3-1

CHAPTER 3

The Accounting Information System

ASSIGNMENT CLASSIFICATION TABLE

Topics Questions

Brief

Exercises Exercises Problems

1. Transaction identification. 1, 2, 3, 5 1, 2 1, 2, 3, 4, 21 13

2. Nominal accounts. 4, 7

3. Trial balance. 6, 13 2, 3, 4 1, 2, 7

4. Adjusting entries. 8, 14, 16, 17 3, 4, 5, 6, 7,

8, 9, 10

5, 6, 7, 8, 9,

10

1, 2, 3, 4, 5,

6, 7, 8, 9, 10,

11, 12

5. Closing. 15 12 11, 12, 17 1, 3, 5, 6, 7,

8, 9, 10, 12

6. Inventory and cost of

goods sold.

9, 10, 11, 12 11 12, 14, 15,

16

7. Work sheet and/or

financial statements.

18 13, 18, 19,

20

1, 2, 4, 5, 9,

11, 12

8. Comprehensive

accounting cycle.

1, 2, 7, 9

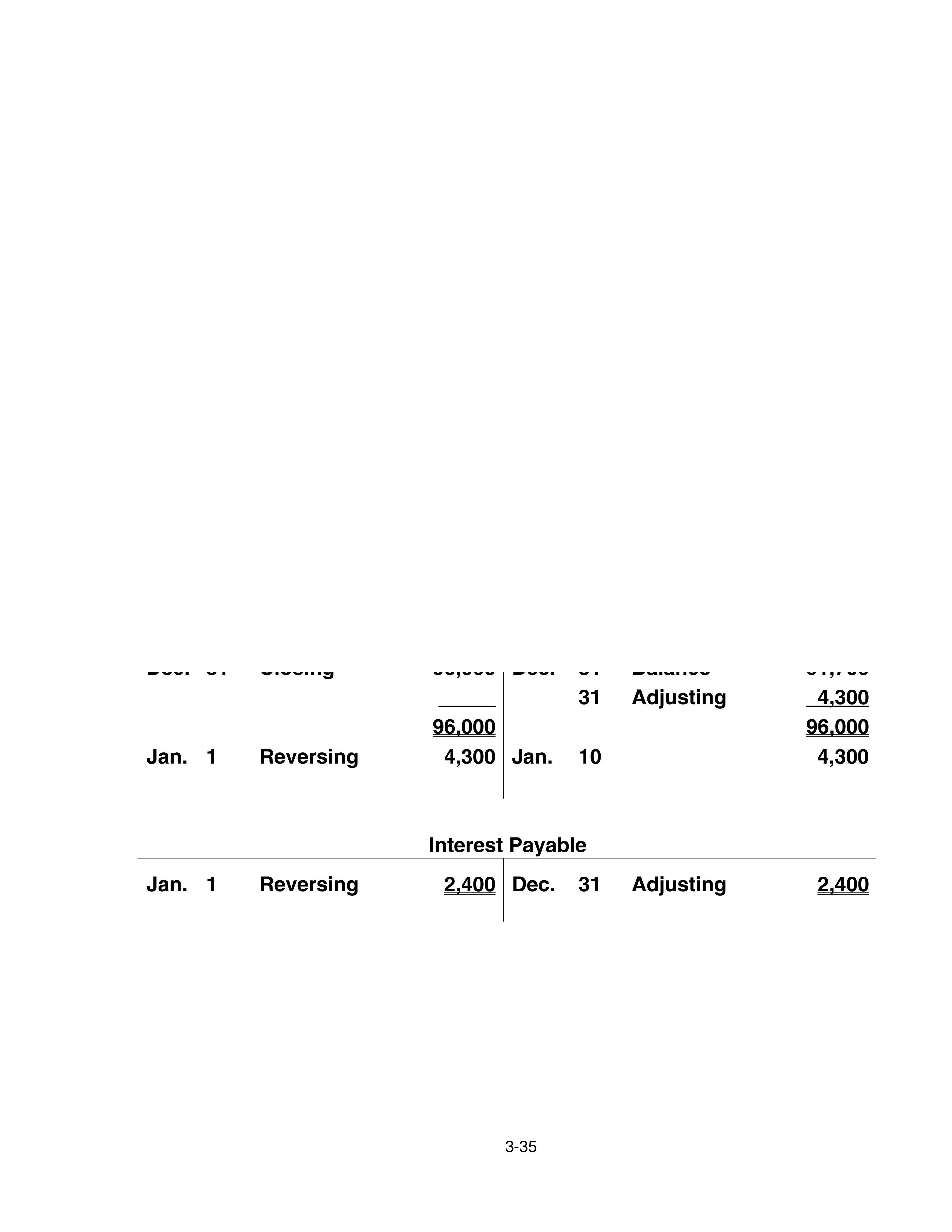

* 9. Reversing entries. 19 13 22, 23

*These topics are dealt with in the Appendix to the Chapter.

