6/11/2023

1

CHAPTER 1:

CONCEPT OF AND NEED

FOR AUDIT

Instructor: Assoc.Prof. Dr. Doan Thanh Nga, CPA (Australia)

1

CHAPTER 1 LEARNING OBJECTIVES

1-1 Define the concept of assurance and compare the purposes and

characteristics of reasonable and limited levels of assurance obtained

from different assurance engagements

1-2 State why users desire assurance reports and provide examples of the

benefits gained from them such as to assure the quality of an entity’s

published corporate responsibility or sustainability report

1-3 Compare the functions and responsibilities of the different parties

involved in an assurance engagement

2

1

2

6/11/2023

2

1. WHAT IS ASSURANCE?

3

1.1. Definition

Assurance engagement: It is when a practitioner expresses a conclusion designed

to enhance the degree of confidence of the intended users other than the responsible

party about the outcome of the evaluation or measurement of a subject matter

against criteria.

1. WHAT IS ASSURANCE?

4

1.1. Definition

5 key elements of an assurance engagement:

Criteria

Report

Evidence

Subject matter

Three party relationship

3

4

6/11/2023

3

1. WHAT IS ASSURANCE?

5

1.1. Definition

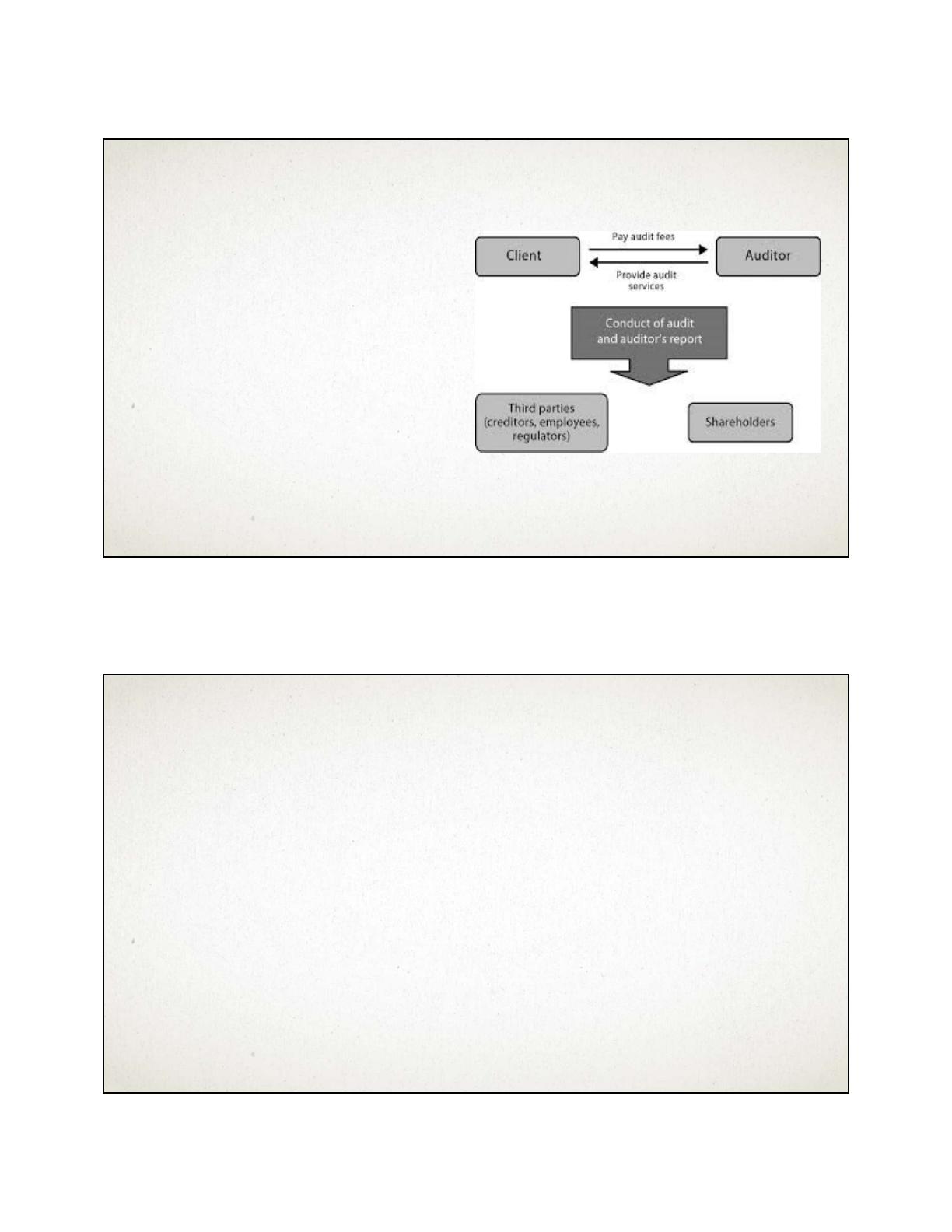

Three people or groups of people

involved:

– the practitioner (accountant)

– the intended users

– the responsible party (the person(s)

who prepared the subject matter)

Three party relationship

1. WHAT IS ASSURANCE?

6

1.1. Definition

Subject matter

The subject matter of an assurance engagement may vary considerably.

However, it is likely to fall into one of three categories:

•Data (for example, financial statements or business projections)

