Lincoln University

ACCT 203 Accounting Information Systems – Semester 1, 2018

Week 1 – Solutions from Chapter 1

Gelinas, U.J., Dull, R.B., & Wheeler, P.R. (2014). Accounting information systems (10 ed). Cengage Learning Australia Pty

Limited: Melbourne, Australia.

DQ 1-1 “I just want to be a good accountant, technology does not interest me.”

Comment on this statement, considering today’s technology environment.

ANS. Possible points that could be made:

a. Distinguish between an accountant and a bookkeeper. An understanding

of accounting software and related technology would enable one to

advance beyond entry-level positions.

b. Without knowledge of computer technology, an accountant can be a

bookkeeper/accountant for a small firm that does not use computers at

all. (With the ubiquitous nature of computers, this has become a weak

argument, at best.) More realistically, with the low cost of accounting

software, only very select organizations may not benefit from automation.

Examples of those organizations would include businesses that sell a low

volume of unique products.

c. Because the ability to access data, present data for decision making, audit

an accounting system, and so on are all affected by computer technology,

the career path for an accountant will be severely limited by a lack of

knowledge of computer technology.

d. The public accounting profession is competitive and the effective use of

technology helps maintain a competitive edge. For example, an auditor

can usually complete an audit engagement in less time—and be surer of

the findings—than he/she would be without using technology in the audit.

This will permit the auditor to charge less for the work and to obtain more

clients. And, if the auditor’s findings can be supported, he/she will be less

likely to experience legal ramifications (e.g., from the SEC, from

stockholders, and so on).

e. The Sarbanes-Oxley Act of 2002 requires that the CFO (and CEO) sign the

financial statements and attest to their accuracy, that companies notify

the Securities and Exchange Commission of material events within two

days, and that companies file their earnings statements within 35 days of

the end of a quarter. All of these requirements have implications for the

organization’s accounting information system and the ability of the CFO to

understand and monitor its operation.

