Tutorial 2 Cash Cycle

5

Tutorial 2: Suggested solutions

Section A:

1. (a) Cash transactions are transactions where payment is made/collected

immediately (upon purchase/sale) whereas credit transactions are

transactions where payment is made/collected at a future date, based

on the credit period given, normally 30 days, 60 days, or 90 days.

(b) Discounts are deductions allowed by the supplier to the customer.

Trade discount is a percentage reduction granted to a customer from

the list price due to the purchase of a large quantity whereas cash

discount (discount received and discount allowed) is a percentage

reduction granted to the customer in order to encourage earlier

payment (earlier than the credit period given).

(c) Cash is money that belongs to the business. It is a current asset.

There are three types of cash in the business, i.e. cash at bank, cash in

hand and petty cash. Cash at bank is the money in the business’

current account with the bank. This account usually does not yield any

interest but offers cheque facility. Cash in hand is the money that the

business keeps in its premises for daily purchases. This is usually

controlled by the cashier. Petty cash is also money kept by the business

for daily small/petty purchases and is usually kept by the petty cashier.

2. (a) Cash Book is a book of prime entry, used to record all types of

cash and cheque transactions, i.e. actual cash received or paid, deposits

into the bank account and issuance of cheques from the bank account.

It is basically putting together side by side the bank, cash, discount

allowed and discount received accounts. On the debit side of the cash

book are the bank and cash items received and discount allowed

columns. On the credit side are the bank and cash items issued/paid and

discount received columns. Since it is four ‘T”accounts put side by

side, the Cash Book also functions as the General Ledger accounts for

cash account and bank account.

(b) The cash book is basically a few “T” accounts put together side by

side. For example, a three column cash book consists of 4 accounts i.e.

bank, cash, discount allowed and discount received. It is a book of

prime entry because this is where transactions are originally recorded

(recorded for the first time). For other transactions like sales and

purhases, the total of the monthly amounts of the books of prime entry

(sales journal and purchases journal) will be posted from the books of

prime entry to the respective “T”accounts (ledger) i.e. sales and

purchases accounts. Not so for the cash and bank closing totals as they

are already recorded in the respective “T”accounts in the cash book.

However, the totals of the discount allowed and discount received

accounts are still posted to their respective discount allowed and

discount received ledger accounts from the cash book.

(c) Bank overdraft is a special loan that had been approved by the bank

for the business to issue cheques more than the amount deposited into

the current account i.e. the current account can go negative without

havings its cheques issued being dishonoured.

The bank overdraft facility will specify the maximum limit available

for the business to use. Bank interest will be calculated based on the

actual amount of bank overdraft balance on a monthly basis.

3. (a) Petty cash book is both a book of original entry and a ledger. It is

used to record small cash payment for any immaterial expenses such

as taxi fare, purchase of stationery, postage, donation and etc. Normally

the cash float amount is not more than RM1000.The workings of the

petty cash book is similar to that of the cash book. The items are

analysed into various categories to enable easy posting to the various

expenses accounts at the end of every month.

(b) The imprest system is used to manage the petty cash of a business.

A float is firstly determined by the management for daily petty cash

payments. This is the maximum amount that is based on the needs of

the business. It is usually small i.e. less than RM1,000. The petty

cashier will receive this amount at the beginning of the month and then

Tutorial 2 Cash Cycle

6

use it to pay for petty items throughout the month. At the end of the

period, the cashier will reimburse the petty cashier the amount of petty

cash spent during the period so that the petty cashier will start with the

same amount of the petty cash float. All payments are usually

evidenced by petty cash vouchers.

