BUS803 Financial Econometrics

Lab 6: Regression with Serial Correlation

Prepared by Stephanie Mark (301406963) & Uchechukwu Anyakora (301356939)

Feb 5, 2020

Outline

1. Find two data series that are likely to be correlated and exhibit serial correlation and/or

heteroscedasticity of returns. You can use any of the data from the previous labs, or find

other data.

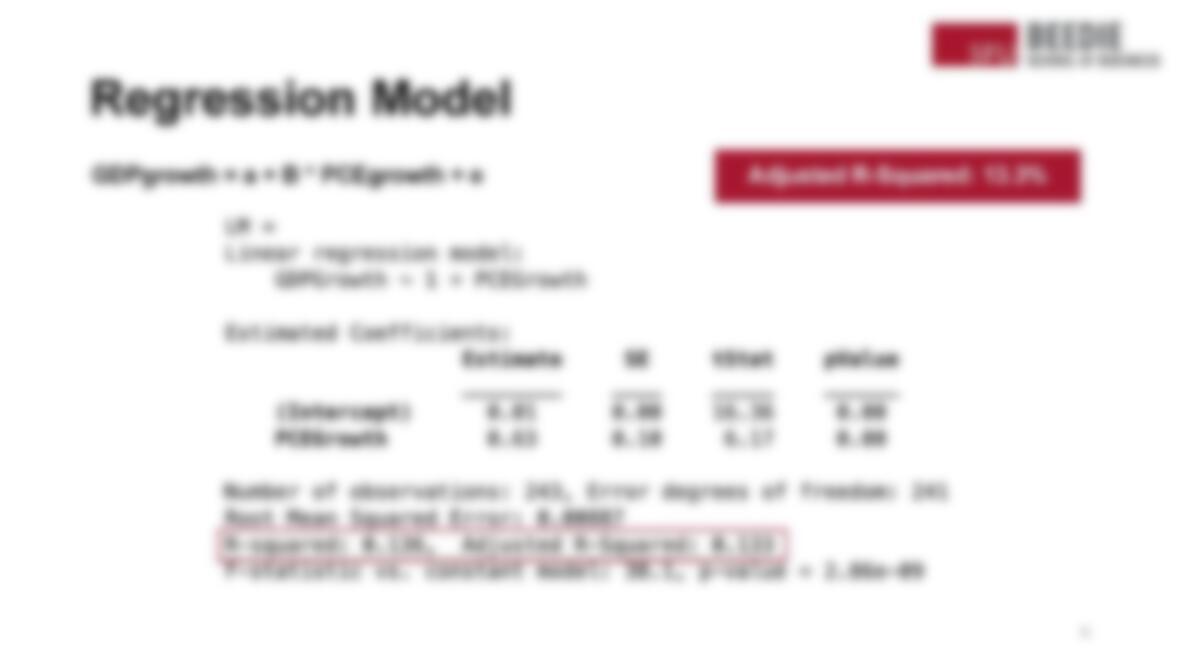

2. Estimate a regression model using one of the variables as a dependent variable and the

other one as an independent variable.

