Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

Corporate finance

Eighth Edition

Chapter 9

The cost of capital and

capital structure

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

2

An Overview of the Cost of Capital

•The cost of capital acts as a link between the

firm’s long-term investment decisions and the

wealth of the owners as determined by investors

in the marketplace.

•It is the “magic number” that is used to decide

whether a proposed investment will increase or

decrease the firm’s stock price.

•Formally, the cost of capital is the rate of return

that a firm must earn on the projects in which it

invests to maintain the market value of its

stock.

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

WHAT IS THE COST OF CAPITAL?

•All providers of finance require returns.

•The required return will reflect the risk of the

investment and the returns of alternatives.

•Companies need information about the cost of

different sources of finance in order to find

the overall cost of finance and to make

investment and financing decisions.

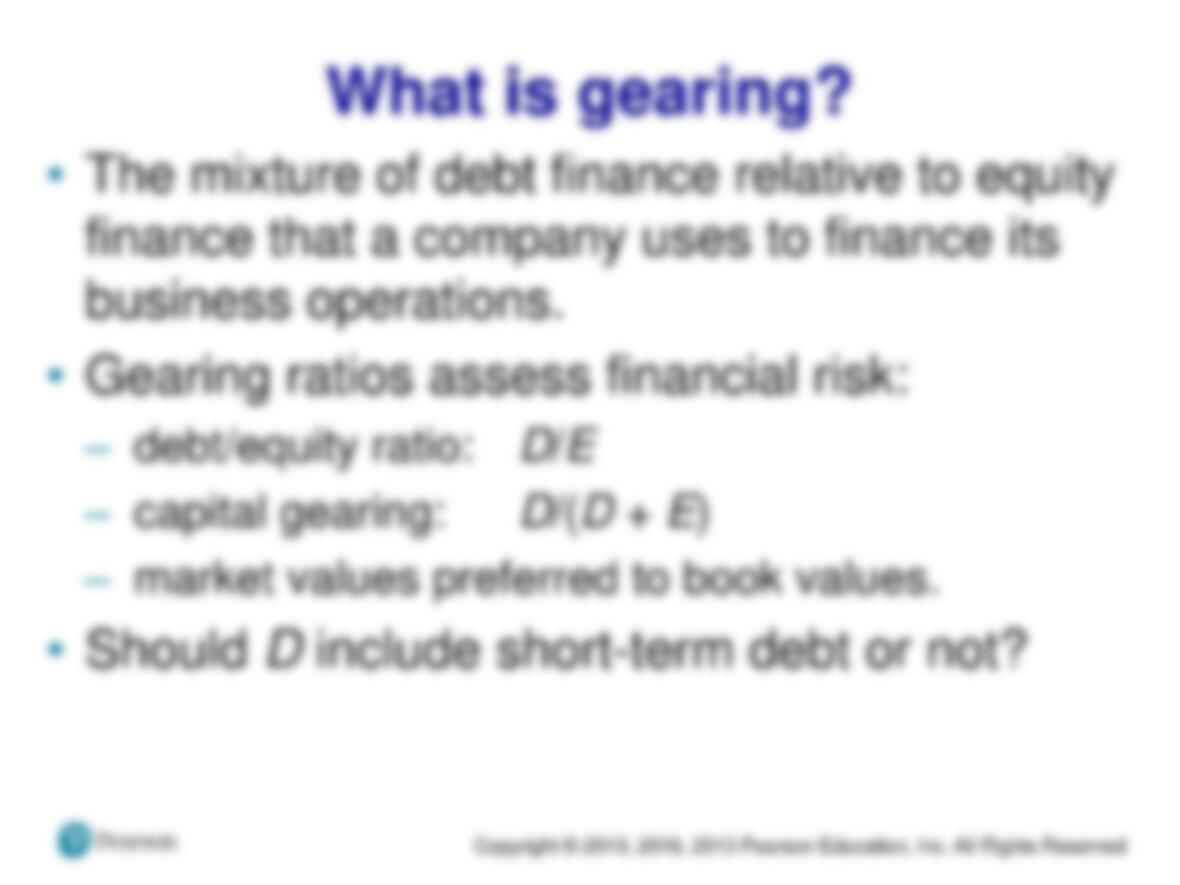

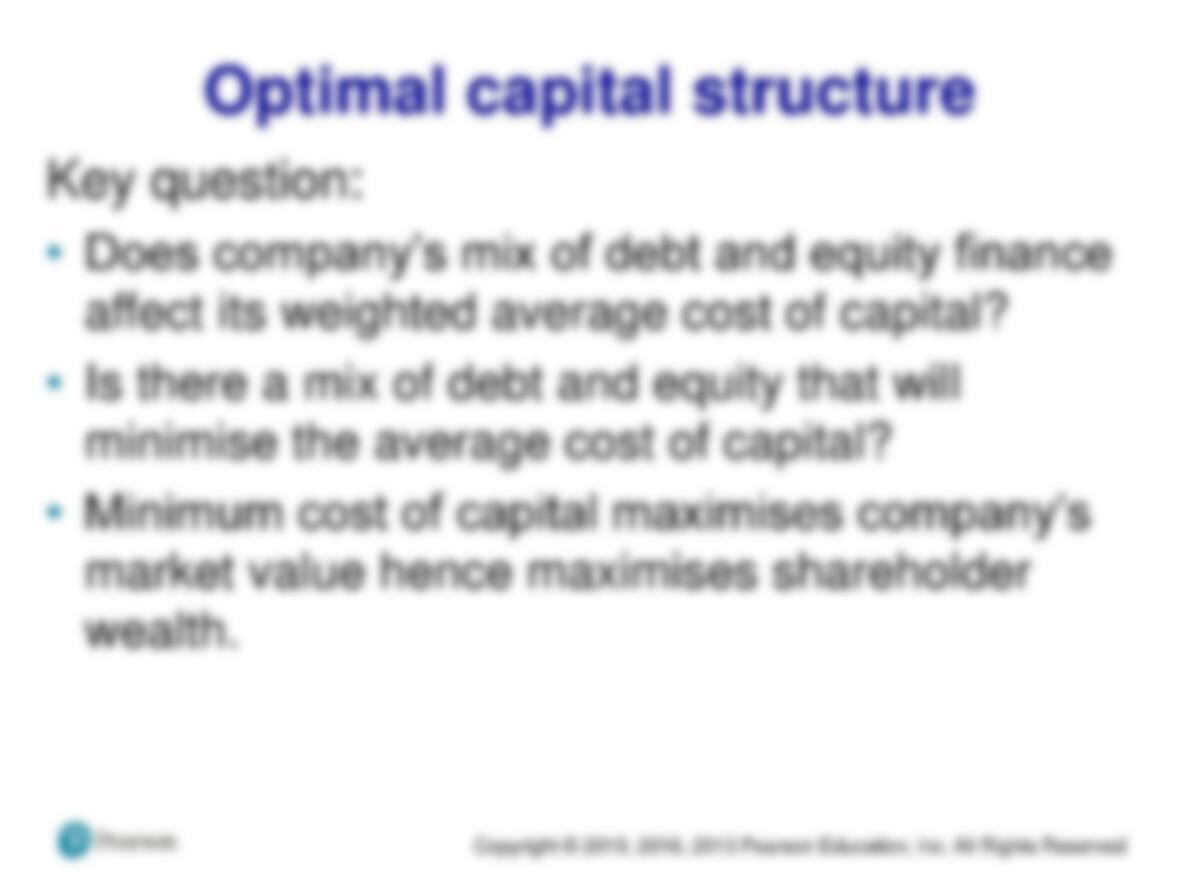

•Perhaps an ‘optimum’ capital structure exists

which a firm can seek to achieve.

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

THE FIRM’S COSTS OF CAPITAL

•For Investors, the rate of return on a security is a

of investing.

•For Financial Managers, that same rate of return

is a way of raising funds (financing) that are

needed to operate the firm, adjusted by flotation

costs and taxes.

•In other words, the cost of raising funds is the

firm’s cost of capital.

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

THE FIRM’S COST OF CAPITAL

•In an efficient market, investor’s required return and

expected return are the same.

•Cost of capital from the firm’s perspective is

actually the expected return from investor’s

perspective, adjusted for the effects of taxes

and flotation costs.

•Afirm’s cost of capital serves as the linkage

between financing and investing decisions. The

cost of capital becomes the hurdle rate that must

be achieved by an investment before it will increase

shareholders’ wealth.

•It is the firm’s required return on investment

projects under consideration.

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

HOW CAN THE FIRM RAISE CAPITAL?

•Bonds / Debentures & Bank Loans

•Preferred Stock

•Common Stock

–Each of these offers a different rate of return

to investors.

