Fall 2019 – Copyright © Janet Huston, Ph.D., Texas Tech University

ACCT 2300 Chapter 3 – Page 1

Chapter 3 Notes

Accrual Accounting and Income

Learning Objectives:

1. Explain how accrual accounting differs from cash-basis accounting

2. Apply the revenue recognition and expense recognition (matching) principles

3. Adjust the accounts

4. Construct financial statements

5. Close the books

6. OMIT: Analyze and evaluate a company’s debt–paying ability

Revenue Recognition Principle

• Revenue: increase in net assets from day to day operations

• Gain: increase in net assets from peripheral or incidental transactions

• Net Assets = Assets – Liabilities

o Increase in Net Assets: either Assets increase or Liabilities decrease

For Revenues and Gains an Increase in Net Assets is either

• Cash ↑ or AR ↑ or NR ↑ or Unearned Revenue ↓

Revenues / Gains

Dr

Cr

↑ Revenue → NI → RE

• Revenue Recognition Principle: explains the timing and measurement of

revenues/gains for firms.

o Timing: when to recognize the revenue.

Recognize revenue when EARNED.

Earned: when a good is transferred or a service is performed

o Measurement: What amount of revenue to recognize.

Cash realized today or the today’s realizable cash equivalent of

future payments.

Realized: cash has been received

Realizable: cash is expected to be received and can be measured.

Revenue

Recognized?

Before Cash Received

(Accrual)

Same Time as Cash

Received

After Cash Received

(Deferral)

Journal Entries

Required:

2 Journal Entries:

1. ↑ Receivable;

↑ Revenue

2. ↑ Cash;

↓ Receivable

1 Journal Entries:

1. ↑ Cash;

↑ Revenue

2 Journal Entries:

1. ↑ Cash;

↑ Liability

2. ↓ Liability;

↑ Revenue

Fall 2019 – Copyright © Janet Huston, Ph.D., Texas Tech University

ACCT 2300 Chapter 3 – Page 2

Matching Principle (Expense Recognition Principle)

• Expense: decrease in net assets from day to day operations

• Loss: decrease in net assets from peripheral or incidental transactions

• Net Assets = Assets – Liabilities

o Decrease in Net Assets: either Assets decrease or Liabilities increase

Expenses / Losses

Dr

Cr

Expense → NI → RE

• Matching Principle: explains the timing and measurement of expenses/losses for

firms.

o Timing: when to incur the expense.

Direct Matching: match expenses with revenues recognized in the

same accounting period

• Expense follows the revenue; the revenue must be

recognized before the expense can be matched.

Example: Our firm sells cars. Before we sell the car, the cost of the

car is considered to be an asset called inventory. When we sell a

car, we recognize Sales Revenue. Then we must incur the expense

of the cost of the car by remove the cost of the car from Inventory

and increasing Cost of Goods Sold. The COGS only increased

because we increased our Sales Revenue.

Indirect Matching: match expenses with a particular period

instead of a revenue.

• Examples: Depreciation on a building, CEO salary, Utility

expense, Rent expense, Insurance expense.

o Measurement: What amount of expense to incur.

Cash paid today or today’s cash equivalent of future payments.

Activity #1

Expense

Incurred?

Before Cash Paid

(Accrual)

Same Time as

Cash paid

After Cash Paid

(Deferral)

Journal Entries

Required:

2 Journal Entries:

1. ↑ Expense;

↑ Liability

2. ↓ Liability;

↓ Cash

1 Journal Entries:

2. ↑ Expense;

↓ Cash

2 Journal Entries:

1. ↑ Prepaid Asset;

↓ Cash

2. ↑ Expense;

↓ Prepaid Asset

Fall 2019 – Copyright © Janet Huston, Ph.D., Texas Tech University

ACCT 2300 Chapter 3 – Page 3

Accrual Basis Accounting versus Cash Basis Accounting

• Accrual basis accounting

o Revenues are recognized when they meet revenue recognition principle

o Expenses are incurred when they meet matching principle.

o Accounting Ph.D. research shows:

Accrual Basis Accounting results in “smooth” earnings.

Accrual Basis Accounting Net Income which is a better indicator of

future cash flows.

• Cash Basis accounting

o Revenues are recognized when cash is

o Expenses are incurred when cash is

Real accounts: Cash and Equity

Nominal Accounts: Revenue, Expense, Withdrawal by owners (all close

to equity)

o Accounting Ph.D. research shows:

Cash Basis Accounting results in “lumpy” earnings.

Cash Basis Accounting is not indicative of what resources were

given up or revenues earned during a period of time.

Which Basis of Accounting is Best?

• Cash basis financial statements are easier to prepare; however, accrual basis

financial statements are required under Generally Accepted Accounting Principles

(GAAP).

• Accounting researchers have generally determined that accrual–based income

statements and balance sheets are more informative of current operations AND

more predictive of future profitability (and even more predictive of future cash

flows).