3-2

ASSIGNMENT CHARACTERISTICS TABLE

Item Description

Level of

Difficulty

Time

(minutes)

E3-1 Transaction analysis–service company. Simple 15-20

E3-2 Corrected trial balance. Simple 10-15

E3-3 Corrected trial balance. Simple 15-20

E3-4 Corrected trial balance. Simple 15-20

E3-5 Adjusting entries. Moderate 15-20

E3-6 Adjusting entries. Moderate 15-20

E3-7 Analyze adjusted data. Complex 15-20

E3-8 Adjusting entries. Moderate 10-15

E3-9 Adjusting entries. Moderate 15-20

E3-10 Adjusting entries and trial balance. Complex 25-30

E3-11 Closing entries. Simple 10-15

E3-12 Closing entries. Moderate 10-15

E3-13 Completing work sheet. Simple 10-15

E3-14 Compute missing amounts. Simple 10-15

E3-15 Find missing amounts–periodic. Moderate 15-20

E3-16 Prepare cost of goods sold–periodic. Moderate 10-15

E3-17 Closing entries for a corporation. Moderate 15-20

E3-18 Work sheet preparation. Moderate 15-20

E3-19 Work sheet and balance sheet presentation. Moderate 20-25

E3-20 Partial work sheet preparation. Moderate 15-20

E3-21 Transactions of a corporation including investment and

dividend.

Moderate 20-25

*E3-22 Closing and reversing entries. Complex 15-20

*E3-23 Adjusting and reversing entries. Complex 15-20

P3-1 Transactions, financial statements–service company. Moderate 25-35

P3-2 Adjusting entries and financial statements. Moderate 35-40

P3-3 Prepare adjusting entries. Moderate 25-30

P3-4 Prepare financial statements and closing entries. Moderate 35-40

P3-5

P3-6 Prepare financial statements, adjusting and closing

entries.

Moderate 40-50

P3-7

P3-8 Adjusting entries. Moderate 15-20

P3-9 Adjusting entries and financial statements. Moderate 25-30

P3-10 Adjusting entries and financial statements. Moderate 25-35

P3-11 Adjusting entries. Moderate 25-30

P3-12 Adjusting and closing. Moderate 30-40

P3-13 Adjusting and closing. Moderate 30-35

3-3

ANSWERS TO QUESTIONS

1. Examples are:

(a) Payment of an accounts payable.

(b) Collection of an accounts receivable from a customer.

(c) Transfer of an accounts payable to a note payable.

2. Transactions (a), (b), (d) are considered business transactions and are recorded in the accounting

records because a change in assets, liabilities, or equities has been effected as a result of a

transfer of values from one party to another. Transactions (c) and (e) are not business

transactions because a transfer of values has not resulted, nor can the event be considered

financial in nature and capable of being expressed in terms of money.

3. Transaction (a): Accounts Receivable (debit), Fees Earned (credit).

Transaction (b): Cash (debit), Accounts Receivable (credit).

Transaction (c): Office Supplies (debit), Accounts Payable (credit).

Transaction (d): Delivery Expense (debit), Cash (credit).

4. Revenue and expense accounts are referred to as temporary or nominal accounts because each

period they are closed out to Income Summary in the closing process. Their balances are reduced

to zero at the end of the accounting period; therefore, the term temporary or nominal is sometimes

given to these accounts.

5. The double-entry system means that for every debit there must be a credit and vice-versa. It does

not mean that each transaction must be recorded twice.

6. Although it is not absolutely necessary that a trial balance be taken periodically, it is customary

and desirable. The trial balance accomplishes two principal purposes:

(1) It tests the accuracy of the entries in that it proves that debits and credits of an equal amount

are in the ledger.

(2) It supplies a list of open accounts and their balances which may be used in preparing the

financial statements and in supplying financial data about the concern.

7. (a) Real account; balance sheet.

(b) Real account; balance sheet.

(c) Merchandise inventory is generally considered a real account appearing on the balance sheet.

It has the elements of a nominal account when the periodic inventory system is used. It

appears on the income statement when the multiple step format is used.

(d) Real account; balance sheet.

(e) Real account; balance sheet.

(f) Nominal account; income statement.

(g) Nominal account; income statement.

(h) Real account; balance sheet.

8. At December 31, the three days’ wages due to the employees represent a current liability. The

related expense must be recorded in this period to properly reflect the expense incurred.

9. (a) In a service company, revenues are service revenues and expenses are operating expenses.

In a merchandising company, revenues are sales revenues and expenses consist of cost of

goods sold plus operating expenses.