–This return is a cost to the firm.

– “Cost of capital” actually refers to the

weighted cost of capital – a weighted average

cost of financing sources.

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

WHAT IS THE COST OF CAPITAL?

•All providers of finance require returns.

•The required return will reflect the risk of the

investment and the returns of alternatives.

•Companies need information about the cost of

different sources of finance in order to find

the overall cost of finance and to make

investment and financing decisions.

•Perhaps an ‘optimum’ capital structure exists

which a firm can seek to achieve.

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

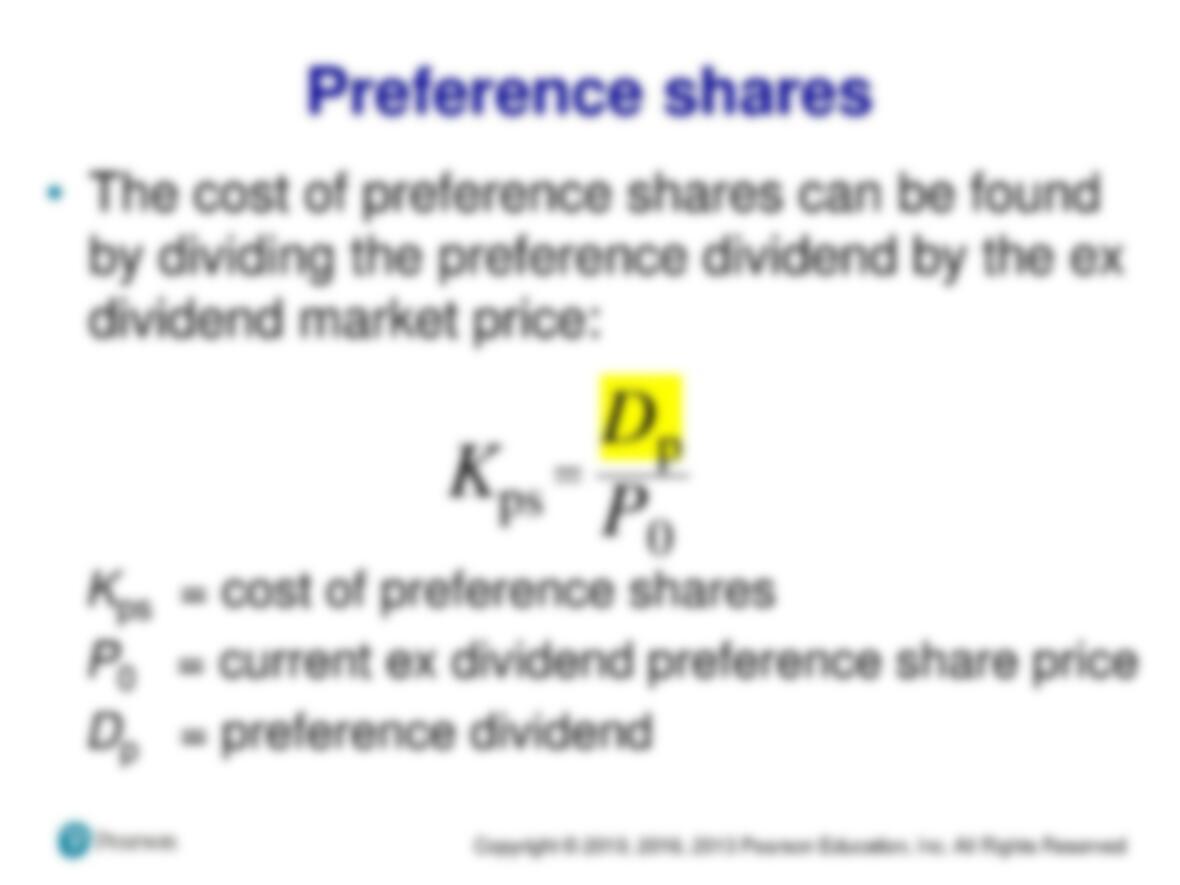

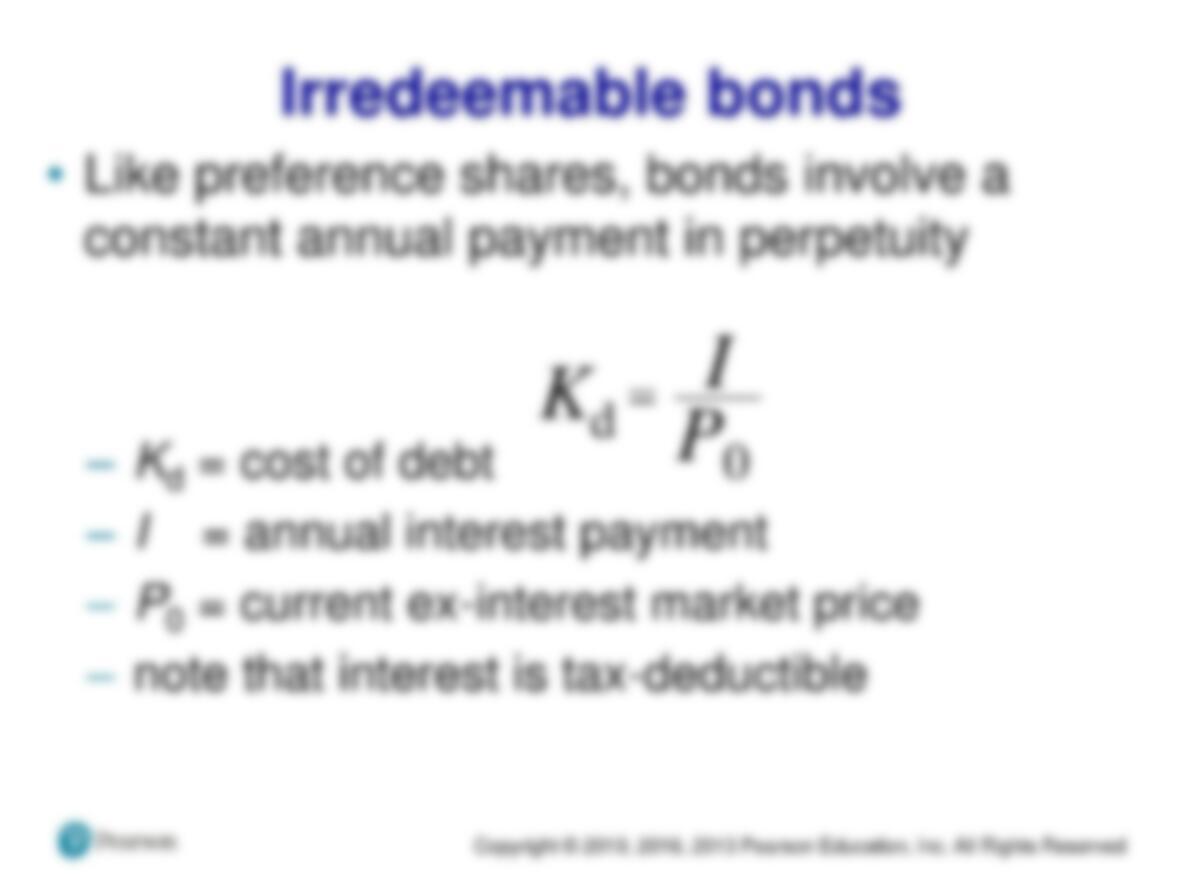

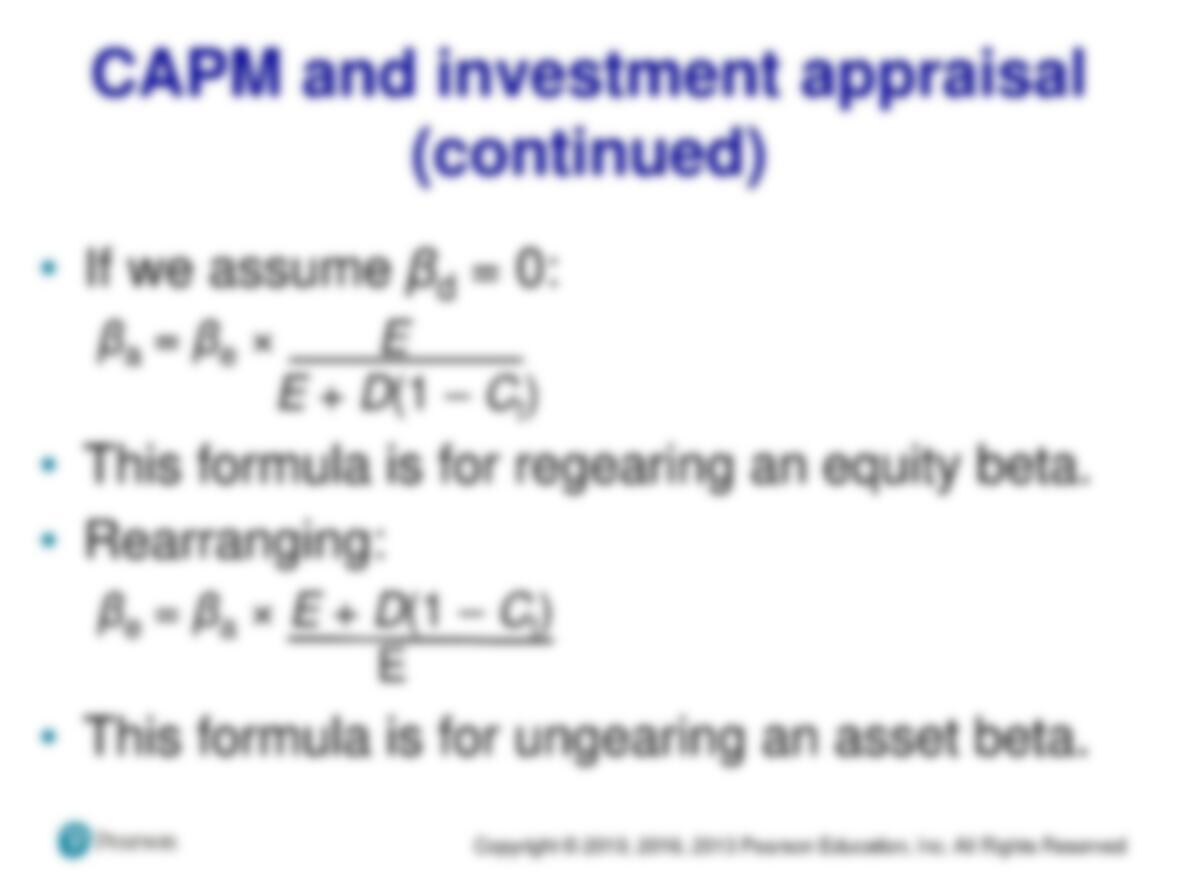

Ordinary shares

•The cost of equity can be found from the

rearranged dividend growth model:

