CORPORATE FINANCE

1

CORPORATE

FINANCE

The key responsibilities of the

CFO

The two main parts of CF are allocation (investment) and financing,

corresponding to the A&L sides of the balance sheet. The ultimate objective is to

maximize the shareholders’ wealth: achieve the highest return on the projects

and ensure the cheapest financing. Evaluation of the investment projects is

based on the discounted cash flows, which are diferent from the accounting

profits (e.g. because of depreciation). The real options approach takes into

account that managers can influence the CFs after the beginning of the project.

Applying similar methods, one can value the company.

The company can be restructured from private to a public one via IPO, and

vice versa. Another type of structural change comes from M&As. The company’s

goal is to acquire the companies bringing synergy gains and those undervalued

due to the inefficient management. The best defence from the acquisition is to

maximize its own value.

The goal of corporate governance is to internalize the external efects, balance

the economic interests of all stakeholders. In well-functioning fnancial markets,

this maximizes shareholder value.

Typical CF

questions:

How to measure the project’s worth for the company?

Are companies’ market prices justified? (e.g., dot-coms)

How to choose among the projects given the budget constraint and

external

effects?

How to account for risks associated with the project?

o Systematic vs company-specific risks

Are risks always bad?

Is it good to have volatile oil prices?

o Yes, if managers have flexibility in the future decisions.

Should we invest now in a project, which seems unprofitable (has negative

NPV)?

o Probably, yes. It may yield high profit in certain future scenarios (oil

pipeline)

Should we invest now in a project, which is profitable (has positive NPV)?

o Probably, not. It may be even more profitable next period (gold extraction)

Should we give managers higher salaries or higher bonuses?

o Bonuses encourage higher performance, but may also lead to

the

manipulations and excessive risk-taking.

Does it matter how to finance the project: by debt or by equity?

Would you like the company to have much debt?

o Yes, to minimize taxes and to discipline the managers. Not too much, to

avoid

bankruptcy.

Should the company borrow money from banks or issue bonds?

o The company can renegotiate the terms of bank credit.

Would you like the company to pay high dividends? (e.g., Microsoft)

CORPORATE FINANCE

2

o Yes, if too much managerial discretion (Surgut). No, because of

double

taxation and signalling that the company has no valuable inv projects.

How will the market react to the share buyback?

o The company signals that its shares are

undervalued. How will the market react to the new

equity issue?

o Usually negatively: either the company’s shares are overvalued, or it

needs to

fnance a new inv project.

How should the company communicate with the market? Always provide

precise

info in time?

What drives the company’s decision to go public? Why are there hardly any

IPOs

in Russia?

Would you like the company to grow via acquisitions?

o Yes, if the main motivation comes form synergy gains, and

not

empire-building.

Specifics of

corporation

Do not take the current form of corporations and stock markets as given, it is

an endogenous outcome!

Advantages of corporation in comparison with sole proprietorship and

partnership:

Ltd liability: lesser risks for investors

o Crucial for development of stock markets and diversification

Easy transfer of ownership

o Promotes liquidity

Unlimited life

o Makes it easier to attract fnancing

Disadvantages:

Separation of ownership and control, the agency conflict

o Solved in two ways: US vs Germany

Double taxation

History: 1811, general act of incorporation in NY, specifying that all investors of

NY

corporations have limited liability

Not so obvious that limiting the freedom of contracts is good

Hot discussion at the time: could spur excessive risk taking

California was the last to copy in 1931

The Objective in Corporate

Finance

“If you don’t know where you are

going,

it does not matter how you get

there

”

