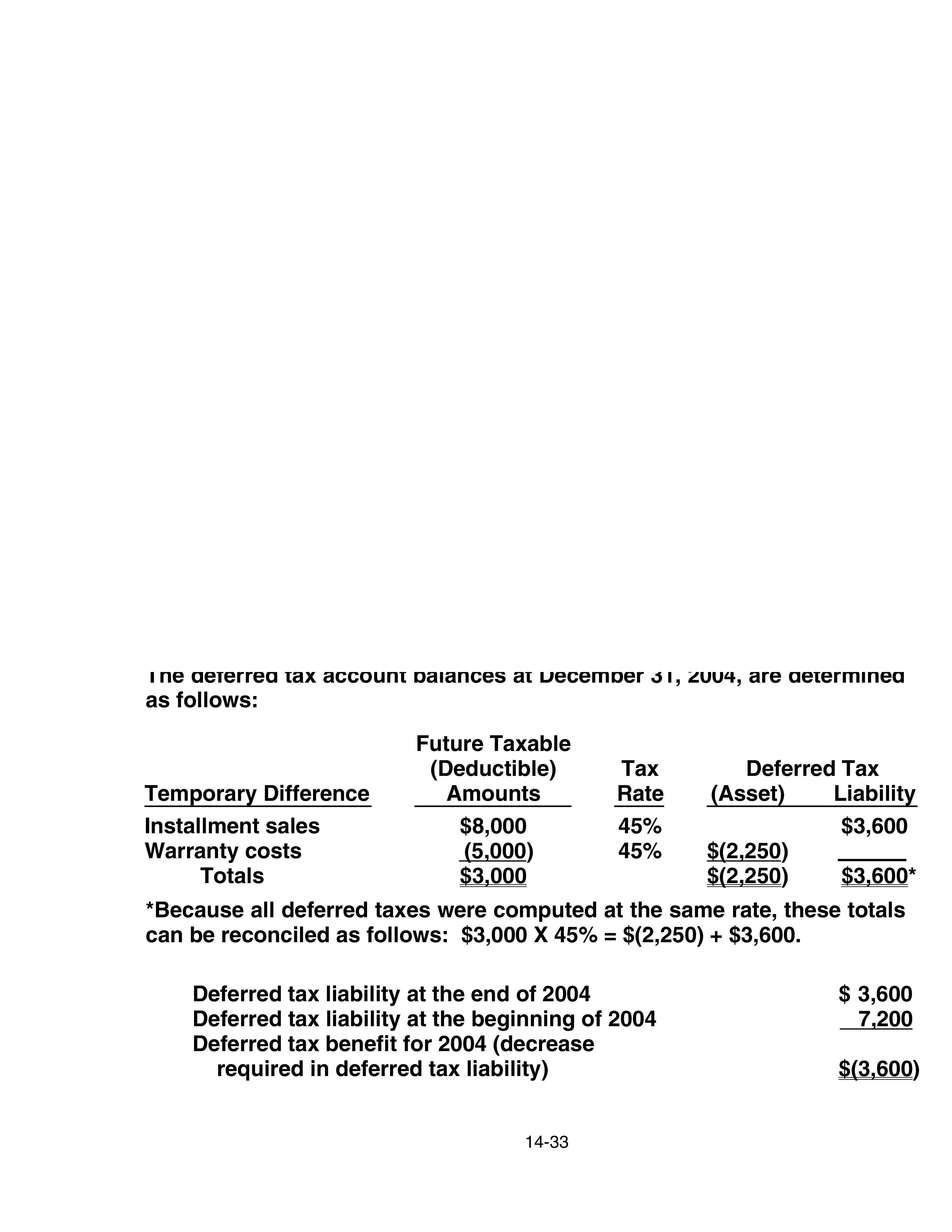

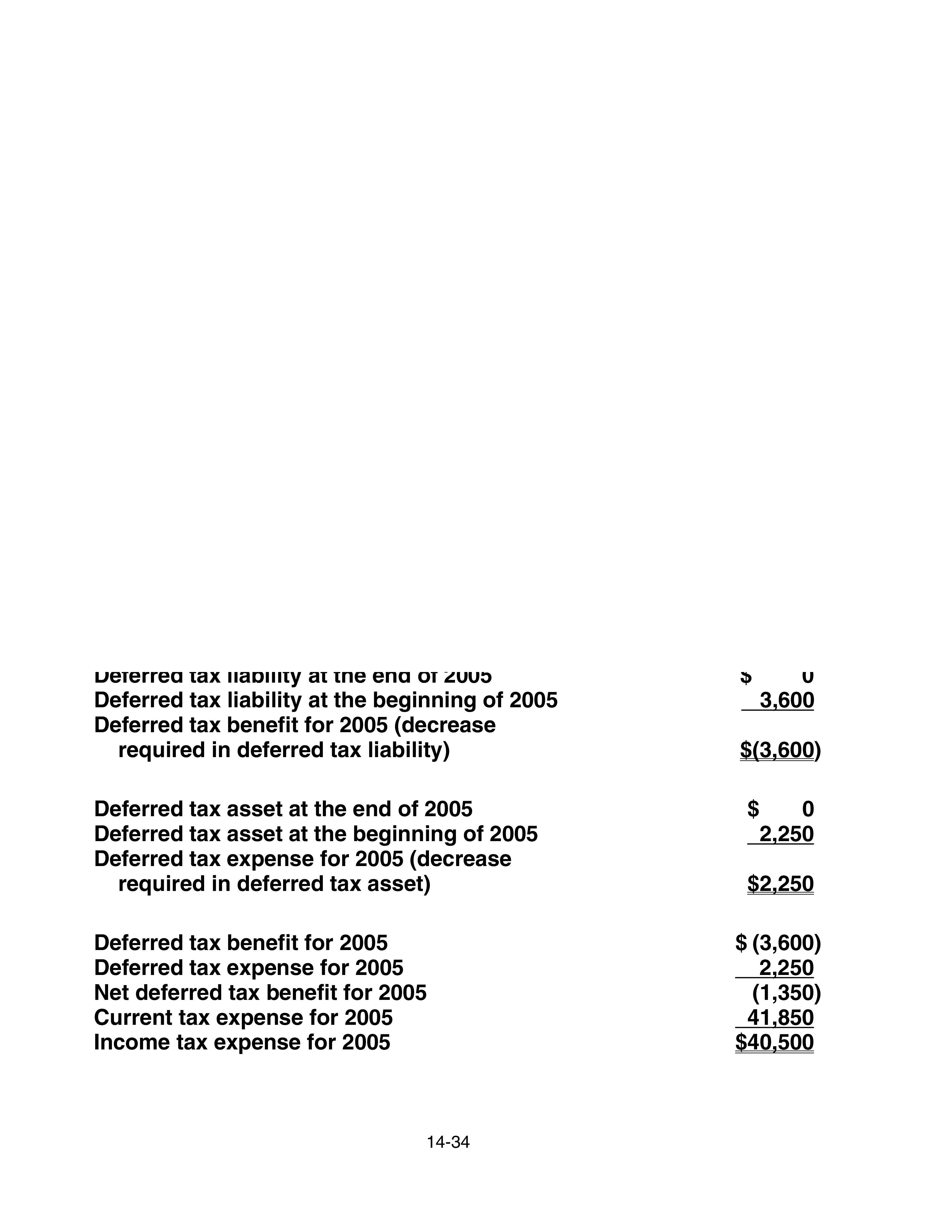

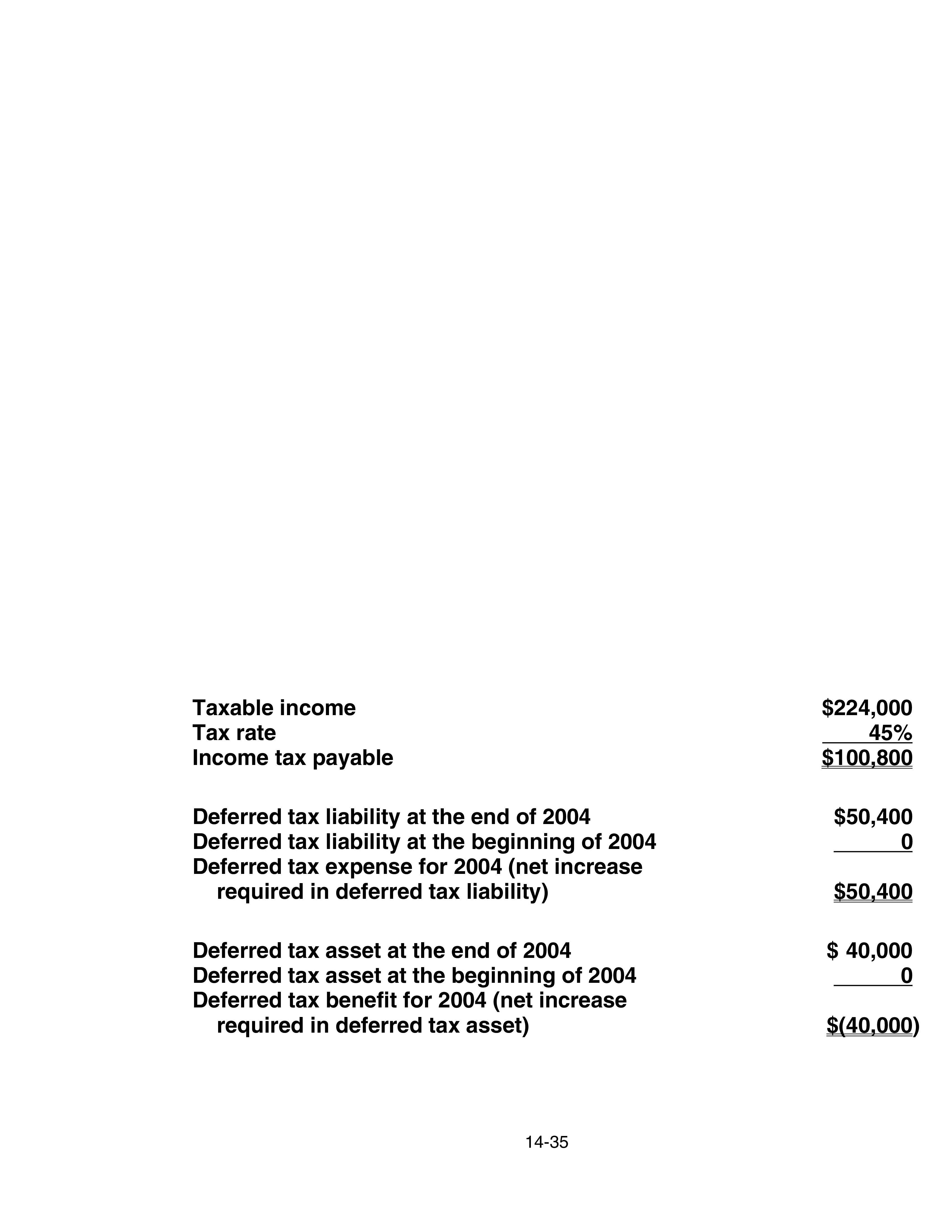

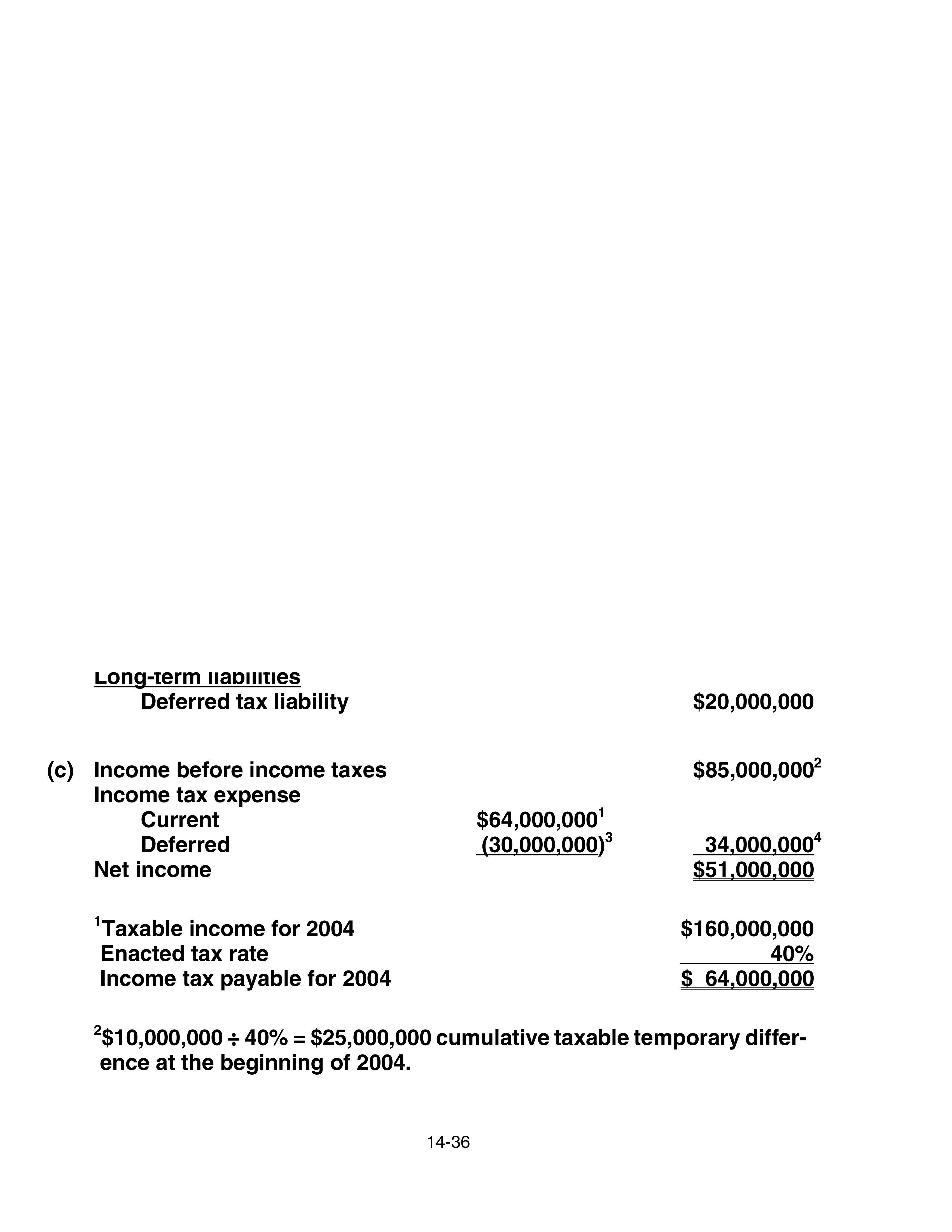

14-1

CHAPTER 14

Accounting for Income Taxes

ASSIGNMENT CLASSIFICATION TABLE

Topics

Questions

Brief

Exercises

Exercises

Problems

Cases

1. Reconcile pretax finan-

cial income with taxable

income.

1, 13 1 1, 2, 4, 7,

12, 18, 20,

21

1, 2, 3, 8

2. Identify temporary and

permanent differences.

2, 3, 4, 5 4, 5, 6, 7 3, 4, 5

3. Determine deferred in-

come taxes and related

items—single tax rate.

6, 7, 13 2, 3, 4, 5,

6, 7, 9

1, 3, 4, 5,

7, 8, 12,

14, 15, 19,

21, 23, 25

3, 4, 8, 9 2

4. Classification of deferred

taxes.

10, 11, 12, 8, 15 7, 11, 16,

18, 19, 20,

21, 22

1, 3, 6 2, 3, 5

5. Determine deferred in-

come taxes and related

items—multiple tax rates,

expected future income.

10 2, 13, 16,

17, 18, 20,

22

1, 2, 6, 7 1, 6, 7

6. Determine deferred taxes,

multiple rates, expected

future losses.

10

7. Carryback and carryfor-

ward of actual NOL.

14, 15, 18, 12, 13, 14 9, 10, 23,

24, 25

5

8. Change in enacted future

tax rate.

