CHAPTER 5

COVERAGE OF LEARNING OBJECTIVES

LEARNING OBJECTIVES QUESTION

S

EXERCISES PROBLEMS OTHER

LO1: Identify the purposes of

the statement of cash flows.

1,2,3

LO2: Classify activities

affecting cash as operating,

investing, or financing

activities.

4,5,6,7,8,9 32 45 71

LO3: Compute and interpret

cash flows from financing

activities.

10,12,13,14,15 33,34 46

LO4: Compute and interpret

cash flows from investing

activities.

11,12,13,14,15 35,36 47,48

LO5: Use the direct method to

calculate cash flows from

operations.

16,17 37,38,39,40 49,50,51,52,

53,54,55

LO6: Use the indirect

method to explain the

difference between net

income and net cash

provided by (used for)

operating activities.

18,19,20,21 41,42 56,57,58,59,

60,61,62,66,

67

LO7: Understand why we

add depreciation to net

income when using the

indirect method for

computing cash flow from

operating activities.

22,23,24 43,44 63

LO8: Show how the balance

sheet equation provides a

conceptual framework for the

statement of cash flows.

25 64,65

LO9: Identify free cash flow,

and interpret information in

statements of cash flow.

26,27,28,29,

30,31

68,69,70 72,73,74

Chapter 5 Statement of Cash Flows 147

CHAPTER 5

5-1 No. All public companies provide a statement of cash flows because it is a required

statement with a required format under both U.S. GAAP and IFRS.

5-2 A cash flow statement shows the sources of changes in cash balances and

a) aids in predicting future cash flows and evaluating how management’s decisions

generate and use of cash.

b) aids in determining a company’s ability to pay dividends and interest and to pay

debts when due.

c) aids in understanding and identifying changes in the mix of productive assets.

d) helps users understand the relationship of net income to changes in cash balances.

5-3 Cash equivalents are highly-liquid, short-term investments that can be converted easily

to cash with little delay. Examples include money market funds and treasury bills.

5-4 Operating activities, investing activities, and financing activities are the three major types

of activities summarized in the statement of cash flows.

5-5 Major operating activities include:

Collections Payments

from customers (for sales) to suppliers (for inventory)

from investees (interest and dividends) to employees (for wages)

to creditors (interest)

to government (taxes)

5-6 Major investing activities include the following:

a) Sales and purchases of plant, property, equipment and other long-term assets

b) Sales and purchases of securities that are not cash equivalents

c) Making and collecting long-term loans

5-7 Major financing activities include the following:

a) Borrowing from (nontrade) creditors

b) Repaying (nontrade) creditors

c) Issuing equity securities

d) Repurchasing equity securities

e) Paying dividends

5-8 Companies include the effect of exchange rates on cash, even though it is not a cash

flow. They include it because it is necessary to reconcile the beginning and ending cash

balances with the increases or decreases in cash on the cash flow statement.

148

5-9 Interest received appears in the operating activities section under both U.S. GAAP and

IFRS. Interest paid is also an operating item under U.S. GAAP. However, companies

reporting under IFRS have a choice of treating interest paid as an operating or financing

item.

5-10 Only increasing long-term debt increases cash. Both repurchasing common shares and

paying dividends decrease cash.

5-11 Selling fixed assets for cash and collecting a loan increase cash. Purchasing equipment

for cash decreases cash. Purchasing fixed assets by issuing debt does not affect cash, but

it should be shown in a schedule of noncash investing and financing activities.

5-12 When liabilities increase, the firm has either raised cash and promised to pay it back later

or it has preserved cash rather than paying it out to reduce amounts owed. Therefore,

more liabilities lead to more cash. Likewise, increases in noncash assets require cash.

Either cash is spent to get the asset or a noncash asset is recorded instead of receiving

cash.

5-13 Noncash investing and financing activities generally could have been accomplished

identically in substance (though not in form) by cash transactions. For example, issuing

debt to purchase an asset could have been accomplished by issuing debt for cash and

then using the cash to purchase the asset. Companies should not be able to prevent

disclosure of such a transaction to readers of the statement of cash flows simply by using

a noncash form of transaction. In addition, these transactions involve important

decisions made by management that should be disclosed to users.

5-14 This transaction should not be shown in the body of the statement of cash flows because

it involves no cash flows. However, it should be reported in an accompanying schedule

of noncash investing and financing activities. Why? The transaction could have been

accomplished by issuing stock for cash and then buying the fixed asset, whereby it would

be in the statement of cash flows. Readers of statements of cash flows should be

informed about such transactions.

5-15 Yes. It is important to know of the periodic need to pay off and refinance debt.

Companies with large short-term debt levels often find it an inexpensive way to borrow,

but when interest rates rise or a company’s financial condition worsens, refinancing may

be both difficult and expensive. The financing section should report the following:

Proceeds from short-term bank loan $1,000,000

Paid short-term bank loan ($1,000,000)

5-16 The direct method and the indirect method are the two major ways of computing net

cash flow from operating activities.

