5-1

CHAPTER 5

Income Statement and Related Information

ASSIGNMENT CLASSIFICATION TABLE

Topics Questions

Brief

Exercises Exercises Problems Cases

1. Income measurement

concepts.

1, 2, 3, 4, 5,

6, 7, 8, 9, 10,

12, 13, 18,

20, 28, 31,

32, 33

3, 5, 6, 7,

9

2. Computation of net

income from balance

sheets and selected

accounts.

1 1, 2, 7

3. Single-step income

statements; earnings

per share.

11, 23, 24 2, 8 3, 4, 5, 6, 7,

10, 15, 16

2, 3, 4, 5 1, 9

4. Multiple-step income

statements.

17 3 4, 5, 6, 8, 11 1, 4

5. Extraordinary items;

accounting changes;

discontinued

operations; prior

period adjustments;

errors.

14, 15, 16,

27, 29

4, 5, 6, 7 9, 10, 11,

12, 13

3, 4, 5, 6,

7, 8

4, 7, 8,

10

6. Retained earnings

statement.

30 9, 10 10, 11, 12,

16

1, 2, 4, 5,

6, 7

7. Intraperiod tax

allocation.

21, 22, 25,

26, 27

8. Comprehensive

income.

34 11 14, 15, 16 11

9. Disposal of a

component (discon-

tinued operations).

35

5-2

ASSIGNMENT CHARACTERISTICS TABLE

Item Description

Level of

Difficulty

Time

(minutes)

E5-1 Computation of net income. Simple 18-20

E5-2 Income statement items. Simple 25-35

E5-3 Single-step income statement. Moderate 20-25

E5-4 Multiple-step and single-step. Simple 30-35

E5-5 Multiple-step and extraordinary items. Moderate 30-35

E5-6 Multiple-step and single-step. Moderate 30-40

E5-7 Compute Income, EPS. Simple 15-20

E5-8 Multiple-step statement with retained earnings. Simple 30-35

E5-9 Earnings per share. Simple 20-25

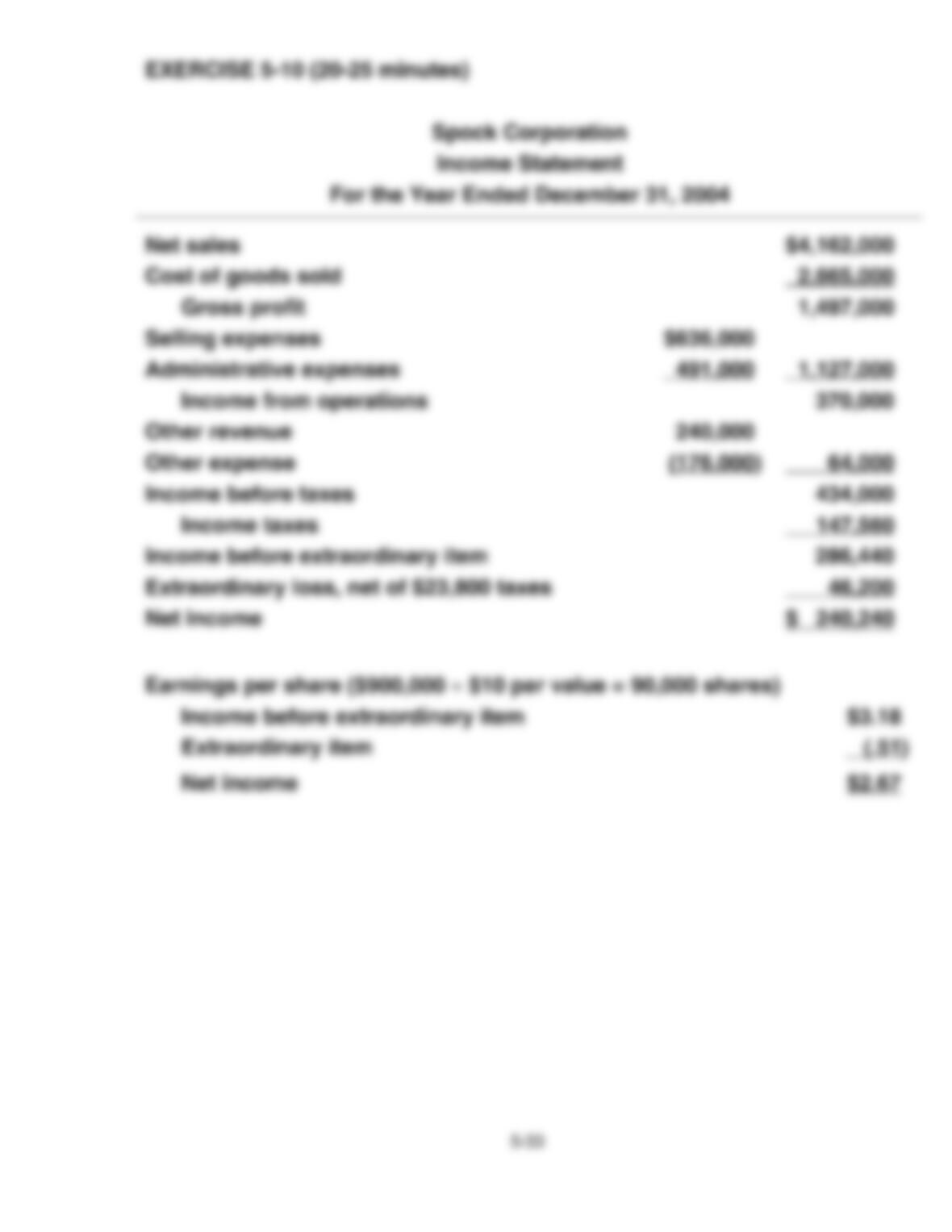

E5-10 Condensed income statement—periodic inventory

method.

Moderate 20-25

E5-11 Retained earnings statement. Simple 20-25

E5-12 Earnings per share. Moderate 15-20

E5-13 Change in accounting principle—depreciation. Moderate 15-20

E5-14 Comprehensive income. Simple 15-20

E5-15 Comprehensive income. Moderate 15-20

E5-16 Single step statement, retained earnings statement,

comprehensive income.

Moderate 30-35

P5-1 Multi-step income, retained earnings. Moderate 30-35

P5-2 Single-step income, retained earnings—periodic

inventory.