14 11 16 2, 7

9. Tracking temporary differ-

ences through reversal.

9 8, 17, 25 2, 7

14-2

ASSIGNMENT CLASSIFICATION TABLE (Continued)

Topics

Questions

Brief

Exercises

Exercises

Problems

Cases

10. Income statement

presentation.

9 1, 2, 3, 4,

5, 7, 10,

12, 16, 23,

24, 25

2, 3, 5, 7,

8, 9

11. Conceptual issues—

tax allocation.

1, 2, 8, 19 1, 2, 7

12. Valuation allowance—

deferred tax asset.

8, 18 7, 14, 15

13. Disclosure and other

issues.

15

14-3

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E14-1 One temporary difference, future taxable amounts, one rate,

no beginning deferred taxes.

Simple 15-20

E14-2 Two temporary differences, future deductible amounts, one

rate, no beginning deferred taxes.

Simple 15-20

E14-3 One temporary difference, future taxable amounts, one rate,

beginning deferred taxes.

Simple 15-20

E14-4 Three differences, compute taxable income, entry for taxes. Simple 15-20

E14-5 Two temporary differences, one rate, beginning deferred

taxes.

Simple 15-20

E14-6 Identify temporary or permanent differences. Simple 10-15

E14-7 Terminology, relationships, computations, entries. Simple 10-15

E14-8 Two temporary differences, one rate, traced for three years. Simple 10-15

E14-9 Carryback and carryforward of NOL, no valuation account,

no temporary differences.

Simple 15-20

E14-10 Two NOLs, no temporary differences, no valuation account,

entries and income statements.

Moderate 20-25

E14-11 Three differences, classify deferred taxes. Simple 10-15

E14-12 Two temporary differences, one rate, beginning deferred

taxes, compute pretax financial income.

Complex 20-25

E14-13 One difference, multiple rates, effect of beginning balance

versus no beginning deferred taxes.

Simple 20-25

E14-14 Deferred tax asset with and without valuation account. Moderate 20-25

E14-15 Deferred tax asset with previous valuation account. Complex 20-25

E14-16 Deferred tax liability, change in tax rate, prepare section of

income statement.

Complex 15-20

E14-17 Two temporary differences, tracked through three years,

multiple rates.

Moderate 30-35

E14-18 Three differences, multiple rates, future taxable income. Moderate 20-25

E14-19 Two differences, one rate, beginning deferred balance,

compute pretax financial income.

Complex 25-30

E14-20 Two differences, no beginning deferred taxes, multiple rates. Moderate 15-20

E14-21 Two temporary differences, multiple rates, future taxable

income.

Moderate 20-25

E14-22 Two differences, one rate, first year. Simple 15-20

E14-23 NOL carryback and carryforward, valuation account versus

no valuation account.

Complex 30-35

E14-24 NOL carryback and carryforward, valuation account needed. Complex 30-35

E14-25 NOL carryback and carryforward, valuation account needed. Moderate 15-20

P14-1 Four differences, beginning deferred balance, one rate. Complex 40-45

P14-2 One temporary difference, tracked for four years, one per-

manent difference, change in rate.

Complex 50-60

P14-3 Second year of depreciation difference, two differences,

single rate, extraordinary item.

Complex 40-45

P14-4 Permanent and temporary differences, one rate. Moderate 20-25

14-4

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

P14-5 Actual NOL without valuation account. Simple 20-25

P14-6 Two differences, two rates, future income expected. Moderate 20-25

P14-7 One temporary difference, tracked three years, change in

rates, income statement presentation.

Complex 45-50

P14-8 Two differences, two years, compute taxable income and

pretax financial income.

Complex 40-50

P14-9 Five differences, one year, income reporting. Complex 40-45

C14-1 Objectives and principles for accounting for income taxes. Simple 15-20

C14-2 Basic accounting for temporary differences. Moderate 20-25

C14-3 Identify temporary differences and classification criteria. Complex 20-25

C14-4 Accounting for and classification of deferred income taxes. Moderate 20-25

C14-5 Explain computation of deferred tax liability for multiple

tax rates.

