Chapter 8

Master Budgeting

Solutions to Questions

8-1 A budget is a detailed quantitative plan

for the acquisition and use of financial and other

resources over a given time period. Budgetary

control involves using budgets to increase the

likelihood that all parts of an organization are

working together to achieve the goals set down

in the planning stage.

8-2

1. Budgets communicate management’s

plans throughout the organization.

2. Budgets force managers to think about

and plan for the future. In the absence of the

necessity to prepare a budget, many managers

would spend all of their time dealing with day-

to-day emergencies.

3. The budgeting process provides a means

of allocating resources to those parts of the

organization where they can be used most

effectively.

4. The budgeting process can uncover

potential bottlenecks before they occur.

5. Budgets coordinate the activities of the

entire organization by integrating the plans of its

various parts. Budgeting helps to ensure that

everyone in the organization is pulling in the

same direction.

6. Budgets define goals and objectives that

can serve as benchmarks for evaluating

subsequent performance.

8-3 Responsibility accounting is a system in

which a manager is held responsible for those

items of revenues and costs—and only those

items—that the manager can control to a

significant extent. Each line item in the budget is

made the responsibility of a manager who is

then held responsible for differences between

budgeted and actual results.

8-4 A master budget represents a summary

of all of management’s plans and goals for the

future, and outlines the way in which these

plans are to be accomplished. The master

budget is composed of a number of smaller,

specific budgets encompassing sales,

production, raw materials, direct labor,

manufacturing overhead, selling and

administrative expenses, and inventories. The

master budget usually also contains a budgeted

income statement, budgeted balance sheet, and

cash budget.

8-5 The level of sales impacts virtually every

other aspect of the firm’s activities. It

determines the production budget, cash

collections, cash disbursements, and selling and

administrative budget that in turn determine the

cash budget and budgeted income statement

and balance sheet.

8-6 No. Planning and control are different,

although related, concepts. Planning involves

developing goals and developing budgets to

achieve those goals. Control, by contrast,

involves the means by which management

attempts to ensure that the goals set down at

the planning stage are attained.

8-7 Creating a “budgeting assumptions” tab

simplifies the process of determining how

changes to a master budget’s underlying

assumptions impact all supporting schedules and

the projected financial statements.

8-8 A self-imposed budget is one in which

persons with responsibility over cost control

prepare their own budgets. This is in contrast to

a budget that is imposed from above. The major

advantages of a self-imposed budget are: (1)

Individuals at all levels of the organization are

recognized as members of the team whose

views and judgments are valued. (2) Budget

estimates prepared by front-line managers are

often more accurate and reliable than estimates

prepared by top managers who have less

intimate knowledge of markets and day-to-day

operations. (3) Motivation is generally higher

when individuals participate in setting their own

goals than when the goals are imposed from

above. Self-imposed budgets create

commitment. (4) A manager who is not able to

meet a budget that has been imposed from

above can always say that the budget was

unrealistic and impossible to meet. With a self–

imposed budget, this excuse is not available.

Self-imposed budgets do carry with

them the risk of budgetary slack. The budgets

prepared by lower-level managers should be

carefully reviewed to prevent too much slack.

8-9 The direct labor budget and other

budgets can be used to forecast workforce

staffing needs. Careful planning can help a

company avoid erratic hiring and laying off of

employees.

