Capodieci Carola 3074708

Donativo Elisa 3068950

Lin Meng 3075257

Sossi Arianna 3065707

Zambolin Alice 3076518

BIEM 18

NINA PINTA SANTA MARIA & Co.

OCEAN CARRIERS

CASE STUDY

EXECUTIVE SUMMARY

Ocean Carriers, a shipping company with headquarters in New York and Hong Kong, is

evaluating a proposed three-year ship lease starting in 2003. Currently, Ocean Carriers does not

have any capesize carrier that meets the customer’s requirements.

Based on our financial analysis, we strongly suggest that Ocean Carriers should accept the

proposal only if the financial base will be set in Hong Kong, where the tax rate is 0%.

Until now the company has always operated vessels not older than 15 years. After the 15th

year, the vessels were scrapped or sold in the secondhand market. However, our computations show

that it will be more profitable to extend their use to 25 years.

SUMMARY OF FACTS

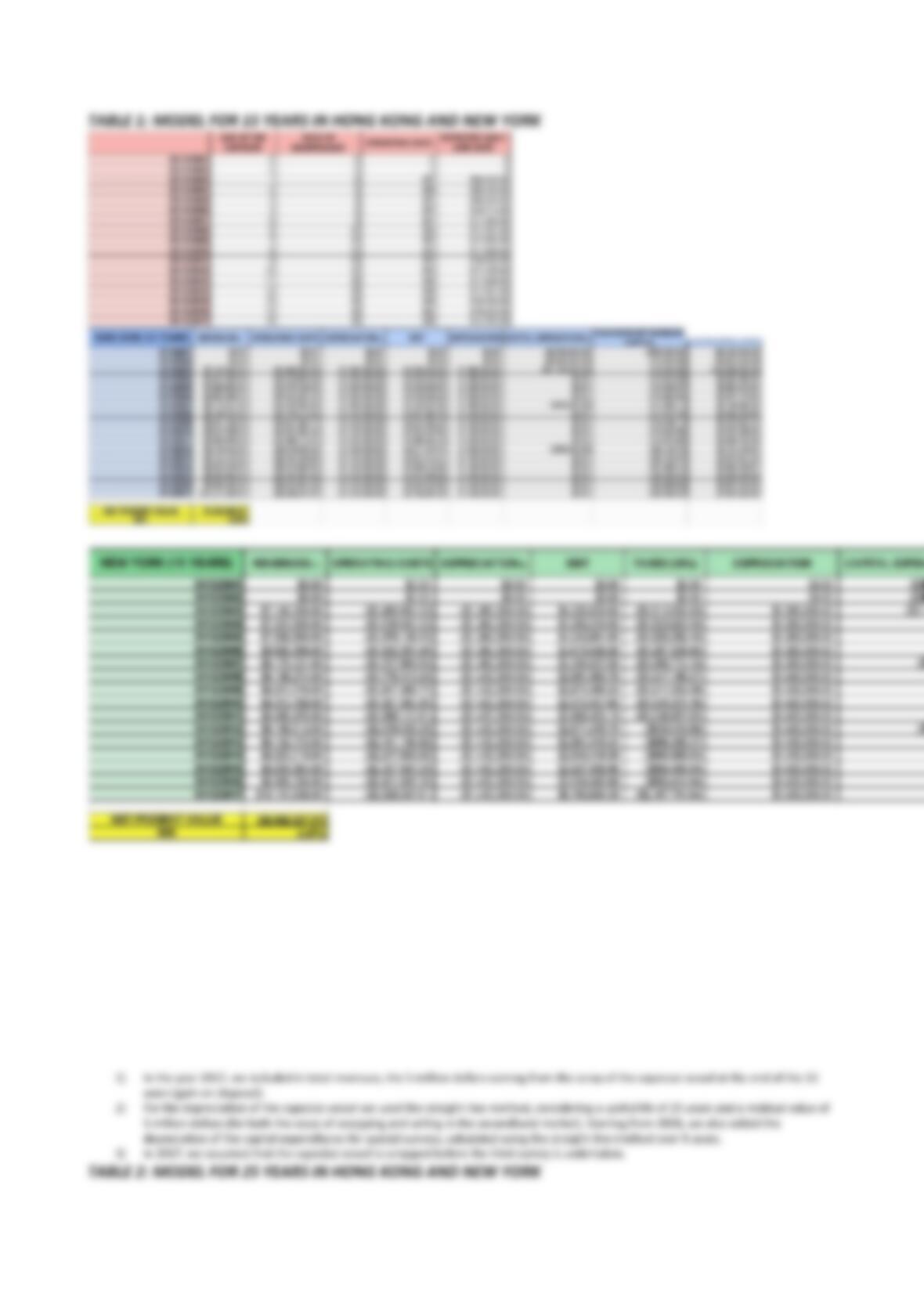

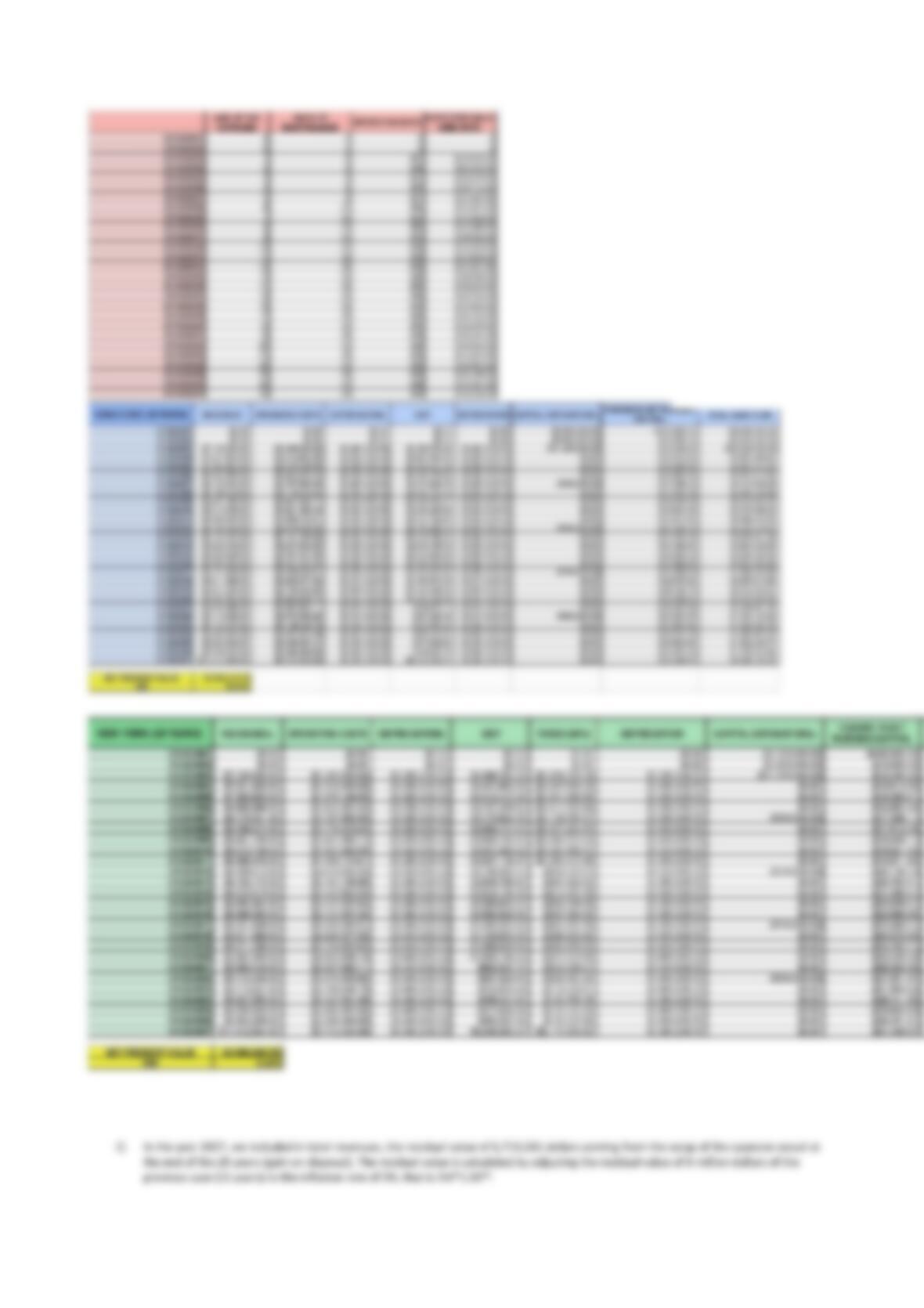

The profitability of the investment depends on the cost of commissioning a new capesize

ship, inflation, daily spot hire rates, operating costs, depreciation and future market expectations.

The price of the new charter, $39 million, will be paid in 3 installments: 10% due immediately,

another 10% in a year’s time and the rest at delivery date. The entire amount is depreciated on a

straight-line basis, with a residual value of $5M in the case of 15 years of usage and $6,719,582

1

in

the case of 25 years. Ocean Carriers incurs operating costs of $4,000 per day during the first year

and they are expected to increase at a rate of 1% above inflation, namely 3%+1%=4%.