Complex 20-25

C14-6 Explain future taxable and deductible amounts, how carry-

back and carryforward affects deferred taxes.

Complex 20-25

C14-7 Explain income effects of deferred taxes, ethics. Moderare 20-25

14-5

ANSWERS TO QUESTIONS

1. Pretax financial income is reported on the income statement and is often referred to as income

before income taxes. Taxable income is reported on the tax return and is the amount upon which

a company’s income tax payable is computed.

2. One objective of accounting for income taxes is to recognize the amount of taxes payable or re-

fundable for the current year. A second is to recognize deferred tax liabilities and assets for the

future tax consequences of events that have already been recognized in the financial statements

or tax returns.

3. A permanent difference is a difference between taxable income and pretax financial income that,

under existing applicable tax laws and regulations, will not be offset by corresponding differences

or “turn around” in other periods. Therefore, a permanent difference is caused by an item that: (1)

is included in pretax financial income but never in taxable income, or (2) is included in taxable in-

come but never in pretax financial income.

Examples of permanent differences are: (1) interest received on municipal obligations (such inter-

est is included in pretax financial income but is not included in taxable income), (2) premiums paid

on officers’ life insurance policies in which the company is the beneficiary (such premiums are not

allowable expenses for determining taxable income but are expenses for determining pretax fi-

nancial income), and (3) compensation expense associated with certain stock option plans. Item

(3), like item (2), is an expense which is not deductible for tax purposes.

4. A temporary difference is a difference between the tax basis of an asset or liability and its re-

ported (carrying or book) amount in the financial statements that will result in taxable amounts or

deductible amounts in future years when the reported amount of the asset is recovered or when

the reported amount of the liability is settled. The temporary differences discussed in this chapter

all result from differences between taxable income and pretax financial income which will reverse

and result in taxable or deductible amounts in future periods.

Examples of temporary differences are: (1) Gross profit or gain on installment sales reported for

financial reporting purposes at the date of sale and reported in tax returns when later collected.

(2) Depreciation for financial reporting purposes is less than that deducted in tax returns in early

years of assets’ lives because of using an accelerated method of depreciation for tax purposes.

(3) Rent and royalties taxed when collected, but deferred for financial reporting purposes and

recognized

as revenue when earned in later periods.

5. An originating temporary difference is the initial difference between the book basis and the tax ba-

sis of an asset or liability. A reversing difference occurs when a temporary difference that origi-

nated in prior periods is eliminated and the related tax effect is removed from the tax account.

6. Book basis of assets $900,000

Tax basis of assets 700,000

Future taxable amounts 200,000

Tax rate 34%

Deferred tax liability (end of 2004) $ 68,000

14-6

Questions Chapter 14 (Continued)

7. Book basis of asset

Tax basis of asset

Future taxable amounts

Tax rate

Deferred tax liability

(end of 2004)

$80,000

0

80,000

34%

$27,200

Deferred tax liability

(end of 2004)

Deferred tax liability

(beginning of 2004)

Deferred tax benefit for 2004

Income tax payable for 2004

Total income tax expense

for 2004

$ 27,200)

68,000)

(40,800)

230,000)

$189,200)

8. A future taxable amount will increase taxable income relative to pretax financial income in future

periods due to temporary differences existing at the balance sheet date. A future deductible

amount will decrease taxable income relative to pretax financial income in future periods due to

existing temporary differences.

A deferred tax asset is recognized for all deductible temporary differences. However, a deferred

tax asset should be reduced by a valuation account if, based on all available evidence, it is more

likely than not that some portion or all of the deferred tax asset will not be realized. More likely

than not means a level of likelihood that is at least slightly more than 50%.