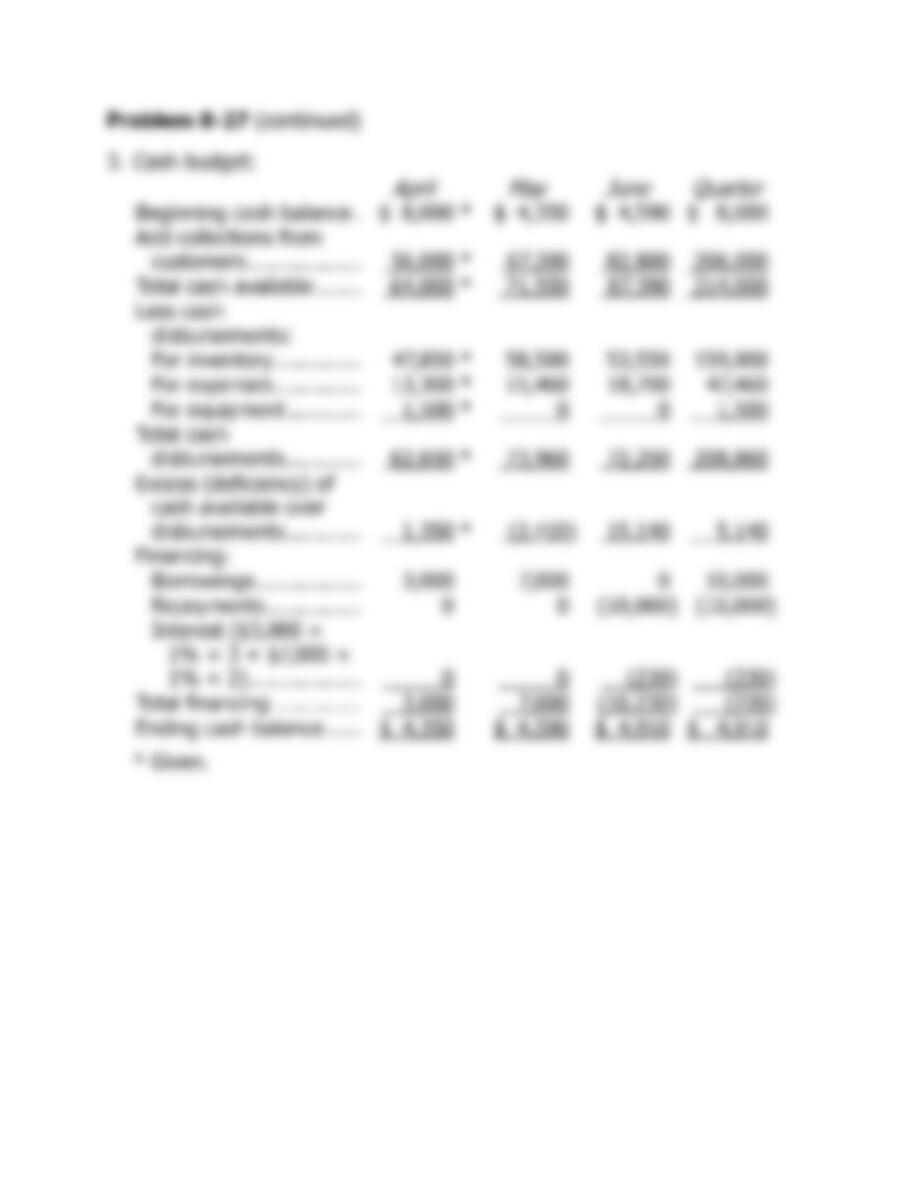

8-10 The principal purpose of the cash

budget is NOT to see how much cash the

company will have in the bank at the end of the

year. Although this is one of the purposes of the

cash budget, the principal purpose is to provide

information on probable cash needs

during

the

budget period, so that bank loans and other

sources of financing can be anticipated and

arranged well in advance.

