Page 1 of 4

THE INSTITUTE OF COST AND MANAGEMENT ACCOUNTANTS OF BANGLADESH

CMA DECEMBER 2013, EXAMINATION

FOUNDATION LEVEL

SUBJECT: 001. PRINCIPLES OF ACCOUNTING

Time: Three hours Full Marks: 100

All questions are to be attempted.

Show computations, where necessary.

Answer must be brief, relevant, neat and clean.

Start answering each question from a fresh sheet.

Q. No. 1.

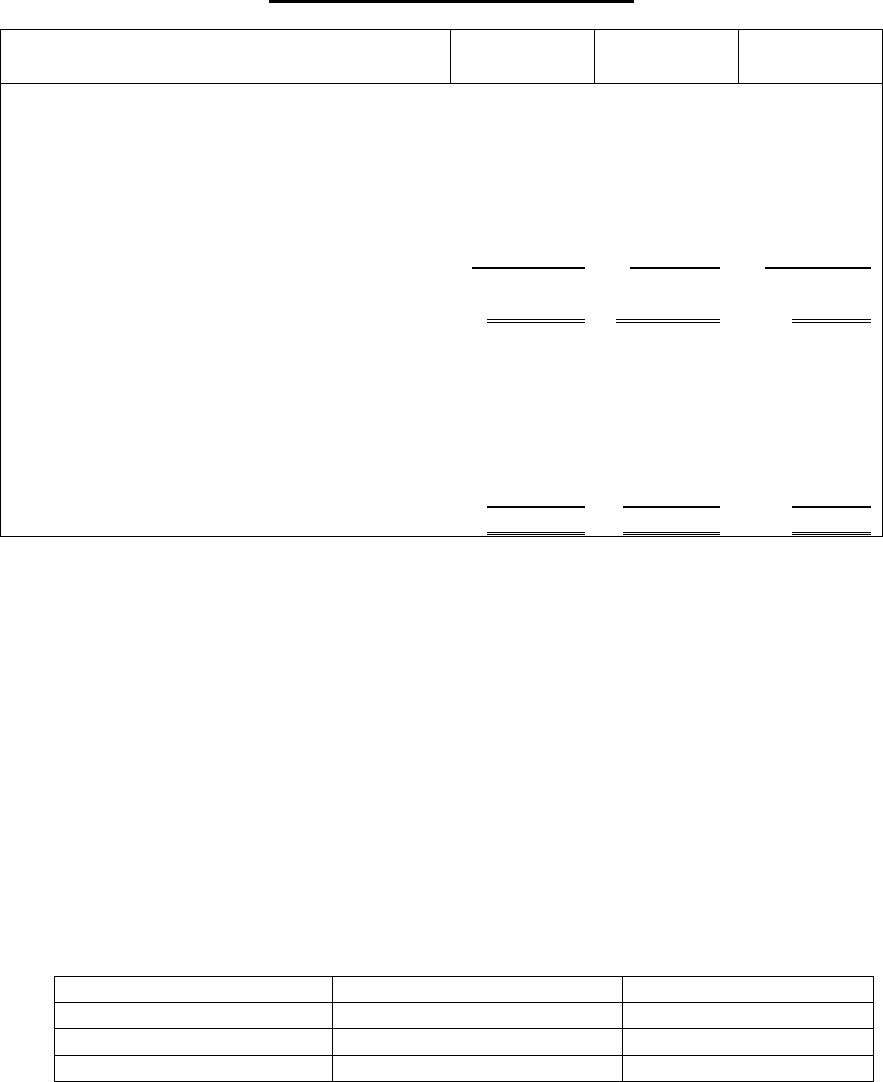

The following is the Trial Balance of M/S Aziz & Co. as on December 31, 2010:

Debit(Tk.)

Credit(Tk.)