9. Taxable income

Tax rate

Income tax payable

Deferred tax liability

(end of 2004)

Deferred tax liability

(beginning of 2004)

Deferred tax expense

for 2004

$100,000

40%

$ 40,000

$ 36,000

0

$ 36,000

Future taxable amounts

Tax rate

Deferred tax liability

(end of 2004)

Current tax expense

Deferred tax expense

Income tax expense for 2004

$90,000

40%

$36,000

$40,000

36,000

$76,000

10. Deferred tax accounts are reported on the balance sheet as assets and liabilities. They should be

classified in a net current and a net noncurrent amount. An individual deferred tax liability or asset

is classified as current or noncurrent based on the classification of the related asset or liability for

financial reporting. A deferred tax asset or liability is considered to be related to an asset or liabil-

ity if reduction of the asset or liability will cause the temporary difference to reverse or turn

around. A deferred tax liability or asset that is not related to an asset or liability for financial report-

ing, including deferred tax assets related to loss carryforwards, shall be classified according to the

expected reversal date of the temporary difference.

11. The balances in the deferred tax accounts should be analyzed and classified on the balance

sheet in two categories: one for the net current amount, and one for the net noncurrent amount.

This procedure is summarized as indicated below.

1. Classify the amounts as current or noncurrent. If an amount is related to a specific asset or

liability, it should be classified in the same manner as the related asset or liability. If not so

related, it should be classified on the basis of the expected reversal date.

2. Determine the net current amount by summing the various deferred tax assets and liabilities

classified as current. If the net result is an asset, report on the balance sheet as a current

asset; if it is a liability, report as a current liability.

14-7

Questions Chapter 14 (Continued)

3. Determine the net noncurrent amount by summing the various deferred tax assets and lia-

bilities classified as noncurrent. If the net result is an asset, report on the balance sheet as a

noncurrent asset (“other assets” section); if it is a liability, report as a long-term liability.

12. A deferred tax asset or liability is considered to be related to an asset or liability if reduction of the

asset or liability will cause the temporary difference to reverse or turn around.

13. Pretax financial income $550,000

Interest income on municipal bonds (70,000)

Hazardous waste fine 30,000

Depreciation ($60,000 – $45,000) 15,000

Taxable income 525,000

Tax rate 30%

Income tax payable $157,500

14. $200,000 (2007 taxable amount)

5% (30% – 25%)

$ 10,000 Decrease in deferred tax liability at the end of 2004

Deferred Tax Liability……………………………………………………………………. 10,000

Income Tax Expense …………………………………………………………….. 10,000

15. Some of the reasons for requiring these disclosures are:

(a) Assessment of the quality of earnings. Many investors seeking to assess the quality of a

company’s earnings are interested in the reconciliation of pretax financial income to taxable

income. Earnings that are enhanced by a favorable tax effect should be examined carefully,

particularly if the tax effect is nonrecurring.

(b) Better prediction of future cash flows. Examination of the deferred portion of income tax ex-

pense provides information as to whether taxes payable are likely to be higher or lower in

the future.

16. The carryback provision permits a company to carry a net operating loss back two years and re-

ceive refunds for income taxes paid in those years. The loss must be applied to the second pre-

ceding year first and then to the preceding year.

The carryforward provision permits a company to carry forward a net operating loss twenty years,

offsetting future taxable income. The loss carryback can be accounted for with more certainty be–

cause the company knows whether it has taxable income in the past; such is not the case with

income in the future.

17. The company may choose to carry the net operating loss forward, or carry it back and then for-

ward for tax purposes. To forego the two-year carryback might be advantageous where a tax-

payer had tax credit carryovers that might be wiped out and lost because of the carryback of the

net operating loss. In addition, tax rates in the future might be higher, and therefore on a present

value basis, it is advantageous to carry forward rather than carry back.

14-8

Questions Chapter 14 (Continued)

For financial reporting purposes, the benefits of a net operating loss carryback are recognized in

the loss year. The benefits of an operating loss carryforward are recognized as a deferred tax as-

set in the loss year. If it is more likely than not that the asset will be realized, the tax benefit of the

loss is also recognized by a credit to income tax expense on the income statement. Conversely, if

it is more likely than not that the loss carryforward will not be realized in future years, then an al-

lowance account is established in the loss year and no tax benefit is recognized on the income

statement of the loss year.

18. Many believe that future deductible amounts arising from net operating loss carryforwards are dif-

ferent from future deductible amounts arising from normal operations. One rationale provided is

that a deferred tax asset arising from normal operations results in a tax prepayment—a prepaid

tax asset. In the case of loss carryforwards, no tax prepayment has been made.