The Foundational 15

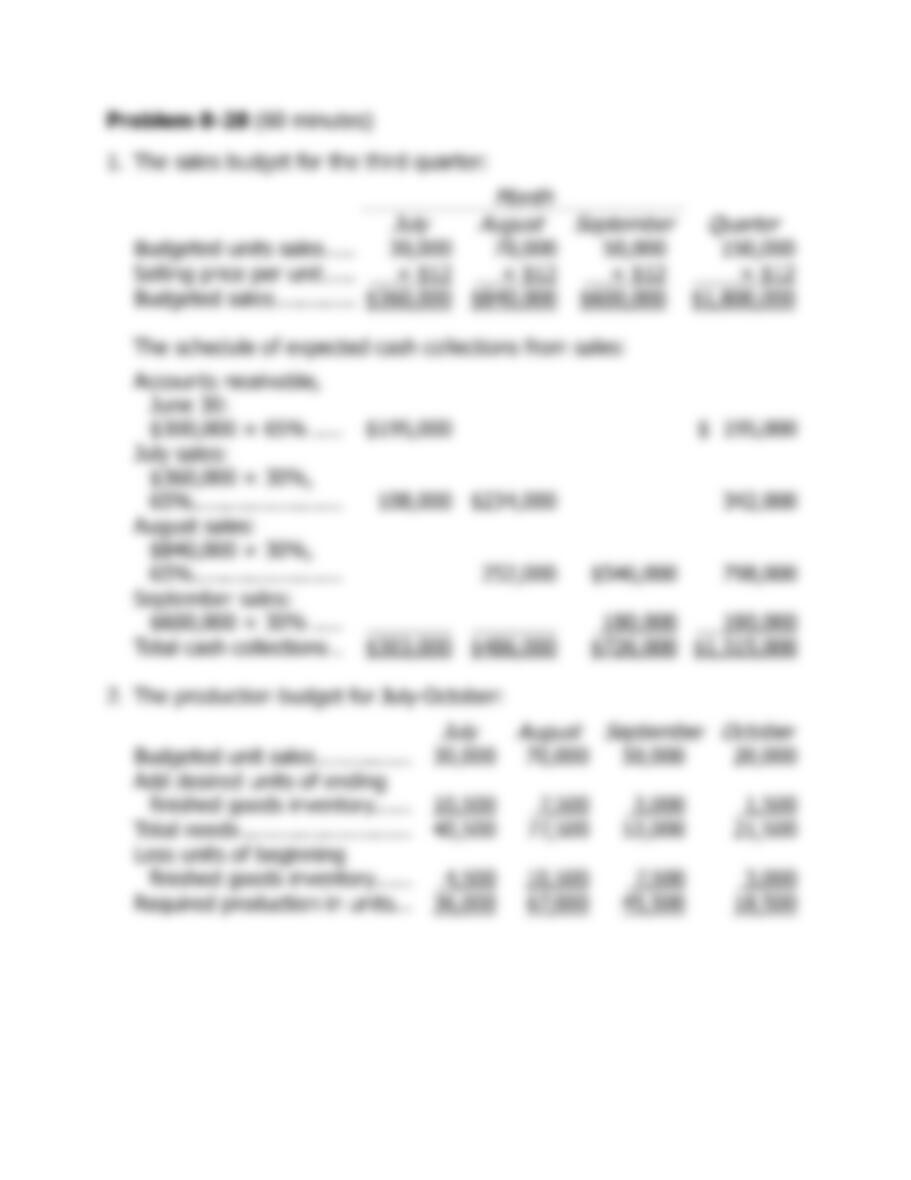

1. The budgeted sales for July are computed as follows:

Unit sales (a) ………………………..

10,000

Selling price per unit (b) ………….

$70

Total sales (a) × (b) ……………….

$700,000

2. The expected cash collections for July are computed as follows:

July

June sales:

$588,000 × 60% ……………….

$352,800

July sales:

$700,000 × 40% ……………….

280,000

Total cash collections …………….

$632,800

3. The accounts receivable balance at the end of July is:

July sales (a) ………………………..

$700,000

Percent uncollected (b) ……………

60%

Accounts receivable (a) × (b) ……

$420,000

4. The required production for July is computed as follows:

July

Budgeted sales in units ………………

10,000

Add desired ending inventory* …….

2,400

Total needs ……………………………..

12,400

Less beginning inventory** …………

2,000

Required production ………………….

10,400

*August sales of 12,000 units × 20% = 2,400 units.

**July sales of 10,000 units × 20% = 2,000 units.

The Foundational 15 (continued)