Capital

7,05,000

Sales

18,98,550

Purchase

12,97,500

Sales Returns

5,250

Accounts Receivable

1,24,500

Cash

63,000

Petty Cash

7,500

Bank Account

3,67,500

Notes Receivable

18,000

Notes Receivable Discounted

15,000

Office Supplies

25,500

Prepaid Insurance

15,750

Accounts Payable

1,87,500

Notes Payable

75.000

Allowance for Bad Debts

9,000

Inventory (1-1-2010)

3,75,000

Delivery Equipment

4,05,000

Accumulated Depreciation– Delivery Equipment

2,02,500

Furniture and Fixtures

1,12,500

Accumulated Depreciation – Furniture and Fixtures

22,500

Machinery and Equipment

3,75,000

Accumulated Depreciation – Machinery and Equipment

75,000

Retained Earnings

69,000

Advertising

18,000

Delivery Salaries

54,000

Office Salaries

39,000

Interest Income

15,450

Interest Expenses

24,000

Suspense Account

52,500

33,27,000

33,27,000

The following adjustments are to be made on December 31, 2010 before closing the books:

1. Inventory on hand at December 31, 2010 Tk. 3,90,000

2. Office supplies Tk. 10,500

3. Bad debt allowance is to be increased by Tk. 12,000

4. Depreciation is to be charged: Delivery Equipment–10%, Furniture & Fixture–15% and

Machinery & Equipment–5%

5. Accrued delivery salaries Tk. 18,000

6. Pre–paid insurance Tk. 5,250

7. Unearned interest income Tk. 1,500

8. Delivery Equipment purchased 5 years back, with Book Value of Tk. 37,500 sold out at

Tk. 52,500 and erroneously credited the sale proceeds to Suspense Account.

9. Advertising expense includes Tk. 8,100 for new product to be sold in 2011.

Page 2 of 4

CMA DECEMBER 2013, EXAMINATION

FOUNDATION LEVEL

SUBJECT : 001. PRINCIPLES OF ACCOUNTING.

Q. No. 1. (cont’d……………)

Required:

(i) Prepare a multiple– step income statement for the year and a classified balance sheet

as on December 31, 2010.

(ii) Pass adjusting and closing entries. [Marks: (15+5) = 20]

Q. No. 2.

(a) Define Revenue as per IAS 18.

(b) A Tk. 210,000 fixed–price contract is entered into for the provision of services. At the

end of 2007, the first accounting period, the contract is thought to be 33% complete

and costs of Tk. 45,000 have been incurred in performing that 33% of the work.

Required:

Calculate the revenue to be recognized in 2007 on the alternative assumptions that:

(i) The costs to complete are reliably estimated at Tk. 90,000; and

(ii) The costs to complete cannot be reliably estimated and it is thought that Tk.

40,000 of the costs incurred are recoverable from the customer.

Fill in the proforma below:

(i) Cost to complete are Tk. 90,000.

(ii) Cost to complete cannot be estimated reliably.

(c) LATENTILE LTD

Latentile Ltd. is a newly–formed company, which uses a chemical process to

manufacture a revolutionary new roof covering, which it sells at a mark–up of 25% on

cost. Its inventories consist of raw material, work in progress and finished goods, and

at the end of its first year of trading, it is having problems valuing inventories.

You ascertain the following information:

(1) Raw material

(i) The process needs at least 100,000 kgs of clay to continue working, but a

physical inventory count reveals that the machinery contains 108,000 kgs.

(ii) The original cost of the initial 100,000 kgs to set up the process was 30p

per kg and you find an invoice to show that the last consignment of 20,000

kgs cost 31p per kg. All other consignments in the year (a total of 200,000

kgs) cost 32p per kg.

(2) Work in progress

(i) The work in progress is currently all 60% complete and you discover that

there are 50,000 units currently going through the process.

(ii) The total number of complete units for the period was, as anticipated,

800,000.

(iii) The costs for the process for the period were as follows.

Tk. ’000

Raw materials 200

Direct labour 242

Factory overheads 191

Administrative expenses attributable to production 114

Distribution costs 90

(3) Finished Goods

(i) There were 70,000 units in inventories.