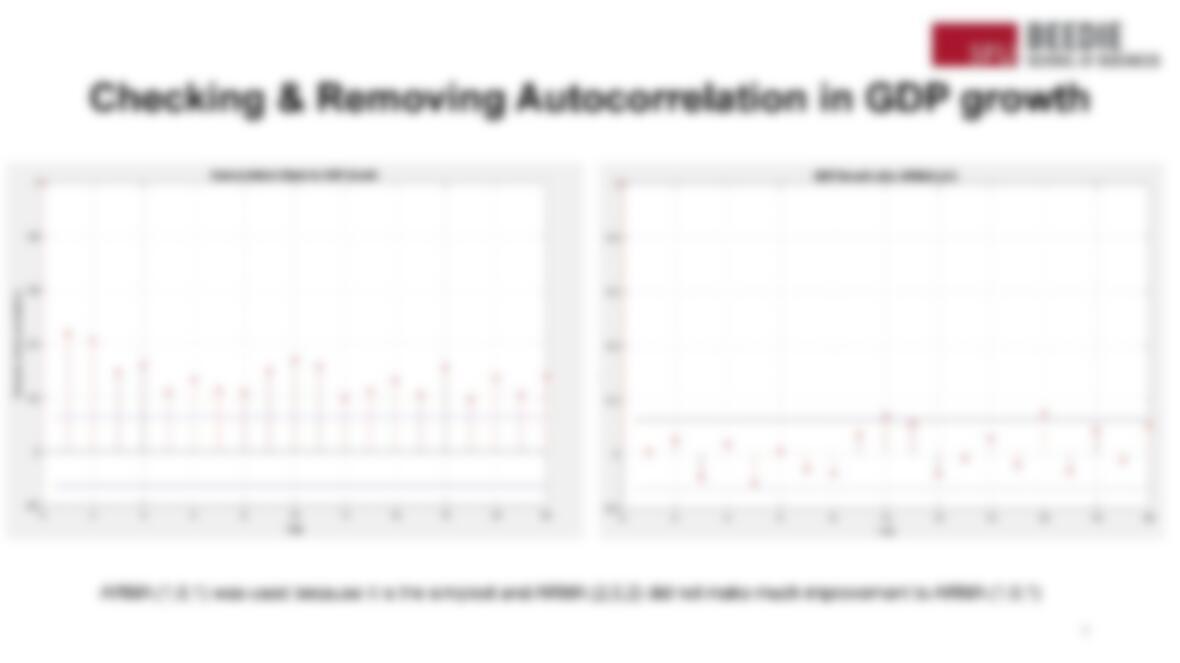

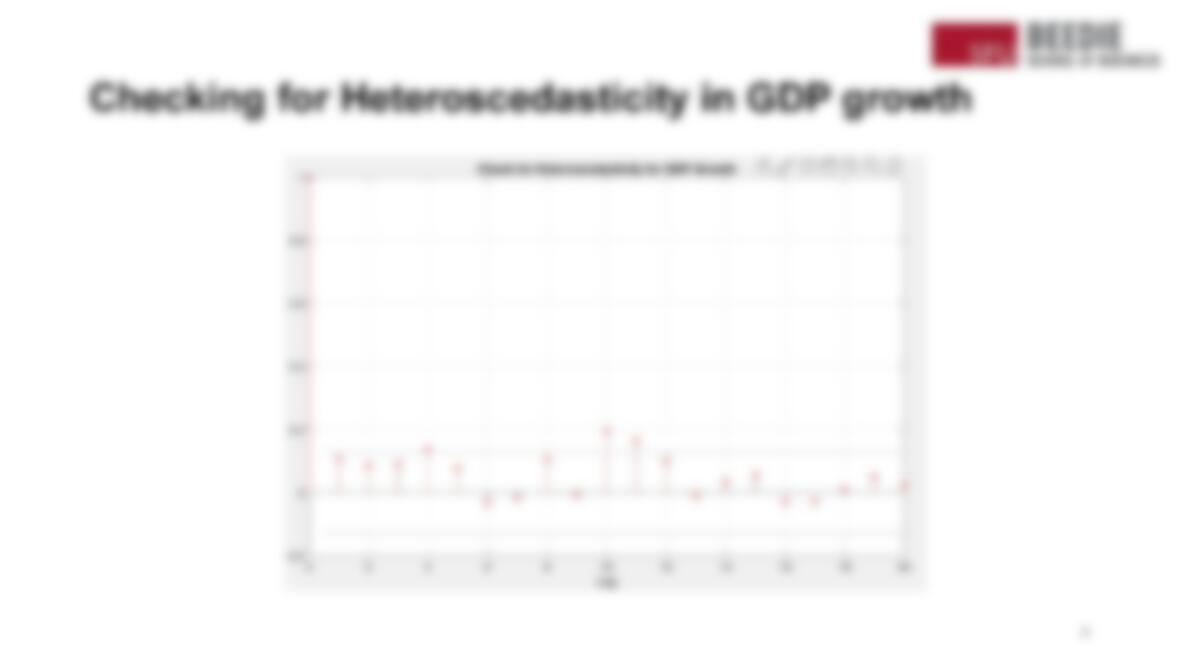

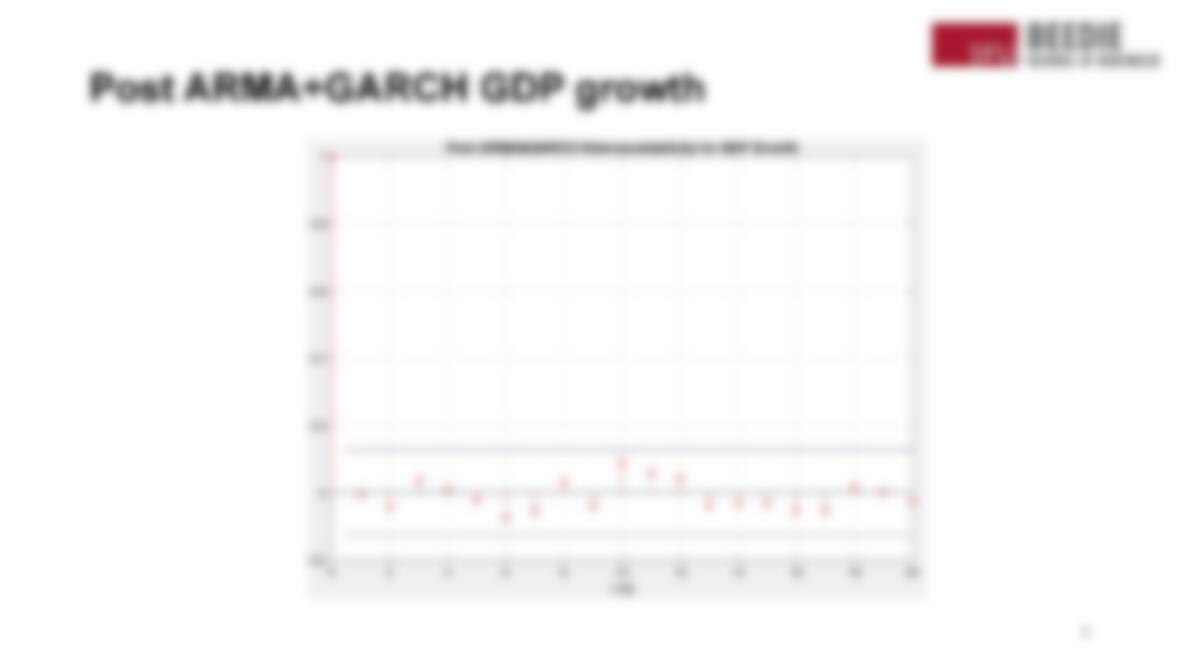

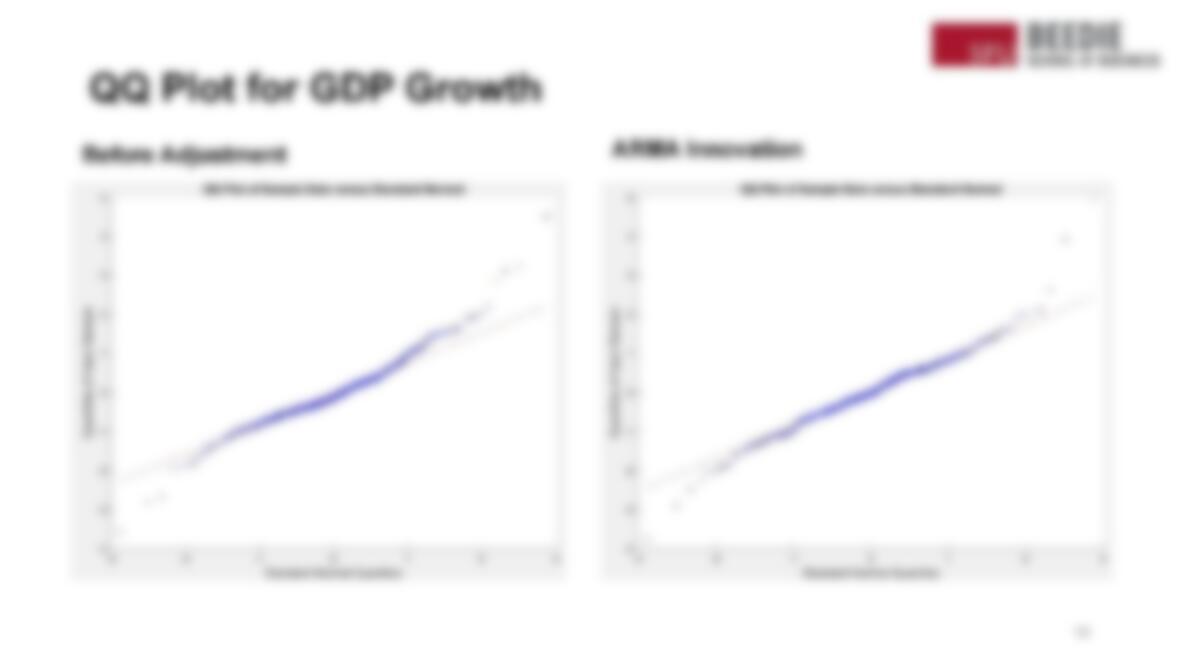