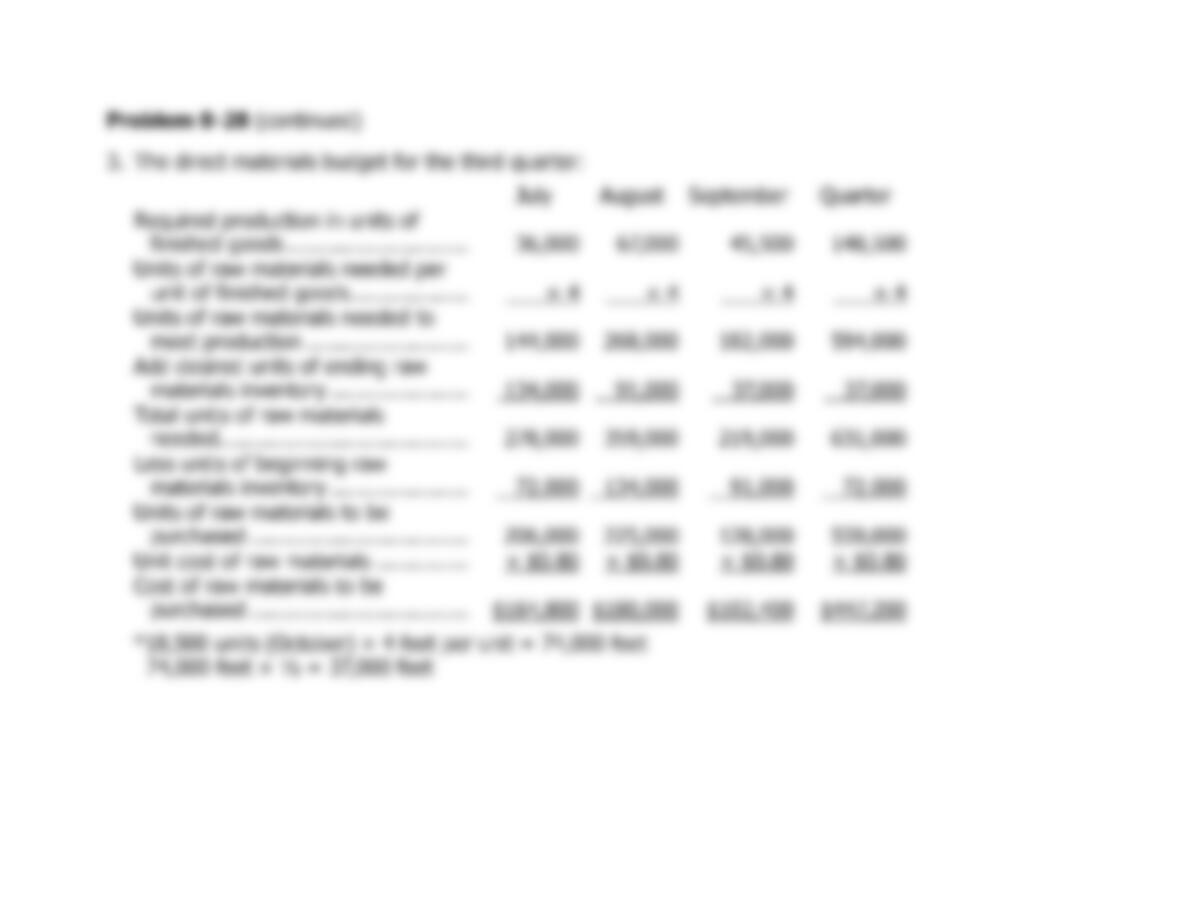

5. The raw material purchases for July are computed as follows:

July

Required production in units of finished goods ……………..

10,400

Units of raw materials needed per unit of finished goods ..

5

Units of raw materials needed to meet production …………

52,000

Add desired units of ending raw materials inventory* …….

6,100

Total units of raw materials needed …………………………...

58,100

Less units of beginning raw materials inventory** …………

5,200

Units of raw materials to be purchased ……………………….

52,900

*61,000 pounds × 10% = 6,100 pounds.

**52,000 pounds × 10% = 5,200 pounds.

6. The cost of raw material purchases for July is computed as follows:

Units of raw materials to be purchased (a)………

52,900

Unit cost of raw materials (b) ……………………….

$2.00

Cost of raw materials to be purchased (a) × (b) .

$105,800

7. The estimated cash disbursements for materials purchases in July is

computed as follows:

July

June purchases:

$88,880 × 70% ………………….

$62,216

July purchases:

$105,800 × 30% ………………..

31,740

Total cash disbursements ………..

$93,956

8. The accounts payable balance at the end of July is:

July purchases (a) ………………….

$105,800

Percent unpaid (b) …………………

70%

Accounts payable (a) × (b) ………

$74,060

The Foundational 15 (continued)

9. The estimated raw materials inventory balance at the end of July is

computed as follows:

Ending raw materials inventory (pounds) (a) ……

6,100

Cost per pound (b) …………………………..………..

$2.00

Raw material inventory balance (a) × (b) ……….

$12,200

10. The estimated direct labor cost for July is computed as follows:

July

Required production in units …………..

10,400

Direct labor hours per unit ……………..

× 2.0

Total direct labor-hours needed (a)…..

20,800

Direct labor cost per hour (b) ………….

$15

Total direct labor cost (a) × (b) ……….

$312,000

11. The estimated unit product cost is computed as follows:

Quantity

Cost

Total

Direct materials …………………..

5 pounds

$2 per pound

$10.00

Direct labor ………………………..

2 hours

$15 per hour

30.00

Manufacturing overhead ……….

2 hours

$10 per hour

20.00

Unit product cost …………………

$60.00

12. The estimated finished goods inventory balance at the end of July is

computed as follows:

Ending finished goods inventory in units (a) …….

2,400

Unit product cost (b) ………………………………….