•Systems or processes (for example, internal control systems or computer

systems)

•Behaviour (for example, social and environmental performance or

corporate governance)

5

6

6/11/2023

4

1. WHAT IS ASSURANCE?

7

1.1. Definition

Criteria

Criteria: to judge whether the information is reliable and can be trusted.

For example, in an assurance engagement relating to financial statements, the

criteria may be accounting standards

Other criteria:

oprocesses may be compared to establish industry best practices (accredited

management standards such as ISO 9000)

oor behaviours to ethical standards, corporate governance or

environmental standards.

1. WHAT IS ASSURANCE?

8

1.1. Definition

Evidence

•The practitioner obtain and evaluate sufficient and appropriate evidence

to support the assurance opinion.

•The practitioner must obtain evidence as to whether the criteria have been

met.

•We will look at the collection of evidence in detail later in this Workbook.

7

8

6/11/2023

5

1. WHAT IS ASSURANCE?

9

1.1. Definition

Report

•Provided in the form of a written report and will contain key information

and any issues or assurances given as a result of the engagement.

Context example: Assurance engagement

Workbook: page 7

10

1. WHAT IS ASSURANCE?

1.1. Definition

9

10

6/11/2023

6

You are an accountant who has been approached by Jamal, who wants to invest in

Company X. He has asked you for assurance whether the most recent financial

statements of Company X are a reliable basis for him to make his investment decision.

Requirement

Identify the key elements of an assurance engagement in this scenario, if you accepted

the engagement.

Interactive question 1: Assurance engagement (p. 7)