Ke = cost of equity

P0= the current ex dividend share price

D1= the dividend received each year

g= the expected growth rate of dividends

g

P0

D1

Ke+

=

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

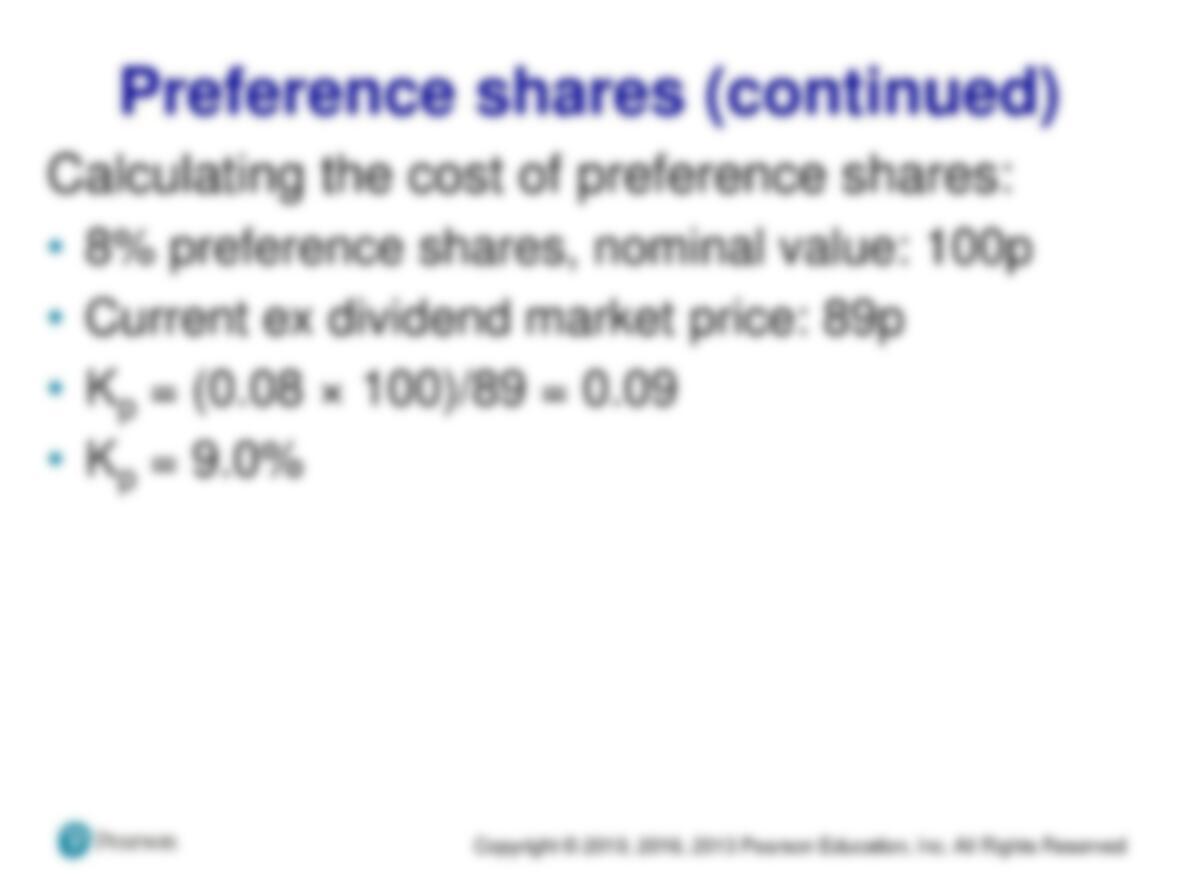

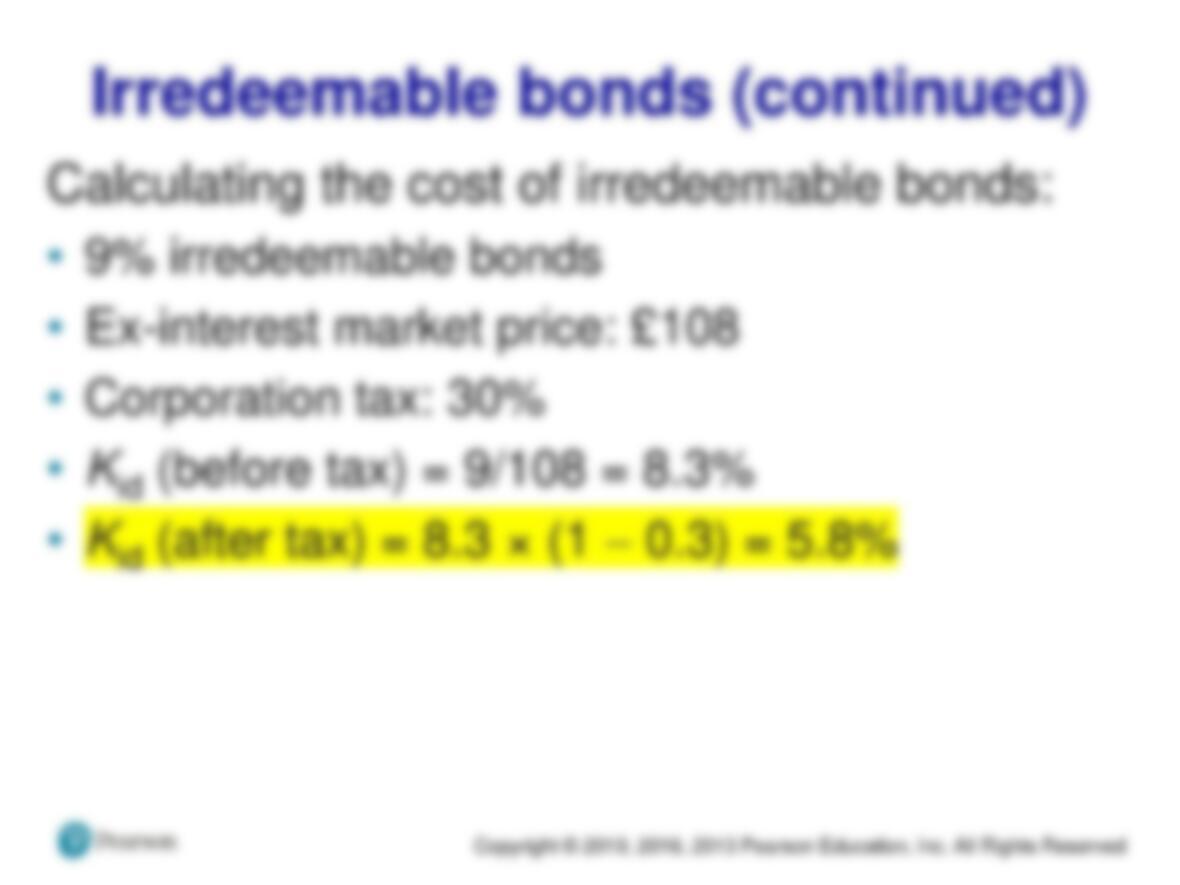

Ordinary shares (continued)