(ii) Of (i) above, it was intended to sell 20,000 units at 75p per unit, a discount

of one third on normal selling price, in a future promotional campaign (a

further 10p per unit distribution costs is to be incurred).

Required:

(i) Explain how BAS 2 Inventories applies the accrual and the going concern bases of

accounting.

Page 3 of 4

CMA DECEMBER 2013, EXAMINATION

FOUNDATION LEVEL

SUBJECT : 001. PRINCIPLES OF ACCOUNTING.

Q. No. 2.(cont’d……………)

(ii) For each of the above categories of inventory, suggest a method of valuation and show

the value as it would appear in the balance sheet.

(iii) If the information regarding costs for the period were not available, suggest an

alternative method of valuing finished goods. [Marks: (4+8+8) = 20]

Q. No. 3.

(a) Explain the term “bank reconciliation” and state the reasons for its preparation.

(b) ABC, a sole trader received his bank statement for the month of June 2001. At that

date the bank balance was Tk. 706,500 whereas his cash book balance was Tk.

2,366,500. His accountant investigated the matter and discovered the following

discrepancies:

1. Bank charges of Tk. 3,000 had not been entered in the cashbook.

2. Cheques drawn by ABC totaling Tk. 22,500 had not yet been presented to the

bank.

3. He had not entered receipts of Tk. 26,500 in his cashbook.

4. The bank had not credited Mr. ABC with receipts of Tk. 98,500 paid into the bank

on 30 June 2001.

5. Standing order payments amounting to Tk. 62,000 had not been entered into the

cashbook.

6. In the cashbook ABC had entered a payment of Tk. 74,900 as Tk. 79,400.

7. A cheque for Tk.15,000 from a debtor had been returned by the bank marked

“refer to drawer” but had not been written back into the cashbook.

8. ABC had brought forward the opening cash balance of Tk. 329,250 as a debit

balance instead of a credit balance.

9. An old cheque payment amounting to Tk. 44,000 had been written back in the

cashbook but the bank had already honored it.

10. Some of ABC’s customers had agreed to settle their debts by paying directly into

his bank account. Unfortunately, the bank had credited some deposits amounting

to Tk. 832,500 to another customer’s account. However acting on information

from his customers ABC had actually entered the expected receipts from the

debtors in is cashbook.

Required:

(i) A statement showing ABC’s adjusted cashbook balance as at 30 June 2001.

(ii) A bank reconciliation statement as at 30 June 2001.

[Marks: 5+15 = 20]

Q. No. 4.

(a) Briefly explain the nature and purpose of accounting for depreciation.

(b) (i) A motor van was bought for Tk. 20,000 on 1 September 2005 with a residual value of

Tk. 2,000. Depreciation was charged at 20% by the reducing balance method on yearly

basis. It was sold for Tk. 18,000 after three years of use on 30 September 2008.

Compute the profit on sale of asset.

(ii) A company is exploring the impact of the two method of depreciation. On 1 January, it

bought machinery for Tk.15,000. The methods are (i) straight line where useful life is 4

years and residual value is Tk. 2,000 and (ii) Reducing balance method – at the rate of

20% per annum. Show how the company’s profit be affected if the straight line method

is used rather than the reducing method?

(iii) A machine was bought for Tk.100,000. Its estimated useful life is four years with a

residual value of Tk.10,000. Depreciation is charged on the straight line method. What

is the percentage of depreciation rate on an annual basis?

Page 4 of 4

CMA DECEMBER 2013, EXAMINATION

FOUNDATION LEVEL

SUBJECT : 001. PRINCIPLES OF ACCOUNTING.

Q. No. 4. (cont’d……………)

(iv) A machine which was bought for Tk.180,000 on 30 April 2008. The residual value was

Tk. 5,000 and depreciation rate was 25%. Depreciation is to be charged under the

reducing balance method on month to month basis. Compute the depreciation at 31st

December 2008.