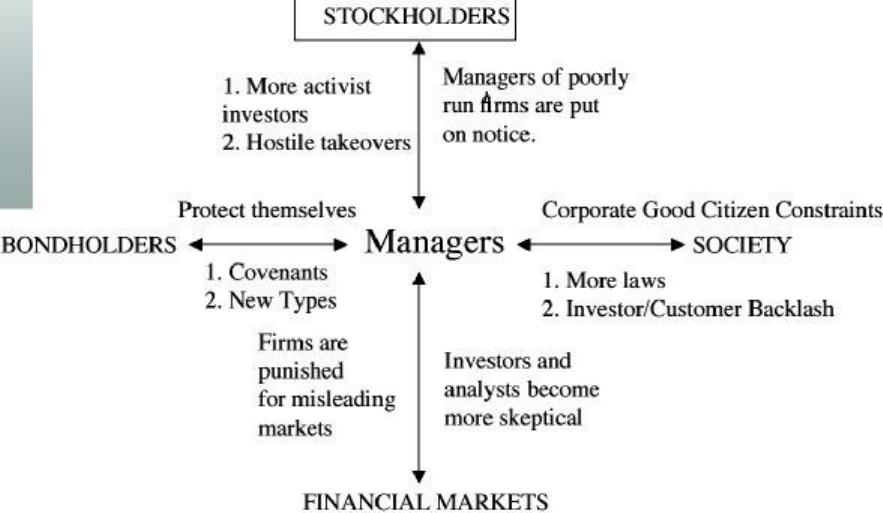

The Classical Viewpoint:

Van Horne: “In this book, we assume that the objective of the firm is to

maximize

its value to its stockholders”

Brealey & Myers: “Success is usually judged by value: Shareholders are made

better off by any decision which increases the value of their stake in the frm…

The

secret of success in financial management is to increase value.”

Copeland & Weston: The most important theme is that the objective of the firm

is

to maximize the wealth of its stockholders.”

Brigham and Gapenski: Throughout this book we operate on the assumption

that

the management’s primary goal is stockholder wealth maximization which

translates

into maximizing the price of the common stock.

Why focus on maximizing stockholder

wealth?

Stock price is easily observable and constantly updated (unlike other

measures of

performance, which may not be as easily observable, and certainly not

updated

as frequently).

If investors are rational (are they?), stock prices refect the wisdom of

decisions,

short term and long term, instantaneously.

The objective of stock price performance provides some very elegant theory

on:

o how to pick projects

o how to finance them

o how much to pay in dividends

The Classical Objective

Function

What can go

wrong?

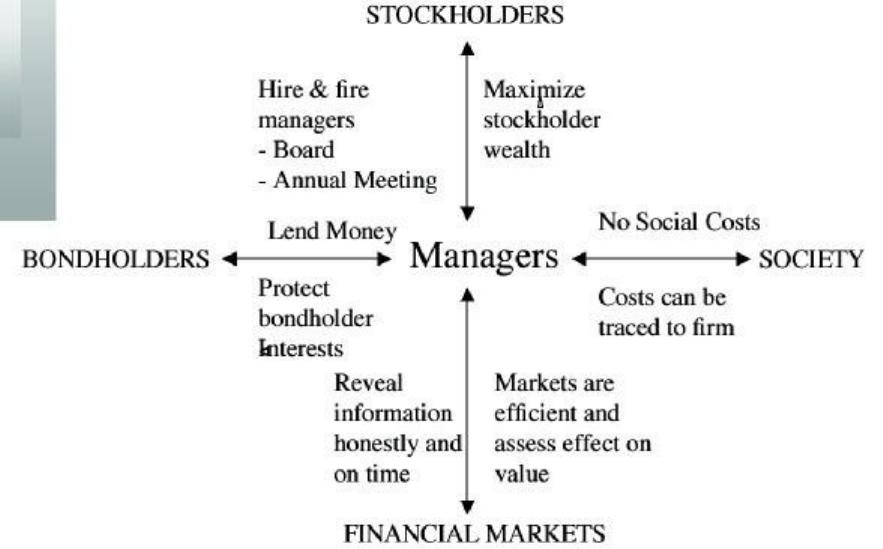

Traditional corporate fnancial theory breaks down when the

interests/objectives of the decision makers in the firm conflict with the

interests of stockholders.

o Bondholders (Lenders) are not protected against expropriation by

stockholders.

o Financial markets do not operate efficiently, and stock prices do not

reflect

the underlying value of the firm.

o Significant social costs can be created as a by-product of stock price

maximization.

Solutions:

Choose a diferent mechanism for corporate governance

Choose a diferent objective:

o Maximizing earnings / revenues / firm size / market share

o The key thing to remember is that these are intermediate objective

functions. To the degree that they are correlated with the long term

health

and value of the company, they work well. To the degree that they do

not,

the firm can end up with a disaster

Maximize stock price, but reduce the potential for conflict and breakdown:

o Making managers (decision makers) and employees into stockholders

o Providing information honestly and promptly to financial markets

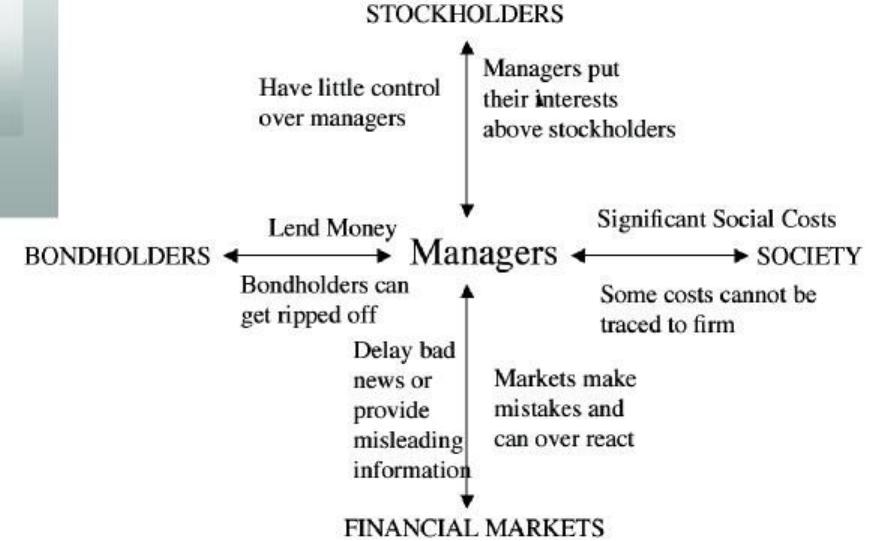

Counter

reaction

The strength of the stock price maximization objective function is its internal

self correction mechanism. Excesses on any of the linkages lead, if

unregulated, to counter actions which reduce or eliminate these excesses

managers taking advantage of stockholders has lead to a much more

active market for corporate control.

stockholders taking advantage of bondholders has lead to

bondholders protecting themselves at the time of the issue.

firms revealing incorrect or delayed information to markets has lead to

markets becoming more “skeptical” and

“

punitive

”

firms creating social costs has lead to more regulations, investor and

customer backlashes.

The Modified Objective Function

For publicly traded firms in reasonably efficient markets, where bondholders

(lenders) are protected:

o Maximize Stock Price: This will also maximize firm value

For publicly traded firms in inefficient markets, where bondholders are

protected:

o Maximize stockholder wealth: This will also maximize firm value, but

might not maximize the stock price

For publicly traded firms in inefficient markets, where bondholders are not

fully

protected

o Maximize firm value, though stockholder wealth and stock prices may

not

be maximized at the same point.

For private firms, maximize stockholder wealth (if lenders are protected) or

firm

value (if they are not)

Relation to investment theory

Use of CAPM to estimate the cost of capital

Option pricing approach for valuing investment projects (real options), equity

of

the firm, and bonds’ credit risk

CORPORATE FINANCE

6

Lecture 2. Analysis of financial

statements

The Firm’s Financial Statements

Balance Sheet

Income Statement

Statement of Cash Flows

Functions: providing

current status and past performance information to owners and creditors

a convenient way for owners and creditors to set performance targets &

to

impose restrictions on the managers of the frm

a convenient template for fnancial planning

Balance

Sheet

Assets ≡ Liabilities + Shareholder’s

Equity

Tabulates a company’s assets and liabilities at a specific point in time

o Info on value of the assets and the capital structure

Sorting of

o Assets by liquidity

o Liabilities by maturity

Assets and liabilities are represented by historical costs

o The original cost adjusted for improvements and aging = Book Value

o Avoid using market value, since is too volatile and easily manipulated

o Preference for underestimating value

Strict categorization into E or L: the liability must satisfy

o The obligation will lead to CF at some specified or determinable date

o The firm cannot avoid the obligation

o The transaction behind the obligation has already happened

However, important liabilities may be under-stated or omitted

Assets

Current Assets (Оборотные средства): will convert into cash within a year

o Cash

o Accounts Receivable (Счета к пол

у

чению)

Recognizing not collectible ones: reserves (danger of

manipulation!)

o Inventory (ТМЗ): valued by FIFO, LIFO, wdt-avg

LIFO increases costs and reduces taxes

LIFO reserve: difference between LIFO and FIFO valuations

Investments and Marketable Securities (Рыночные цб)

o Minority passive / active investment (<20% / 20-50% of the ownership):

BV

or MV

o If majority active investment (>50%): include in the consolidated

balance

sheet

Intangible Assets (Нематериальные активы): amortized over expected life