Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

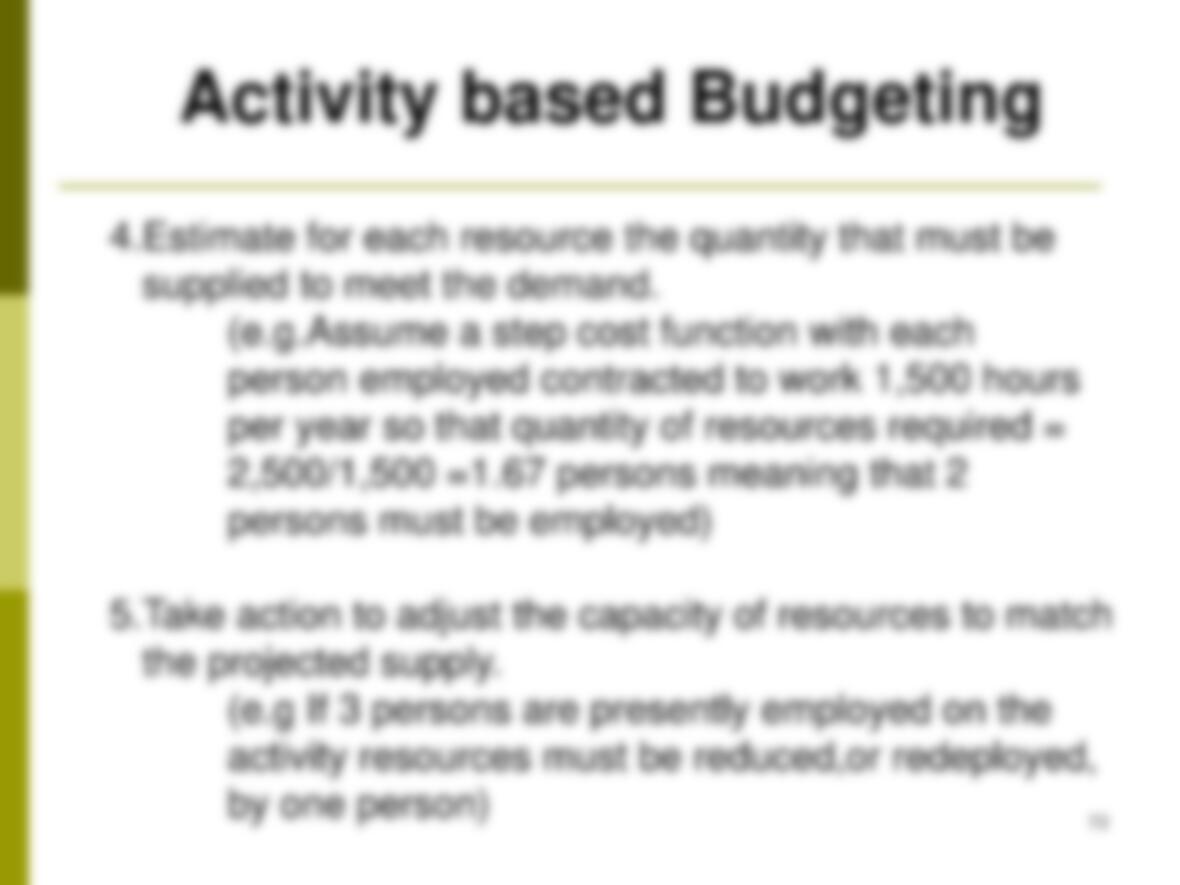

Activity-based Costing (ABC),

Activity-based Management (ABM)

& Activity-based Budgeting (ABB)