Simple 25-30

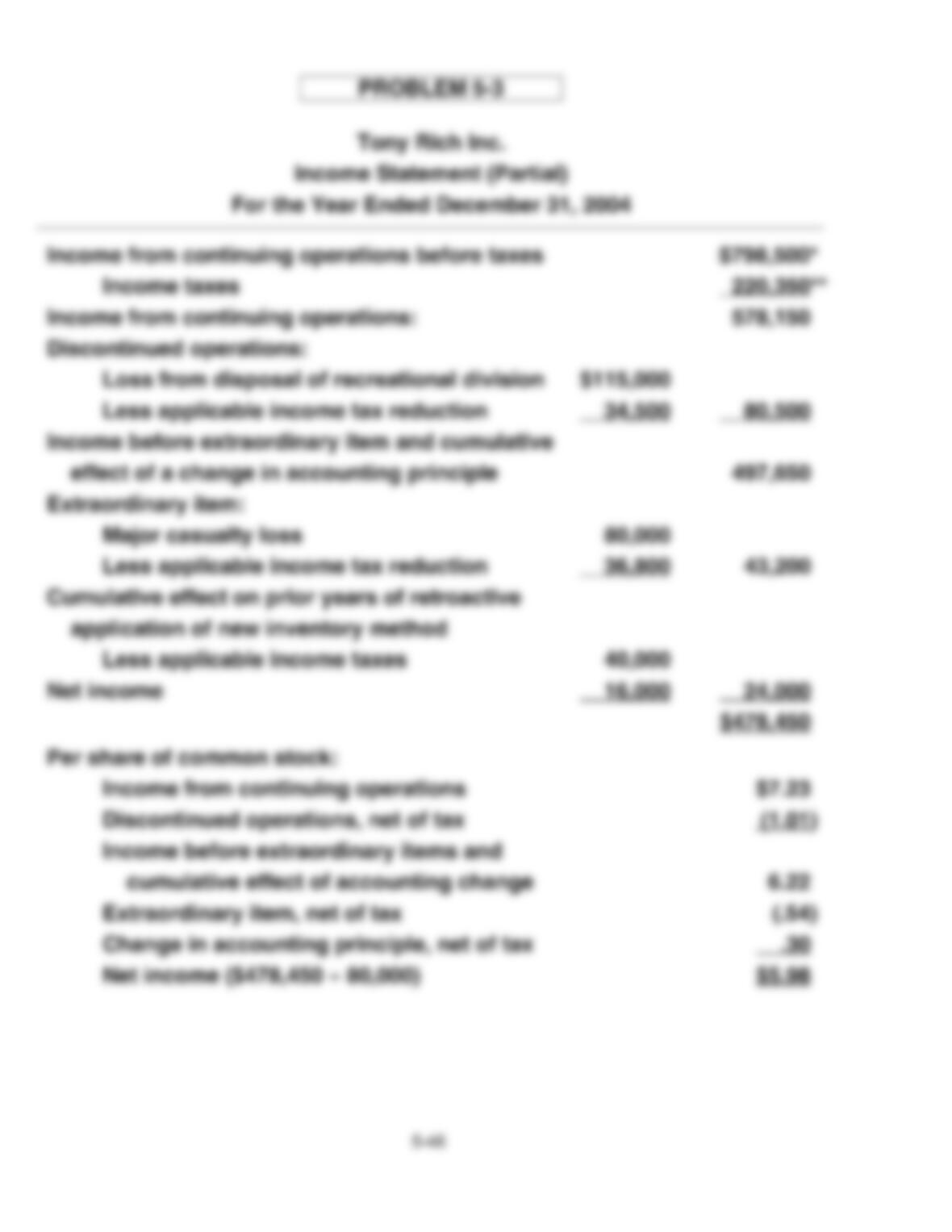

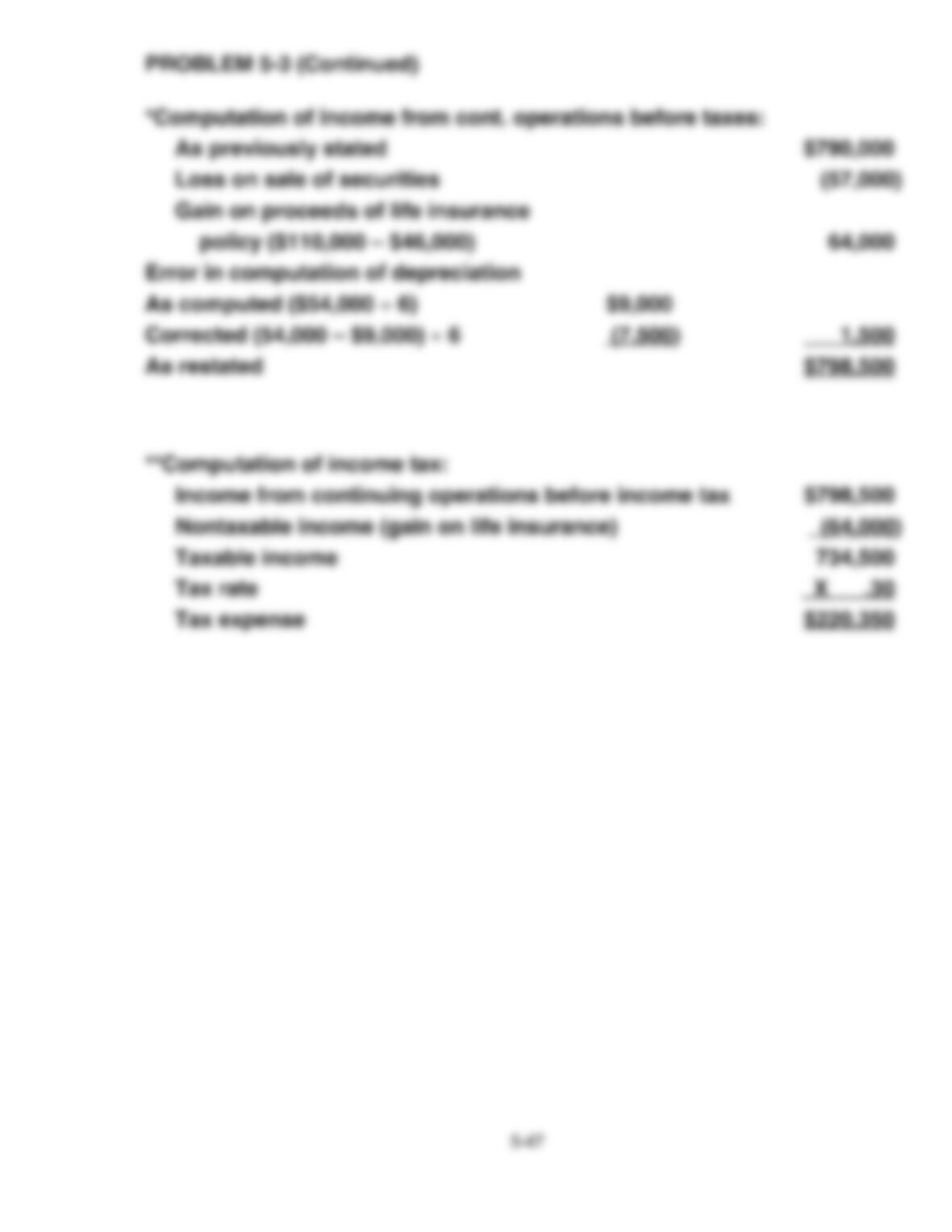

P5-3 Irregular items. Moderate 30-40

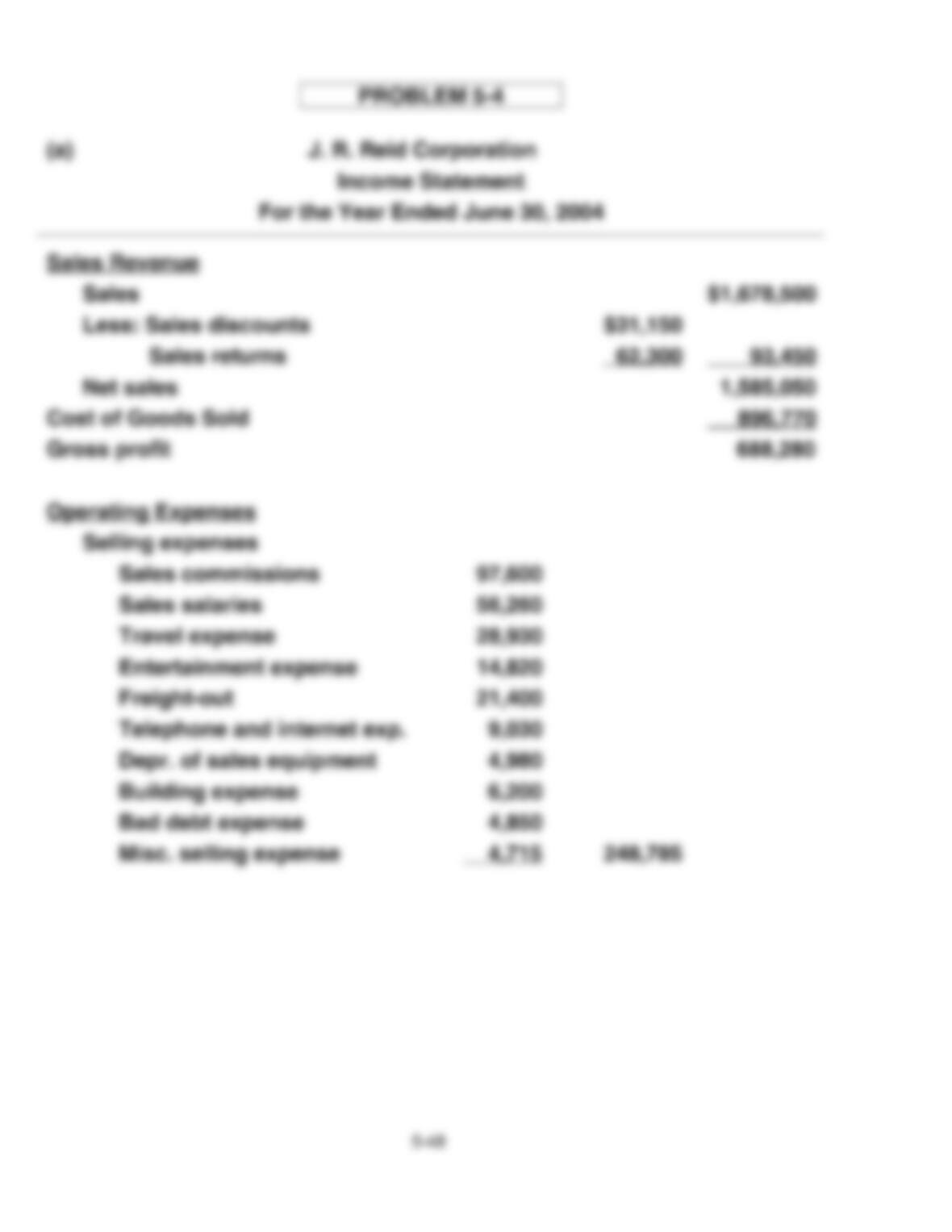

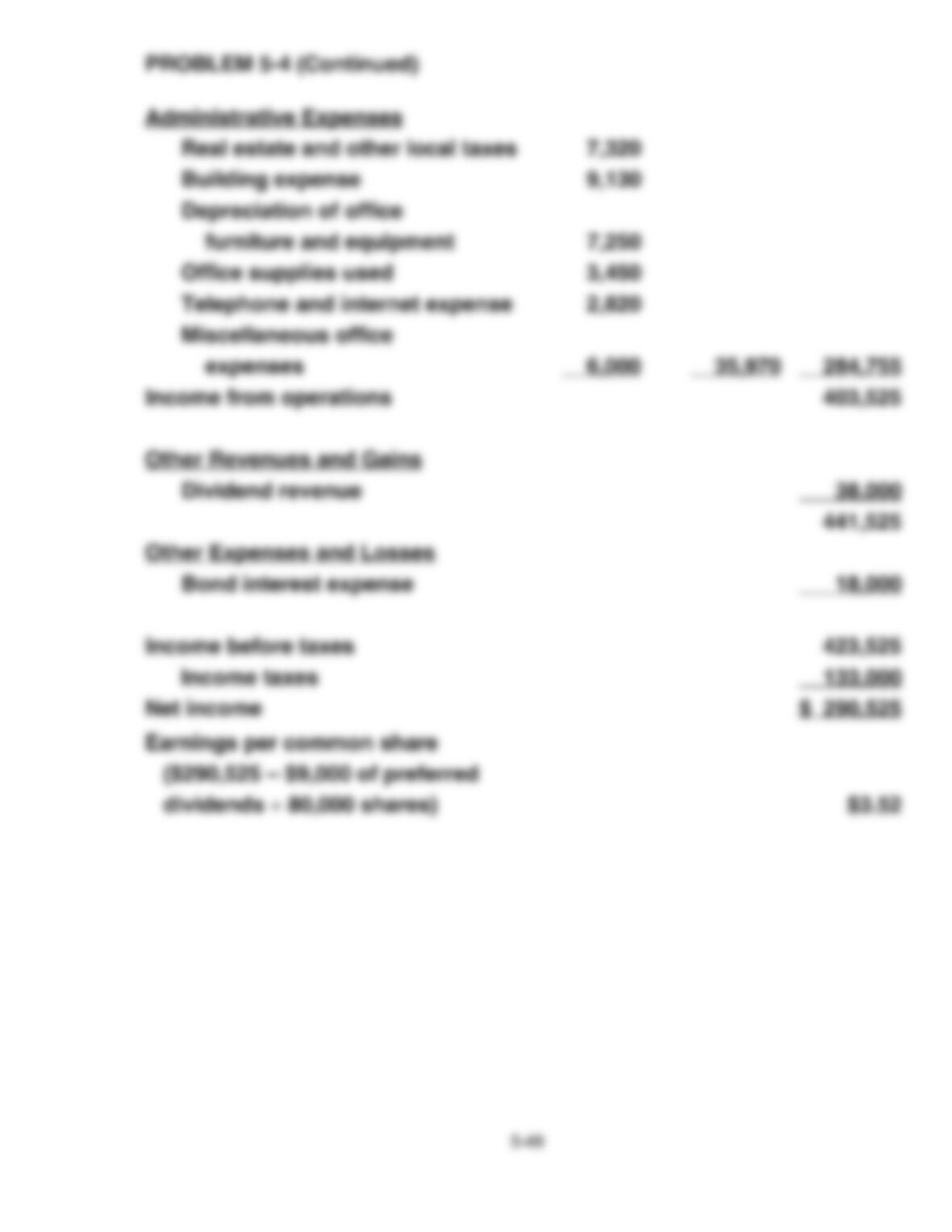

P5-4 Multi- and single-step income, retained earnings. Moderate 45-55

P5-5 Irregular items. Moderate 20-25

P5-6 Retained earnings statement, prior period adjustments. Moderate 25-35

P5-7 Income statement and irregular items. Complex 40-50

P5-8 Income statement and irregular items. Moderate 25-35

C5-1 Identification of income statement deficiencies. Simple 20-25

C5-2 Identify income statement deficiencies. Simple 10-15

C5-3 All-inclusive vs. current operating. Moderate 25-35

C5-4 Extraordinary items. Moderate 20-25

C5-5 Earnings management—ethical issues. Moderate 20-25

C5-6 Earnings management Simple 15-20

C5-7 Income reporting items. Simple 25-30

C5-8 Identification of extraordinary items. Moderate 30-35

C5-9 Identification of income statement weaknesses. Moderate 30-40

C5-10 Classification of income statement items. Moderate 20-25

C5-11 Comprehensive income. Simple 10-15

5-3

ANSWERS TO QUESTIONS

1. The income statement is important because it provides investors and creditors with information

that helps them predict the amount, timing, and uncertainty of future cash flows. It helps

investors and creditors predict future cash flows in a number of different ways. First, investors

and creditors can use the information on the income statement to evaluate the past

performance of the enterprise. Second, the income statement helps users of the financial

statements to determine the risk (level of uncertainty) of income–revenues, expenses, gains,

and losses–and highlights the relationship among these various components.

It should be emphasized that the income statement is used by parties other than investors and

creditors. For example, customers can use the income statement to determine a company’s

ability to provide needed goods or services, unions examine earnings closely as a basis for

salary discussions, and the government uses the income statements of companies as a basis

for formulating tax and economic policy.

2. Information on past transactions can be used to identify important trends that, if continued,

provide information about future performance. If a reasonable correlation exists between past

and future performance, predictions about future earnings and cash flows can be made. For

example, a loan analyst can develop a prediction of future performance by estimating the rate

of growth of past income over the past several periods and project this into the next period.

Additional information about current economic and industry factors can be used to adjust the

trend rate based on historical information.

3. Some situations in which changes in value are not recorded in income are:

a) Unrealized gains or losses on investments,

b) Changes in the market values of long term liabilities, such as bonds payable,

