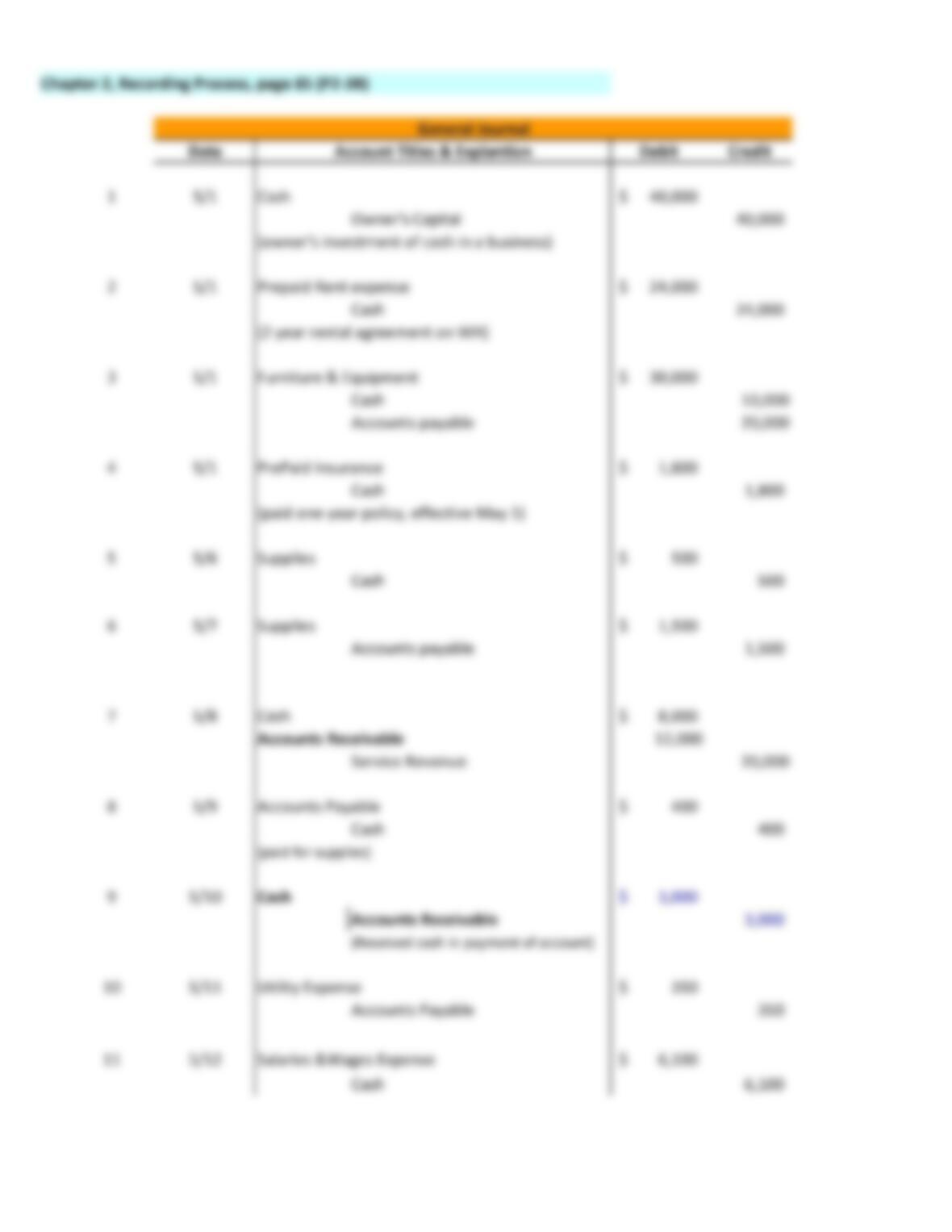

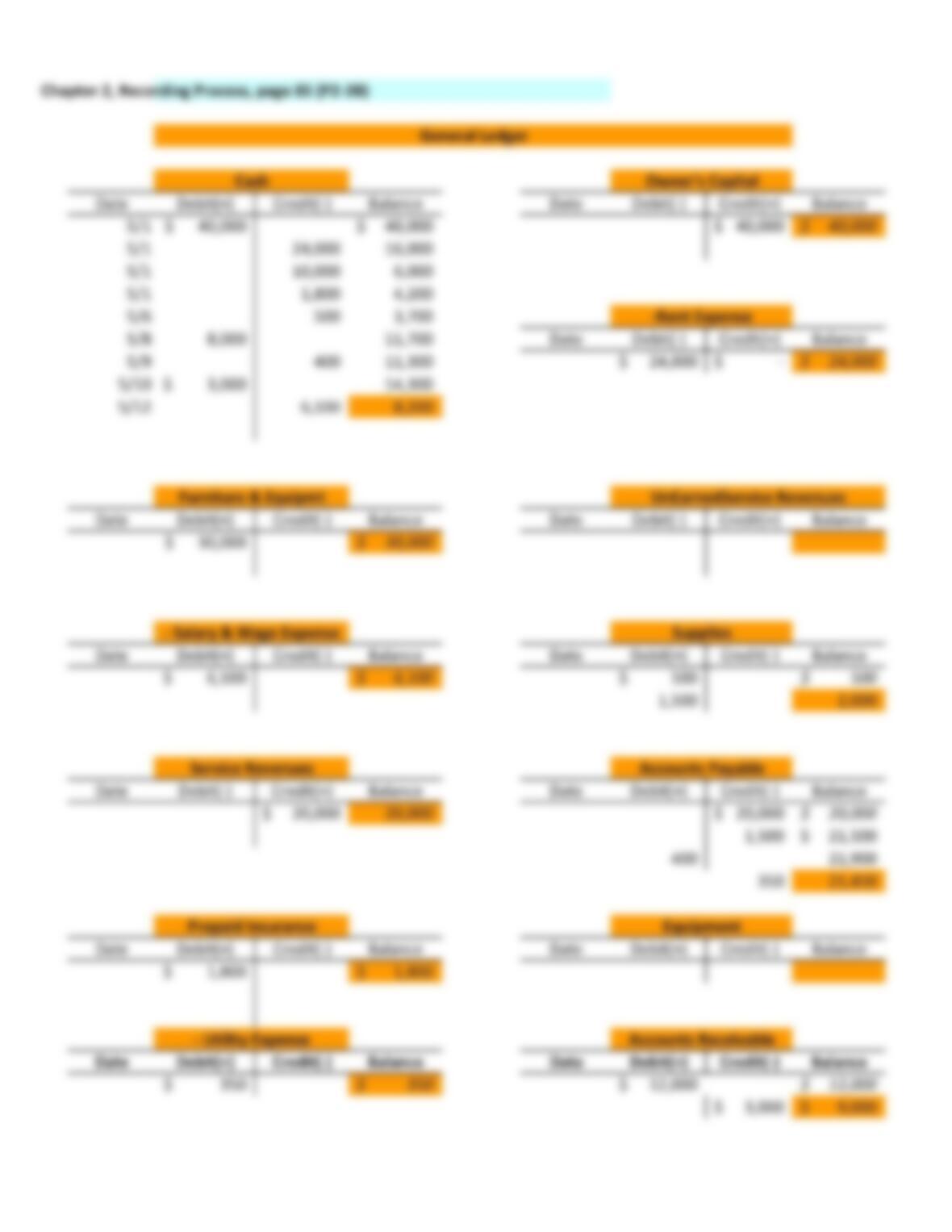

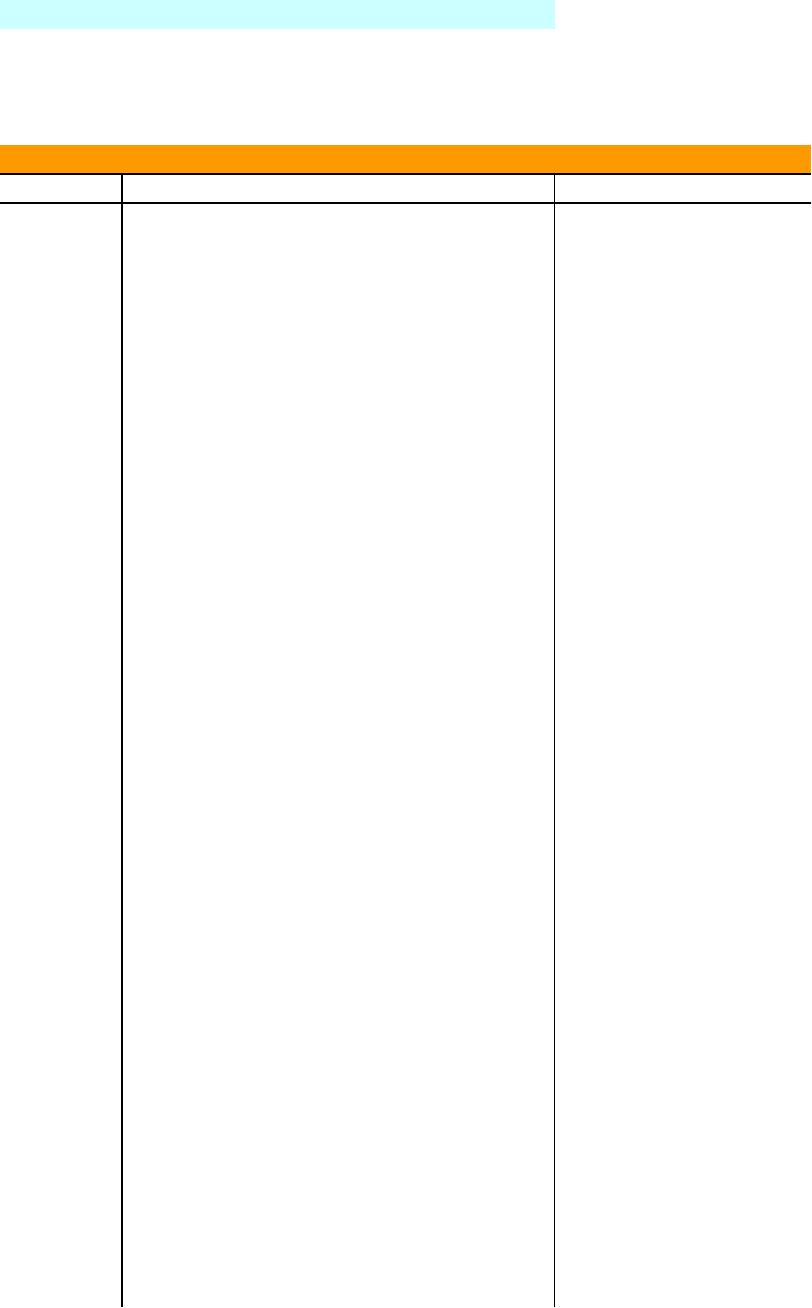

Chapter 2, Recording Process, pages 59 – 60

General Journal

transactions (activities) are recorded, entered General Journal

Date Debit Credit

1/1/2013 Cash 20,000$

Owner’s Capital 20,000

(owner’s investment of cash in a business)

1/2 Equipment 4,800$

Accounts Payable 4,800

(purchase of equipment on account)

