CHAPTER 6

CHAPTER 6

ADJUSTMENTS FOR

ADJUSTMENTS FOR

ACCRUALS

ACCRUALS

AND

AND

PREPAYMENTS

PREPAYMENTS

LEARNING OBJECTIVES

LEARNING OBJECTIVES

To make adjustments for accrued &

To make adjustments for accrued &

prepaid expenses

prepaid expenses

To make adjustments for revenues owing

To make adjustments for revenues owing

& revenues received in advance

& revenues received in advance

To ascertain the actual amount of

To ascertain the actual amount of

expense & revenues in the Profit & Loss

expense & revenues in the Profit & Loss

Account

Account

To show the recording of accruals &

To show the recording of accruals &

prepayments in the Balance Sheet

prepayments in the Balance Sheet

INTRODUCTION

INTRODUCTION

In the trial balance, as far as expenses are

In the trial balance, as far as expenses are

concerned, it records only the expenses paid for

concerned, it records only the expenses paid for

the period.

the period.

So do the revenues where it records only the

So do the revenues where it records only the

revenues received during the period.

revenues received during the period.

Therefore, adjusting entries are made at the end of

Therefore, adjusting entries are made at the end of

the accounting period to ensure that revenues are

the accounting period to ensure that revenues are

recorded in the period in which they are earned, &

recorded in the period in which they are earned, &

expenses are recognized in the period which they

expenses are recognized in the period which they

are incurred.

are incurred.

This is to get the correct figure for net profit during

This is to get the correct figure for net profit during

the period.

the period.

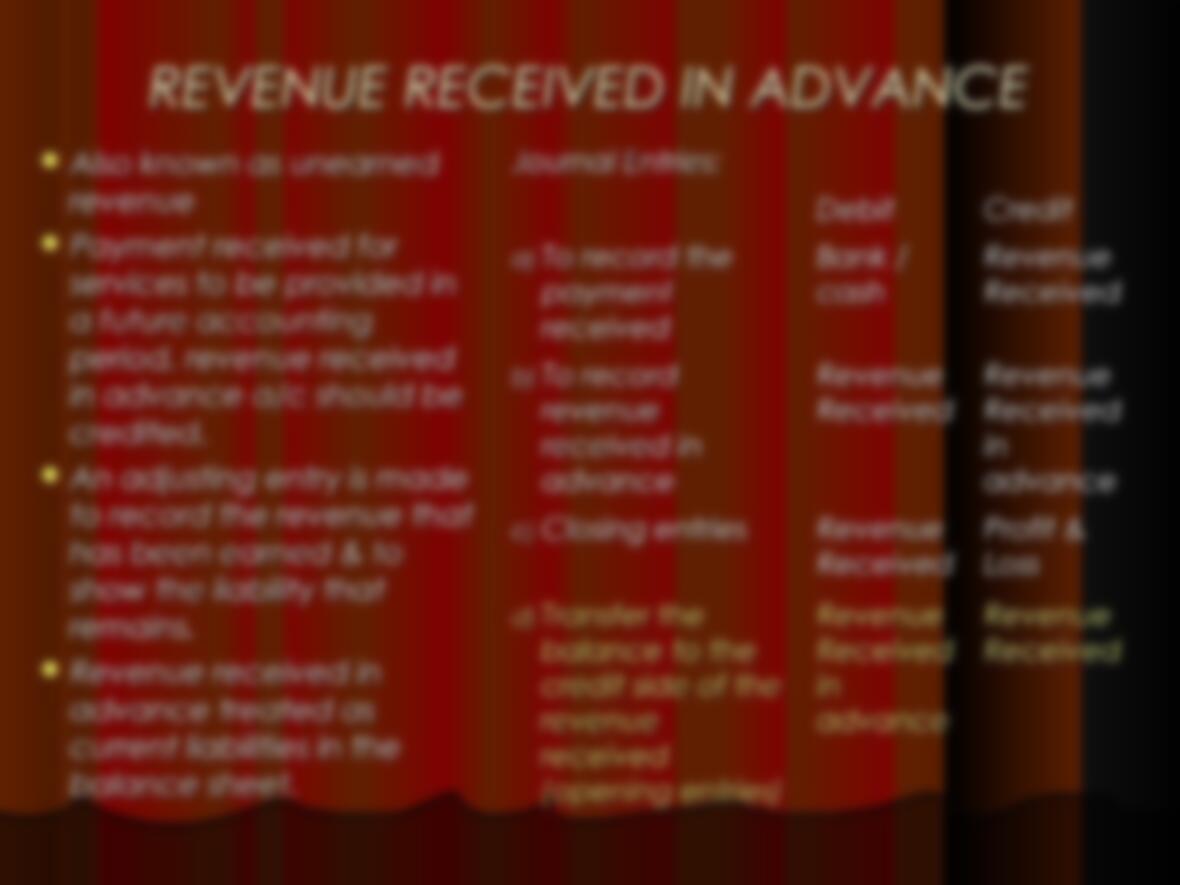

TYPES OF ADJUSTING ENTRIES FOR NOMINAL

TYPES OF ADJUSTING ENTRIES FOR NOMINAL

ACCOUNTS

ACCOUNTS

Revenues & expenses

Revenues & expenses

accounts are considered as

accounts are considered as

nominal accounts. Adjusting

nominal accounts. Adjusting

entries for nominal accounts

entries for nominal accounts

can be classified into the

can be classified into the

following categories:

following categories:

Expenses

Expenses Revenues

Revenues

Prepaid

Prepaid

expenses or

expenses or

expenses paid

expenses paid

in advance

in advance

Revenues

Revenues

received in

received in

advance or

advance or

unearned

unearned

revenues

revenues

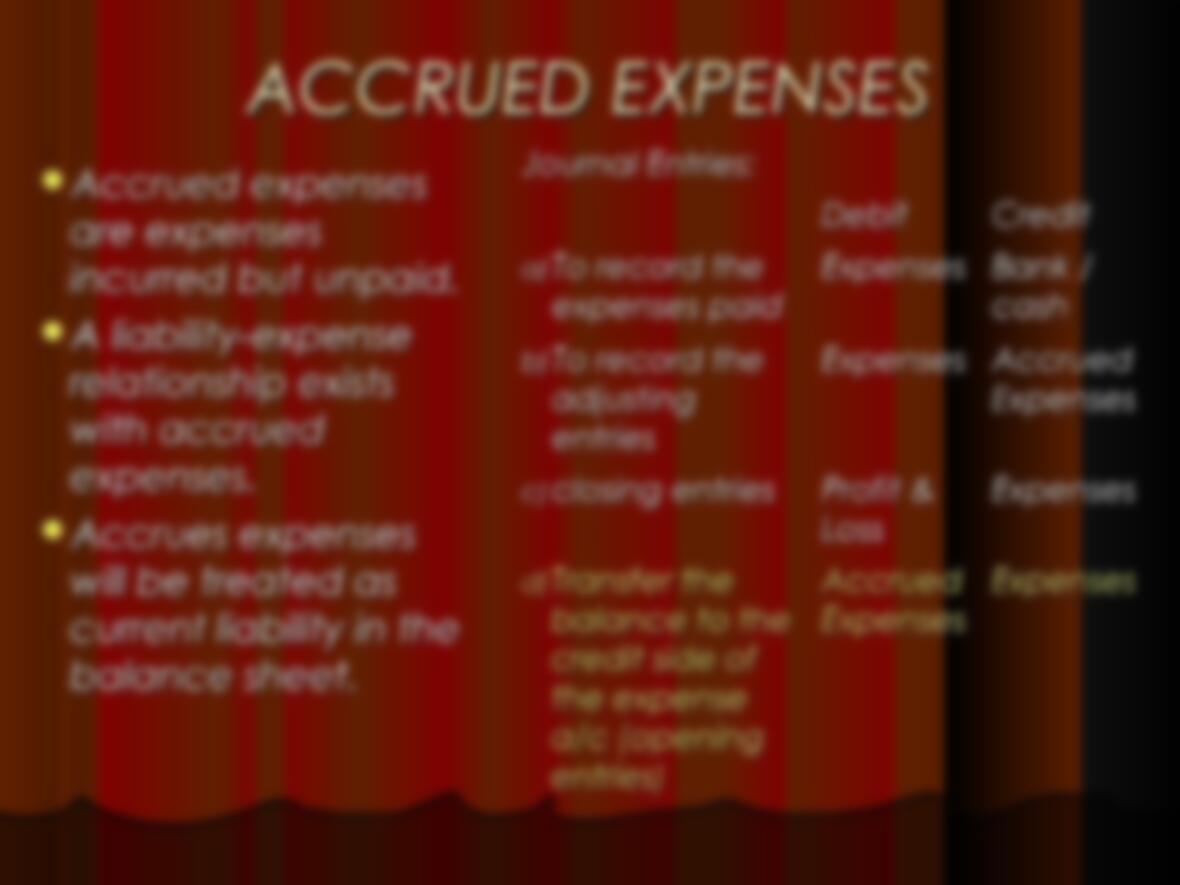

Accrued

Accrued

expenses or

expenses or