c) Changes in value of property, plant and equipment, such as land, natural resources, or

equipment,

d) Changes in the values of intangible assets such as customer goodwill, brand value, or

intellectual capital.

Note that some of these omissions arise because the items (e.g., brand value) are not

recognized in financial statements, while others (value of land) are recorded in financial

statements but measurement is at historical cost.

4. Some situations in which application of different methods or estimates lead to comparison

problems include:

a. Inventory methods – LIFO vs. FIFO,

b. Depreciation Methods – Straight-line vs. accelerated,

c. Accounting for long-term contracts – percentage of completion vs. completed contract,

d. Estimates of useful lives or salvage values for depreciable assets,

e. Estimated of bad debts,

f. Estimates of warranty returns.

5. The transaction approach focuses on the activities that have occurred during a given period

and instead of presenting only a net change, a description of the components that comprise the

change is included. In the capital maintenance approach, therefore, only the net change

(income) is reflected whereas the transaction approach not only provides the net change

(income) but the components of income (revenues and expenses). The final net income figure

should be the same under either approach given the same valuation base.

5-4

Questions Chapter 5 (Continued)

6. Earnings management is often defined as the planned timing of revenues, expenses, gains and

losses to smooth out bumps in earnings. In most cases, earnings management is used to

increase income in the current year at the expense of income in future years. For example,

companies prematurely recognize sales before they are complete in order to boost earnings.

Earnings management can also be used to decrease current earnings in order to increase

income in the future. The classic case is the use of “cookie jar” reserves, which are

established, by using unrealistic assumptions to estimate liabilities for such items as sales

returns, loan losses, and warranty returns.

7. Earnings management has a negative effect on the quality of earnings if it distorts the

information in a way that is less useful for predicting future cash flows. Within the Conceptual

Framework, useful information is both relevant and reliable. However, earnings management

reduces the reliability of income, because the income measure is biased (up or down) and/or

the reported income that is not representationally faithful to that which it is supposed to report

(e.g., volatile earnings are made to look more smooth).

8. Caution should be exercised because many assumptions and estimates are made in

accounting and the income figure is a reflection of these assumptions. If for any reason the

assumptions are not well-founded, distortions will appear in the income reported. The

objectives of the application of generally accepted accounting principles to the income