Others argue that realization of a loss carryforward is less likely—and thus should require a more

severe test—than for a net deductible amount arising from normal operations. Some have sug-

gested that the test be changed from “more likely than not” to “probable” realization. Others have

indicated that because of the nature of net operating losses, deferred tax assets should never be

established for these items.

14-9

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 14-1

2004 taxable income $110,000

Tax rate X 40%

12/31/04 income taxes payable $ 44,000

BRIEF EXERCISE 14-2

Excess depreciation on tax return $30,000

Tax rate 30%

Deferred tax liability $9,000

BRIEF EXERCISE 14-3

Income tax expense…………………………………………… $67,500 ***

Deferred tax liability……………………………………………………… 9,000 *

Income tax payable………………………………………………………. 58,500 *

* $195,000 x 30% = $58,500

** $30,000 x 30% = $9,000

*** $58,500 + $9,000 = $67,500

The $9,000 deferred tax liability should be classified as a noncurrent

liability. The balances in the deferred tax accounts should be classified

in the same manner as the related asset. Since property, plant, and

equipment is a noncurrent asset, noncurrent liability is the proper

classification for the deferred tax liability.

BRIEF EXERCISE 14-4

Deferred tax liability, 12/31/04 $42,000

Deferred tax liability, 12/31/03 25,000

Deferred tax expense for 2004 17,000

Current tax expense for 2004 43,000

Total tax expense for 2004 $60,000

14-10

BRIEF EXERCISE 14-5

Book value of warranty liability $125,000

Tax basis of warranty liability 0

Cumulative temporary difference at 12/31/04 125,000

Tax rate X 40%

12/31/04 deferred tax asset $ 50,000

BRIEF EXERCISE 14-6

Deferred tax asset, 12/31/04 $59,000

Deferred tax asset, 12/31/03 35,000

Deferred tax benefit for 2004 (24,000)

Current tax expense for 2004 61,000

Total tax expense for 2004 $37,000

BRIEF EXERCISE 14-7

Income Tax Expense ………………………………………………. 80,000

Allowance to Reduce Deferred Tax Asset

to Expected Realizable Value………………………… 80,000

BRIEF EXERCISE 14-8

Income before income taxes $175,000

Income tax expense

Current $40,000

Deferred 30,000 70,000

Net income $105,000

BRIEF EXERCISE 14-9

Income Tax Expense ………………………………………………. 71,100

Income Tax Payable ($144,000* X 45%)……………… 64,800

Deferred Tax Liability ($14,000 X 45%) ………………. 6,300

*$154,000 + $4,000 – $14,000 = $144,000

14-11

BRIEF EXERCISE 14-10

Year Future taxable amount Rate Deferred tax liability

2005

2006

2007

$ 42,000

294,000

294,000

34%

34%

40%

$ 14,280

99,960

117,600

$231,840

BRIEF EXERCISE 14-11

Income Tax Expense …………………………………………….. 80,000

Deferred Tax Liability ($2,000,000 X 4%) ………….. 80,000

BRIEF EXERCISE 14-12

Income Tax Refund Receivable ……………………………… 135,000

Benefit Due to Loss Carryback ……………………….. 135,000

$97,500 + [($450,000–$325,000) X 30%]

BRIEF EXERCISE 14-13

Income Tax Refund Receivable ……………………………… 160,000

Benefit Due to Loss Carryback ……………………….. 160,000

Deferred Tax Asset ($500,000 – $400,000) X .40………. 40,000

Benefit Due to Loss Carryforward …………………… 40,000

BRIEF EXERCISE 14-14

Income Tax Refund Receivable ……………………………… 160,000

Benefit Due to Loss Carryback ……………………….. 160,000

Deferred Tax Asset ($500,000 – $400,000) X .40………. 40,000

Benefit Due to Loss Carryforward …………………… 40,000

Benefit Due to Loss Carryforward………………………….. 40,000

Allowance to Reduce Deferred Tax Asset

to Expected Realizable Value………………………. 40,000

BRIEF EXERCISE 14-15

Current assets

Deferred tax asset $14,000