2

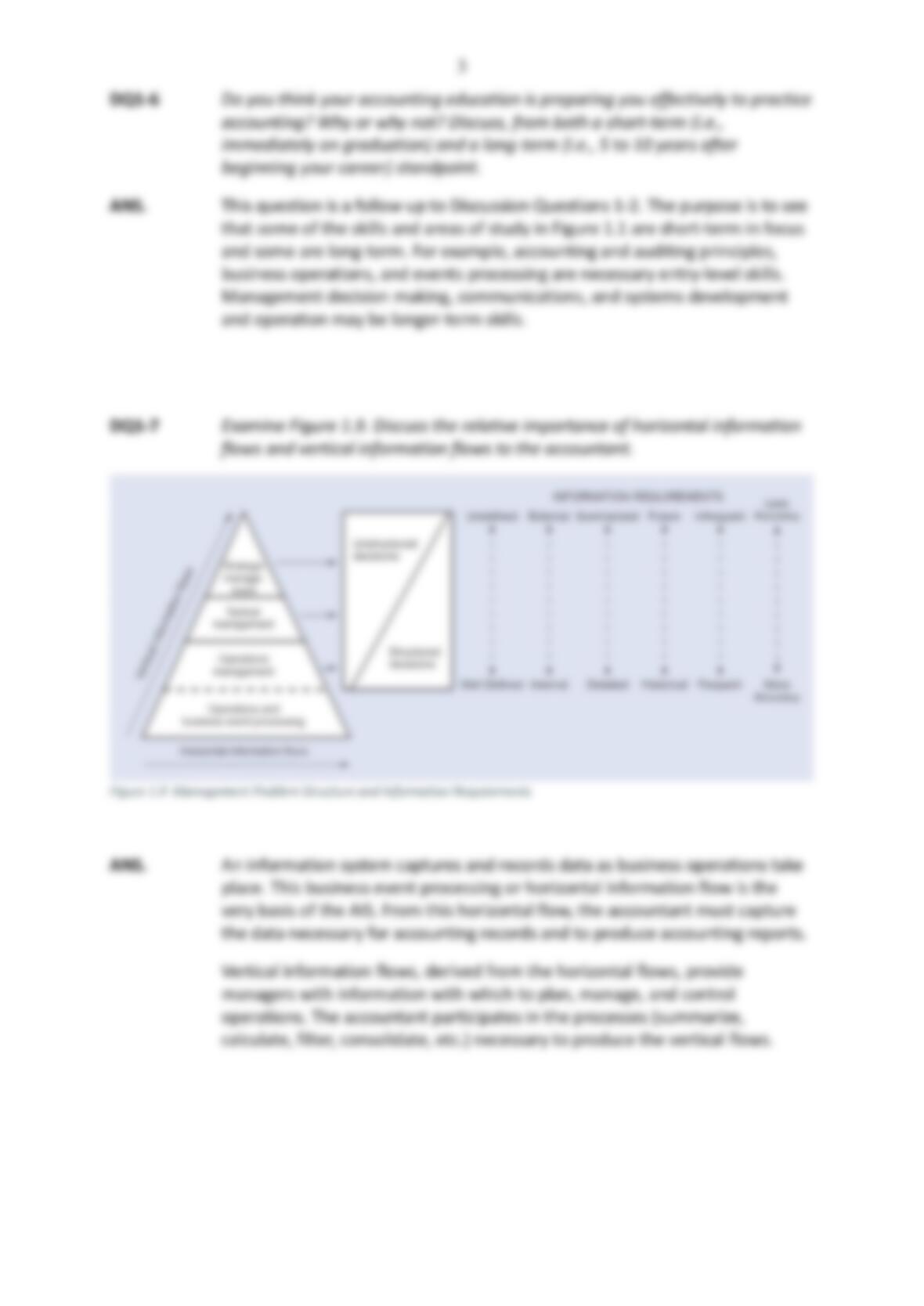

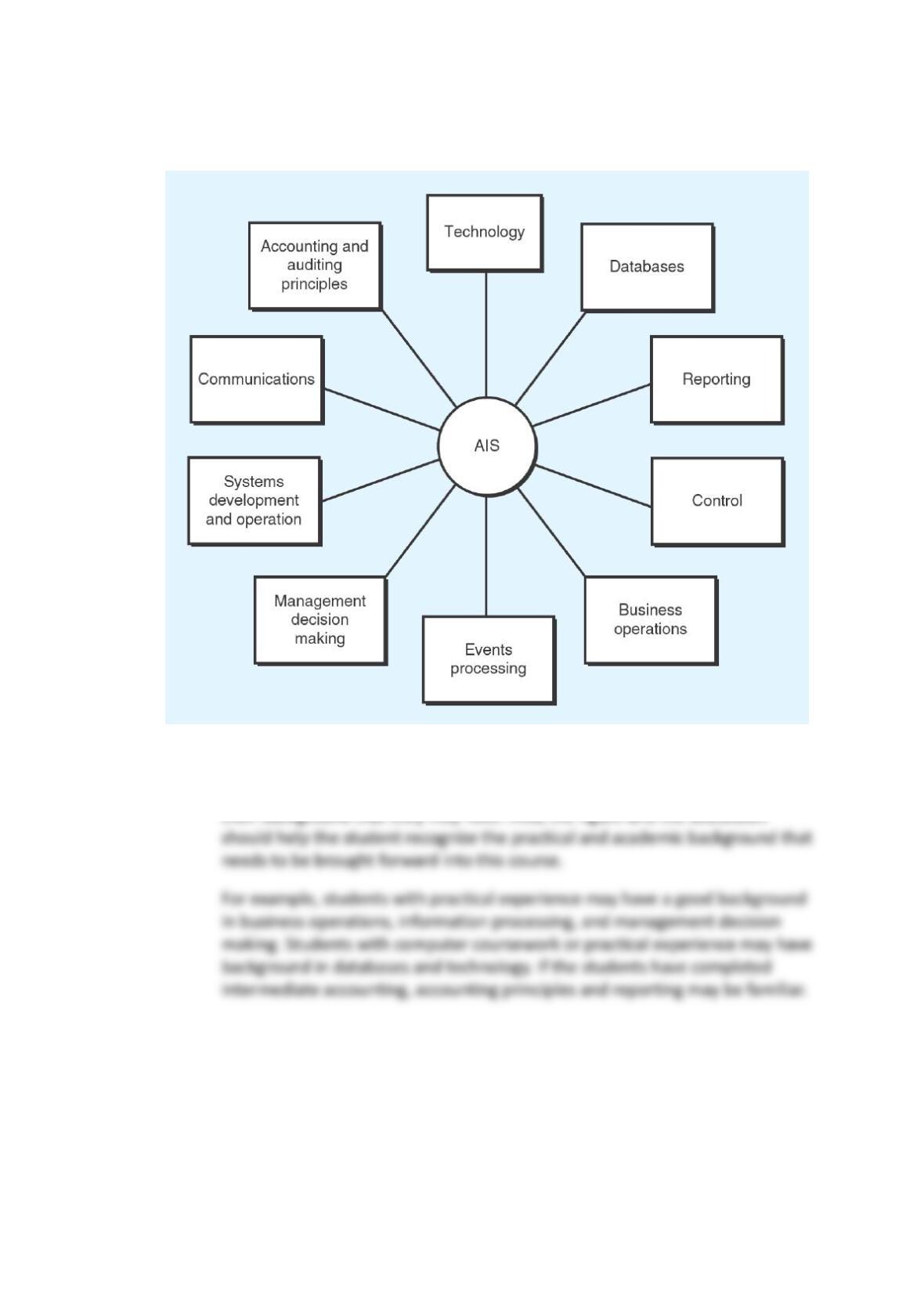

DQ 1-2 Examine Figure 1.1. Based on any work experience and university education to

date, with which elements are you least comfortable? With which are you

most comfortable? Discuss your answers.

Figure 1.1 Elements in the Study of AIS

ANS. The point of this question is to get the students to see the breadth of

coverage of the AIS course and to see how the course will help fill in gaps in