Chapter 4

Traditional Costing Approach

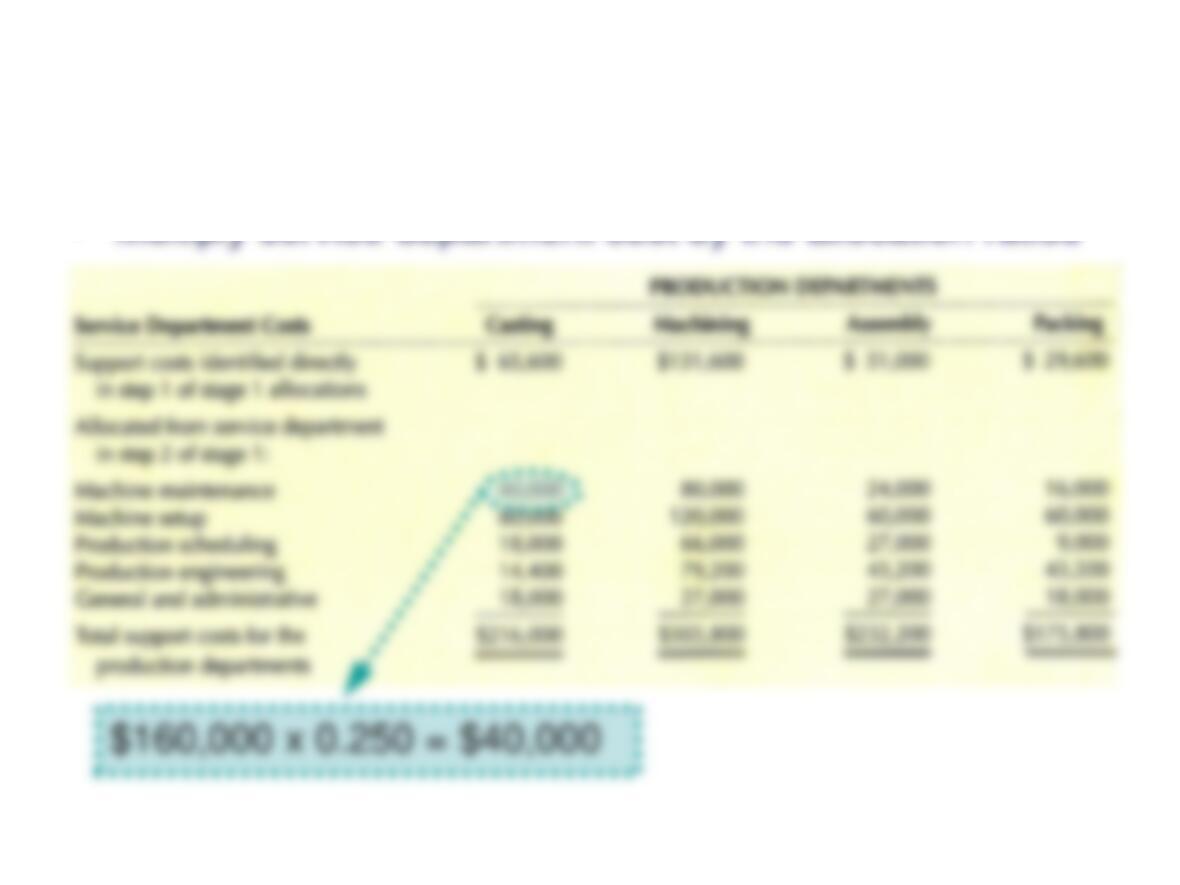

Service Department

Cost Allocations

Operating Expense Allocations

•Traditional cost accounting systems

assign operating expenses to products

with a two-stage procedure:

1. Expenses are assigned to production

departments

2. Production department expenses are

assigned to the products

•Departmental structure influences the

first-stage allocation process

Effect Of Departmental Structure

•Departments that have direct responsibility

for converting raw materials into finished

products are called production

departments

•Service departments perform activities

that support production, such as:

•Machine setup

•Production engineering

•Production scheduling

–All service department costs are indirect support

activity costs because they do not arise from direct

production activities

•Machine maintenance

Two-Stage Cost Allocation

Conventional product costing systems assign

indirect costs to jobs or products in two stages

1. In the first stage:

–System identifies indirect costs with various

production and service departments

–Service department costs are then allocated to

production departments

2. The system assigns the accumulated indirect

costs for the production departments to

individual jobs or products based on

predetermined departmental cost driver rates

Two-Stage Cost Allocation(2 of 2)

