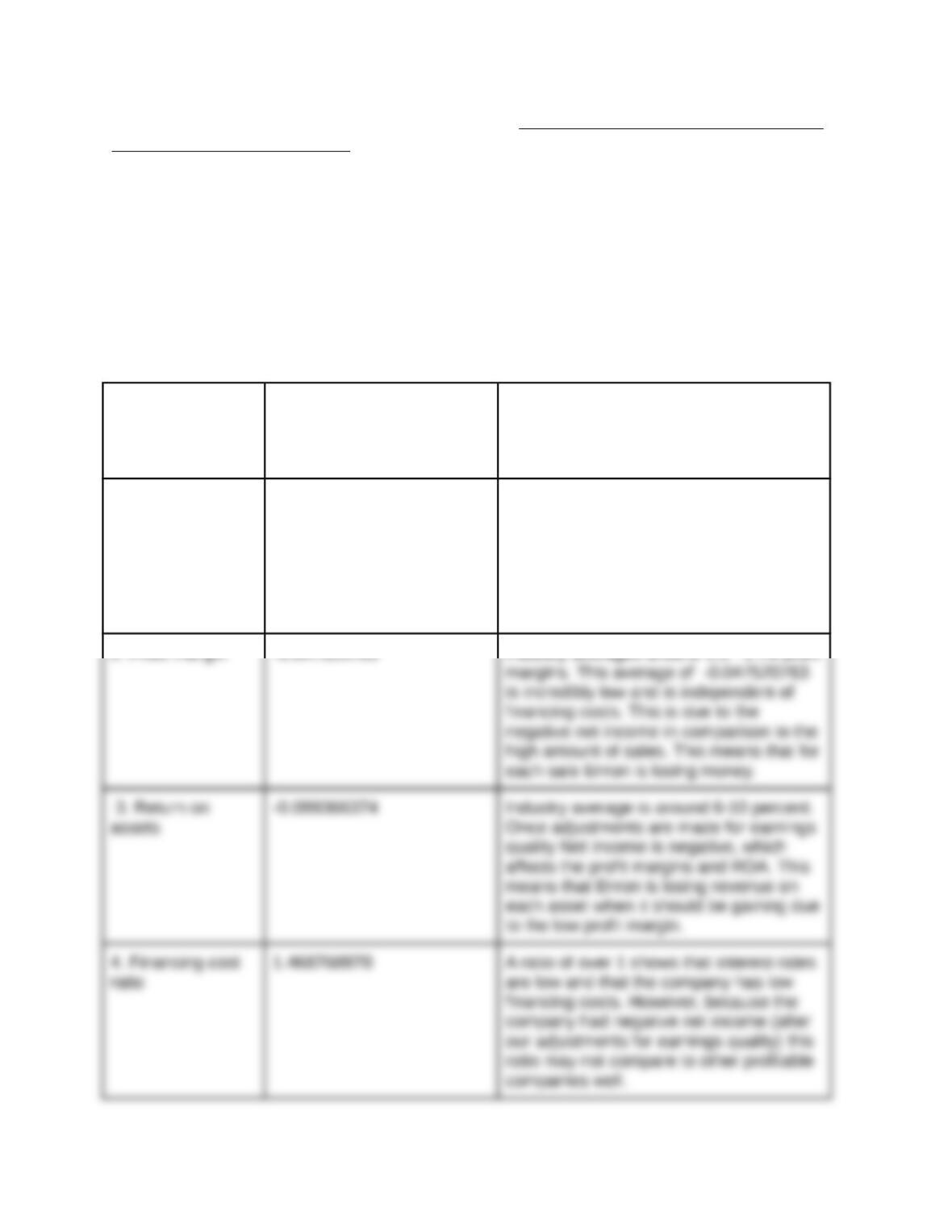

1. Asset turnover 2.091009666 The larger the number, the more able the

company is to create sales with their

asset base. The industry average is 2.11.

Enron is within industry averages, which

means that sales are healthy and that

Enron is able to create sales with their

asset base.