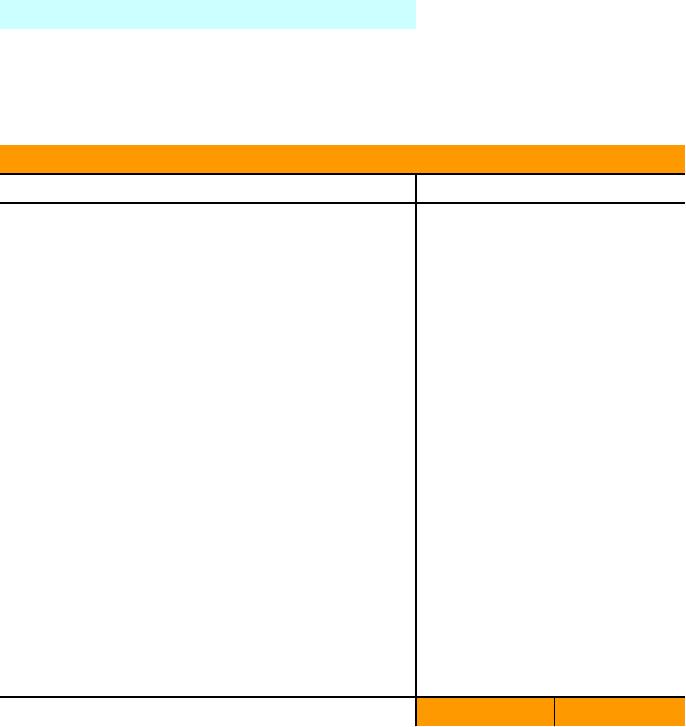

Chapter 2, Recording Process, pages 73 – 74

Snow Company

Trial Balance, December 31, 2012

Account Title Debit Credit

Cash 7,000$

Accounts Receivable 4,000

PrePaid Insurance 6,000

Equipment 88,000

Notes Payable 19,000

Accounts Payable 22,000

Salaries & Wages Payable 2,000

Owner’s Capital 20,000

Owner’s Drawings 8,000

Service Revenue 95,000

Salaries & Wages Expense 42,000

Insurance Expense 3,000

158,000$ 158,000$

General Journal

Account Titles & Explantion

Trial Balance

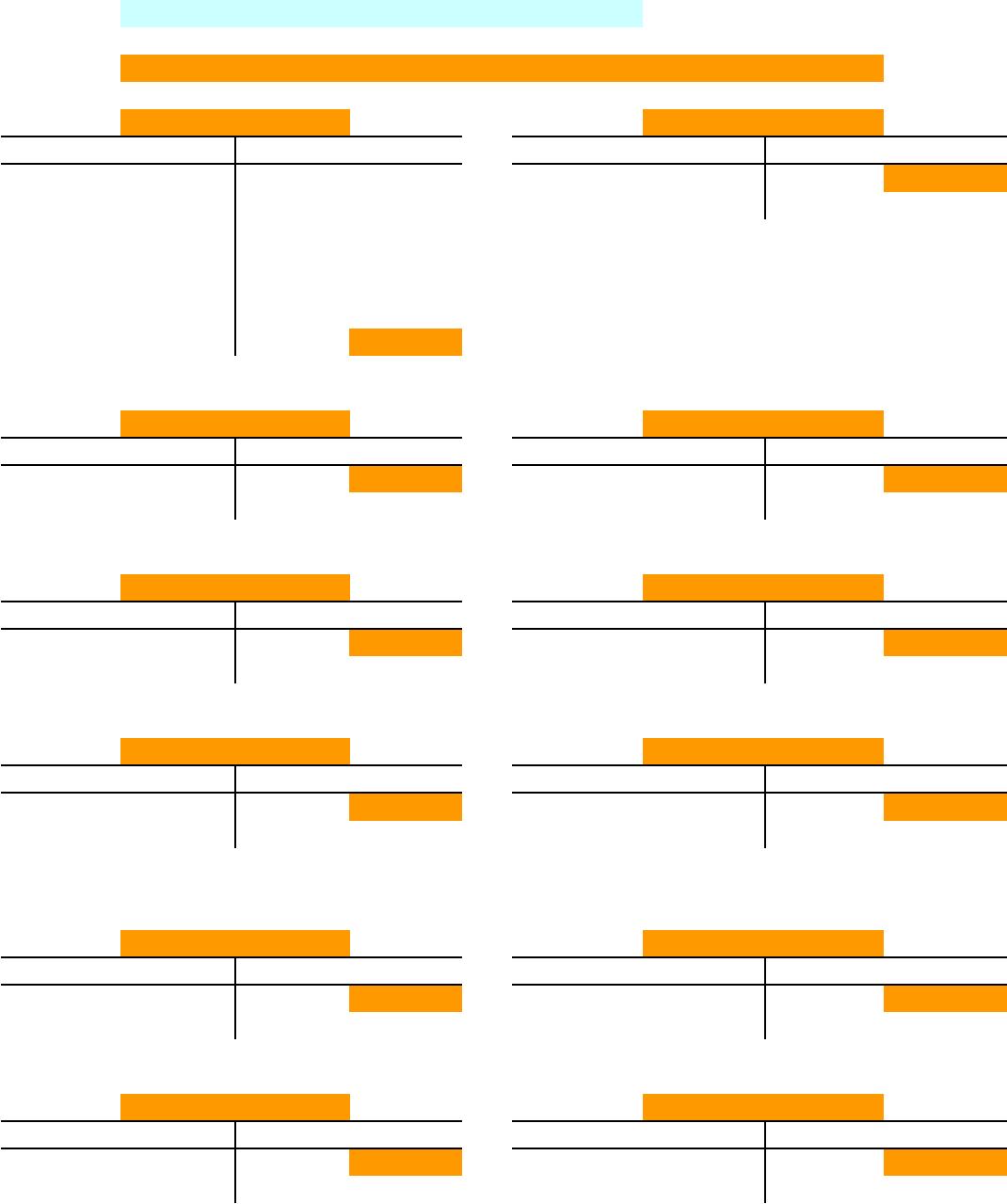

Chapter 2, Recording Process, page 69

General Journal and General Ledger

transactions (activities) are recorded, entered General Journal

post entries to General Ledger

Date Debit Credit

3/4/2013 Cash 2,280$