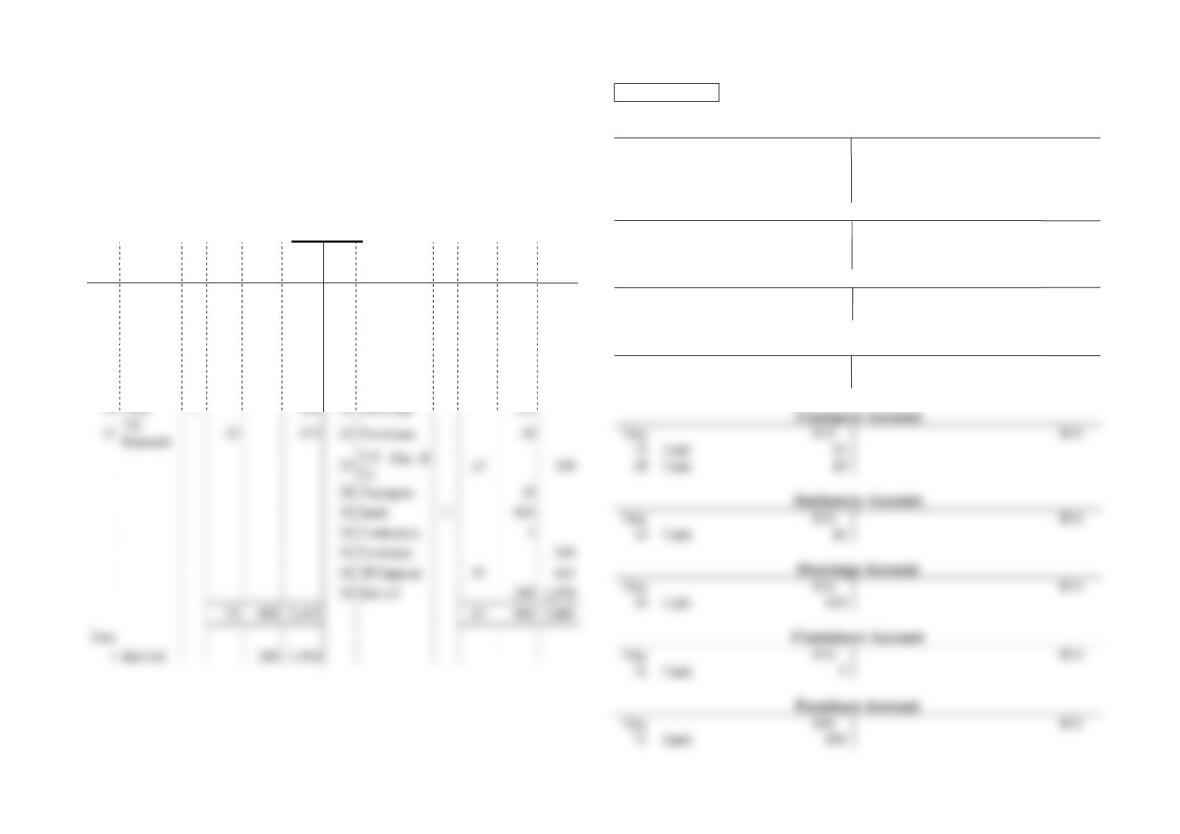

Question 4

Cash Book

Date

Particular

Fol

Disc.

Cash

Bank

Date

Particular Fol

Disc.

Cash

Bank

Allw

Rec’d

May

RM

RM RM May

RM RM RM

1

Capital

800

1,000

2

Purchases

400

9

Sales

80

2

Rates

40

15

Capital

1,000

10

Transport 12

16

TR:

T

odds

30

570

14

Stationery 16

General Ledger

Capital Account

RM

May

RM

1

Cash

8

00

1

Bank

1,000

15

Bank

1,000

Purchases Account

May

RM

RM

2

Bank

400

24

Cash

28

Rates Account

May

RM

RM

2

Bank

40

Sales Account

RM

May

RM

9

Cash

80

Ken

neth

Co

May

RM

RM

10

Cash

12

28

Cash

10

May

RM

RM

May

RM

RM

20

Cash

120

May

RM

RM

31

Cash

5

May

RM

RM

31

Bank

200