5-17 The information for the direct-method cash flow statement comes directly from entries

into a company’s Cash account.

Chapter 5 Statement of Cash Flows 149

5-18 Companies recognize sales revenue on the accrual basis when it is earned and realized

(or realizable), not when cash is received. Therefore, cash collections from customers

will not ordinarily equal sales revenue during any given period. Sometimes cash from

customers arrives before it is earned (creating a liability to perform) or after it is earned

(collection eliminates an account receivable).

5-19 Changes in the Inventory and Accounts Payable accounts explain the difference between

Cost of Goods Sold and cash payments to suppliers.

5-20 The required adjustments are to add noncash expenses and losses, deduct noncash

revenues and gains, add decreases in operating assets and increases in operating

liabilities, and deduct increases in operating assets and decreases in operating liabilities.

5-21 Strictly speaking, net losses, by themselves, do not drain cash. A net loss is an excess of

expenses over revenues; it is an income statement item rather than an item on a

statement of cash flows. As an extreme example, equipment may be sold below its book

value and cause a net loss, but cash proceeds resulting from the transaction would be an

addition to cash, not a cash drain.

5-22 The erroneous impression is that depreciation is a source of cash because it is added to

net income to determine cash flow from operations. Depreciation is an allocation of an

asset’s original cost to expense that does not entail a current cash outlay; that is,

depreciation is a noncash expense. It is added to net income when using the indirect

method only to offset its deduction in computing net income.

5-23 The newsletter reinforces the widely held erroneous impression that depreciation

provides cash. See the solution to 5-22.

5-24 Under the indirect method for reporting cash flows from operations, depreciation is very

prominent in the calculation, although not directly a source of cash. Depreciation is one

of the items that reconcile net income to net cash flow from operating activities.

5-25 Cash + Noncash assets = Liabilities + Paid-in capital + Retained earnings

Cash = Liabilities + Paid-in capital + Retained earnings – Noncash assets

5-26 Profitable companies often lack for cash because they are growing quickly and must

acquire inventory for future sales while waiting to collect growing receivable balances.

New firms in industries such as computers, electronics, and bio-tech might experience

this.

5-27 Large, noncash expenses such as depreciation could cause this. The airline industry

might be a good example.

150

5-28 I would be concerned about this company. Negative cash flow from operations and new

investing is not uncommon among new, high-growth firms. However, at that stage of a

company’s life the financing is generally from equity and longer–term debt. The

significant use of short-term debt suggests that the equity and long-term debt markets

are not and will not be open to this client. Unless profitability and positive cash flow

from operations are around the corner, this company could have serious problems

raising additional capital. This may not be a good investment.

5-29 It is always hard to know what is in a manager’s mind. Google experienced explosive

growth. It has acquired companies on a regular basis, but its available cash and liquid

investments continue to grow. It does not make sense to continue to manage low

yielding investments in government bonds and such. Unlike some companies, Google

chose not to pay dividends or buy back its own common stock. It seems that Google’s

management feels that its future opportunities are great enough that it should have the

funds available for further investment when appropriate.

5-30 Until 2002 Amazon had negative cash flows from operations, and therefore its free cash

flow was negative. This is often the case for new companies that are proceeding toward

but not yet at profitable operations. The positive cash flow from operations after 2002

indicates that Amazon is maturing. The growing free cash flow is a sign that Amazon is

entering a stage where growth may be slowing but profitability is increasing.

5-31 This attitude would prevent anyone from ever investing in a brand new company with a

great idea. Since these companies are often risky, this strategy might be quite

appropriate for investors who are retired and rely on investments for living expenses.

However, for a younger person with more ability to take risk, an appropriate exposure

to young, dynamic growth companies might be quite appropriate. The characteristics

referred to in the question identify the target investments as young growth companies

for the most part but do not reveal much about other investment decision variables such

as the industry, the age of the firm, the nature of the product, and so on.