Service Revenue 2,280

3/15 Salaries & Wages Expense 400$

Cash 400

3/19 Utilities Expense 92$

Cash 92

post entries to General Ledger post entries to General Ledger

3/1/2013 600$ 400 3/15 Date Debit(+) Credit(-) Balance

3/4 2,280 92 3/19 3/1/2013 600$ 600$

3/31/2013 2,388$ 3/4 2,280 2,880

balance 3/15 400 2,480

3/19 92 2,388

3/31/2013 2,388$

General Journal

Account Titles & Explantion

Cash

Cash

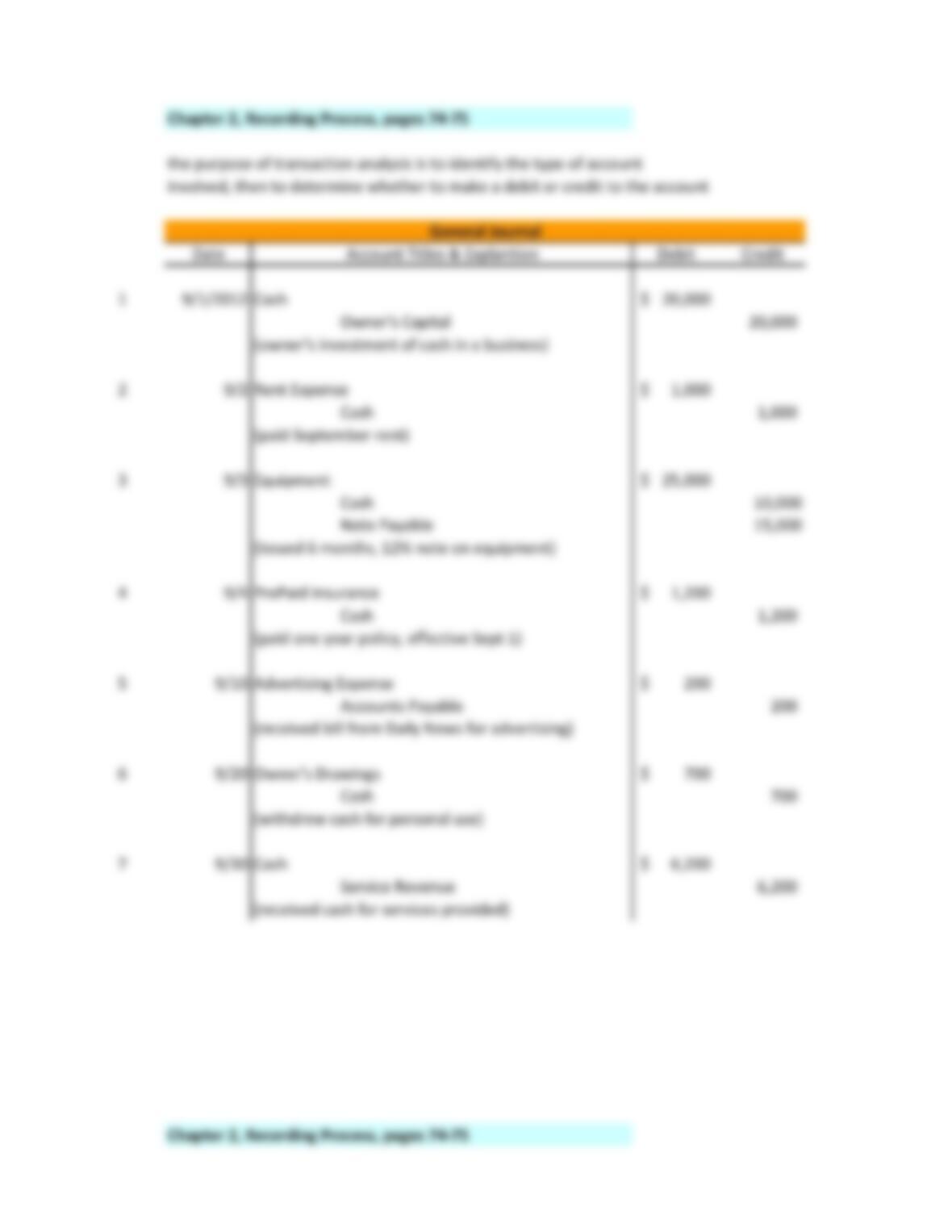

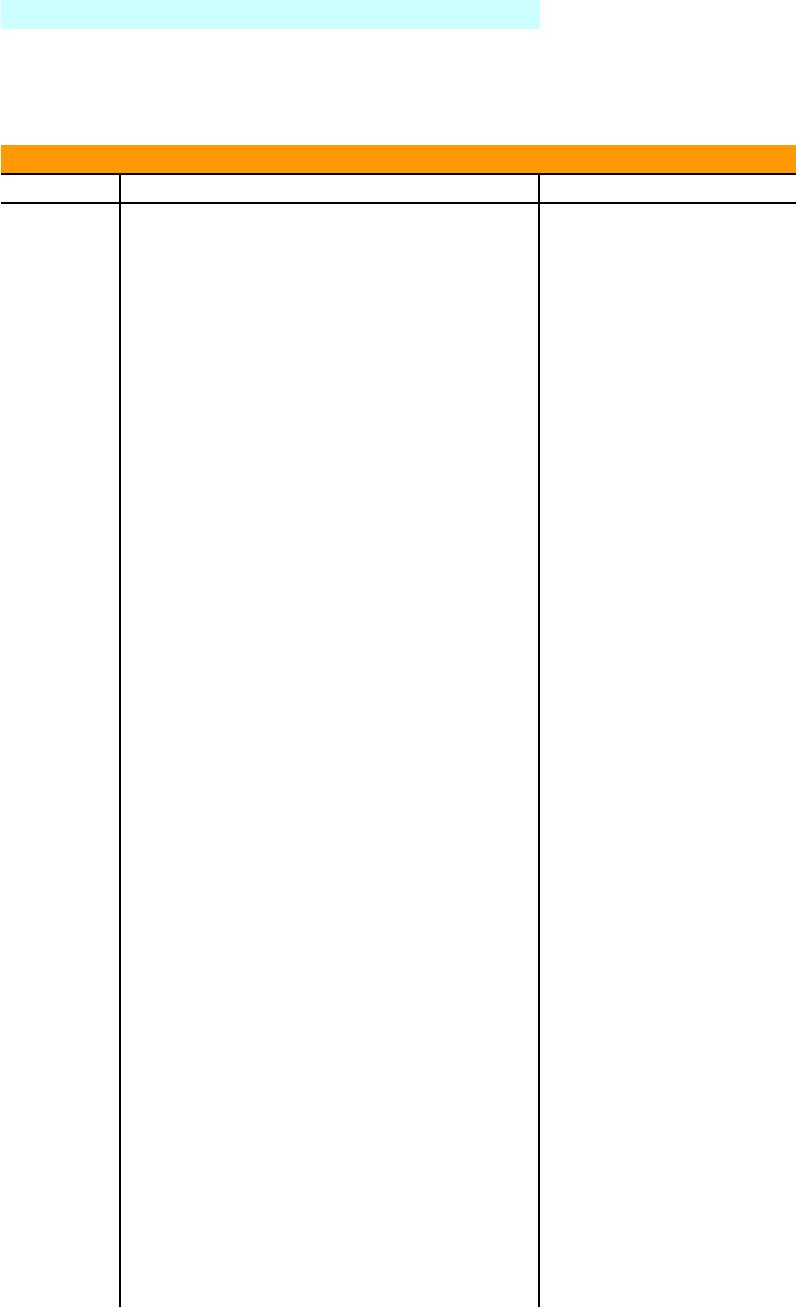

Chapter 2, Recording Process, pages 63 – 72 (pg 70)

The purpose of transaction analysis is to identify the type of account

involved, then to determine whether to make a debit or credit to the account

Date Debit Credit

1 10/1/2013 Cash 10,000$

Owner’s Capital 10,000

(owner’s investment of cash in a business)

2 10/1 Equipment 5,000$

Notes Payable 5,000

(purchase of equipment on account)

(issued 3 month, 12% note for equip)

3 10/2 Cash 1,200$

UnEarned Service Revenue 1,200

(cash received for future service)

4 10/3 Rent Expense 900$

Cash 900

(paid october rent)

5 10/4 PrePaid Insurance 600$

Cash 600

(paid one year policy, effective October 1)

6 10/5 Supplies 2,500$

Accounts Payable 2,500

(purchased supplies on account)

7 10/20 Owner’s Drawings 500$

Cash 500

(withdrew cash for personal use)

8 10/26 Salaries &Wages Expense 4,000$

Cash 4,000

(paid salaries to date)

9 10/31 Cash 10,000$

Service Revenue 10,000

(received cash for services provided)

General Journal

Account Titles & Explantion

Chapter 2, Recording Process, pages 63 – 72 (pg 71)