expenses owing

expenses owing

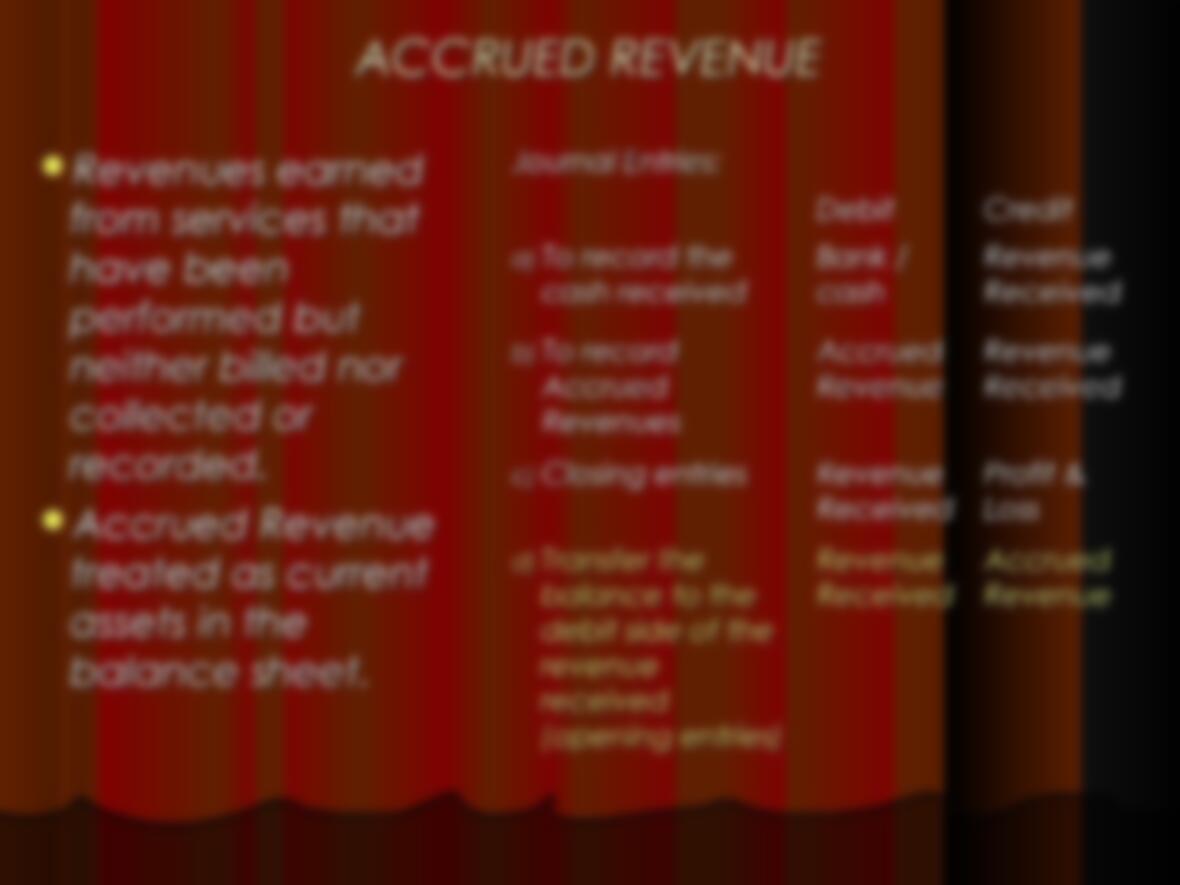

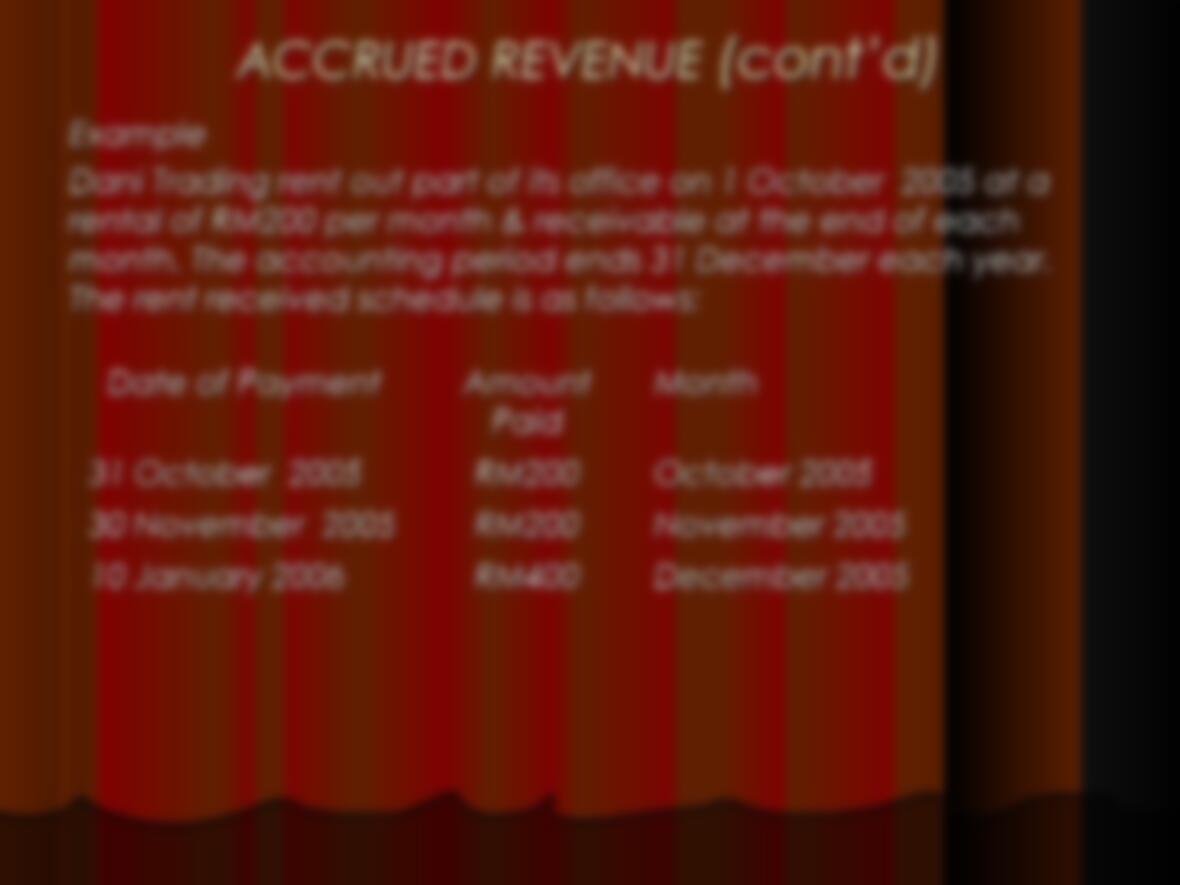

Accrued

Accrued

revenues or

revenues or

revenues

revenues

owing

owing

– Before making adjustments,

– Before making adjustments,

one must observed the

one must observed the

following:

following:

•

The accounting period

The accounting period

•

Any balances b/d at the

Any balances b/d at the

beginning of the year

beginning of the year

•Any balances b/d at the

Any balances b/d at the

end of the year

end of the year

•Amount actually paid

Amount actually paid

during the year

during the year

•Amount actually charged

Amount actually charged

to the TPL accounts during

to the TPL accounts during

the year

the year

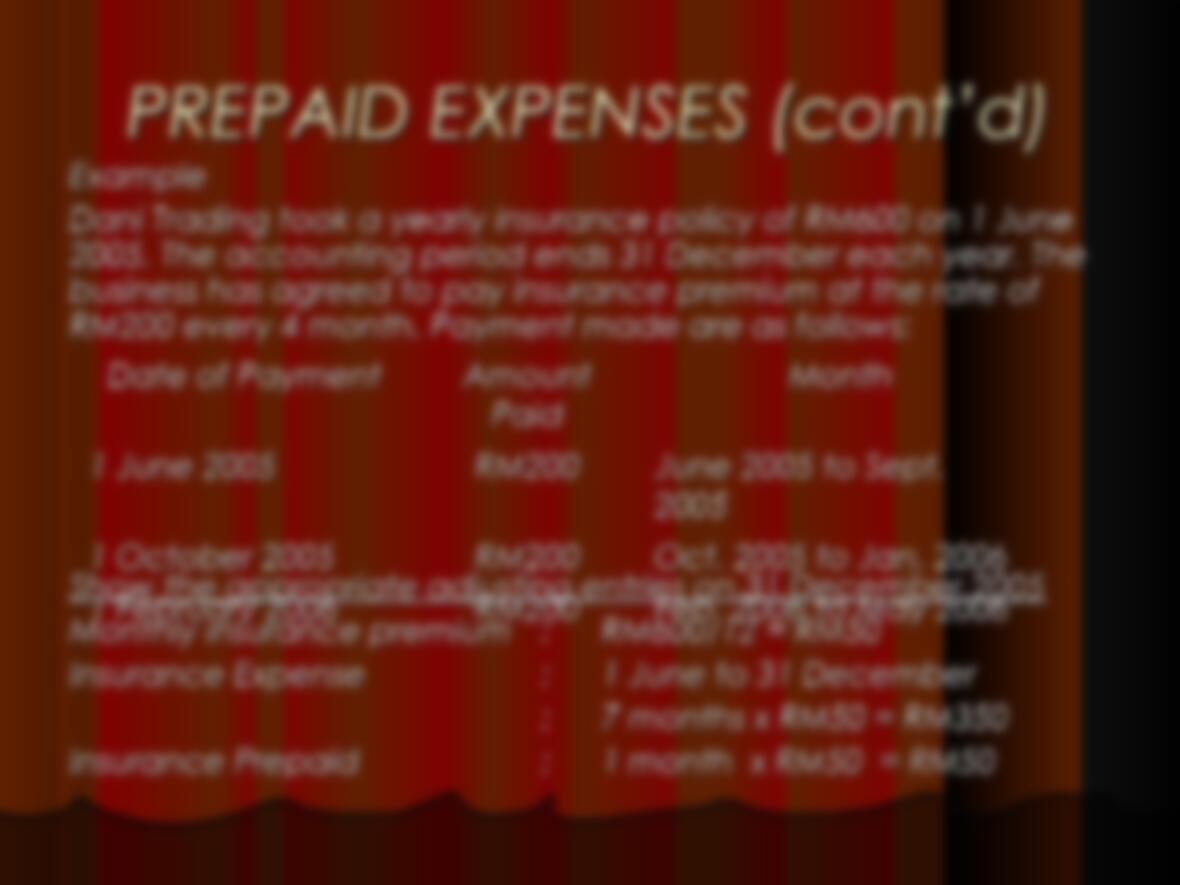

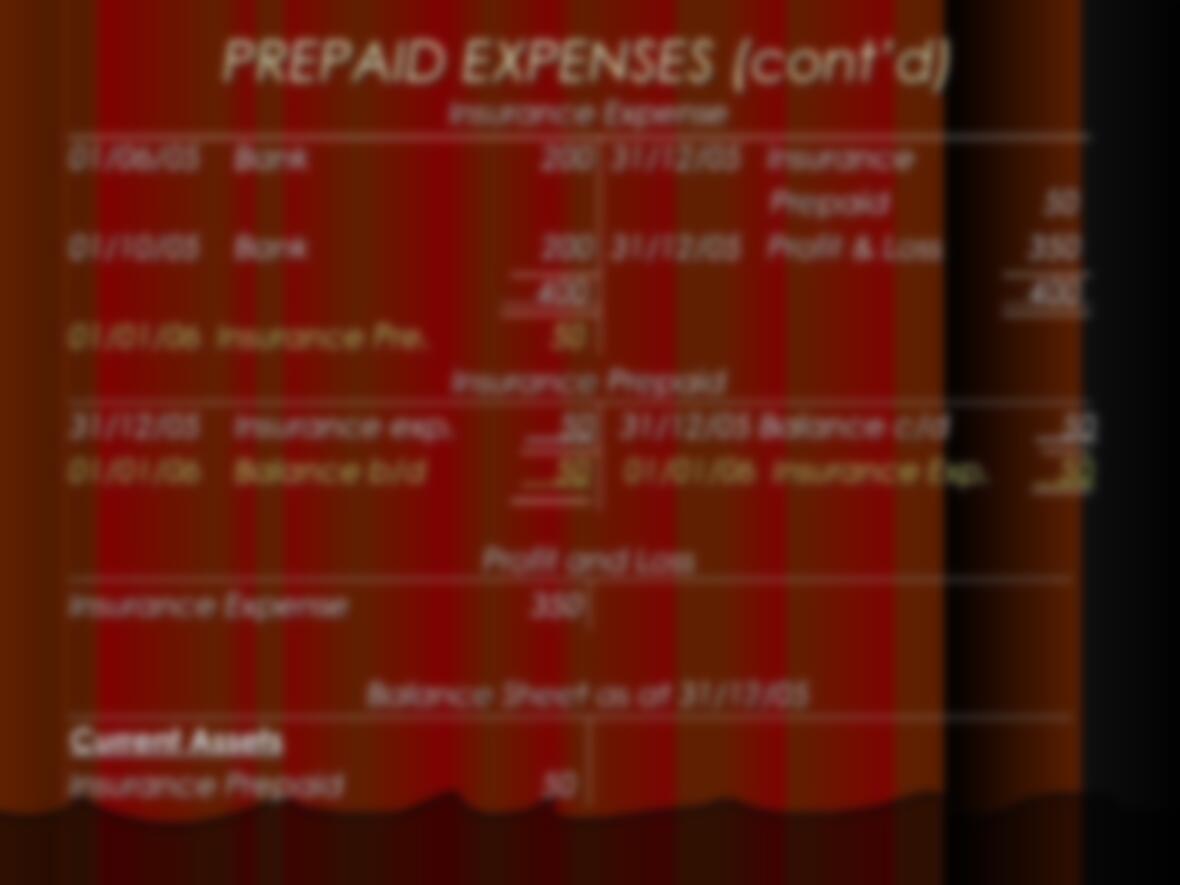

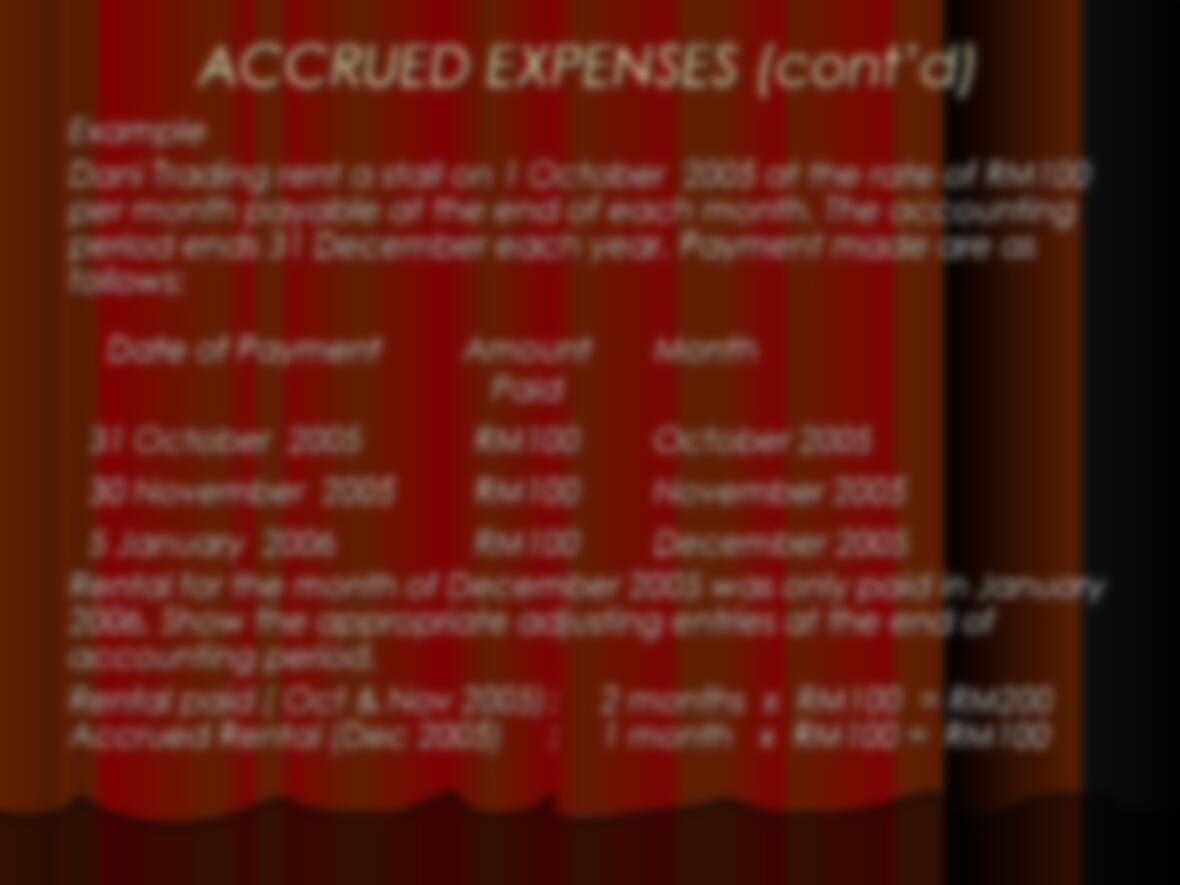

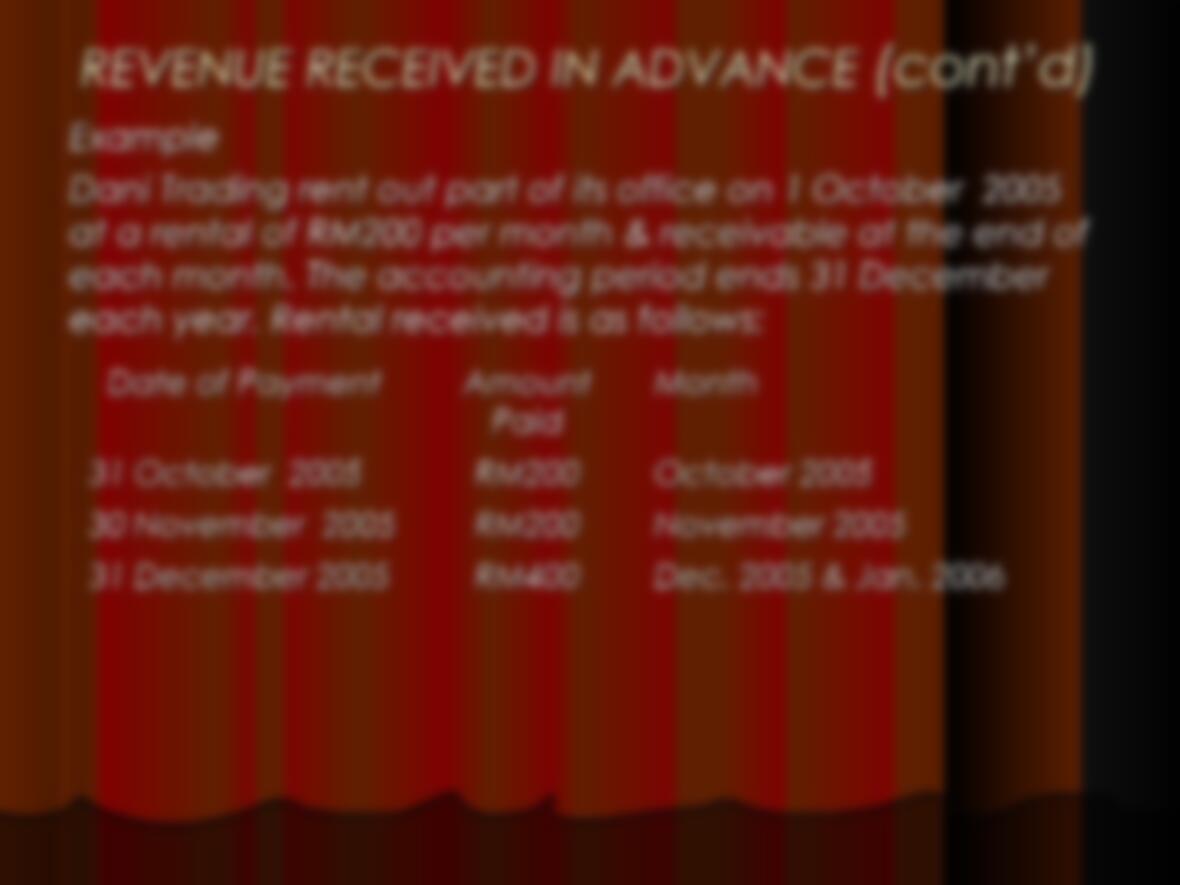

PREPAID EXPENSES

PREPAID EXPENSES

Prepaid expenses are

Prepaid expenses are

payment of expenses

payment of expenses

that will benefit more

that will benefit more

than one accounting

than one accounting

period.

period.