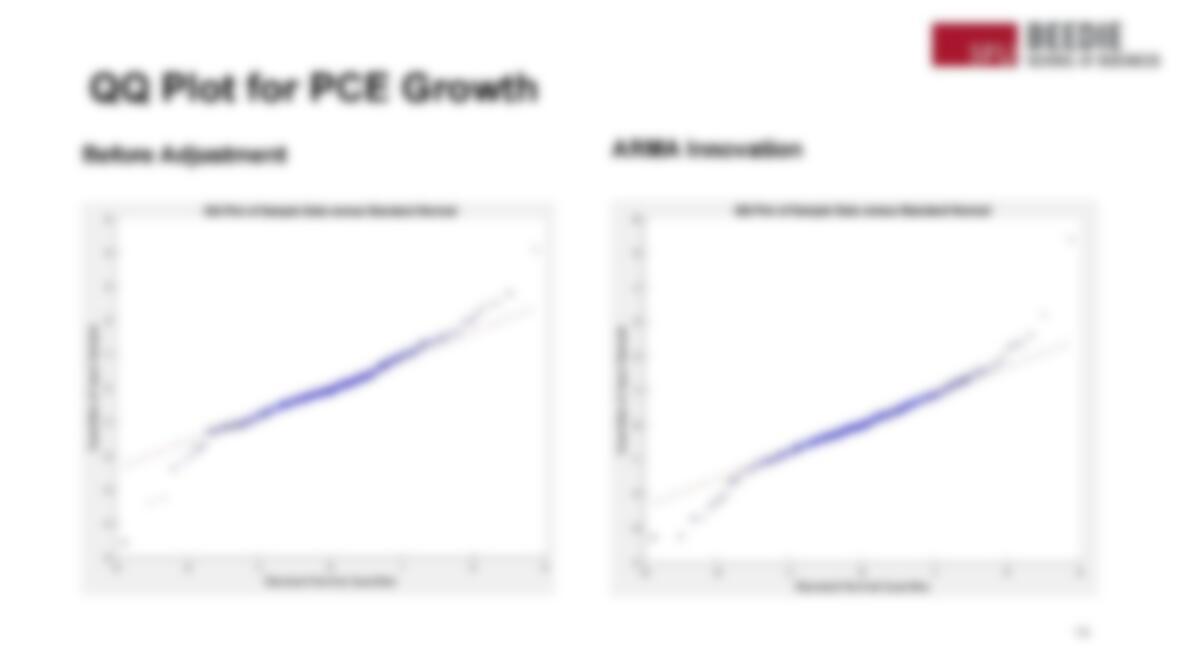

3. Estimate an ARMA/GARCH model for each data series separately to remove any serial

correlation or heteroscedasticity.

4. Re-estimate the regression from Step 2 above using the standardized residuals from the

ARMA/GARCH models. Compare the results from Step 2 and Step 4.