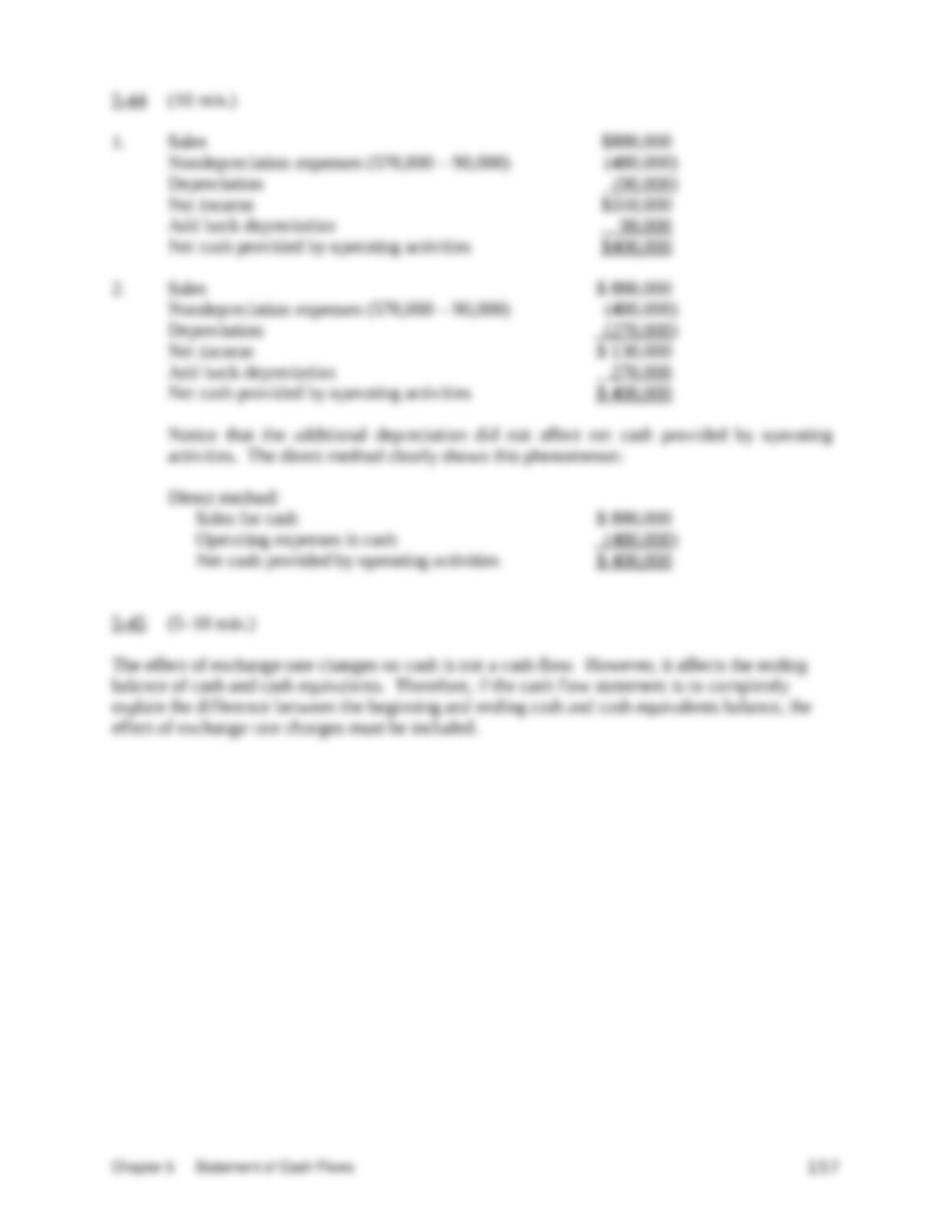

5-32 (5–10 min.)

a. Operating f. Financing

b. Financing g. Operating

c. Financing h. Operating

d. Investing i. Financing

e. Financing

Because net income and depreciation appear in the body of the statement of cash flows,

AT&T must use the indirect method for reporting cash flows from operating activities.

Chapter 5 Statement of Cash Flows 151

5-33 (10 min.)

BUBBA’S CATFISH, INC.

Statement of Cash Flows from Financing Activities

For the Year Ended December 31, 20X1

Proceeds from issuance of common stock $100,000

Proceeds from issuance of debt 50,000

Dividends paid (2,000)

Repurchase of common shares from stockholders (10,000 )

Net cash provided by financing activities $138,000

5-34 (10 min.)

MARSEILLES SHIPPING COMPANY

Statement of Cash Flows from Financing Activities

For the Year Ended December 31, 20X0

Cash flows from financing activities:

Proceeds from issue of long-term debt € 180,000

Payment to retire long-term debt (160,000)

Payment to retire common stock (35,000)

Dividends paid (11,000)

Net cash used for financing activities € (26,000)

Notice especially that both proceeds from the new issue and the payment to retire long–

term debt are listed. Presenting only the net amount, €20,000 of proceeds, is not permitted.

Also, the interest is omitted because most companies, whether reporting under IFRS or

U.S. GAAP, would consider it an operating activity, not a financing activity. However, in

reporting under IFRS, Marseilles Shipping could list the €21,000 interest payment as a financing

activity, making net cash used for financing activities €26,000 + €21,000 = €47,000.

5-35 (5–10 min.)

BRISBANE TRADING COMPANY

Statement of Cash Flows from Investing Activities

For the Year 20X0

Purchases of fixed assets $(160,000)

Proceeds from the sale of fixed assets 20,000

Investment in Fellski Company (65,000)

Net cash used for investing activities $(205,000)

152

5-36 (5–10 min.)

JACOBY COMPANY

Schedule of Noncash Investing and Financing Activities

Note payable issued for acquisition of fixed assets $122,000

Common stock issued on conversion of preferred shares 340,000

Mortgage assumed on acquisition of warehouse 530,000

5-37 (5 min.)

There are two ways to compute cash collections:

Sales $800,000

Less increase in accounts receivable (30,000)

Cash received from customers $770,000

Or

Cash sales (.2 × $800,000) $160,000

Collections of receivables

[(.8 × $800,000) + $60,000 – $90,000] 610,000

Cash received from customers $770,000