3-4

Questions Chapter 3 (Continued)

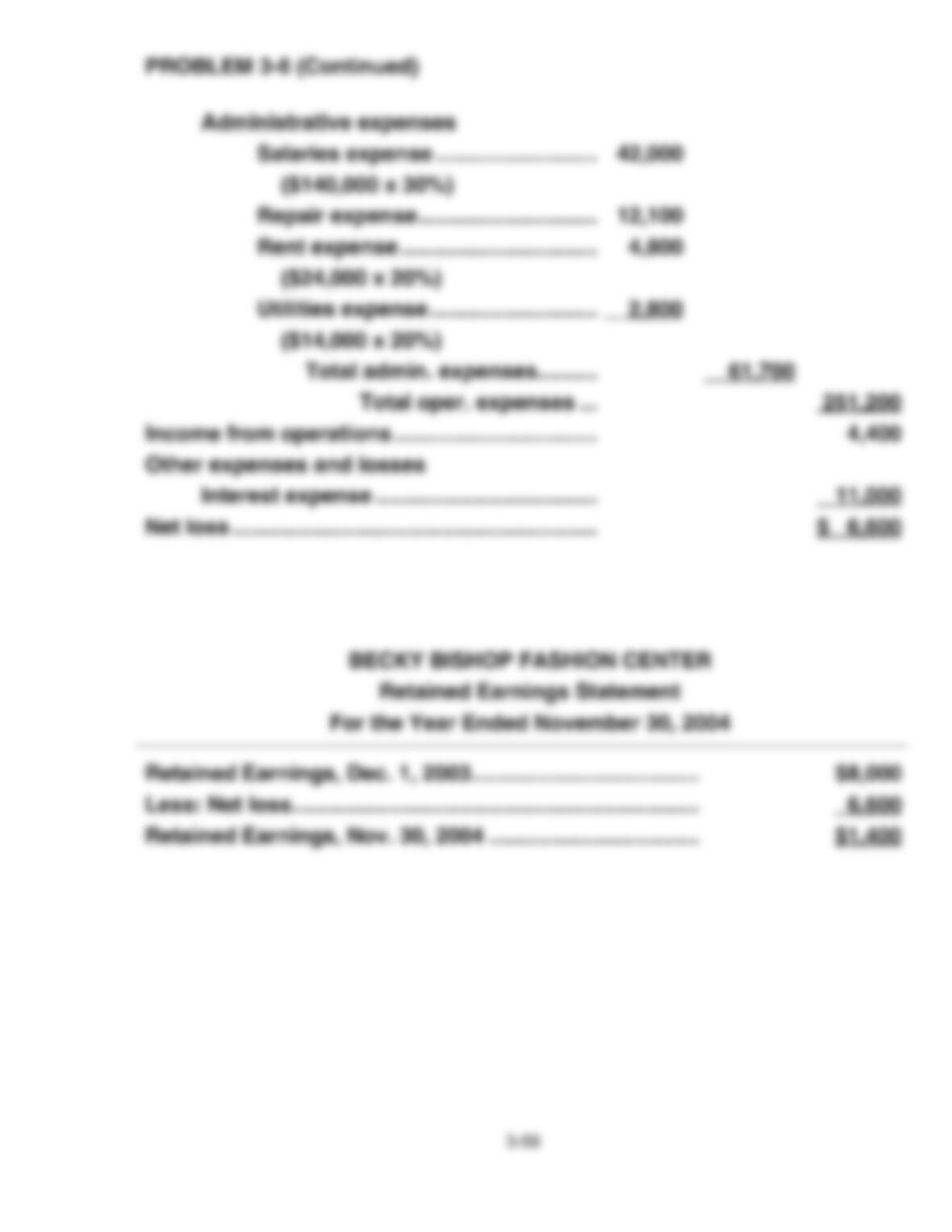

(b) The measurement process in a merchandising company consists of comparing the sales price

of the merchandise inventory to the cost of goods sold and operating expense.

10. The purpose of the Cost of Goods Sold account is to act as a clearing account for bringing

together those items directly affecting the Cost of Goods Sold for this period. Example of items

that would appear in this account are: (1) Purchases, (2) Purchase Discounts, (3) Purchase

Returns, (4) Purchase Allowances, (5) Transportation-in, (6) Inventory (beginning), and (7)

Inventory (ending). The ending balance represents the cost of goods sold.

11. In a perpetual inventory system, when inventory is sold, Cost of Goods Sold is debited and

Inventory is credited. At the end of the period, Cost of Goods Sold is closed to Income Summary.