2

Data Selection

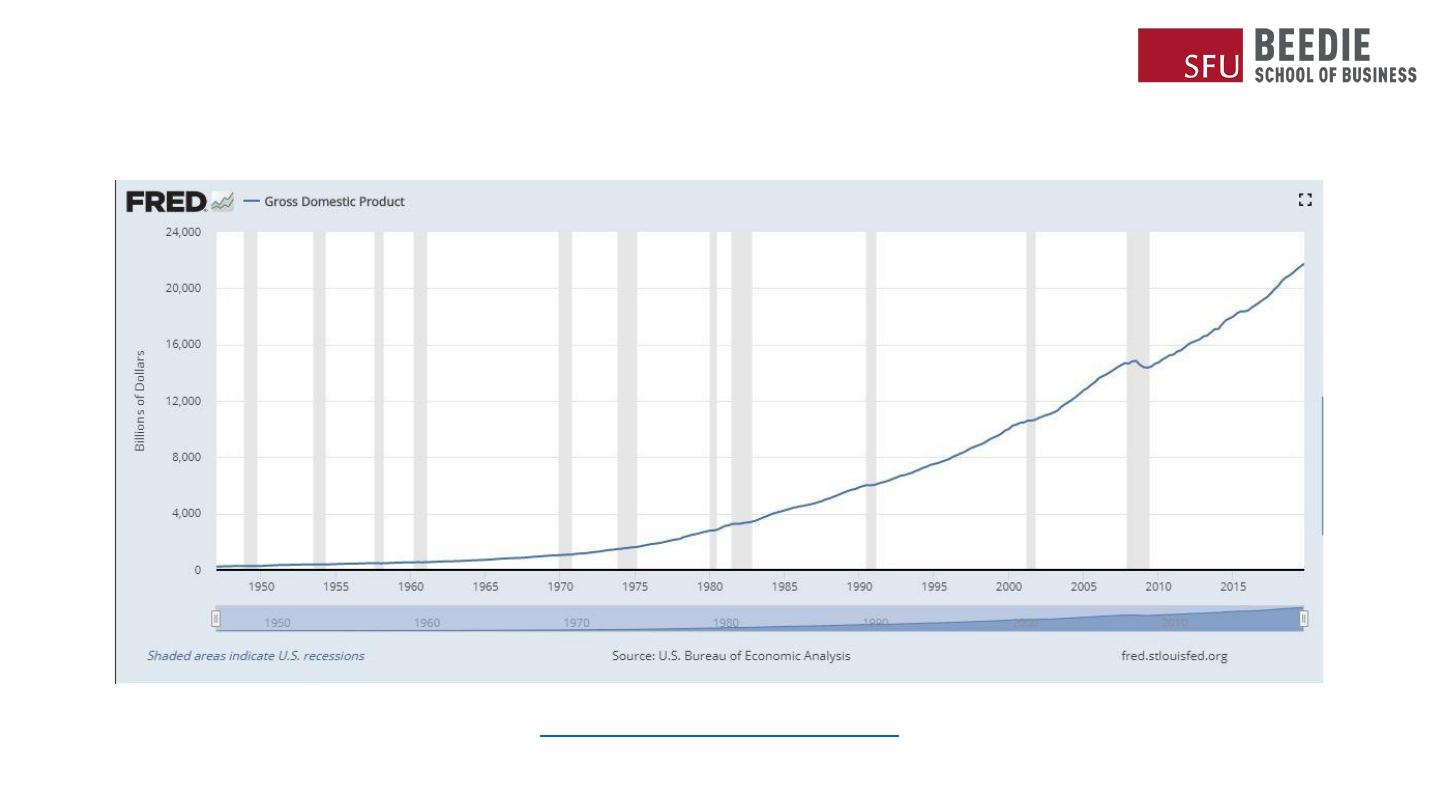

●We used GDP and personal

consumption expenditure as correlation

will exist between them

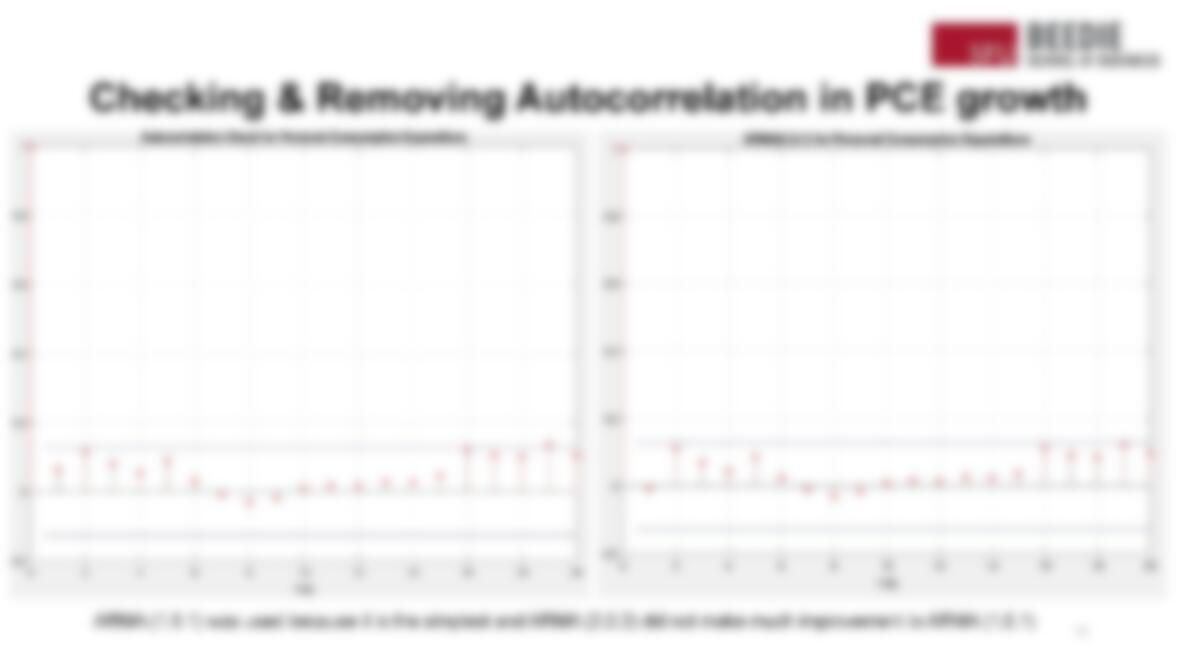