Date Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

10/1/2013 10,000$ 10,000$ 10/2/2013 1,200$ 1,200$

10/2 1,200 11,200

10/3 900 10,300

10/4 600 9,700

10/20 500 9,200

10/26 4,000 5,200

10/31 10,000 15,200$

Date Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

10/5/2013 2,500$ 2,500$ 10/1/2013 10,000$ 10,000$

Date Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

10/4/2013 600$ 600$ 10/20/2013 500$ 500$

Date Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

10/1/2013 5,000$ 5,000$ 10/31/2013 10,000$ 10,000$

Date Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

10/1/2013 5,000$ 5,000$ 10/26/2013 4,000$ 4,000$

Date Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

10/5/2013 2,500$ 2,500$ 10/3/2013 900$ 900$

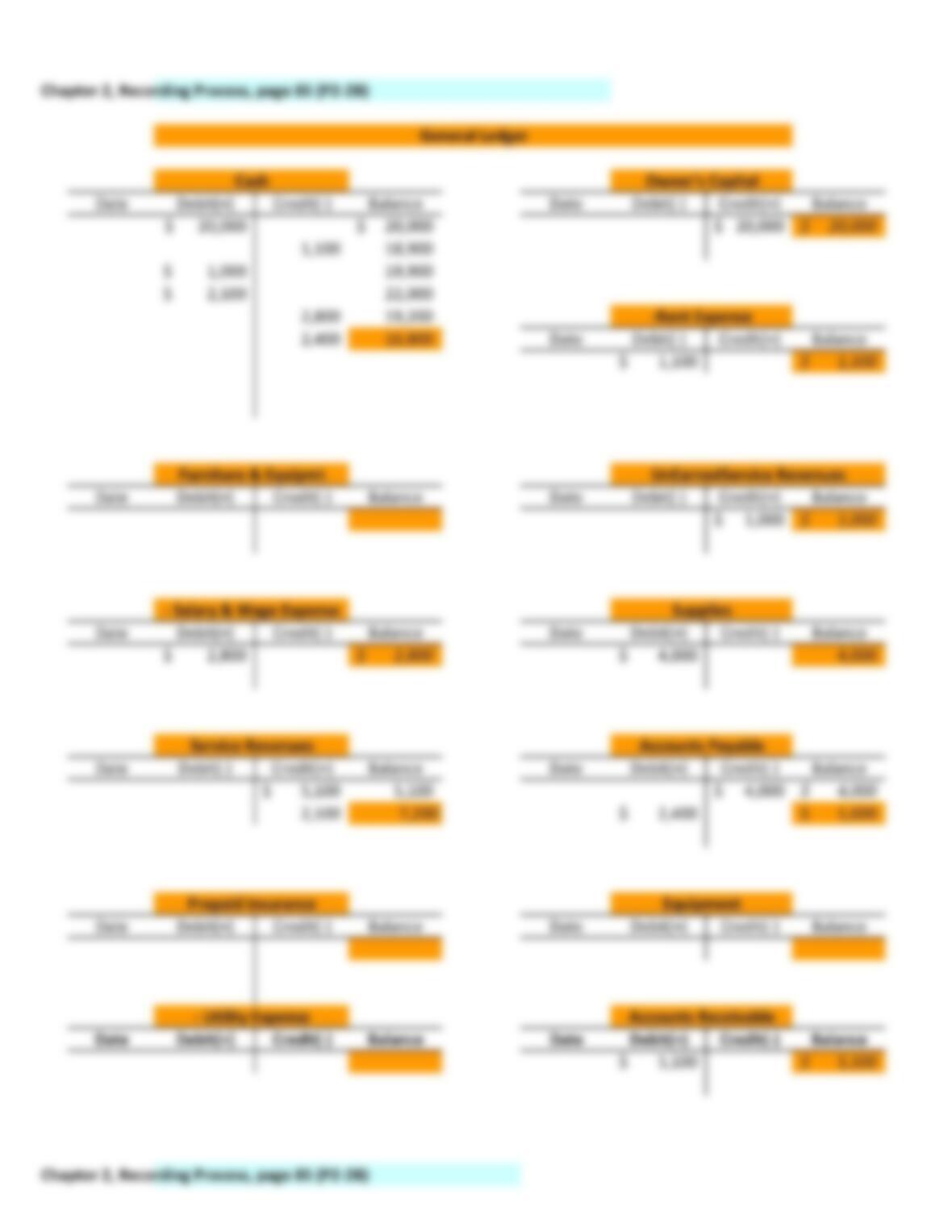

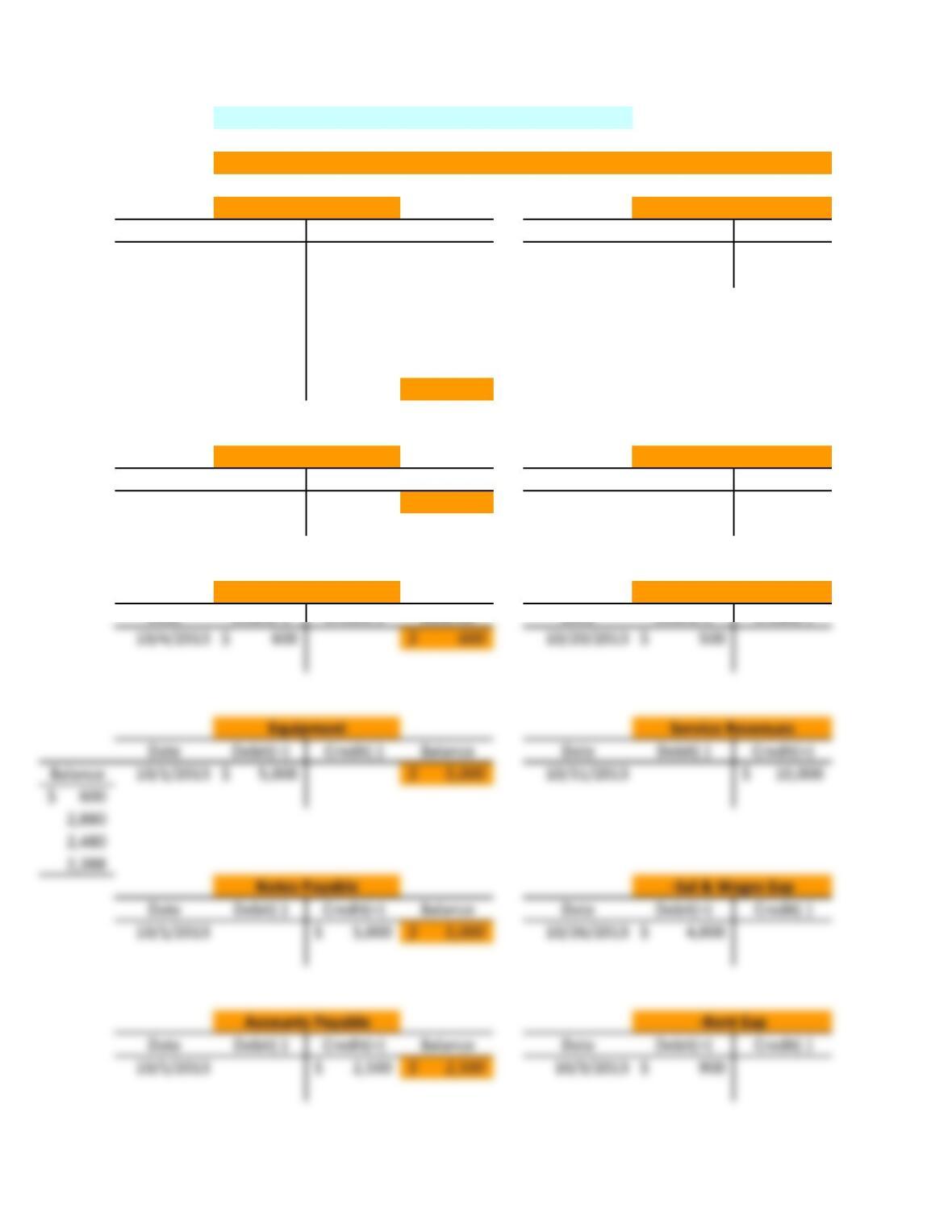

General Ledger

Cash

UnEarn Ser Rev

Supplies

Owner’s Capital

Service Revenues

-Owner’s Drawings

Equipment

Notes Payable

Accounts Payable

-Sal & Wages Exp

-Rent Exp

PrePaid Insur

Chapter 2, Recording Process, pages 63 – 72 (pg 72)

Pioneer Company

Trial Balance, October 31, 2012

Account Title Debit Credit

Cash 15,200$

Supplies 2,500

PrePaid Insurance 600

Equipment 5,000

Notes Payable 5,000

Accounts Payable 2,500

UnEarned Service Revenue 1,200

Owner’s Capital 10,000

Owner’s Drawings 500

Service Revenue 10,000

Salaries & Wages Expense 4,000

Rent Expense 900

28,700$ 28,700$

Trial Balance

Chapter 2, Recording Process, pages 63 – 72 (pg 70)

The purpose of transaction analysis is to identify the type of account

