Tutorial 1 Introduction to Accounting

4

Tutorial 1: Suggested solutions

Section A

1. Accounting is the process of providing data/information to the respective

users to help them make business decisions. It involves the following stages:

i) Collecting – source documents as evidence/proof of transactions

and as the source for recording business transactions.

ii) Recording – relevant details from source documents in the respective

books of prime entry.

iii) Summarising – from the books of prime entry and transferring

(posting) these summaries to the respective ledgers (T accounts).

iv) Communicating the accounting information to users, by preparing the

financial statements for decision making purposes.

2. Bookkeeping is an initial part of the accounting process that emphasise on –

collecting and recording business transactions from the source documents

to the respective books of prime entry, using the double entry system.

Accounting is the process of providing data/information to the

respective users to help them make business decisions.

3. Accounting equation is an equation which is based on the principle that

all the assets (resources) available/owned by a business are either

provided by the owner (equity) and/or supplied by outsiders

(liabilities) i.e.

Assets = Equity + Liabilities

It follows that after every business transaction, the equation still

balances.

4. In order for accounting information to be useful in helping users make

decisions, they need to be sorted into orderly and meaningful

categories (classified). They also need to be summarised so that the

users can ascertain the performance and position of the business rather

than getting lost in the mass pool of data.

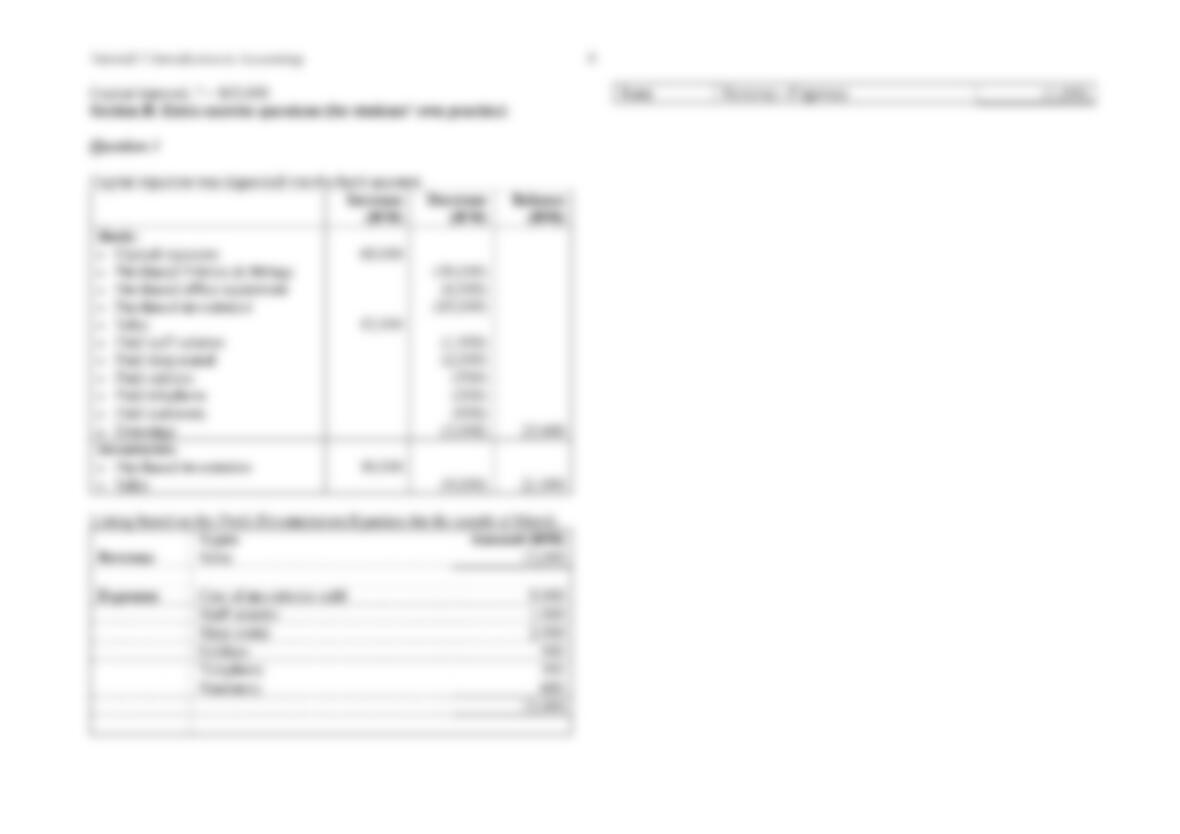

5. Liabilities = RM32,000

Assets = RM85,000

Equity = RM67,000

Equity = RM156,900

Liabilities = RM38,000

6.

Types Amount (RM)

Assets

Bank

20,000

Cash

2,000

Inventories

19,000

Motor vehicles

80,000

Receivables

18,000

139,000

Liabilities

Loan

50,000

Payables

15,000

Equity

Capital

?