(v) A fixed asset cost Tk.100,000 had a book value of Tk. 40,000. It was sold for

Tk.10,000. What is the provision for depreciation sold? [Marks: 5 + (3+3+3+3+3) = 20]

Q. No. 5.

Careg Ltd manufactures and sells heavy plant. The company also hires out plant for monthly

periods (or multiples thereof). You ascertain the following details:

(1) Freehold land:

Freehold land was acquired on 1 February 2008 for Tk. 100,000 to build a new factory.

Due to planning difficulties, building has not yet been started. The directors wish to

revalue the land to its fair value of Tk.130,000 at 30 September 2009.

(2) Buildings:

On 1 October 2008 the directors reviewed the useful life of the buildings and determined

that the remaining life was 56 years. The buildings were acquired for Tk. 200,000 on 1

October 2004, when their useful life was estimated at 40 years.

(3) Plant and Machinery:

Plant and machinery is accounted for under the cost model accounting policy and is

depreciated at the rate of 40% per annum based on carrying amount. Such plant has an

estimated life of five years.

(i) Plant which cost Tk. 20,000 on 1 October 2006 was classified as held for sale on 1

February 2009. The sale was agreed at Tk. 5,600 and completed on 31 March

2009.

(ii) New plant acquired cost Tk. 60,000 on 1 January 2009.

At 1 October 2008 the cost of plant and machinery (not leased) was Tk. 200,000, with

accumulated depreciation of Tk. 72,000.

(4) Computer:

Previously this has been depreciated on a straight–line basis at the rate of 10% per

annum on cost. The computer was acquired on 1 January 2007 for Tk. 60,000, and by

the beginning of this accounting year Tk.10,500 of depreciation had been charged. In an

effort to charge out computer time to departments, a record is now kept of computer time

used. Management wishes to depreciate the computer on a usage basis. The

manufacturer’s estimate of total usage time of the computer’s life is 40,000 hours. The

data processing manager estimates that some 10,000 hours have been worked prior to

the current accounting period. During the current year the record shows 4,800 hours

worked. The computer will have a scrap value of Tk. 4,500 at the end of its useful life.

Required:

(i) Prepare the schedule of non–current assets which will form the note to the company’s

published balanced sheet at 30 September 2009.

(ii) Briefly explain the qualitative characteristics contained in BFRS-1 Framework for the

Preparation and Presentation of Financial Statements illustrating your answer with

reference to the provisions of BAS 16 Property, Plant and Equipment.

[Marks: (16+4) = 20]

=THE END =

Page 1 of 2

THE INSTITUTE OF COST AND MANAGEMENT ACCOUNTANTS OF BANGLADESH

CMA DECEMBER 2013, EXAMINATION

FOUNDATION LEVEL

SUBJECT: 002. BUSINESS COMMUNICATION AND OFFICE MANAGEMENT.

Time: Three Hours

Full Marks:100

Answer THREE questions from each part, where Q. No. 4 and 8 are compulsory.

Answer must be brief, relevant, neat and clean.

Use fresh sheet for answering each question.

GROUP – A : BUSINESS COMMUNICATION

Q. No. 1.

(a) Define Business Communication. What are the conditions of communication?

(b) Discuss the requirements of effective Communication.

(c) What are the main problems of communication in the business enterprise of Bangladesh?

[Marks: (5+5+5) = 15]

Q. No. 2.

(a) What are the forms of upward communication?

(b) Discuss the process to write a Cover Letter.

(c) XYZ Enterprise wishes to place an order with Asian Paints Ltd. for various paints. Prepare

an order using imaginary terms and conditions.

[Marks: (4+5+6) = 15]

Q. No. 3.

(a) Write your resume with a forwarding letter to the H.R. department of XYZ. Ltd. for the

suitable post in Finance department.

(b) What is corporate annual report? What is the difference between statutory meeting and

statutory reports?

(c) Write a business report to be placed on the board meeting regarding the market position of

an export oriented manufacturing industry.