Prepaid expenses often

Prepaid expenses often

occur with regard to

occur with regard to

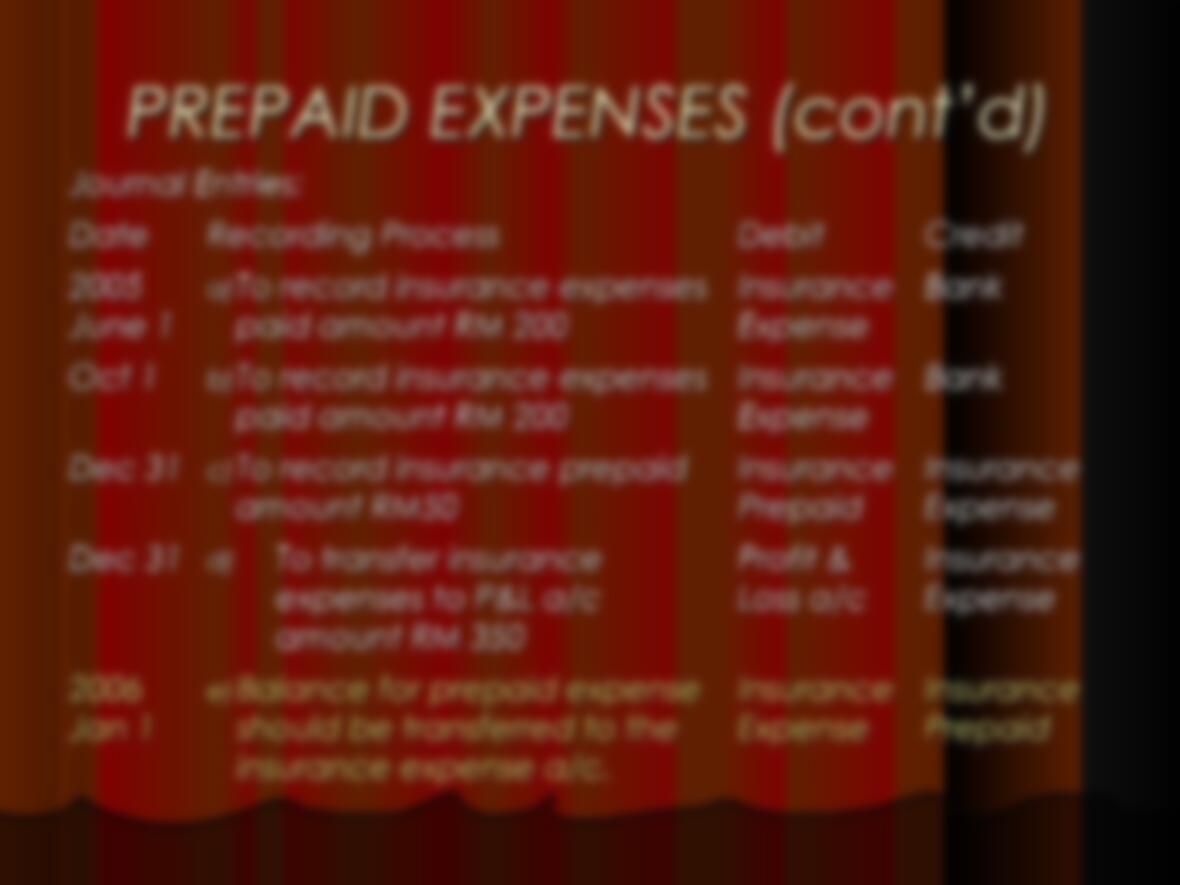

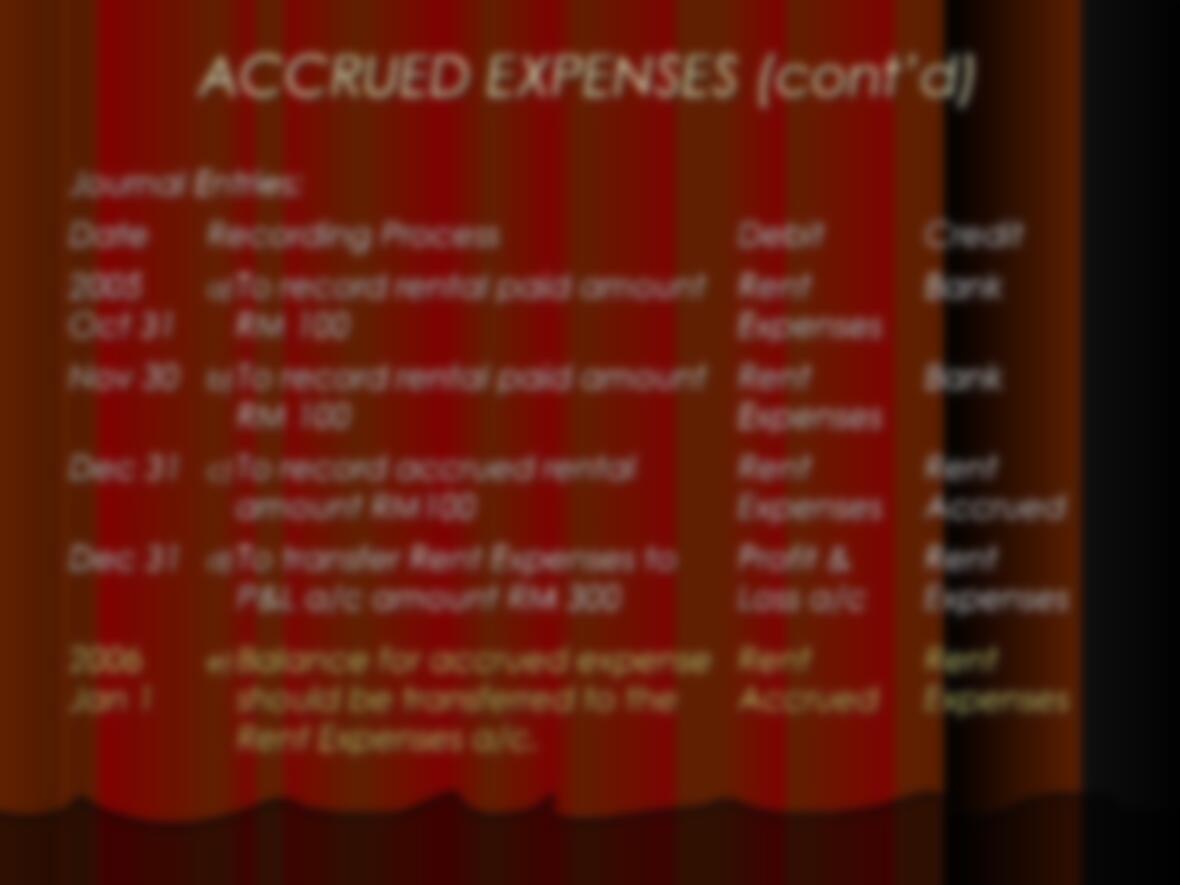

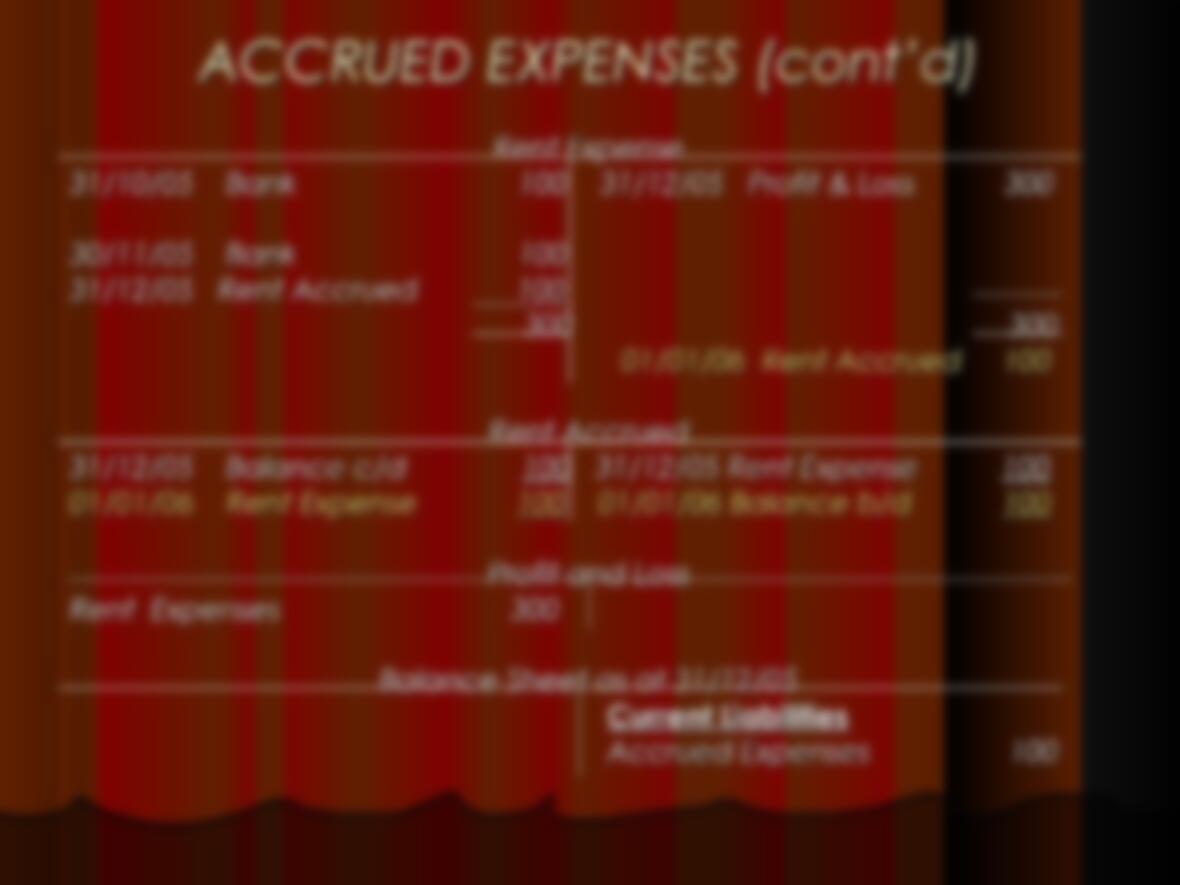

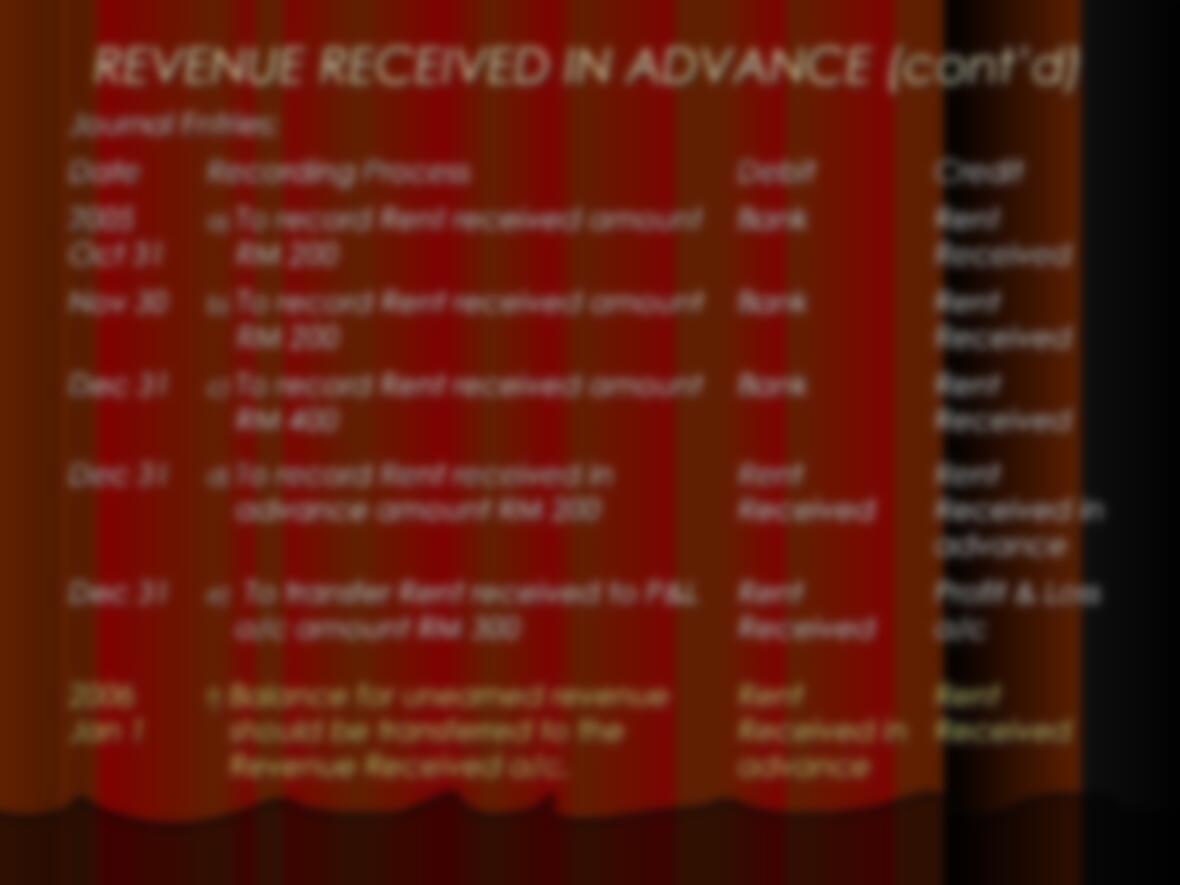