$60.00

Ending finished goods inventory (a) × (b) ……….

$144,000

The Foundational 15 (continued)

13. The estimated cost of goods sold for July is computed as follows:

Unit sales (a) ……………………………………………

10,000

Unit product cost (b) ………………………………….

$60.00

Estimated cost of goods sold (a) × (b) …………..

$600,000

The estimated gross margin for July is computed as follows:

Total sales (a) …………………………………………..

$700,000

Cost of goods sold (b) ………………………………..

600,000

Estimated gross margin (a) – (b) …………………..

$100,000

14. The estimated selling and administrative expense for July is computed

as follows:

July

Budgeted unit sales ……………………………..

10,000

Variable selling and administrative …………..

expense per unit ……………………………….

× $1.80

Total variable expense ………………………….

$18,000

Fixed selling and administrative expenses …

60,000

Total selling and administrative expenses …

$78,000

15. The estimated net operating income for July is computed as follows:

Gross margin (a) ……………………………………….

$100,000

Selling and administrative expenses (b) ………….

78,000

Net operating income (a) – (b) ……………………..

$ 22,000

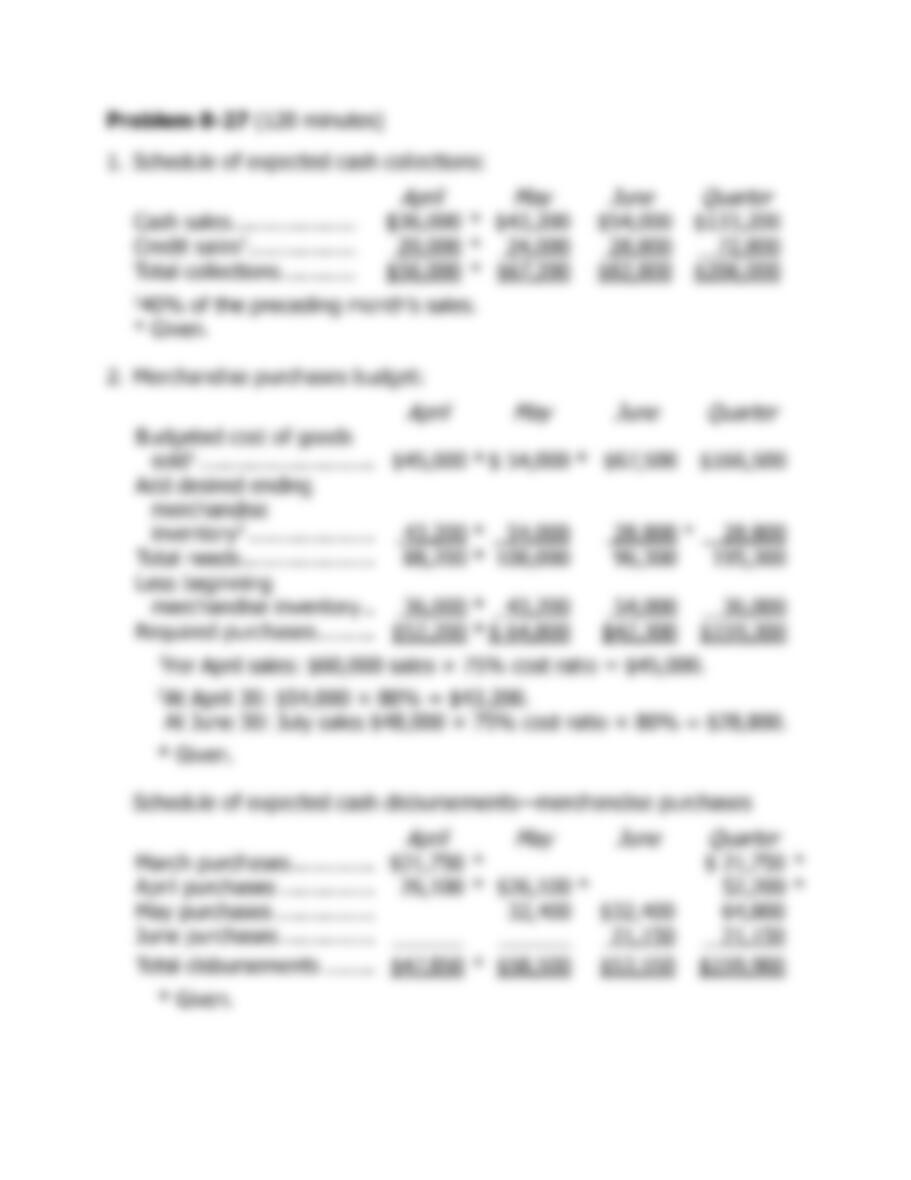

Exercise 8-1 (20 minutes)

1.