11

12

1. WHAT IS ASSURANCE?

1.2. Levels of assurance

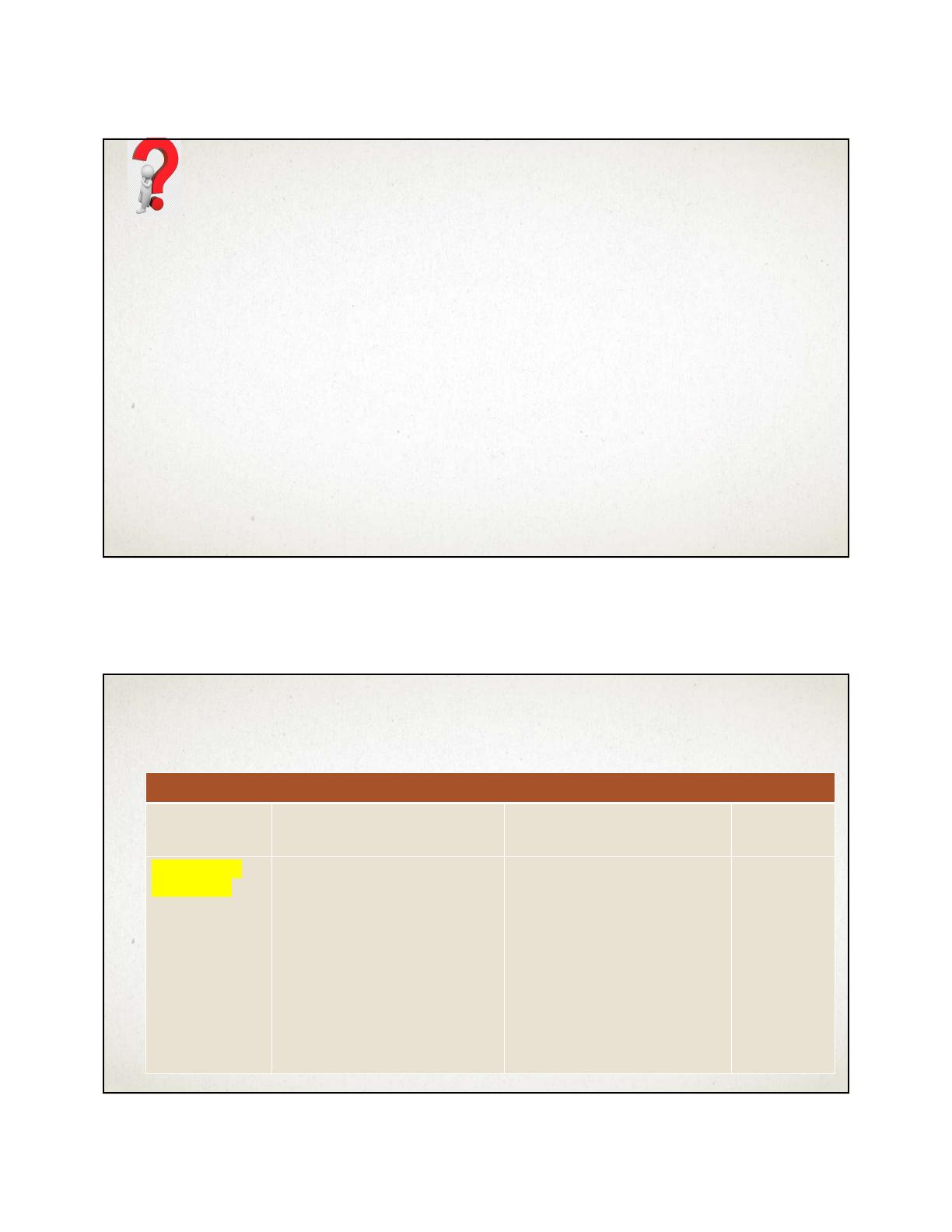

Summary of types of engagement

Conclusion

given

Example of wording Evidence obtainedType of

engagement

Positive

expression

In our opinion, the financial

statements present fairly, in

all material respects, (or give

a true and fair view of) the

financial position of the

Company, and of its financial

performance and its cash

flows for the year.

Sufficient appropriate

evidence is obtained by:

•Obtaining an understanding

of the entity

•Assessing risk

•Responding to risk

•Performing further

procedures (sampling) to

draw a conclusion

Reasonable

assurance

engagement:

High level of

assurance (less

than absolute

assurance)

Eg: statutory

audit

11

12

6/11/2023

1. WHAT IS ASSURANCE?

1.2. Levels of assurance

Summary of types of engagement

Conclusion

given

Example of wording Evidence sought Type of

engagement

Negative

expression

Based on our work described in

this report, nothing has come to

our attention that causes us to

believe that internal control is

not effective, in all material

respects, based on XYZ criteria.

The evidence gathered

is limited, involving

techniques such as

enquiry and analytical

procedures

Limited

assurance

engagement

(less than

reasonable

assurance)

Eg: review of