ACC 299 Fall 2018 Prof. Graybeal

– 1 –

Chapter 10

Cost Concepts for Decision Making.

Cost is often a key factor in decision making. When choosing between alternatives,

such as making a product versus buying it, the cost of one alternative should be

compared to the costs of other alternatives. One of the first steps to making these

decisions is to identify the relevant costs.

Identifying Relevant Costs.

A relevant cost is a cost that should have a bearing on which alternative the manager

selects.

a. Any cost that is avoidable is relevant for decision purposes. An

avoidable cost is a cost that can be eliminated (in whole or in part) as a

result of choosing one alternative over another. All costs are avoidable,

except sunk costs and future costs that do not differ between the

alternatives at hand. Note that “unavoidable” costs, are those that

cannot be avoided, in other words, unavoidable costs will have to be paid

regardless of the alternative chosen. (example: fixed cost)

b. Differential costs, or a cost that is different for each alternative, are

avoidable costs.

Four steps should be followed in identifying relevant costs in a decision situation.

Assemble all the costs and revenues associated with each alternative being

considered.

Eliminate those costs that are sunk costs.

Eliminate those costs and revenues that do not differ between alternatives.

Make a decision based on the remaining costs and revenues.

Types of costs that are found in decision making:

1. Different Costs for Different Purposes.

Costs which are relevant in one decision situation are not necessarily relevant in

another. In each situation the manager must examine the data and isolate the

relevant costs. Example: Suppose you are choosing between two different jobs.

Job 1 is 20 miles from your home and Job 2 is 35 miles from you home, obviously

the cost of travel is relevant in this decision choice as one requires you to drive

(and incur greater time sacrifices and greater cost) more than the other. But

instead, suppose you are choosing between two jobs that are in opposite

directions from your home but both are 15 minutes from your home. In this

case, travel costs are not relevant to your decision. Thus, you cannot make a

generic statement that travel cost should always influence your decision when

choosing a job as in the second scenario travel costs are the same and thus have

no influence on you choice, whereas travel costs would influence your decision

in the first scenario.

ACC 299 Fall 2018 Prof. Graybeal

– 2 –

2. Sunk Costs.

A sunk cost is a cost that has already been incurred and that cannot be avoided

regardless of which course of action a manager may decide to take. Example: In

preparation for summer employment, you bought a new lawnmower at the end

of last summer when it was at its lowest cost of the year, with the intent of using

that mower to create your own summer lawn care business the following

summer. When summer arrived, you were given the opportunity to work in your

uncle’s business as an office assistant. In choosing between the two jobs, one

think that you cannot consider is the money you have already spent on the

mower as that is a sunk cost. The cost has already been incurred and cannot be

avoided regardless of which summer job you choose.

a. As such, sunk costs have no relevance to future events and must be

ignored in decision making.

b. There is a strong human inclination not to exclude sunk costs when

making decisions.

Many people have difficulty correctly dealing with the book value of

old equipment in decisions. The book value of an asset is a sunk cost

which must be absorbed by the firm regardless of whether the asset

is kept and used or whether it is disposed of in some manner.

People are especially reluctant to discard sunk costs in decision-

making when the sunk costs are a consequence of a past decision that

in retrospect was unwise. People have a tendency to become

committed to courses of action that have not worked out.

Abandoning an asset for a loss is an admission of failure.

3. Future Costs That Do Not Differ.

Any future cost that does not differ between the alternatives in a decision

situation is not a relevant cost so far as that decision is concerned. Example:

Buying steel toed boots for summer job – future cost that would be not differ,

you would continuously buy because you know you would need them –

regardless.

ACC 299 Fall 2018 Prof. Graybeal

– 3 –

Example

Ellis Dover is a scout for a Major League Baseball team based in Phoenix, Arizona.

Ellis needs to travel to Los Angeles, California on June 1 to perform a variety of

professional functions prior to the team travelling to Los Angeles to play. If Ellis

flies, he could catch a 6 a.m. flight on June 1. In order to perform all of his

professional responsibilities, Ellis will need to spend the night and catch a flight

on June 2nd to return to Phoenix. If Ellis flies, he will need to rent a car for $38

per day. To cover meals and other incidental expenses, Ellis will receive $45 per

day (per diem) for each day he works out of town. Flights between Phoenix and

Los Angeles can be purchased for $89 one way.