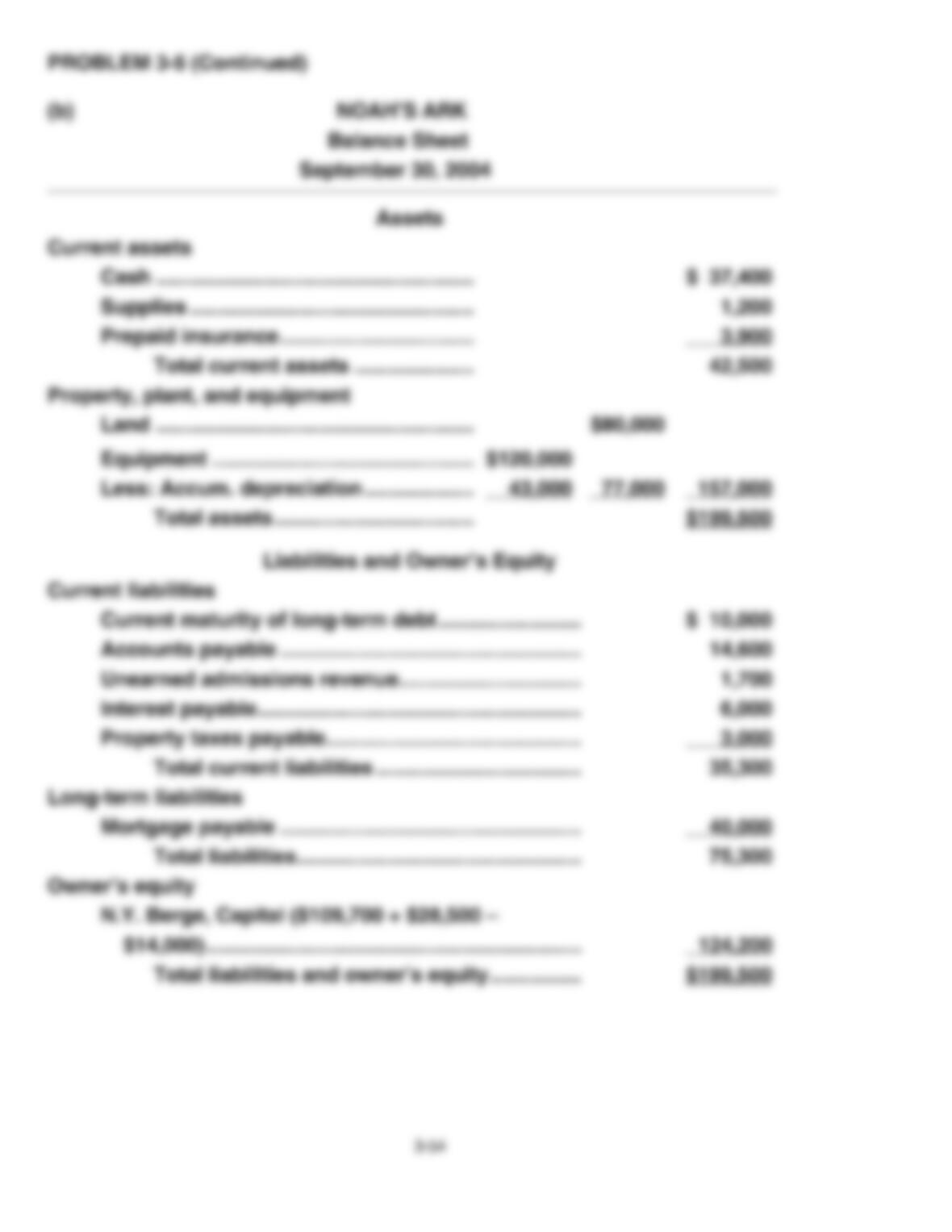

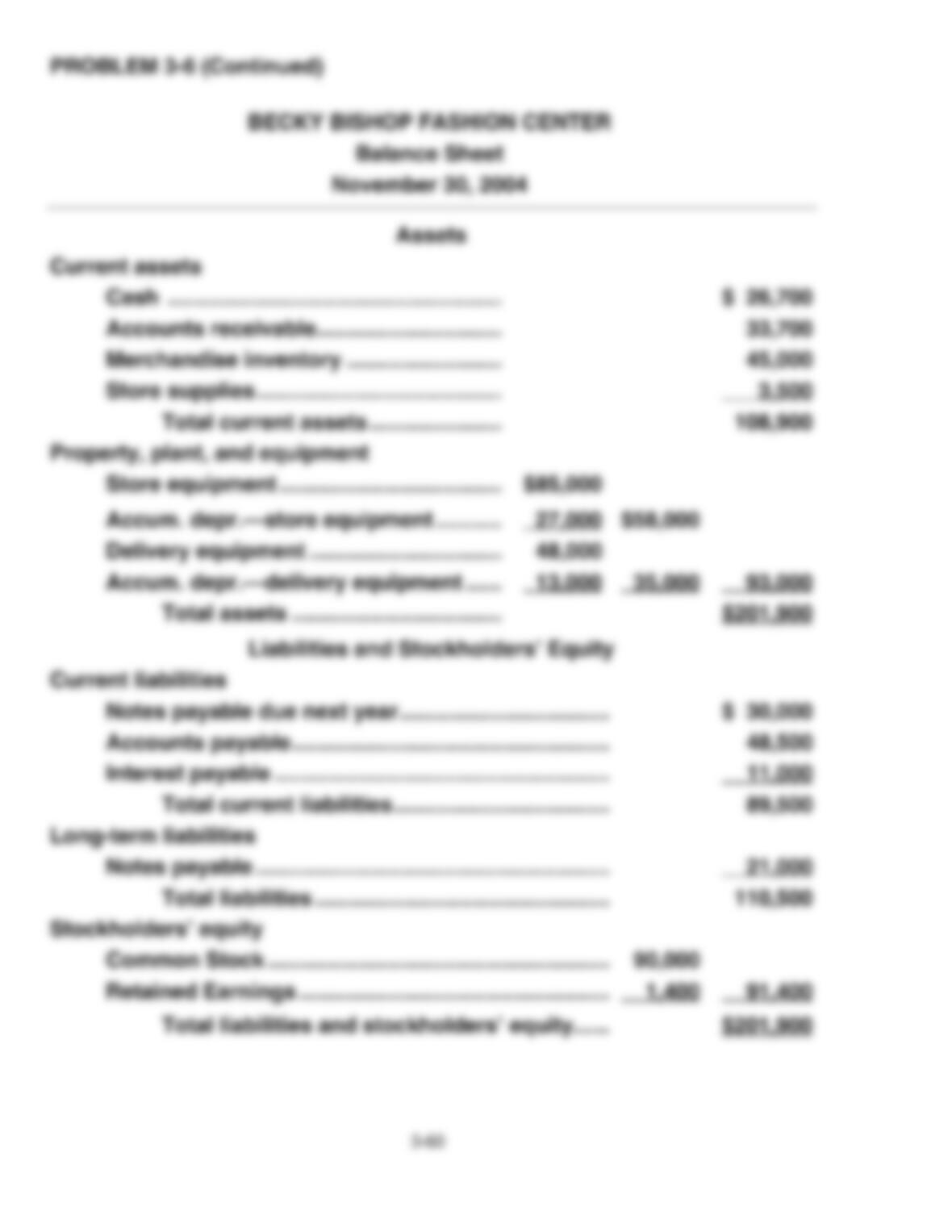

12. On the balance sheet, the effect of the error is (1) the equipment account is understated, and (2)

the Capital account (Retained Earnings) is understated. On the income statement, (1) purchases

and cost of goods sold are overstated and (2) net income is understated. (Note to instructor: The

instructor should also be ready to discuss the effect that the omission of the depreciation charge

on the computer might have.)

13. (a) No change.

(b) Before closing, balances exist in these accounts; after closing, no balances exist.