April

May

June

Total

February sales:

$230,000 × 10% …….

$ 23,000

$ 23,000

March sales: $260,000

× 70%, 10% ………….

182,000

$ 26,000

208,000

April sales: $300,000 ×

20%, 70%, 10% …….

60,000

210,000

$ 30,000

300,000

May sales: $500,000 ×

20%, 70% …………….

100,000

350,000

450,000

June sales: $200,000 ×

20% …………………….

40,000

40,000

Total cash collections ….

$265,000

$336,000

$420,000

$1,021,000

Notice that even though sales peak in May, cash collections peak in

June. This occurs because the bulk of the company’s customers pay in

the month following sale. The lag in collections that this creates is even

more pronounced in some companies. Indeed, it is not unusual for a

company to have the least cash available in the months when sales are

greatest.

2. Accounts receivable at June 30:

From May sales: $500,000 × 10% ……………………

$ 50,000

From June sales: $200,000 × (70% + 10%) ………

160,000

Total accounts receivable at June 30 …………………

$210,000

Exercise 8-2 (10 minutes)

April

May

June

Quarter

Budgeted unit sales ……………..

50,000

75,000

90,000

215,000

Add desired units of ending

finished goods inventory* ……

7,500

9,000

8,000

8,000

Total needs ………………………..

57,500

84,000

98,000

223,000

Less units of beginning finished

goods inventory ………………..

5,000

7,500

9,000

5,000

Required production in units …..

52,500

76,500

89,000

218,000

*10% of the following month’s sales in units.

