Advanced Accounting

Thirteenth Edition, Global Edition

Chapter 3

An Introduction to

Consolidated Financial

Statements

Copyright © 2018 Pearson Education, Ltd. All Rights Reserved.

Intro to Consolidations: Objectives

3.1 Recognize the benefits and limitations of

consolidated financial statements.

3.2 Understand requirements for including a subsidiary

in consolidated financial statements.

3.3 Apply consolidation concepts to parent company

recording of an investment in a subsidiary company

at the date of acquisition.

3.4 Record the fair value of a subsidiary at the date of

acquisition

3.5 Learn the concept of noncontrolling interest when a

parent company acquires less than 100 percent of a

subsidiary’s outstanding common stock.

Copyright © 2018 Pearson Education, Ltd. All Rights Reserved.

Intro to Consolidations: Objectives (continued)

3.6 Prepare consolidated balance sheets subsequent to

the acquisition date, including preparation of

eliminating entries.

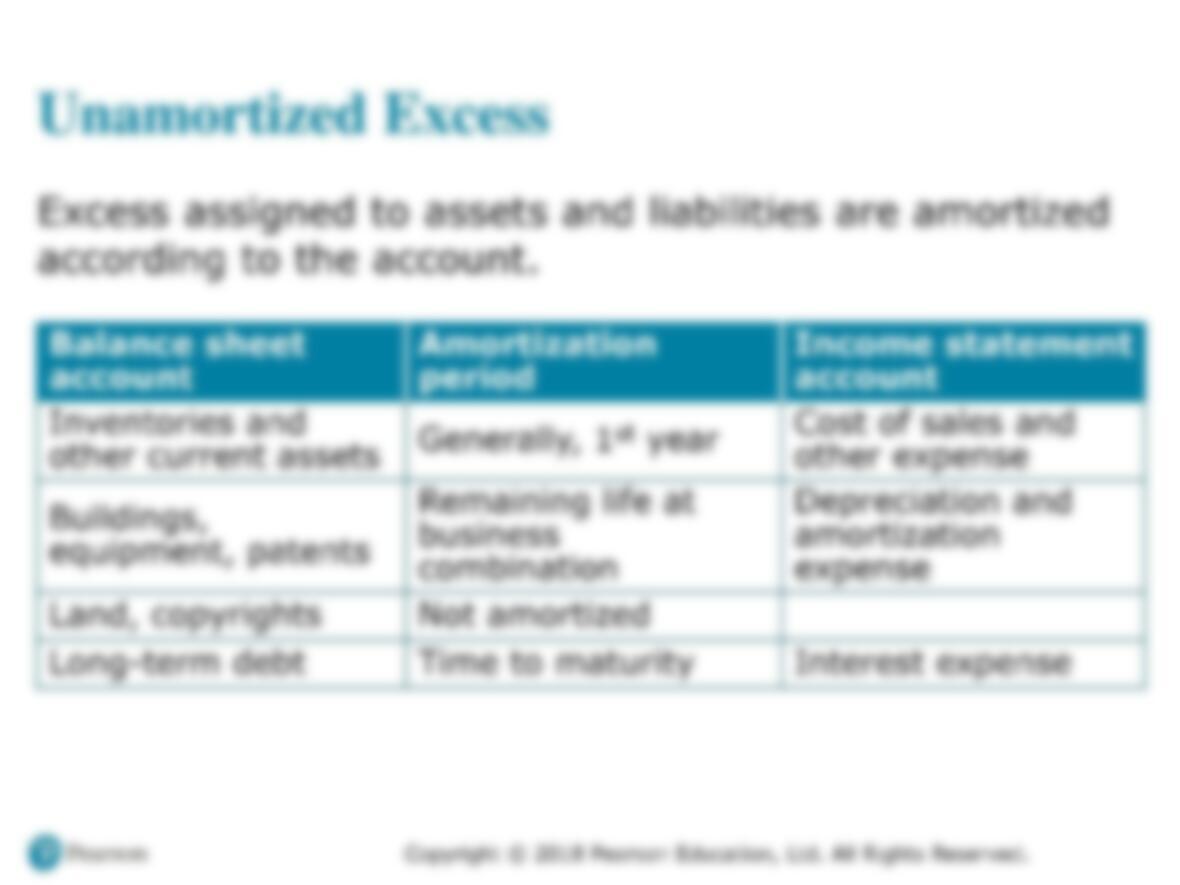

3.7 Amortize the excess of the fair value over the book

value in periods subsequent to the acquisition.

3.8 Apply the concepts underlying preparation of a

consolidated income statement.

Copyright © 2018 Pearson Education, Ltd. All Rights Reserved.

3.1: Benefits and Limitations

An Introduction to Consolidated Financial Statements

Copyright © 2018 Pearson Education, Ltd. All Rights Reserved.

Business Acquisitions

Business combinations through stock acquisitions

–Acquire controlling interest in voting stock

–More than 50%

–May have control through indirect ownership

Business combination occurs once

–Acquisition of additional subsidiary stock is

simply additional investment.

Copyright © 2018 Pearson Education, Ltd. All Rights Reserved.

Consolidated Statements

–Primarily benefit the owners and creditors of the

parent

–Not primarily intended for the noncontrolling

owners nor the subsidiary’s creditors

–Subsidiaries issue separate statements for the

benefit of their owners and creditors.

3.2: Subsidiaries