Allocating Service Department

Costs To Production Departments

•There are three ways that companies

allocate service department costs to

production departments:

–Direct allocation

–Sequential allocation

–Reciprocal allocation

•The last two are used when service

departments consume services provided by

other departments

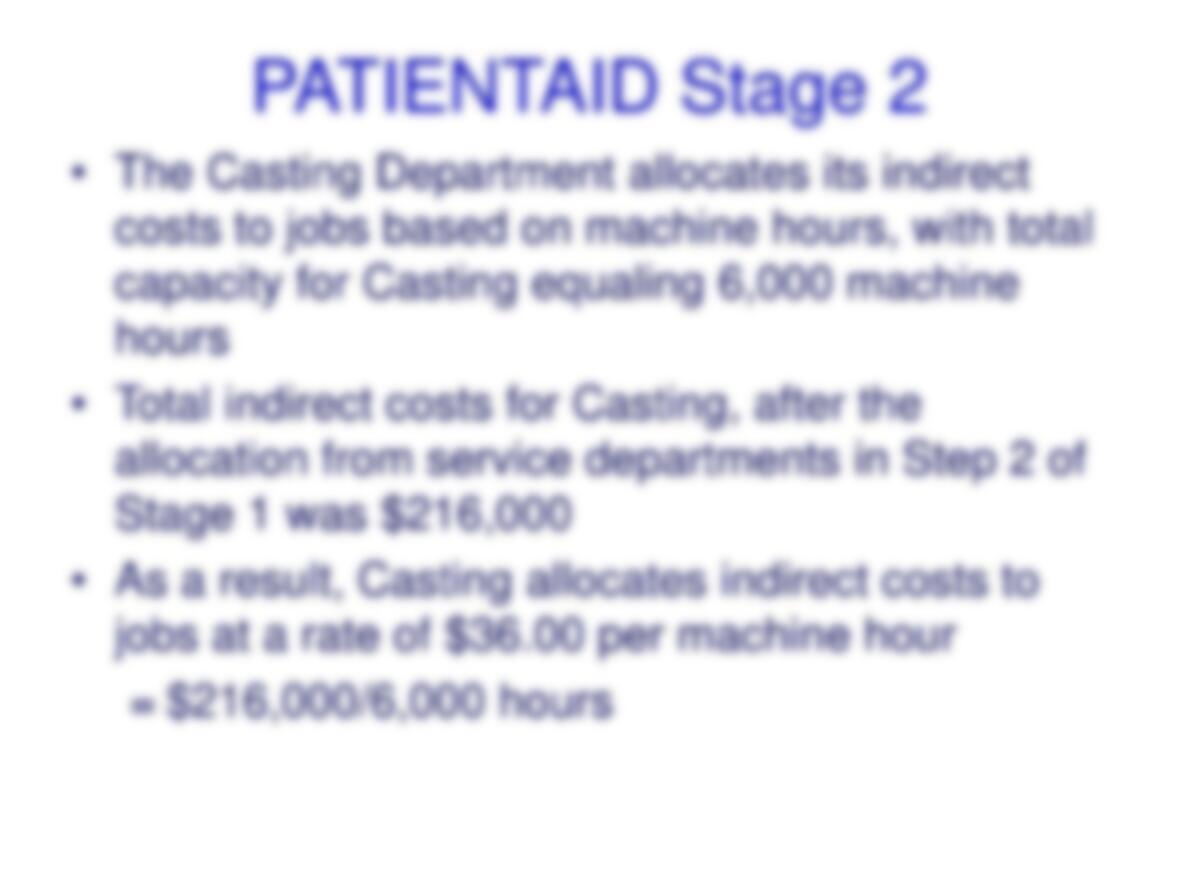

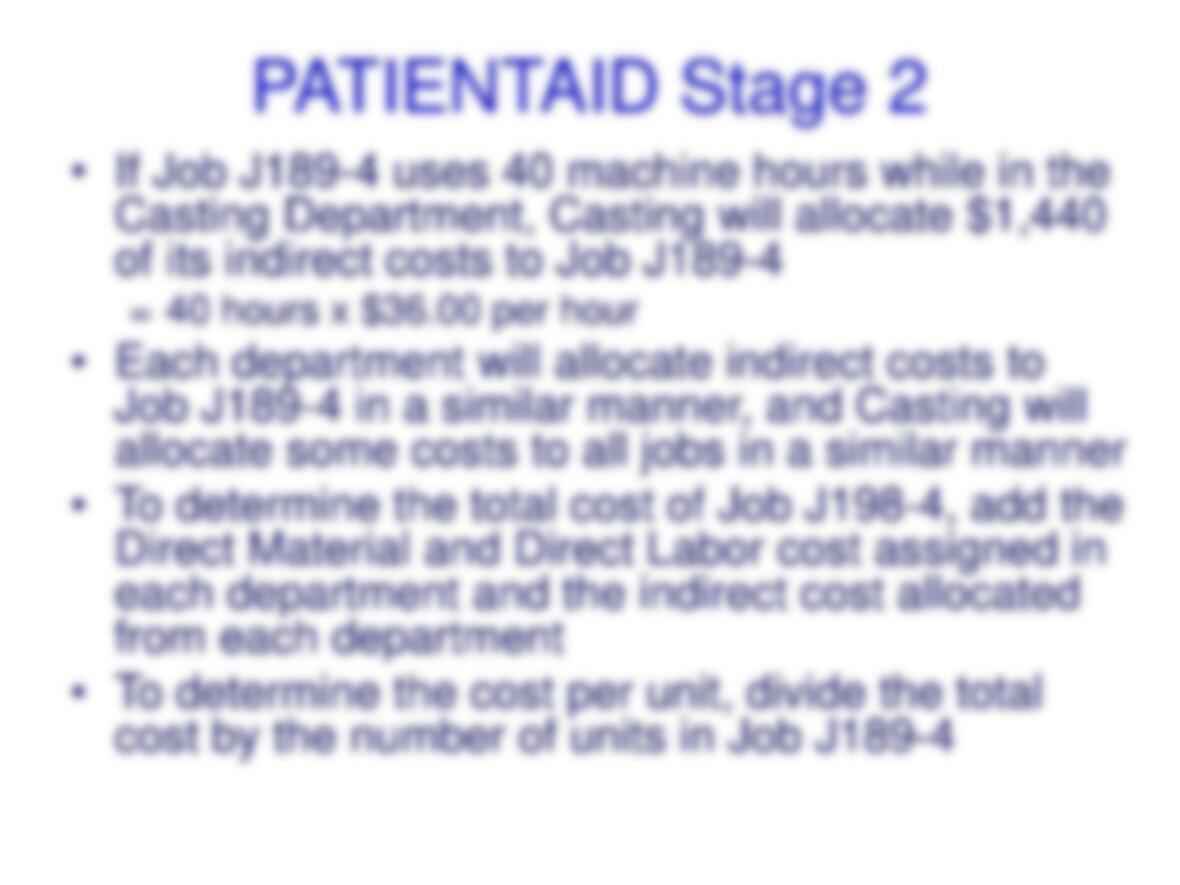

PATIENTAID EXAMPLE

Step 1 of Stage 1 cost allocations (given)

Direct Allocation Method

•The direct allocation method is a simple

method that allocates the service

department costs directly to the production

departments

–Allocations to production departments are

based on each production department’s

relative use of the applicable cost driver

–Possibility that some of the activities of a

service department may benefit other service

departments as well as production

departments is ignored

Allocation Bases Values

Allocation Ratios

300,000 / 1,200,000 = 0.250

Based on relative allocation basis value

Allocation of

Service Department Costs