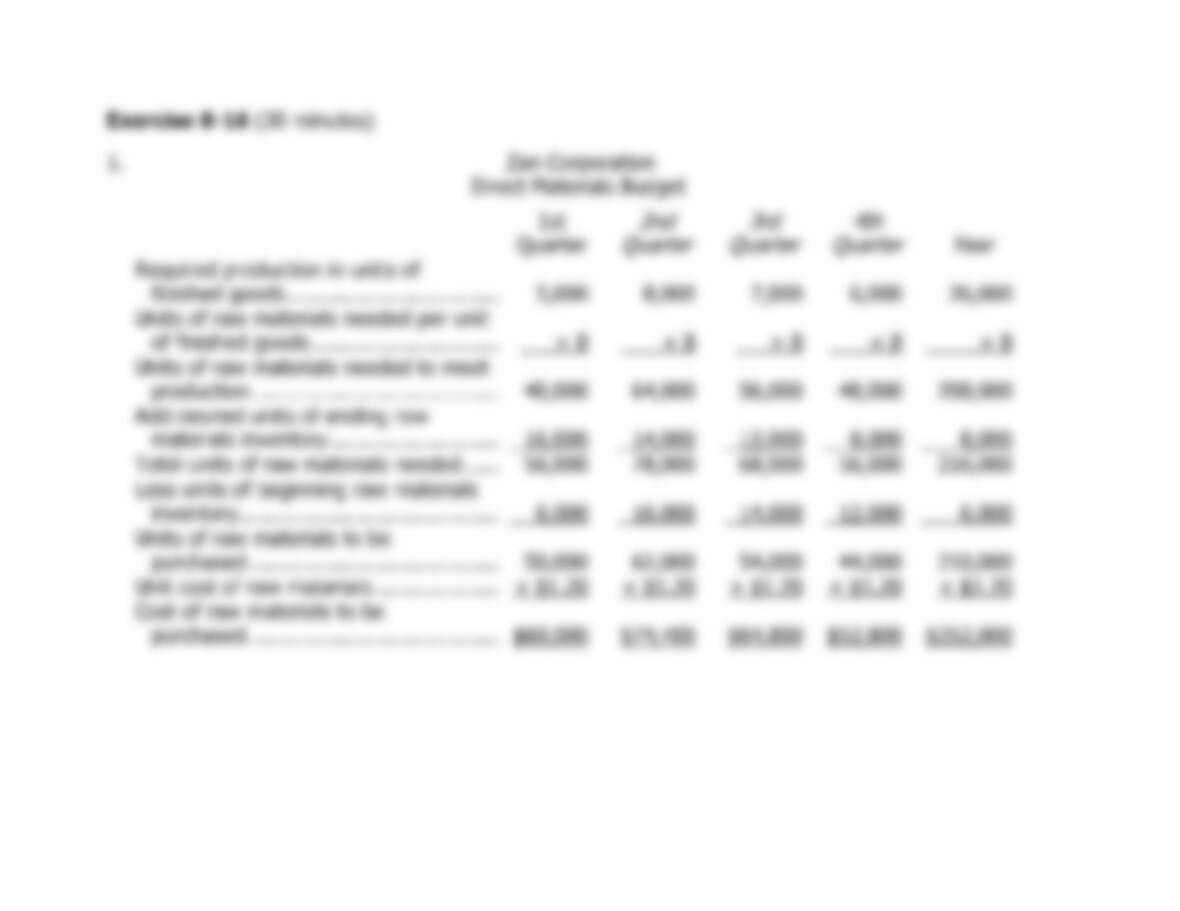

Exercise 8-3 (15 minutes)

Quarter—Year 2

First

Second

Third

Fourth

Year

Required production in units of finished

goods …………………………..………………….

60,000

90,000

150,000

100,000

400,000

Units of raw materials needed per unit of

finished goods …………………………………..

× 3

× 3

× 3

× 3

× 3

Units of raw materials needed to meet

production ………………………………………..

180,000

270,000

450,000

300,000

1,200,000

Add desired units of ending raw materials

inventory ………………………………………….

54,000

90,000

60,000

42,000

42,000

Total units of raw materials needed ………….

234,000

360,000

510,000

342,000

1,242,000

Less units of beginning raw materials

inventory ………………………………………….

36,000

54,000

90,000

60,000

36,000

Units of raw materials to be purchased ……..

198,000

306,000

420,000

282,000

1,206,000

Unit cost of raw materials ……………………….

× $1.50

× $1.50

× $1.50

× $1.50

× $1.50

Cost of raw materials to purchased …………..

$297,000

$459,000

$630,000

$423,000

$1,809,000

Exercise 8-4 (20 minutes)

1. Assuming that the direct labor workforce is adjusted each quarter, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ……………………….

8,000

6,500

7,000

7,500

29,000

Direct labor time per unit (hours) …………………

× 0.35

× 0.35

× 0.35

× 0.35

× 0.35

Total direct labor-hours needed……………………

2,800

2,275

2,450

2,625

10,150

Direct labor cost per hour …………………………..

× $12.00

× $12.00

× $12.00

× $12.00

× $12.00

Total direct labor cost ………………………………..

$ 33,600

$ 27,300

$ 29,400

$ 31,500

$121,800

2. Assuming that the direct labor workforce is not adjusted each quarter and that overtime wages are

paid, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ………………………

8,000

6,500

7,000

7,500

Direct labor time per unit (hours) ………………..

× 0.35

× 0.35

× 0.35

× 0.35

Total direct labor-hours needed ………………….

2,800

2,275

2,450

2,625

Regular hours paid …………………………………..

2,600

2,600

2,600

2,600

Overtime hours paid …………………………………

200

0

0

25

Wages for regular hours (@ $12.00 per hour) ..

$31,200

$31,200

$31,200

$31,200

$124,800

Overtime wages (@ 1.5 × $12.00 per hour) ….

3,600

0

0

450

4,050

Total direct labor cost ……………………………….

$34,800

$31,200

$31,200

$31,650

$128,850

Exercise 8-5 (15 minutes)

1.

Yuvwell Corporation

Manufacturing Overhead Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted direct labor-hours …………………………..

8,000

8,200

8,500

7,800

32,500

Variable manufacturing overhead rate ……………..

× $3.25

× $3.25

× $3.25

× $3.25

× $3.25

Variable manufacturing overhead ……………………

$26,000

$26,650

$27,625

$25,350

$105,625

Fixed manufacturing overhead ……………………….

48,000

48,000

48,000

48,000

192,000

Total manufacturing overhead ……………………….

74,000

74,650

75,625

73,350

297,625

Less depreciation …………………………..……………

16,000

16,000

16,000

16,000

64,000

Cash disbursements for manufacturing overhead .

$58,000

$58,650

$59,625

$57,350

$233,625

2.

Total budgeted manufacturing overhead for the year (a) …

$297,625

Budgeted direct labor-hours for the year (b) …………………

32,500

Predetermined overhead rate for the year (a) ÷ (b) ……….