(c) Before closing, balances exist in these accounts; after closing, no balances exist.

(d) Before closing, a balance exists in this account exclusive of the income or loss for the period;

during the period the balance is decreased by dividends declared; after closing, the balance is

increased or decreased by the amount of income or loss.

(e) No change.

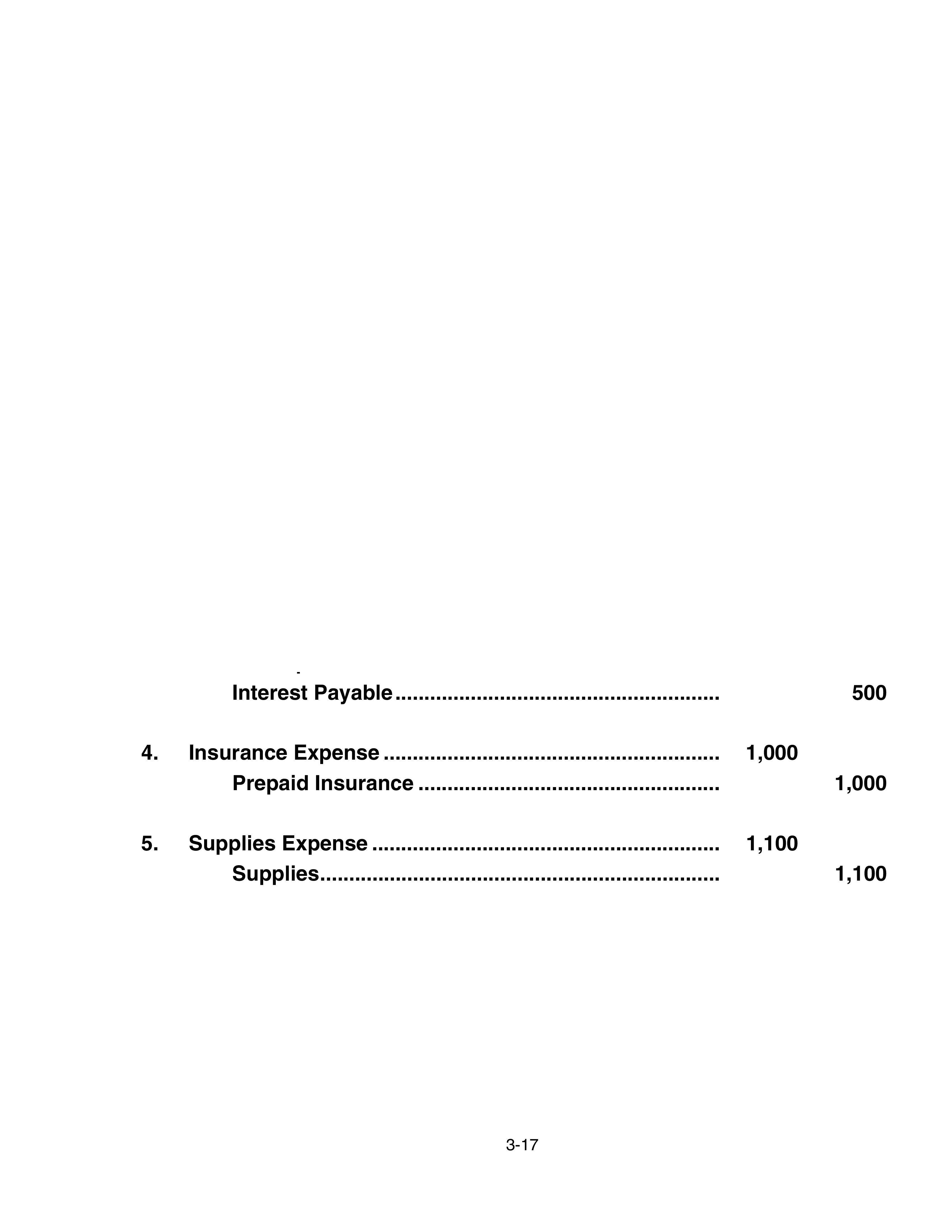

14. Adjusting entries are prepared prior to the preparation of financial statements in order to bring the

accounts up to date and are necessary (1) to achieve a proper matching of revenues and