Drawings

(5,000)

Loss

(

13,000

)

139,000

Capital ? = RM92,000

Tutorial 1 Introduction to Accounting

5

7.

Revenue Correct classification Dr/Cr

Discount received

Income (Other income)

Cr

Commission received

Income (Other income)

Cr

Rece

ivables

Asset

Dr

Cash from owner

Equity

Cr

Sales

Income

Cr

Inventory sold Cost of goods sold –

Expenses

Dr

Insurance claim

received

Income (Other income) Cr

Carriage inwards Cost of goods sold –

Expenses

Dr

Advertising

Expenses

Dr

Office stationery Expenses. Or is it Asset?

(Can do discussion)

Dr

management & control, liability of owner(s), sharing of profit, taxability

etc. Each also has its advantages and disadvantages. Please refer Lecture

notes for details.

10 Your answer should touch on these areas:

Ease of raising capital, management & control of business, profit

sharing, liability of owners on business’ debts, how are the owners

taxed etc.

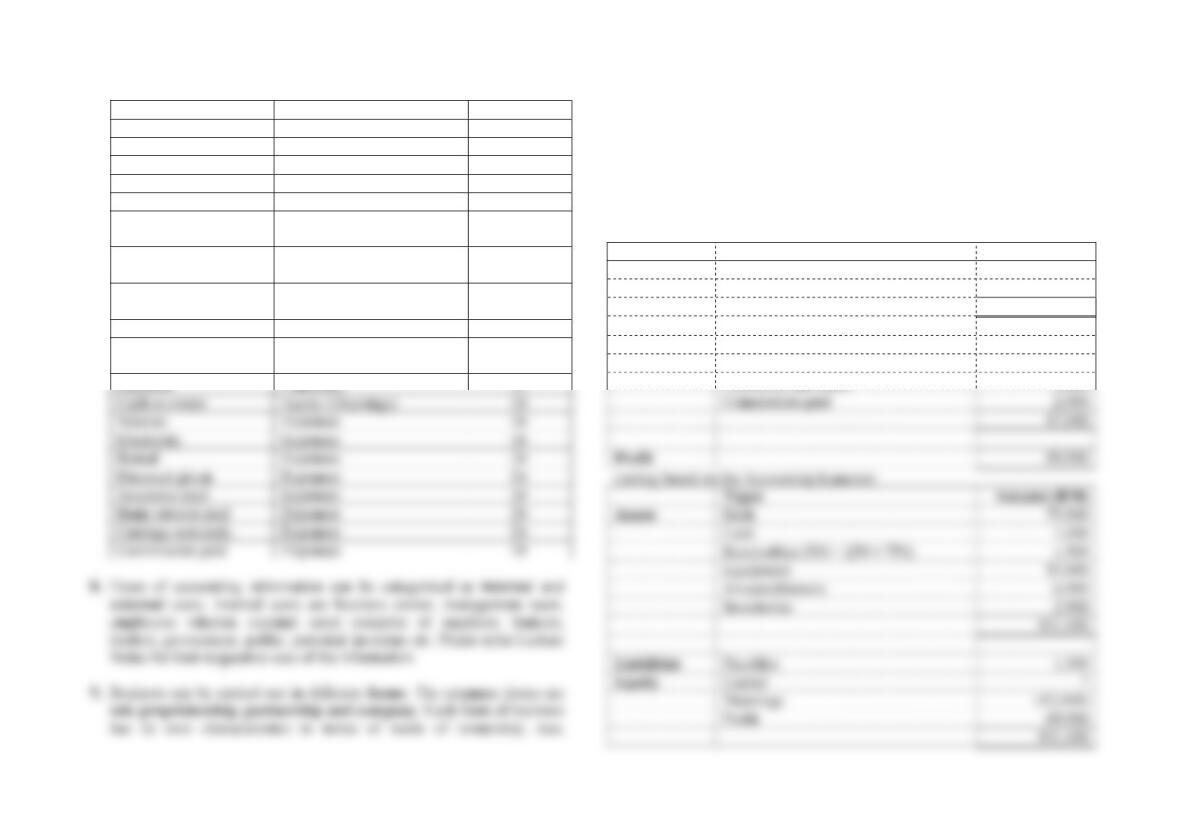

11.

Listing based on the Profit Determination Equation:

Types Amount (RM)

Revenue

Sales

86,6

6

0

Interest received

300

86,96

0

Expenses

Cost of inventories sold

5,150

Rental

6,000

Electricity and water

3,880

Cash to owner

Equity (Drawings)

Dr

Salaries

Expenses

Dr

Rental

Expenses

Dr

Discount given

Expenses

Dr

Bank interest p

aid

Expenses

Dr

Commission paid

2,000

1

7

,

0

30

69,930

Cash

1,030

Inventories

2,900

Payables

1,500

Capital

?