$9.16

Exercise 8-6 (15 minutes)

Weller Company

Selling and Administrative Expense Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted unit sales …………………………………….

15,000

16,000

14,000

13,000

58,000

Variable selling and administrative expense per

unit ……………………………………………………….

× $2.50

× $2.50

× $2.50

× $2.50

× $2.50

Variable selling and administrative expense ………

$ 37,500

$ 40,000

$ 35,000

$ 32,500

$145,000

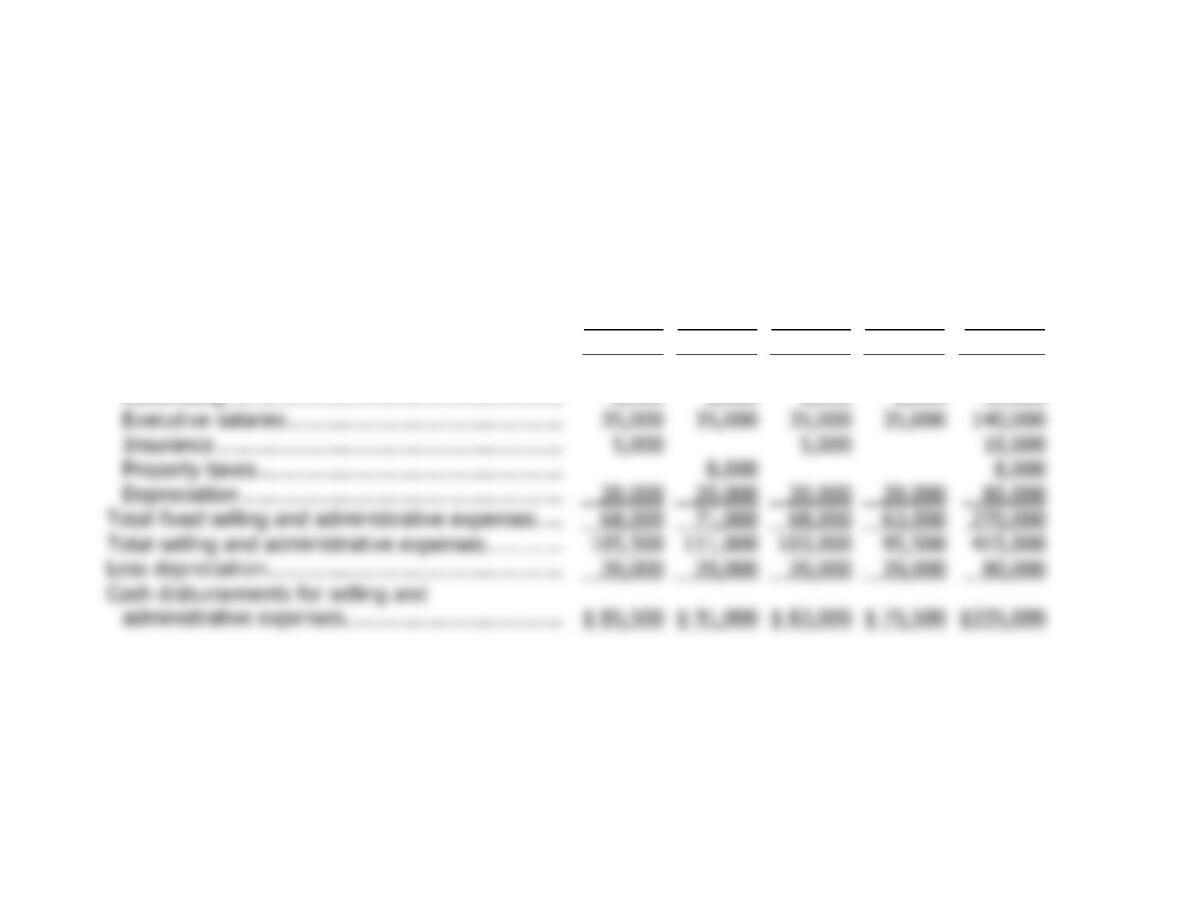

Fixed selling and administrative expenses:

Executive salaries ……………………………………..

Insurance ……………………………………………….

Property taxes ………………………………………….

Total fixed selling and administrative expenses ….

105,500

111,000

103,000

$ 85,500

$ 91,000

$ 83,000

$ 75,500

$335,000