• Note that public companies MUST use accrual basis accounting.

• Private companies (such as sole proprietorships, partnerships and private

corporations) can use EITHER Cash OR Accrual Basis. However, if a private

company has a lot of bank financing, the bank may require annual financial

statements that are prepared in accordance with GAAP (which means the

financial statements would need to be accrual basis financial statements).

In this class, we will ALWAYS USE ACCRUAL BASIS ACCOUNTING (which is

in accordance with GAAP).

Fall 2019 – Copyright © Janet Huston, Ph.D., Texas Tech University

ACCT 2300 Chapter 3 – Page 4

Example of Accrual versus Cash Basis Accounting

Assume that Cortana has invested $1,500 in her business. She will buy and sell radar jammers to

Elites. Cortana can purchase radar jammers for $12 and sell them for $20. She starts out on her

first day. She leases a booth for $300 a day from the Arbiter (the Arbiter extends credit and lets

Cortana pay for the booth at the end of the week). Cortana purchases 100 radar jammers for $12

each ($1,200). Cortana is able to sell all 100 of the radar jammers for $20 each (total of $20 *

100 radar jammers or $2,000). However, only 25 jammers are sold for cash and the remaining 75

jammers are sold on credit and Cortana will get the money at the end of the week.

First, let’s consider how much cash Cortana has at the end of day 1.

Starts with

$1,500

Rents booth

no effect on cash (Cortana doesn’t have to pay until later)

Purchases radar jammers

minus $1,200

Sells 25 jammers for cash

add $500 (25 jammers for $20 each)

Sells 75 jammers on credit

no effect on cash (Cortana won’t collect cash until later)

Ending Cash Balance

$800

The cash that Cortana has is the same regardless of whether she is using accrual or cash basis

accounting. However, the Income Statement and Balance Sheet will look very different:

INCOME STATEMENT FOR DAY 1:

Accrual Basis

Cash Basis

Revenue (100 jammers X $25)

$2,000

Revenue (25 jammers X $25)

$500

Less expenses:

Cost of jammers ($12 x 100)

$1,200

Cost of jammers ($12 x 100)

$1,200

Booth fee

$300

Booth fee (didn’t pay yet)

$ 0 .

Net Income

$500

Net Loss

($700)

BALANCE SHEET AT THE END OF DAY 1:

Accrual Basis

Cash Basis

Cash

$800

Cash

$800

A/R ($20 X 75 jammers)

$1,500

A/R

$0

Inventory

$0

Inventory

$0

Total Assets

$2,300

Total Assets

$800

Accounts Payable (booth fee)

$300

Accounts Payable

$0

Owner’s Equity (original investment)

$1,500

Owner’s Equity

$1,500

Retained Earnings (the net income)

$500

R/E (the net loss)

($700)

Total Liabilities & Equity

$2,300

Total Liabilities & Equity

$800

Note that net income is drastically different depending on whether the accrual basis or the cash

basis of accounting is used. Cash basis Net Income is simply the cash received for revenues less

the cash paid out for expenses. Accrual basis Net Income recognizes revenue EARNED and

expenses INCURRED regardless of when the cash is exchanged. Also, note that the balance

sheet is very different. While the cash account is the same regardless of the method used, Cash

Basis Balance Sheets do NOT recognize accounts receivable or accounts payable.

Activity #2

Fall 2019 – Copyright © Janet Huston, Ph.D., Texas Tech University

ACCT 2300 Chapter 3 – Page 5

12 Steps of Accounting Cycle (continued from Chapter 2)

1.

2.

3.

4.

5. End of Period

6. Adj. Journal Entries (AJE)

7. Post to Ledger

8. Adjusted TB

9. Prepare FS

10. Closing Entries (CJE)

11. Post to Ledger

12. Post Closing TB

Step 5. End of Period

• End of Period: artificial time period like end of quarter or fiscal year.

• Going Concern Assumption: assumes firm will have infinite life

o To know how well the business did, we would have to shut down the

business, selling all assets, paying all liabilities, and returning remainder to

owners.

o But we don’t want our firm to go out of business so we assume….

• Periodicity Assumption: breaks life of firm into artificial time periods for the

purpose of creating financial statements.

o Ensures accounting information is reported in regular intervals

Step 6. Record Adjusting Entries (AJE)

• Adjusting Journal Entries: journal entries made at the end of the accounting

period to bring all accounts up to date so that financial statements can be prepared

on an accrual basis.

o Update all unrecorded Revenues and Expenses due to the passage of

o Ensure that Revenue Recognition & Expense Recognition (Matching)

Principles are being followed. These two principles make up the accrual

basis of accounting.

o Required by Periodicity and Going Concern Assumptions.