Calculating Keusing dividend growth model:

•Current ex dividend share price = 417p

•Current dividend per share = 23p

•Expected dividend growth rate = 5%

•Next year’s dividend (D1) = 23 × 1.05 = 24.2p

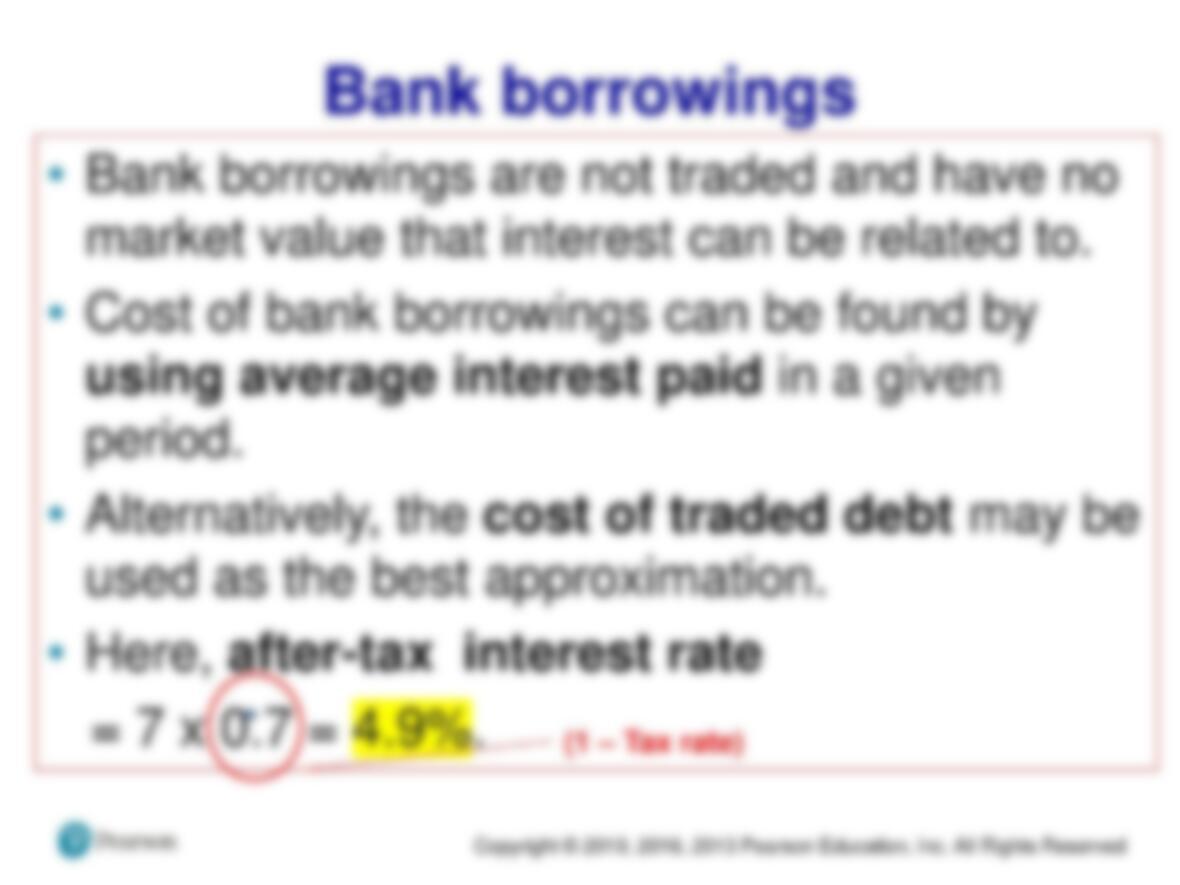

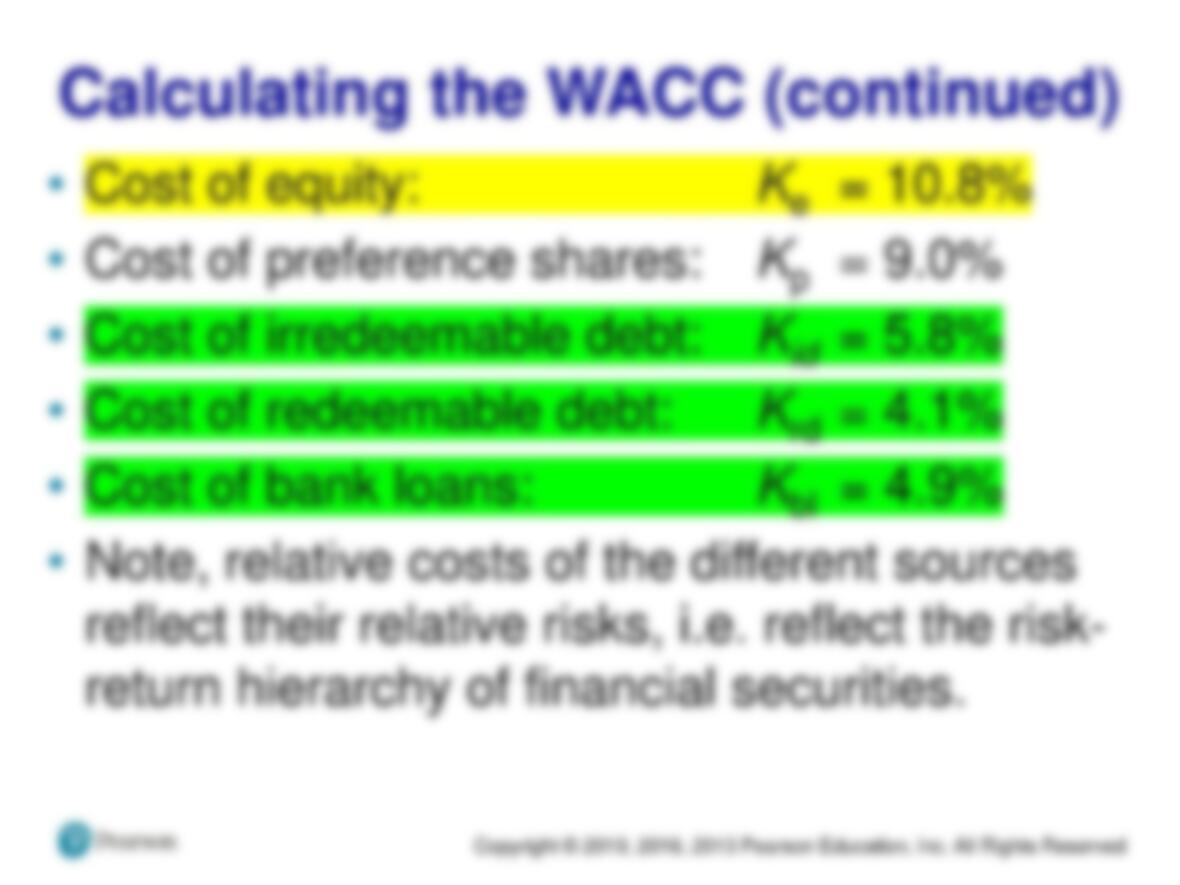

•Ke= (24.2/417) + 0.05 = 0.058 + 0.05 = 0.108

•Ke= 10.8%

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

Ordinary shares (continued)

•The cost of equity can also be found from the

CAPM:

Rj= Rf+ βj(Rm–Rf) = Ke

where:

Rm= return of the market

Rf= risk-free rate of return

(Rm–Rf) = equity risk premium

βj= beta value of ordinary share

Copyright © 2019, 2016, 2013 Pearson Education, Inc. All Rights Reserved

•The CAPM differs from dividend valuation

models in that it explicitly considers the firm’s

risk as reflected in beta.

•On the other hand, the dividend valuation

model does not explicitly consider risk.

•Dividend valuation models use the market

price (P0)as areflection of the expected risk-

return preference of investors in the

marketplace.

Cost of Common Stock

Retained earnings

•Retained earnings have an opportunity

cost which is equal to the cost of equity.

•The cost of retained earnings can thus be