The new capesize vessel will be rented for $20,000 a day with an annual escalation of $200

per day, while by the end of the contract the daily rent is assumed to follow the adjusted daily hire

rate. During maintenance days – 8 for the first 5 years, 12 for the following 5 and subsequently 16 –

the hire rate will not be charged, while operating costs will nonetheless incur.

As shown in Exhibit 1, the company anticipates the amounts in preparation for the Special

1

5M*1.03^10

Surveys, to be depreciated using a straight-line method over a 5-year period. Moreover, Mary Linn

forecasts an initial investment in net working capital of $500,000 which will increase with inflation.

STATEMENT OF THE PROBLEM

This analysis is aimed to analyze the long-term profitability of commissioning a new

capesize to satisfy the requirements of the leasing contract, which only locks the daily hire rates for

three years. We will consider two alternative cases, namely a tax-free scenario in which Ocean

Carriers is based in Hong Kong, and another where it is instead subject to a 35% tax rate in New

York. In addition, we will also evaluate whether it is reasonable to adopt an alternative policy

according to which the vessels are kept for more than 15 years.

ANALYSIS

In order to assess the profitability of the investment opportunity, we will analyze the term

structure of daily hire rates and the long-term prospects of the capesize dry bulk market.

The main drivers of spot hire rates are the forces of demand and supply for shipping. The

demand is influenced by the world economy in the basic industries, mostly iron and coal, and