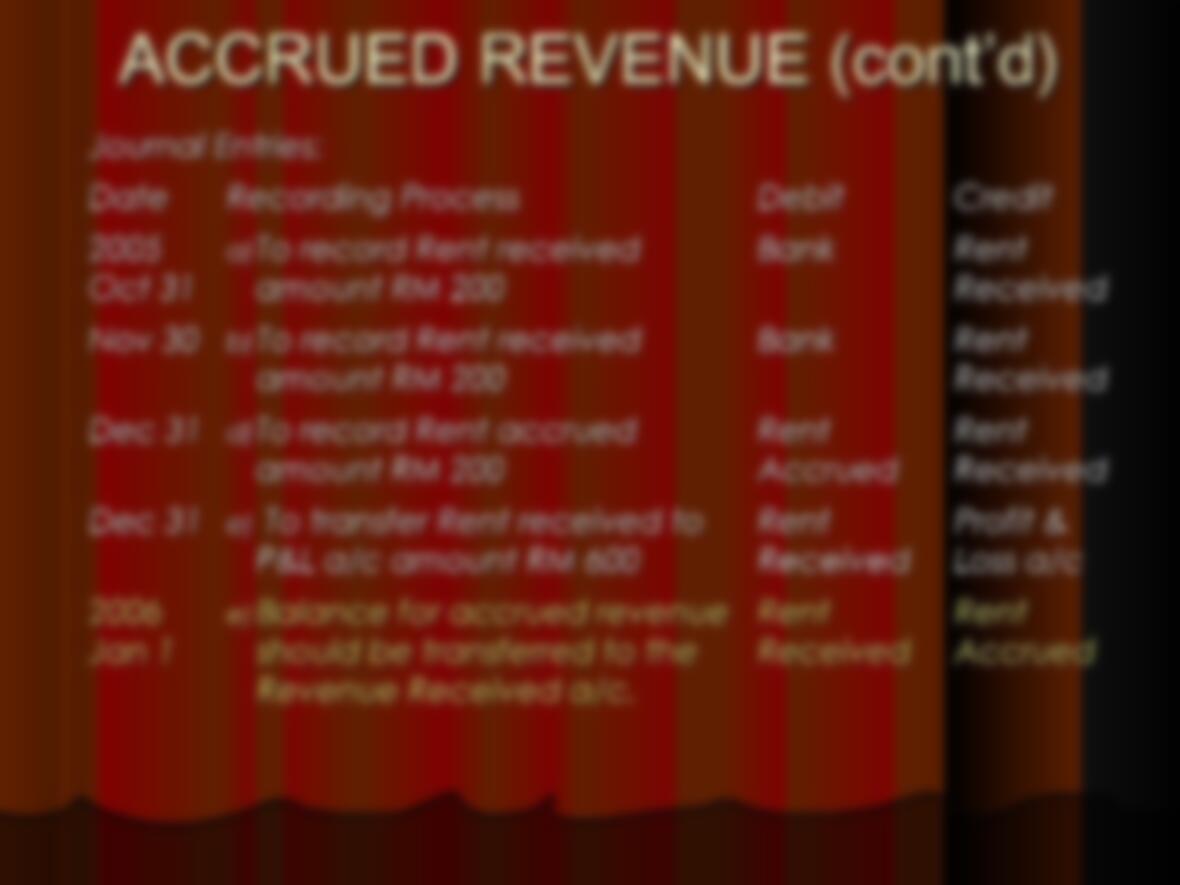

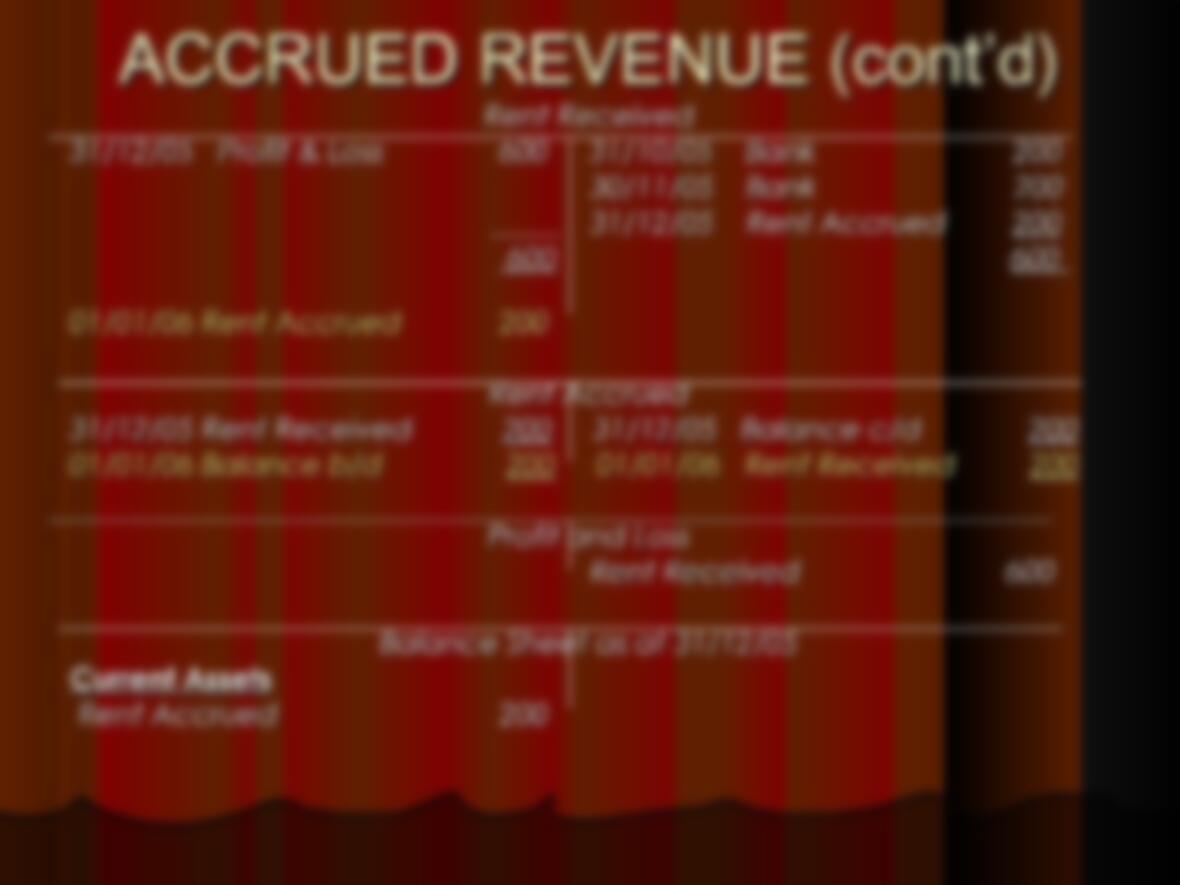

Journal Entries:

Journal Entries:

Debit

Debit Credit

Credit

a)

a) To record the

To record the

expenses paid

expenses paid

Expenses

Expenses Bank /

Bank /

cash

cash

b)

b) To record the

To record the

adjusting entries

adjusting entries

Expenses

Expenses

Prepaid

Prepaid

Expenses

Expenses

c)

c) To transfer the

To transfer the

expenses incurred

Profit &

Profit &

Loss

Expenses

Expenses