statement are to measure and report the results of operations as they occur for a specified

period without recognizing any artificial exclusions or modifications.

9. The term “quality of earnings” refers to the credibility of the earnings number reported.

Companies that use aggressive accounting policies report higher income numbers in the short-

run. In such cases, we say that the quality of earnings is low. Similarly, if higher expenses are

recorded in the current period, in order to report higher income in the future, then the quality of

earnings is considered low.

10. The major distinction between revenues and gains (or expenses and losses) depends on the

typical activities of the enterprise. Revenues can occur from a variety of different sources, but

these sources constitute the entity’s ongoing major or central operations. Gains also can arise

from many different sources, but these sources occur from peripheral or incidental transactions

of an entity. The same type of distinction is made between an expense and a loss.

11. The advantages of the single-step income statement are: (1) simplicity and conciseness, (2)

probably better understood by the layperson, (3) emphasis on total costs and expenses, and

net income, and (4) does not imply priority of one revenue or expense over another. The

disadvantages are that it does not show the relationship between sales and cost of goods sold

and it does not show other important relationships and information, such as income from

operations, income before taxes, etc.

12. Operating items are the expenses and revenues which relate directly to the principal activity of

the concern; they are revenues realized from, or expenses which contribute to, the sale of

goods or services for which the company was organized. The nonoperating items result from

secondary activities of the company. They are not directly related to the principal activity of the

company but arise from subsidiary activities.

5-5

Questions Chapter 5(Continued)

13. The current operating performance income statement contains only the revenues and usual

expenses of the current year, with all unusual gains or losses or material corrections of prior

periods’ revenues and expenses appearing in the retained earnings statement. The all-

inclusive income statement includes all items of income and expense and gains and losses

recognized in the accounts during the year. The retained earnings statement then would

include only the beginning balance, the net amount transferred from income summary,

dividends, and transfers to and from appropriations.

In APB Opinion No. 9, the APB recommended a modified all-inclusive income statement,

excluding from the income statement only those items, few in number, which meet the criteria

for prior period adjustments and which would thus appear as adjustments to the beginning

balance in the retained earnings statement. Subsequently a number of pronouncements have

reinforced this position.