• Rules of Adjusting Entries:

1. Do not include cash in adjusting entry

2. Every adjusting entry always affects:

at least one account (asset, liability, or equity account)

and at least one account (revenue or expense account)

• Adjusting entries are either Accruals or Deferrals

ABCD:

Fall 2019 – Copyright © Janet Huston, Ph.D., Texas Tech University

ACCT 2300 Chapter 3 – Page 6

• Accruals: when revenue recognized or expense incurred before cash changes

hands Cash comes after (A before C)

o Accrued revenues (assets): revenue is recognized before cash is received

Example 1: On Oct 1, 2018, Sparky invests $20,000 in a CD earning 8% interest

annually. The CD matures on Sept 30, 2019. Principal and interest to be received

at maturity. Sparky’s year-end is Dec 31. Provide the required AJE, use GJEF.

Suppose the company didn’t recognize the revenue until it received the cash. How

would the assets, liabilities, equity and net income be affected in 2018 and 2019?

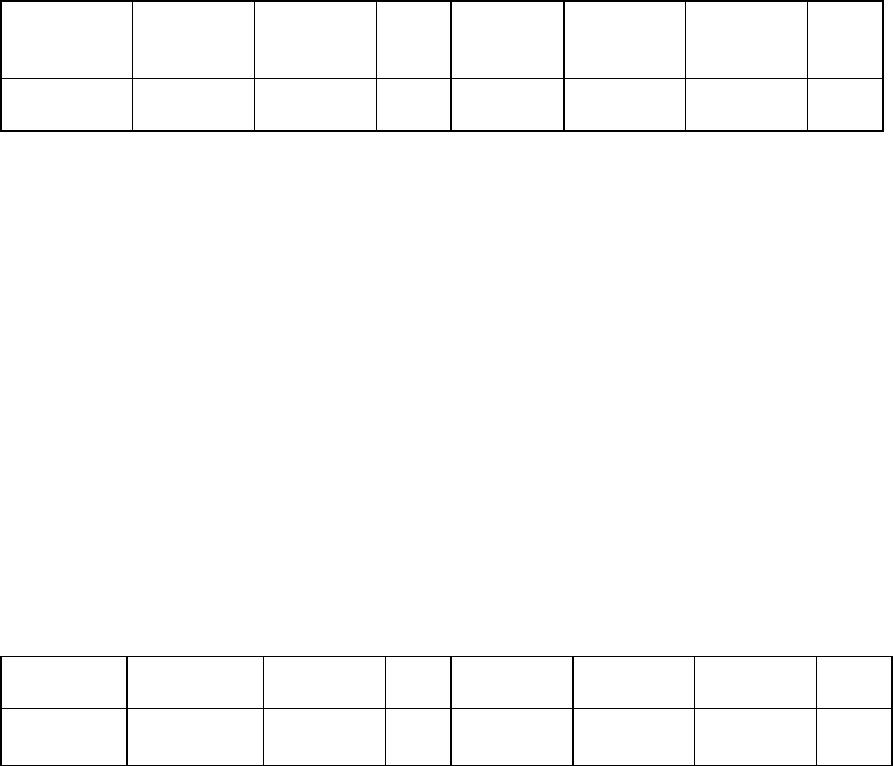

Assets

12/31/2018

Liabilities

12/31/2018

Equity

12/31/2018

NI

2018

Assets

12/31/201

9

Liabilities

12/31/2019

Equity

12/31/2019

NI

2019

↓ 400

OK

↓ 400

↓ 400

OK

OK

OK

↑ 400

Rev ↓ Rev ↑

o Accrued expenses (liabilities): expenses incurred before cash is paid or

liability recorded

Example 2: Sparky pays employees every other Friday. Employees work 5 days

(M-F) and earn $1,000/day. Fiscal year-end and Dec 31, 2018 falls on the second

Wednesday in the pay period. Provide the required AJE and the entry on Jan 2,

2019 (pay day), use GJEF.

Suppose the company didn’t incur the expense until it paid the cash on Jan 2,

2019. How would the assets, liabilities, equity and net income be affected in

2018 and 2019?

Assets

12/31/2018

Liabilities

12/31/2018

Equity

12/31/2018

NI

2018

Assets

12/31/2019

Liabilities

12/31/2019

Equity

12/31/2019

NI

2019

OK

↓ 8k

↑ 8k

↑ 8k

OK

OK

OK

↓ 8k

↓ Exp ↑ Exp

• Deferrals (commonly referred to as Prepayments): Cash changes hands before the

revenue is recognized or the expense is incurred. Cash comes first (C before D)

o Deferred revenues: cash is received before revenue is recognized

Happens when firm is prepaid for service or goods.

At end of period, firm must recognize the correct amount of revenue

earned and obligation to provide goods/services in the future.

Example 3: College Rentals, Inc. realizes $1,800 for 6 months rent revenue on

November 1, 2018, with the original journal entry included a credit to a real