●There’s evidence that there is mild positive

autocorrelation in the growth of GDP

○It means that if GDP grows faster

than average in one period, there is a

tendency for it to grow faster than

average in the following periods

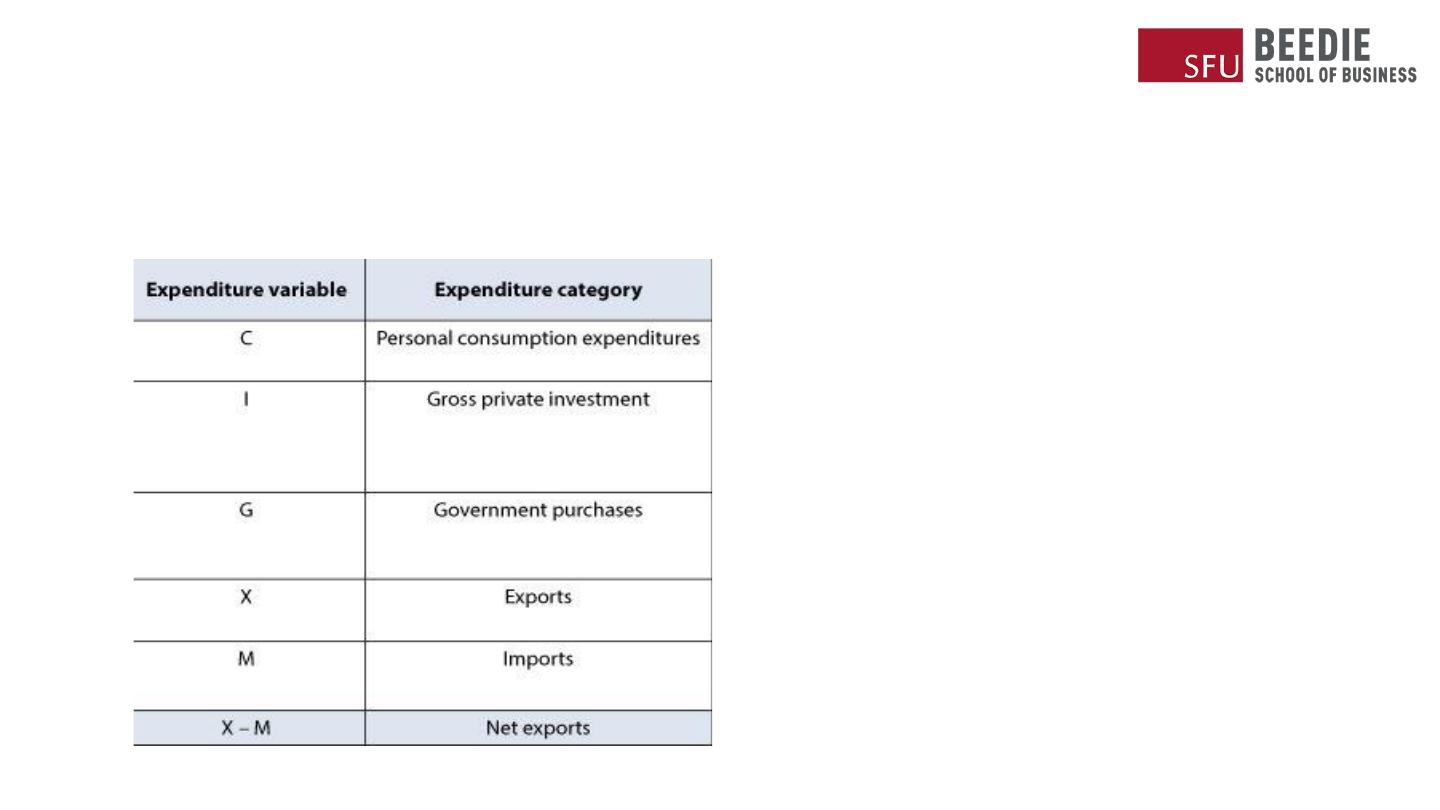

GDP = C + I + G + (X – M)

3

GDP Trend

https://fred.stlouisfed.org/series/GDP

4

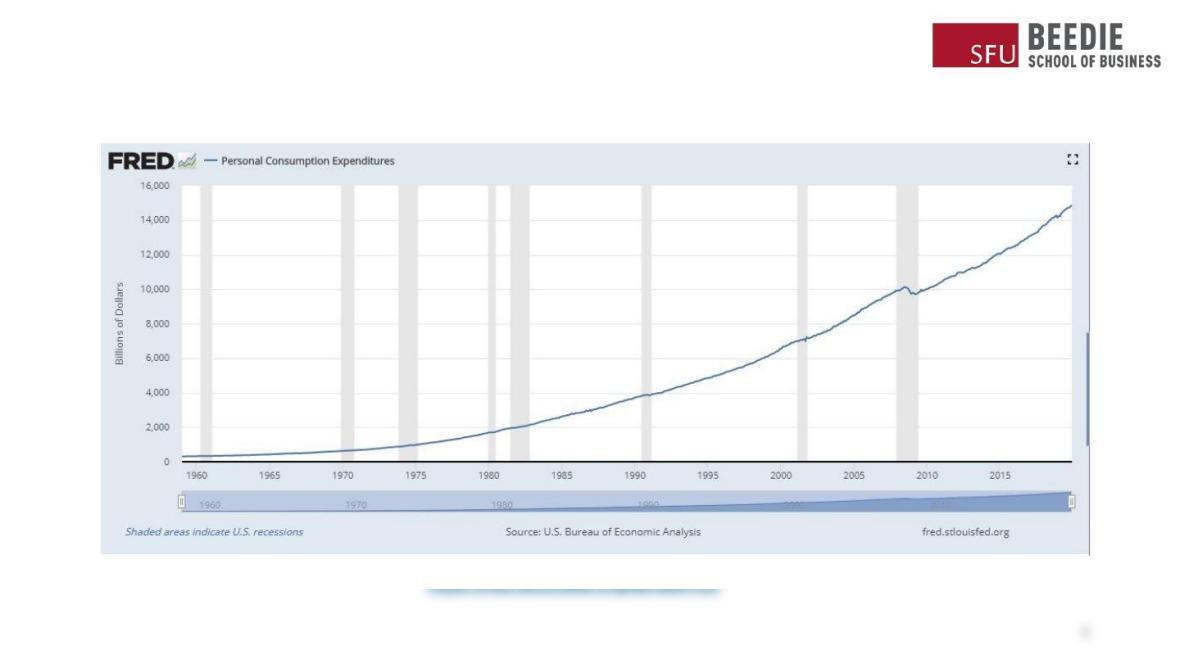

Personal Consumption Expenditure Trend