14. Items that are considered prior period adjustments should be charged or credited to the

opening balance of retained earnings. Prior period adjustments would ordinarily be either

corrections of errors made in a prior period discovered after issuance of financial statements for

that period or retroactive adjustments required or permitted by an FASB Statement or APB

Opinion.

15. (a) This might be shown in the income statement as an extraordinary item if it is a material,

unusual, and infrequent gain realized during the year. However, in general and in accord

with APB Opinion No. 30, this transaction would normally not be considered

extraordinary, but would be shown in the nonoperating section of a multiple-step income

statement. If unusual or infrequent but not both, it should be separately disclosed in the

income statement.

(b) The bonus should be shown as an operating expense in the income statement. Although

the basis of computation is a percentage of net income, it is an ordinary operating

expense to the company and represents a cost of the service received from employees.

(c) If the amount is immaterial, it may be combined with the depreciation expense for the year

and included as a part of the depreciation expense appearing in the income statement. If

the amount is material, it should be shown in the retained earnings statement as an

adjustment to the beginning balance of retained earnings, treated as a prior period

adjustment.

(d) This should be shown in the income statement. One treatment would be to show it in the

statement as a deduction from the rent expense, as it reduces an operating expense and

therefore is directly related to operations. Another treatment is to show it in the other

revenues and gains section of the income statement.

(e) Assuming that a provision for the loss had not been made at the time the patent

infringement suit was instituted, the loss should be recognized in the current period in

computing net income. It may be reported as an unusual loss.

(f) This should be reported in the income statement, but not as an extraordinary item

because it relates to usual business operations of the firm.

5-6

Questions Chapter 5 (Continued)

16. (a) The remaining book value of the equipment should be depreciated over the remainder of

the five-year period. The additional depreciation ($425,000) is not a correction of an error

and is not shown as an adjustment to retained earnings.

(b) The loss should be shown as an extraordinary item, assuming that it is unusual and

infrequent.

(c) Should be shown either as other expenses or losses or in a separate section,

appropriately labeled as an unusual item, if unusual or infrequent but not both. It should

not be shown as an extraordinary item.

(d) Assuming that a receivable had not been recorded in the previous period, the gain should

be recognized in the current period in computing net income, but not as an extraordinary

item.

(e) A correction of error should be considered a prior period adjustment and the beginning

balance of Retained Earnings should be restated.

(f) The cumulative effect of $925,000 should be separately reported between extraordinary

items and net income.

17. (a) Other expenses or losses section or in separate section, appropriately labeled as an

unusual item, if unusual or infrequent but not both.

(b) Operating expense section or other expenses and losses section or in separate section,

appropriately labeled as an unusual item, if unusual or infrequent but not both. APB

Opinion No. 30 specifically states that the effect of a strike does not constitute an

extraordinary item.

(c) Operating expense section, as a selling expense, but sometimes reflected as an

administrative expense.

(d) Separate section after income from continuing operations, entitled discontinued

operations.

(e) Other revenues and gains section or in a separate section, appropriately labeled as an

unusual item, if unusual or infrequent but not both.

(f) Other revenues and gains section.

(g) Operating expense section, normally administrative. If a manufacturing concern, may be

included in cost of goods sold.

(h) Other expenses or losses section or in separate section, appropriately labeled as an

unusual item, if unusual or infrequent but not both.

18. Bonds and Glavine should not report the sales in a similar manner. This type of transaction

appears to be typical of Bonds’ central operations. Therefore, Bonds should report revenues of

$160,000 and expenses of $100,000 ($70,000 + $30,000). However, Glavine’s transaction

appears to be a peripheral or incidental activity not related to their central operations. Thus,

Glavine should report a gain of $60,000 ($160,000 – $100,000). Note that although the

classification is different, the effect on net income is the same ($60,000 increase).

19. You should tell Rex that a company’s reported net income is the same whether the single-step

or multiple-step format is used. Either way, the company has the same revenues, gains,

expenses, and losses; they are simply organized in a different format.

20. Both formats are acceptable. The amount of detail reported in the income statement is left to

the judgment of the company, whose goal in making this decision should be to present financial

statements which are most useful to decision makers. We want to present a simple,

understandable statement so that a reader can easily discover the facts of importance;

therefore, a single amount for selling expenses might be preferable. However, we also want to

fully disclose the results of all activities; thus, a separate listing of expenses may be preferred.

Note that if the condensed version is used, it should be accompanied by a supporting schedule

of the eight components in the notes to the financial statements.

5-7

Questions Chapter 5 (Continued)

21. Intraperiod tax allocation should not affect the reporting of an unusual gain. The FASB

specifically prohibits a “net-of-tax” treatment for such items to insure that users of financial

statements can easily differentiate extraordinary items from material items that are unusual or

infrequent, but not both. “Net-of-tax” treatment is reserved for discontinued operations,

extraordinary items, cumulative effect of a change in accounting principle, and prior period

adjustments.

22. Intraperiod tax allocation has no effect on reported net income, although it does affect the

amounts reported for various components of income. The effects on these components offset

each other so net income remains the same. Intraperiod tax allocation merely takes the total

tax expense and allocates it to the various items which affect the tax amount.

23. If Letterman has preferred stock outstanding, the numerator in its computation may be

incorrect. A better description of “earnings per share” is “earnings per common share.” The

numerator should include only the earnings available to common shareholders. Therefore, the

numerator should be: net income less preferred dividends.

The denominator is also incorrect if Letterman had any common stock transactions during the

year. Since the numerator represents the results for the entire year, the denominator should

reflect the weighted average number of common shares outstanding during the year, not the

shares outstanding at one point in time (year-end).

24. The earnings per share trend is not favorable. Extraordinary items are one-time occurrences

which are not expected to be reported in the future. Therefore, earnings per share on income

before extraordinary items is more useful because it represents the results of ordinary business

activity. Considering this EPS amount, EPS has decreased from $7.21 to $6.40.

25. Tax allocation within a period is the practice of allocating the income tax for a period to such

items as income before extraordinary items, extraordinary items, and prior periods adjustments.

The justification for tax allocation within a period is to produce financial statements which

disclose an appropriate relationship, for example, between income tax expense and (a) income

before extraordinary items, (b) extraordinary items, and (c) prior periods adjustments (or of the

opening balance of retained earnings).

26. Tax allocation within a period (intraperiod) becomes necessary when a firm encounters such

items as discontinued operations, extraordinary items, accounting changes, or adjustments of

prior periods (that is, of the opening balance of retained earnings). Such allocation is

necessary to bring about an appropriate relationship between income tax expense and income

from continuing operations, discontinued operations, income before extraordinary items,

extraordinary items, etc.

Tax allocation within a period is handled by first computing the tax expense attributable to

income before extraordinary items, assuming no discontinued operations. This is simply

computed by ascertaining the income tax expense related to revenue and expense

transactions entering into the determination of such income. Next, the remaining income tax

expense attributable to other items is determined by the tax consequences of transactions

involving these items. The applicable tax effect of these items (extraordinary, accounting

changes, prior period adjustments) should be disclosed separately because of their materiality.

5-8

Questions Chapter 5 (Continued)

27.