involved, then to determine whether to make a debit or credit to the account

Date Debit Credit

1 10/1/2013 Cash 10,000$

Owner’s Capital 10,000

(owner’s investment of cash in a business)

2 10/1 Equipment 5,000$

Notes Payable 5,000

(purchase of equipment on account)

(issued 3 month, 12% note for equip)

3 10/2 Cash 1,200$

UnEarned Service Revenue 1,200

(cash received for future service)

4 10/3 Rent Expense 900$

Cash 900

(paid october rent)

5 10/4 PrePaid Insurance 600$

Cash 600

(paid one year policy, effective October 1)

6 10/5 Supplies 2,500$

Accounts Payable 2,500

(purchased supplies on account)

7 10/20 Owner’s Drawings 500$

Cash 500

(withdrew cash for personal use)

8 10/26 Salaries &Wages Expense 4,000$

Cash 4,000

(paid salaries to date)

9 10/31 Cash 10,000$

Service Revenue 10,000

(received cash for services provided)

General Journal

Account Titles & Explantion

Chapter 2, Recording Process, pages 63 – 72 (pg 71)

Date Debit(+) Credit(-) Balance Date Debit(-) Credit(+)

10/1/2013 10,000$ 10,000$ 10/2/2013 1,200$

10/2 1,200 11,200

10/3 900 10,300

10/4 600 9,700

10/20 500 9,200

10/26 4,000 5,200

10/31 10,000 15,200$

Date Debit(+) Credit(-) Balance Date Debit(-) Credit(+)

10/5/2013 2,500$ 2,500$ 10/1/2013 10,000$

Owner’s Capital

-Owner’s Drawings

General Ledger

Cash

UnEarn Ser Rev

Supplies

PrePaid Insur

Date Debit(+) Credit(-) Balance Date Debit(+) Credit(-)

Date Debit(+) Credit(-) Balance Date Debit(-) Credit(+)

10/1/2013 5,000$ 5,000$ 10/26/2013 4,000$