Phoenix is approximately 300 miles from Los Angeles, a 5-hour drive at speed

limits permitted on the freeways connecting the two cities. If he drives from

Phoenix to Los Angeles, Ellis would need to leave the afternoon of May 31 and

would be reimbursed $.50 per mile. He would need to spend 2 nights in a hotel,

the night of May 31 and the night of June 1. He would return to Phoenix by car

on June 2nd. The hotel used by the team charges $160 per night.

What is the relevant cost of driving? (cost that differ from flying)

-Mileage

(𝟑𝟎𝟎 𝒎𝒊𝒍𝒆𝒔 𝒙 𝟐𝒘𝒂𝒚𝒔 𝒙 $. 𝟓𝟎 𝒑𝒆𝒓 𝒎𝒊𝒍𝒆)+ $𝟏𝟔𝟎.𝟎𝟎 𝒆𝒙𝒕𝒓𝒂 𝒉𝒐𝒕𝒆𝒍 𝒏𝒊𝒈𝒉𝒕

+ $𝟒𝟓.𝟎𝟎 𝒑𝒆𝒓 𝒅𝒊𝒆𝒎 = $𝟓𝟎𝟓.𝟎𝟎

What is the relevant cost of flying?(cost that differ from driving)

-Flight

𝒇𝒍𝒊𝒈𝒉𝒕( $𝟖𝟗.𝟎𝟎 + 𝟐 𝒘𝒂𝒚𝒔)+ 𝒓𝒆𝒏𝒕𝒂𝒍 𝒄𝒂𝒓 ($𝟑𝟖.𝟎𝟎 + 𝟐 𝒅𝒂𝒚𝒔)= $𝟐𝟓𝟒.𝟎𝟎

What is the incremental or differential cost of driving over flying?

Relevant driving cost – Relevant flying cost

$505.00 – $254.00 = $251.00

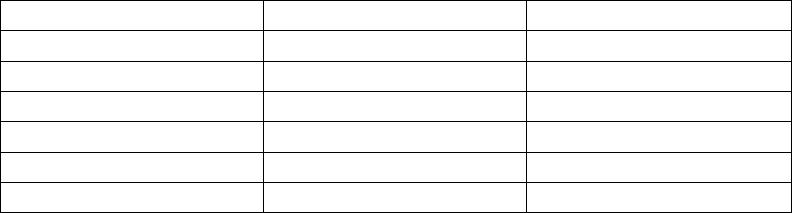

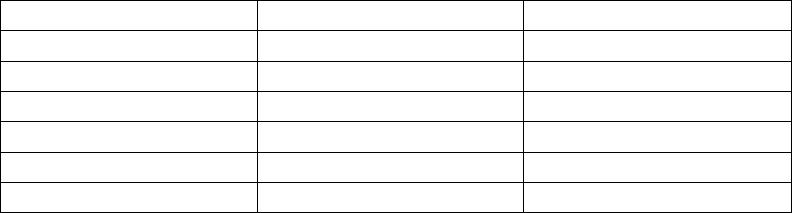

What is the total cost of each alternative?

Driving

Flying

Flight

$89.00 x 2 ways

Rental Car

$38.00 x 2 days

Per Diem

$45.00 x 3 days

$45.00 x 2 days

Hotel

$160.00 x 2 days

$160.00

Mileage

300 x 2 x $.50

Total:

= $755.00

=$504.00

Difference $755.00 – $504.00 = $251.00

ACC 299 Fall 2018 Prof. Graybeal

– 4 –

Problem 1:

Sam is trying to explain to Lexi about relevant costs and said that relevant costs are

those costs that are avoidable in making a business decision. Help Sam explain this to

Lexi given the following data, what is the total relevant cost of internal production of

2,000 products? Why are these particular costs relevant? Why are the others not

relevant?

Direct materials $12

Direct labor $ 4

Variable overhead $ 1

Total fixed overhead $9,000

Avoidable fixed $6,000

Sunk cost $8,000

Solution:

Relevant Costs: Direct materials $12

Direct labor $ 4

Variable Overhead $ 1

Total variable cost per unit $ 17

Units Produced x 2,000

Total variable costs $34,000

Avoidable Fixed Costs + 6,000

Relevant Costs $40,000

The $40,000 will only be incurred if units are produced, therefore these are avoidable

costs. If one was considering whether to stop, reduce or increase production, these

are the costs that should be considered in the analysis, adjusted obviously for the

units of production being considered. However, $3,000 of the fixed costs are

unavoidable and will be incurred whether or not there is any production, therefore

these fixed costs are not relevant and should not influence production decisions. Sunk

costs are always unavoidable as they are costs that have already been incurred and

cannot be “undone” thus they have no bearing on production decisions and are not

relevant.