Natsume Sozeki Company

Partial Income Statement

For the Year Ended December 31, 2003

Income before taxes and extraordinary item $1,000,000

Income taxes 340,000

Income before extraordinary item 660,000

Extraordinary item—gain on sale of plant (condemnation) $450,000

Less applicable income tax 135,000 315,000

Net income $ 975,000

28. The damages would probably be reported in Pierogi Corporation’s financial statements in the

other expenses or losses section. If the damages are unusual in nature, the damage

settlement might be reported as an unusual item. The damages would not be reported as a

prior period adjustment.

29. The assets, cash flows, results of operations, and activities of the plants closed would not

appear to be clearly distinguishable, operationally or for financial reporting purposes, from the

assets, results of operations, or activities of the Tiger Paper Company. Therefore, disposal of

these assets is not considered to be a disposal of a component of a business that would

receive special reporting.

30. The major items reported in the retained earnings statement are: (1) adjustments of the

beginning balance for prior period adjustments, (2) the net income or loss for the period, (3)

dividends for the year, and (4) restrictions (appropriations) of retained earnings. It should be

noted that the retained earnings statement is sometimes composed of two parts,

unappropriated and appropriated.

31. Generally accepted accounting principles are ordinarily concerned only with a “fair

presentation” of business income. In contrast, taxable income is a statutory concept which

defines the base for raising tax revenues by the government, and any method of accounting

which meets the statutory definition will “clearly reflect” taxable income as defined by the

Internal Revenue Code. It should be noted that the Code prohibits use of the cash receipts and

disbursements method as a method which will clearly reflect income in accounting for

purchases and sales if inventories are involved.

The cash receipts and disbursements method will not usually fairly present income because:

1. The completed transaction, not receipt or disbursement of cash, increases or diminishes

income. Thus, a sale on account produces revenue and increases income, and the

incurrence of expense reduces income without regard to the time of payment of cash.

2. The matching principle requires that costs be matched against related revenues produced.

In most situations the cash receipts and disbursements method will violate the matching

principle.

3. Consistency requires that accountable events receive the same accounting treatment from

accounting period to accounting period. The cash receipts and disbursements method

permits manipulation of the timing of revenues and expenses and may result in treatments

which are not consistent, detracting from the usefulness of comparative statements.

32. Problems arise both from the revenue side and from the expense side. There sometimes may

be doubt as to the amount of revenue under our common rules of revenue recognition.

However, the more difficult problem is the determination of costs expired in the production of

revenue. During a single fiscal period it often is difficult to determine the expiration of certain

5-9

Questions Chapter 5 (Continued)

costs which may benefit several periods. Business is continuous and estimates have to be

made of the future if we are to systematically apportion costs to fiscal periods. Examples of

items which present serious obstacles include such items as institutional advertising and

organization costs.

Accountants have established certain rules for handling revenues and costs which are applied

consistently and in a systematic manner. From period to period, application of these rules

generally results in a satisfactory matching of costs and revenues unless there are large

changes from one period to another. These rules, influenced by conservatism in the face of the

uncertainties involved, tend to charge costs to expense earlier than might be ideally desirable if

we had more knowledge of the future.

Costs or expenses of the types mentioned above, by their very nature, defy any attempt to

relate them to revenues of a specific period or periods. Although it is known that institutional

advertising will yield benefits beyond the present, both the amount of such benefits and when

they will be enjoyed are shrouded in uncertainty. The degree of certainty with which their time

distribution can be forecast is so small and the results, therefore, so unreliable that the

accountant writes them off as applicable to the period or periods in which the expense was

incurred.

33. Components are the major subsections of an income statement such as income from

continuing operations, income from discontinued operations, other revenues and gains, etc.

Elements are the basic ingredients which comprise the income statement; that is, revenues,

gains, expenses, and losses. Items are descriptions of the elements such as rent revenue, rent

expense, etc.

In order to predict the future, the amounts of individual items may have to be reported. For

example, if “income from continuing operations” is significantly lower this year and is reported

as a single amount, users would not know whether to attribute the decrease to a temporary

increase in an expense item (for example, an unusually large bad debt), a structural change

(for example, a change in the relationship between variable and fixed expense), or some other

factor. Another example is income data that are distorted because of large discretionary

expenses.

34. Other comprehensive income must be displayed (reported) in one of three ways: (1) a second

separate income statement, (2) a combined income statement of comprehensive income, or (3)

as part (separate columns) of the statement of stockholders’ equity.

35. The results of continuing operations should be reported separately from discontinued

operations, and any gain or loss from disposal of a component of a business should be

reported with the related results of discontinued operations and not as an extraordinary item.

The following format illustrates the proper disclosure:

Income from continuing operations before income taxes $XXX

Income tax expense XXX

Income from continuing operations XXX

Discontinued operations

Gain (loss) on disposal of Division X

(less applicable income taxes of $—) XXX

Net income $XXX

5-10

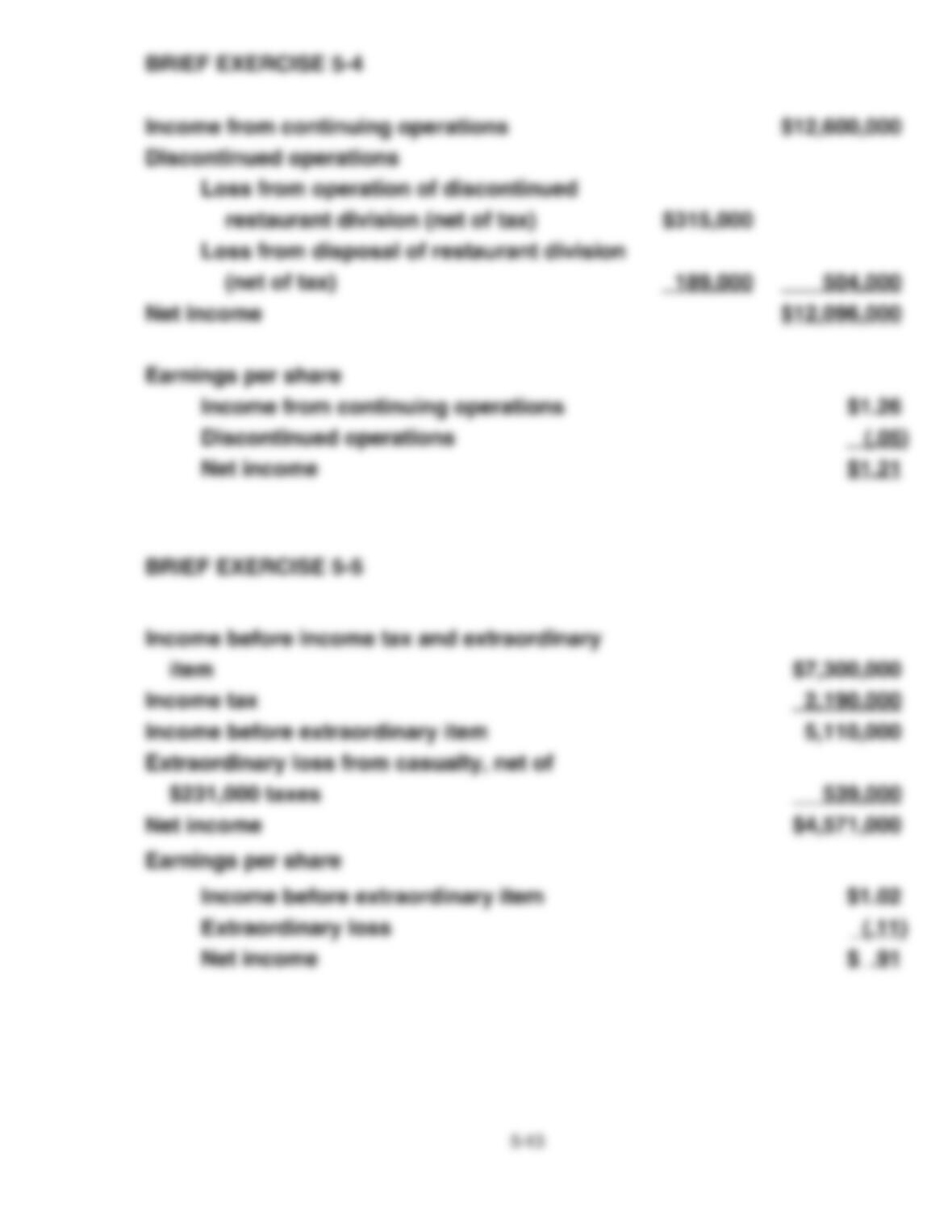

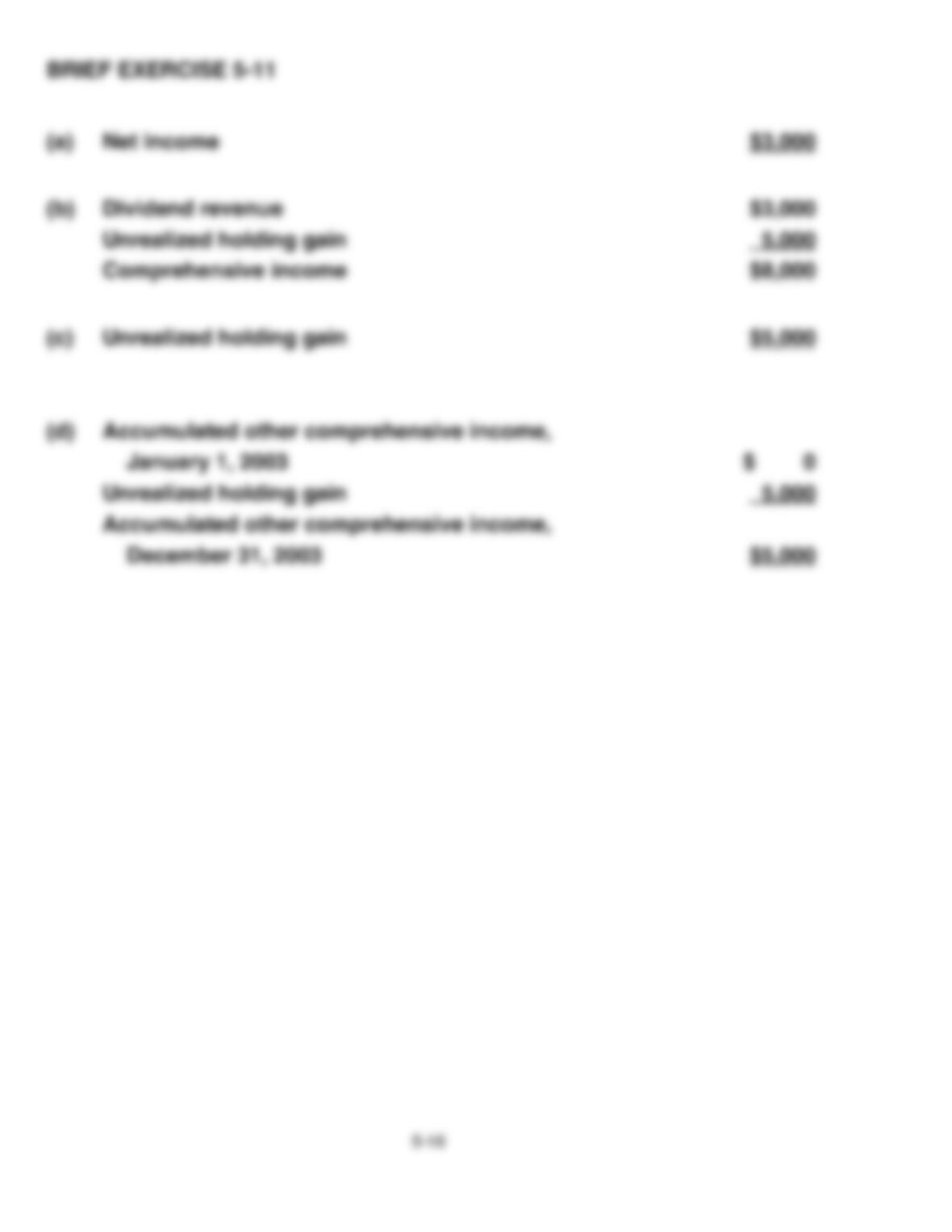

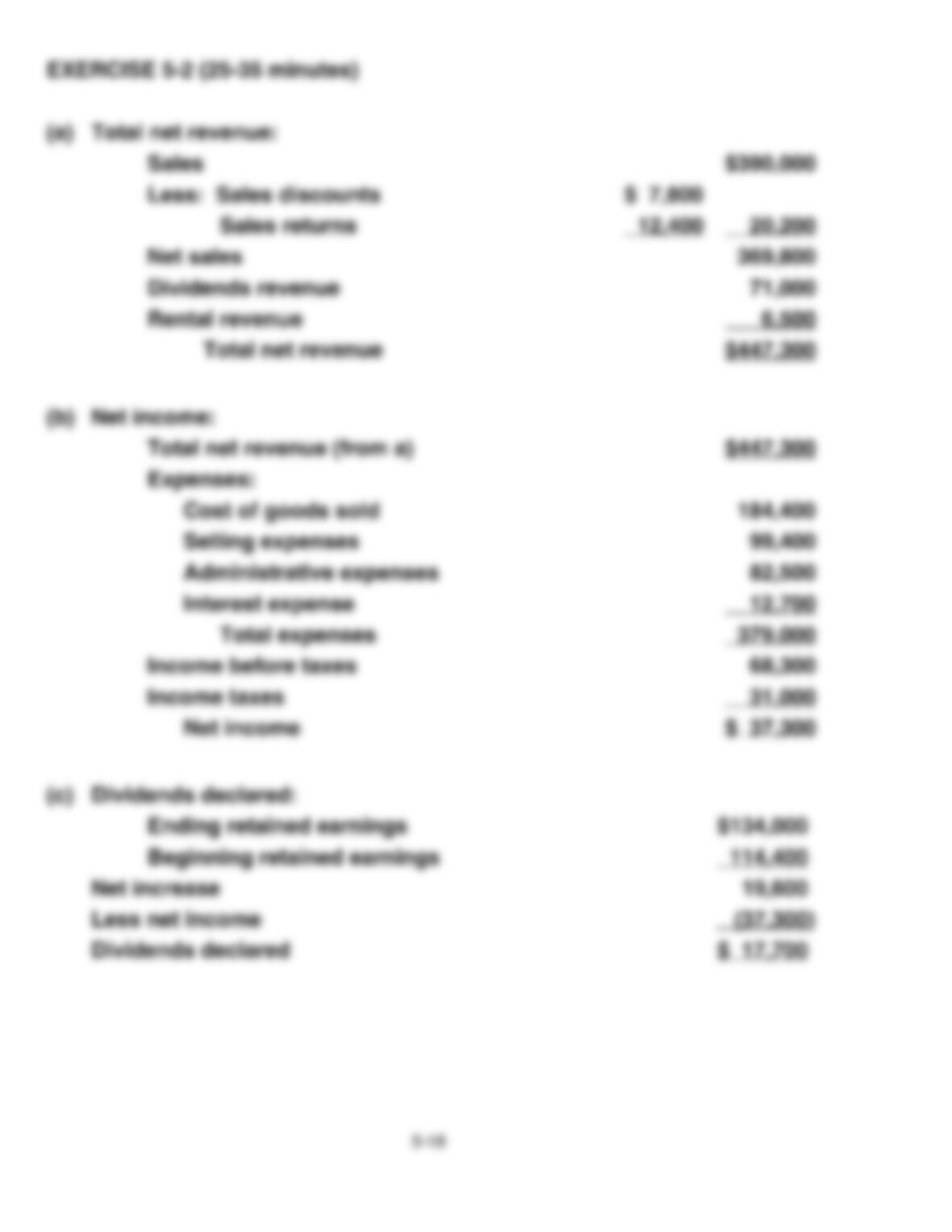

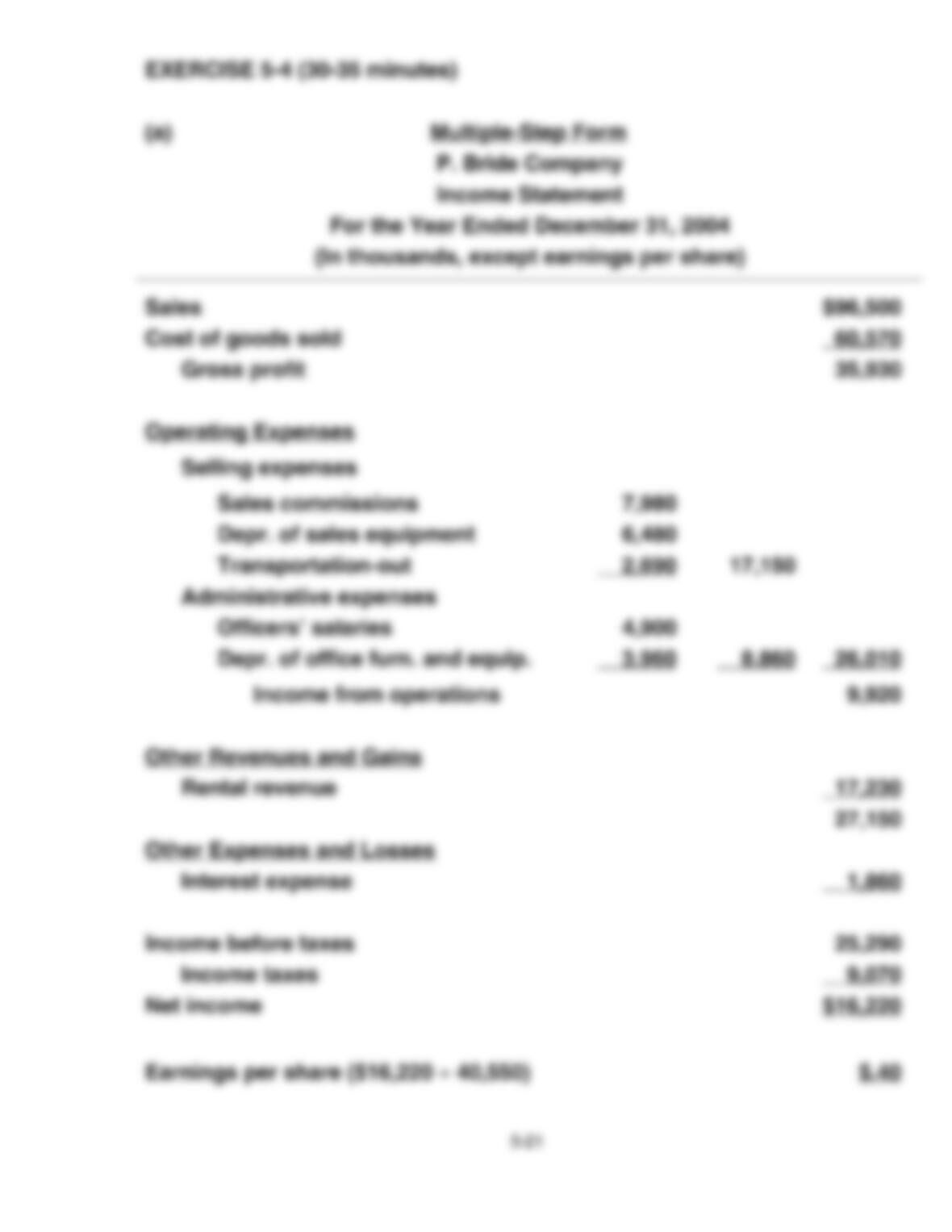

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 5-1

Tim Allen Co.

Income Statement

For the Year 2003

Revenues

Sales $540,000

Expenses

Cost of Goods Sold $320,000

Wages Expense 120,000

Other Operating Expenses 10,000

Income Tax Expense 25,000

Total Expenses 475,000

Net income $65,000

Earnings per share $0.65

5-11

BRIEF EXERCISE 5-2

Turner Corporation

Income Statement

For the Year Ended December 31, 2004

Revenues

Net sales $2,400,000

Interest revenue 31,000

Total revenues 2,431,000

Expenses

Cost of goods sold $1,250,000

Selling expenses 280,000

Administrative expenses 212,000

Interest expense 45,000

Income tax expense* 193,200

Total expenses 1,980,200

Net income $ 450,800

Earnings per share** $6.44

*($2,431,000 – $1,250,000 – $280,000 – $212,000 – $45,000) X 30% =

$193,200.

**$450,800 ÷ 70,000 shares.

BRIEF EXERCISE 5-3

Turner Corporation

Income Statement

For the Year Ended December 31, 2004

Net sales $2,400,000

Cost of goods sold 1,250,000

Gross profit 1,150,000

Selling expenses $280,000

Administrative expenses 212,000 492,000

Income from operations 658,000