expenses in measuring income and (2) to achieve an accurate presentation of assets and equities.

15. Closing entries are prepared to transfer the effect of nominal accounts to capital after the adjusting

entries have been recorded and the financial statements prepared. Closing entries are necessary

to reduce the balances in nominal accounts to zero in order to prepare the accounts for the next

period’s transactions.

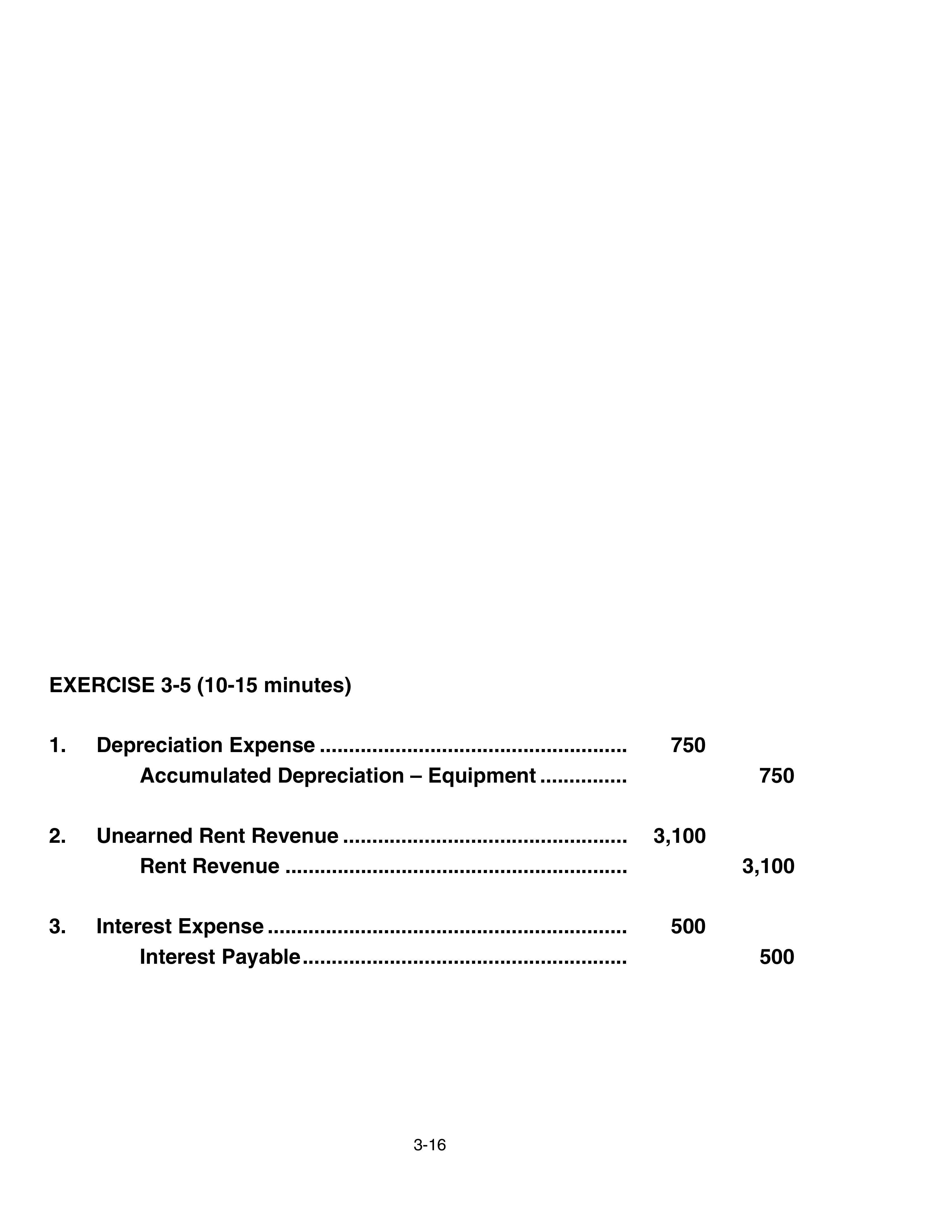

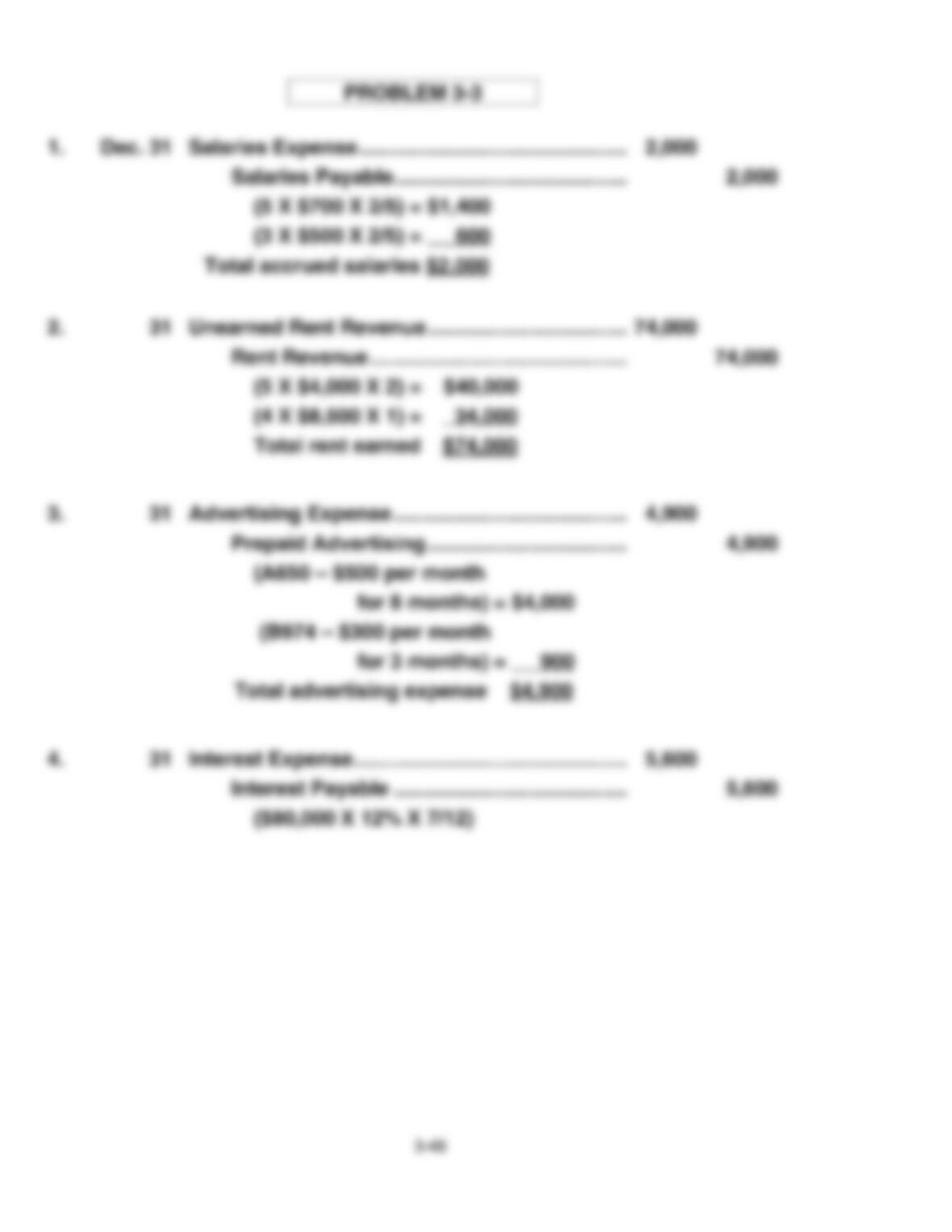

16. Cost – Salvage Value = Depreciable Cost: $3,000 – $0 = $3,000. Depreciable Cost ÷ Useful Life =

Depreciation Expense For One Year $3,000 ÷ 5 years = $600 per year. The asset was used for 6

months (7/1 – 12/31), therefore 1/2-year depreciation expense should be reported. Annual

depreciation x 6/12 = amount to be reported on 2003 income statement: $600 x 6/12 = $300.

17.

December 31

Interest Receivable………………………………………………………………………………… 10,000

Interest Revenue ……………………………………………………………………………. 10,000

(To record accrued interest revenue on loan)

Accrued expenses result from the same causes as accrued revenues. In fact, an accrued

expense on the books of one company is an accrued revenue to another company.

3-5

Questions Chapter 3 (Continued)

18. A work sheet is not a permanent accounting record and its use is not required in the accounting

cycle. The work sheet is an informal device for accumulating and sorting information needed for

the financial statements. Its use is optional in helping to prepare financial statements.

*19. Reversing entries are made at the beginning of the period to reverse the accrued items and some

prepaid items. Reversing entries are not necessary. They are made to simplify the recording of

certain transactions that will occur later in the period. The same results will be attained whether or

not reversing entries are recorded.