ACC 299 Fall 2018 Prof. Graybeal

– 5 –

Various Business Decisions:

There are many decisions, or situations where a choice between alternatives must be

made, in the everyday operations of a business. What follows is an introduction to some

basic business decisions and how relevant costs, relevant revenues, differential

(incremental) costs and differential (incremental) revenues can be used to analyze these

decision choices. Keep in mind, that we are purely looking at numbers and are not

considering qualitative factors but in reality, those would need to be considered as well.

1. Adding or Dropping a Segment.

Decisions relating to dropping old products (or segments) and adding new

products (or segments) are among the most difficult that a manager makes. Two

basic approaches can be used to analyze data in this type of decision.

• Compare Contribution Margins and Fixed Costs.

A segment should be added only if the increase in total contribution margin is

greater than the increase in fixed cost. A segment should be dropped only if the

decrease in total contribution margin is less than the decrease in fixed cost.

• Compare Net Incomes.

A second approach is to calculate the total net income under each alternative.

The alternative with the highest net income is preferred. This approach requires

more information than the first approach since costs and revenues that don’t

differ between the alternatives are included in the analysis when the net

incomes are compared. (We assume in this chapter that any choice that

maximizes net operating income will also maximize net income. We focus on

net operating income in the text since we want to defer discussion of taxes to

Chapter 15.)

• Beware of Allocated Common Costs.

Allocated common costs are sometimes referred to as corporate or

headquarter costs. As an example, think of the headquarters building of Ford

Motor. In that building you will find the CEO, the VP’s, the accounting and

marketing and much of the HR components of the organization. Nothing is

produced or sold from that location, yet there are many costs associated with

that building and its occupants. These costs have to be “shared” among the

revenue generating components of the organization and thus these costs are

“allocated” or “split” between the revenue generating parts of the business.

This allocation can be based on percentage of revenue, square footage of the

factory, number of employees, etc. There are any number of ways the allocation

can occur. The important thing to note at this point is that allocated common

costs can make a segment look unprofitable, whereas, in fact, dropping the

segment might result in a decrease in overall company net operating income.

Allocated costs that would not be affected by a decision are irrelevant and

should be ignored in a decision relating to adding or dropping a segment.

ACC 299 Fall 2018 Prof. Graybeal

– 6 –

Example:

The Chia Pet Dept. of Trends Past Their Prime, Inc., has revenues of $600,000,

variable expenses of $300,000, avoidable fixed expenses of $100,000 and

unavoidable fixed expenses of $250,000. Trends is trying to decide what to do

with the Chia Pet Department. What is the effect on Trends’ net income if the

Chia Pet Dept. is eliminated?

Note: unavoidable fixed expenses of $250,000 will continue to exist even if

Chia Pet Department is eliminated, such as corporate cost.

Solution

Keep

Eliminate

Revenues

$600,000

0

Variable Cost

– (300,000)

0

Contribution Margin

= $300,000

0

Avoidable Fixed Cost

– ($100,00)

– ($250,00)

– ($250,000)

PreTax Income

= – ($50,000)

– ($250,000)

Conclusion: Keep Chia Pet Department it contributes to corporate profit more

than if it is eliminated. Its actually making $250,000 if it decides to keep the

unavoidable fixed expenses.

ACC 299 Fall 2018 Prof. Graybeal

Problem 2:

Betty Hopper, controller for Diamond Manufacturing Company, has prepared the

following financial information for the most recent period showing profitability the of its

three divisions:

The Furniture Division has been operating at a similar loss for a period of time and

Diamond’s management is considering eliminating the Furniture Division. The factory

insurance and advertising assigned to the Furniture Division is avoidable if the division is

discontinued. Depreciation will remain unchanged if a division is dropped. Discontinuing

Appliance

Electronics

Furniture

Sales

$102,000

$108,000

$120,000

Variable expenses

86,000

92,000

114,000

Contribution margin

16,000

16,000

6,000

Fixed expenses:

Factory insurance

1,000

1,400

2,200

Depreciation

2,000

2,600

3,600

Advertising

600

600

600

Utilities

800

1,000

1,200

Total fixed expenses

4,400

5,600

7,600

Operating income

$11,600

$10,400

($ 1,600)