[Marks: (4+5+6) = 15]

Q. No. 4.

Write short notes on any FIVE of the following:

(a) Short Analytical Report;

(b) Oral Communication;

(c) Bill of Exchange;

(d) Central Depository system (CDS);

(e) Organization chart;

(f) Letter of credit;

(g) Certificate of Incorporation;

(h) EPB;

(i) SAFA.

[Marks: (4 x 5) = 20]

Page 2 of 2

CMA DECEMBER 2013, EXAMINATION

FOUNDATION LEVEL

SUBJECT: 002. BUSINESS COMMUNICATION AND OFFICE MANAGEMENT.

GROUP – B : OFFICE MANAGEMENT

Q. No. 5.

(a) Define the term “Inter office relationship”. Discuss the main features stating nature of office

work.

(b) Office management is the task of planning, coordinating and motivating the efforts towards

the specific objective in the office. Discuss.

(c) Why “noise control” is essential and how it can be achieved?

[Marks: (5+5+5) = 15]

Q. No. 6.

(a) What is the meaning of Industrial Engineering?

(b) How “Time Study” and “Motion Study” increase the productivity of an organization?

(c) What factors would you consider before selecting a suitable filing system?

[Marks: (5+5+5) = 15]

Q. No. 7.

(a) What is motivation? Discuss the business ethics in the office.

(b) Describe the procedure for maintaining incoming and outgoing mail of an office.

(c) Discuss the position of office manager in the organization.

[Marks: (6+5+4) = 15]

Q. No. 8.

Write short notes on any FIVE of the following:

(a) Office automation.

(b) Job description and Job Specification.

(c) Security and secrecy.

(d) File server & Exchange server.

(e) Transference and good governance.

(f) Code of conduct in the organization.

(g) Scientific Office Management.

(h) Page indexing.

[Marks: (4 x 5) = 20]

= THE END =

THE INSTITUTE OF COST AND MANAGEMENT ACCOUNTANTS OF BANGLADESH

CMA DECEMBER 2013, EXAMINATION

FOUNDATION LEVEL

SUBJECT: 003. QUANTITATIVE TECHNIQUES.

Time: Three hours

Full Marks: 100

Answer any TEN questions, FIVE from each part.

Answer must be brief, relevant, neat and clean.

Use a fresh sheet for answering each question.

Start answering each question from a fresh sheet.

PART – A: BUSINESS MATHEMATICS

Q. No. 1.

(a) The universal set is given by

},20:{ ∈= xxxU N,

and

},14,8,6,2{=A

},14,10,8,4{=B

}.18,14,12,10,6{=C

Find (i)

,‘‘ BA ∪

(ii)

),‘‘( BAC ∪∩

(iii)

).( CBA −∩

(b) Out of the total 150 students who appeared in an examination, 45 failed in Accounting, 50

failed in Business Mathematics, and 45 in Costing. Those who failed both in Accounting

and Business Mathematics were 30, those who failed both in Business Mathematics and

Costing were 32, and those who failed both in Accounting and Costing were 35. The

students who failed in all three subjects were 25. Find out the number of students who

failed at least in any one of the subjects. [Marks: (5+5) = 10]

Q. No. 2.

(a) Income of a man from interest and wages is Tk.5000. He doubles his interest and also

gets an increase of 50% in wages and his income increases to Tk.8000. What was his

original income separately in terms of interest and wages?

(b) Tk.15,000 is invested at the beginning of 1998. It remains invested and on 1st January

each subsequent year, another Tk.600 is added to it. What sum will be available on 1st

January 2005 if interest is compounded annually at the rate of 4% per annum?

[Marks: (5+5) = 10]

Q. No. 3.

(a) A factory produces 400 bulbs for a total cost of Tk.1600 and 800 bulbs for a total cost of

Tk.2400. Given that the cost curve is a straight line, find the equation of the straight line

and use it to find the cost of producing 5000 bulbs.

(b) A manufacturer has a fixed cost of Tk.60,000 and variable cost is Tk.9 per unit of

production. Selling price is Tk.12 per unit.

(i) Write the revenue and cost functions.

(ii) At what number of units will break–even occur?