3-6

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 3-1

May 1 Cash …………………………………………………………… 3,000

Common Stock…………………………………….. 3,000

3 Equipment ………………………………………………….. 1,100

Accounts Payable ………………………………… 1,100

13 Rent Expense ……………………………………………… 400

Cash…………………………………………………….. 400

21 Accounts Receivable…………………………………… 500

Service Revenue ………………………………….. 500

BRIEF EXERCISE 3-2

Aug. 2 Cash ……………………………………………………………. 12,000

Equipment …………………………………………………… 2,500

Brett Favre, Capital ……………………………….. 14,500

7 Supplies ………………………………………………………. 400

Accounts Payable …………………………………. 400

12 Cash ……………………………………………………………. 1,300

Accounts Receivable……………………………………. 670

Service Revenue……………………………………. 1,970

3-7

BRIEF EXERCISE 3-2 (Continued)

15 Rent Expense ………………………………………………. 600

Cash……………………………………………………… 600

19 Supplies Expense ………………………………………… 130

Supplies………………………………………………… 130

BRIEF EXERCISE 3-3

July 1 Prepaid Insurance………………………………………… 18,000

Cash……………………………………………………… 18,000

Dec. 31 Insurance Expense ………………………………………. 3,000

Prepaid Insurance …………………………………. 3,000

($18,000 x 1/2 x 1/3)

BRIEF EXERCISE 3-4

July 1 Cash ……………………………………………………………. 18,000

Unearned Insurance Revenue………………… 18,000

Dec. 31 Unearned Insurance Revenue ………………………. 3,000

Insurance Revenue ……………………………….. 3,000

($18,000 x 1/2 x 1/3)

3-8

BRIEF EXERCISE 3-5

Aug. 1 Prepaid Insurance………………………………………… 8,400

Cash……………………………………………………… 8,400

Dec. 31 Insurance Expense ………………………………………. 1,750

Prepaid Insurance …………………………………. 1,750

($8,400 x 5/24)

BRIEF EXERCISE 3-6

Nov. 1 Cash ……………………………………………………………. 2,700

Unearned Rent Revenue………………………… 2,700

Dec. 31 Unearned Rent Revenue ………………………………. 1,800

Rent Revenue ……………………………………….. 1,800

($2,700 x 2/3)

BRIEF EXERCISE 3-7

Dec. 31 Salaries Expense …………………………………………. 3,600

Salaries Payable ……………………………………. 3,600

($6,000 x 3/5)

Jan. 2 Salaries Payable…………………………………………… 3,600

Salaries Expense …………………………………………. 2,400

Cash……………………………………………………… 6,000

3-9

BRIEF EXERCISE 3-8

Dec. 31 Interest Receivable ………………………………………. 300

Interest Revenue……………………………………. 300

Feb. 1 Cash ……………………………………………………………. 10,400

Notes Receivable…………………………………… 10,000

Interest Receivable………………………………… 300

Interest Revenue……………………………………. 100

BRIEF EXERCISE 3-9

Dec. 31 Interest Expense ………………………………………….. 400

Interest Payable…………………………………….. 400

31 Accounts Receivable……………………………………. 1,400

Service Revenue……………………………………. 1,400

31 Salaries Expense …………………………………………. 700

Salaries Payable ……………………………………. 700

31 Bad Debt Expense ……………………………………….. 900

Allowance for Doubtful Accounts…………… 900

3-10

BRIEF EXERCISE 3-10

Depreciation Expense ………………………………………………….. 3,000

Accumulated Depreciation – Equipment ………………… 3,000

Equipment……………………………………………………………………. $30,000

Less: Accumulated Depreciation – Equipment ……………… 3,000 $27,000

BRIEF EXERCISE 3-11

Beginning inventory $ 81,000

Purchases $540,000

Less: Purchase returns $5,800

Purchase discounts 5,000 10,800

Net purchases 529,200

Add: Freight-in 16,200

Cost of goods purchased 545,400

Cost of goods available for sale 626,400

Ending inventory 70,200

Cost of goods sold $556,200

3-11

BRIEF EXERCISE 3-12

Sales……………………………………………………………………………. 828,900

Interest Revenue ………………………………………………………….. 13,500

Income Summary…………………………………………………… 842,400

Income Summary …………………………………………………………. 780,300

Cost of Goods Sold ……………………………………………….. 556,200

Operating Expenses………………………………………………. 189,000

Income Tax Expense ……………………………………………… 35,100

Income Summary …………………………………………………………. 62,100

Retained Earnings …………………………………………………. 62,100

Retained Earnings………………………………………………………… 18,900

Dividends………………………………………………………………. 18,900

*BRIEF EXERCISE 3-13

(a) Salaries Payable ………………………………………………… 3,600

Salaries Expense…………………………………………. 3,600

(b) Salaries Expense ……………………………………………….. 6,000

Cash……………………………………………………………. 6,000

(c) Salaries Payable ………………………………………………… 3,600

Salaries Expense ……………………………………………….. 2,400

Cash……………………………………………………………. 6,000

SOLUTIONS TO EXERCISES

EXERCISE 3-1 (15-20 minutes)

Apr. 1 Cash ……………………………………………………………. 32,000

Equipment …………………………………………………… 14,000

Beverly Crusher, Capital………………………… 46,000

2 No entry—not a transaction.

3 Supplies ………………………………………………………. 700

Accounts Payable …………………………………. 700

7 Rent Expense ………………………………………………. 600

Cash……………………………………………………… 600