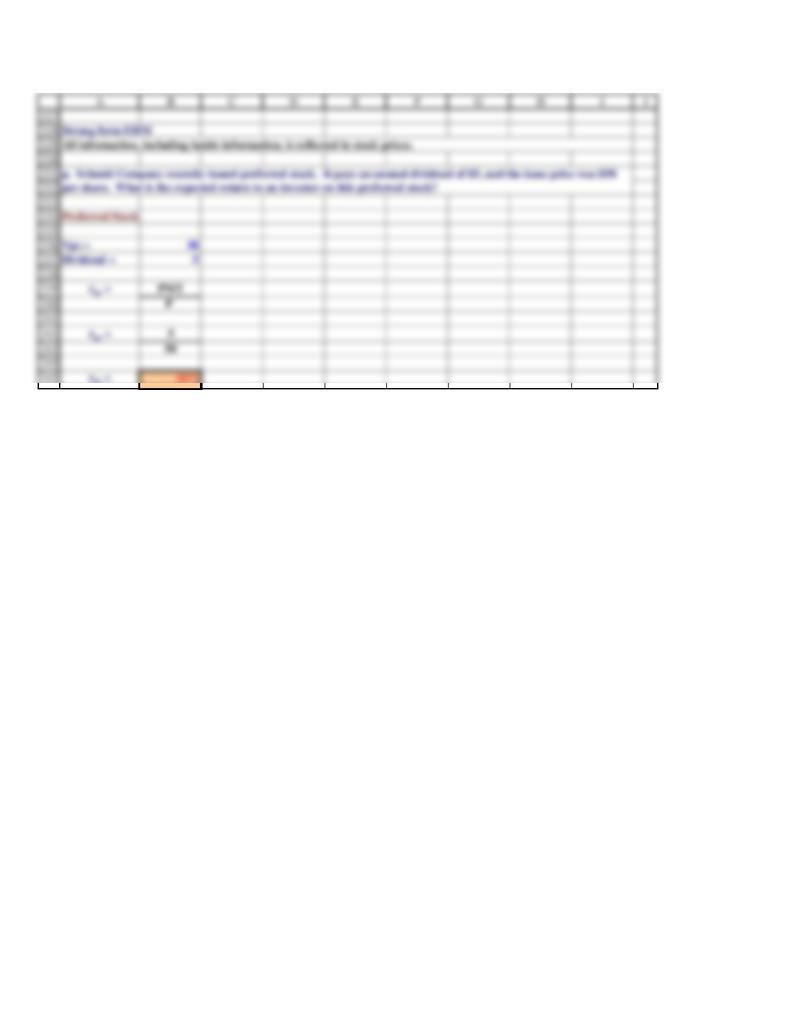

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

A B C D E F G H I J

Ch 7 Mini Case 5/11/2003

Situation

Features of Common Stock

Classified Stock

THE DISCOUNTED DIVIDEND APPROACH

D 1+D 2+. . . . D n

( 1 + r s ) ( 1 + r s ) 2 ( 1 + r s ) n

VALUING STOCKS WITH A CONSTANT GROWTH RATE

The dividend stream theoretically extends on out forever, i.e., n = infinity. Obviously, it would not be feasible to deal

with an infinite stream of dividends, but fortunately, an equation has been developed that can be used to find the PV

of the dividend stream, provided it is growing at a constant rate.

Naturally, trying to estimate an infinite series of dividends and interest rates forever would be a tremendously

difficult task. Now, we are charged with the purpose of finding a valuation model that is easier to predict and

construct. That simplification comes in the form of valuing stocks on the premise that they have a constant growth

rate.

(2.) What is a constant growth stock? How are constant growth stocks valued?

Here is the basic dividend valuation equation:

Classified Stock carries special provisions. For example, shares could be classified as founders shares which come

with voting rights but dividend restrictions.

b. (1.) Write out a formula that can be used to value any stock, regardless of its dividend pattern.

The value of any financial asset is equal to the present value of future cash flows provided by the asset. When an

investor buys a share of stock, he or she typically expects to receive cash in the form of dividends and then,

eventually, to sell the stock and to receive cash from the sale. Moreover, the price any investor receives is dependent

upon the dividends the next investor expects to earn, and so on for different generations of investors. Thus, the

stock’s value ultimately depends on the cash dividends the company is expected to provide and the discount rate used

to find the present value of those dividends.

Chapter 7. Mini Case

P 0 =

a. Describe briefly the legal rights and privileges of common stockholders.

Sam Strother and Shawna Tibbs are senior vice-presidents of the Mutual of Seattle. They are co-directors of the

company’s pension fund management division, with Strother having responsibility for fixed income securities

(primarily bonds) and Tibbs being responsible for equity investments. A major new client, theNorthwestern

Municipal Alliance, has requested that Mutual of Seattle present an investment seminar to the mayors of the

represented cities, and Strother and Tibbs, who will make the actual presentation, have asked you to help them.

To illustrate the common stock valuation process, Strother and Tibbs have asked you to analyze the Temp Force

Company, an employment agency that supplies word processor operators and computer programmers to businesses

with temporarily heavy workloads. You are to answer the following questions.

1. Common Stock represents ownership 2. Ownership implies control 3. Stockholders elect directors 4. Directors hire

management who attempt to maximize stock price.

57

58

59

60

61

62

63

64

65

66

67

68

69

70

A B C D E F G H I J

D 1

( r s – g )

In this stock valuation model, we first assume that the dividend and stock will grow forever at a constant growth rate.

Naturally, assuming a constant growth rate for the rest of eternity is a rather bold statement. However, considering

the implications of imperfect information, information asymmetry, and general uncertainty, perhaps our assumption

of constant growth is reasonable. It is reasonable to guess that a given will experience ups and downs throughout its

life. By assuming constant growth, we are trying to find the average of the good times and the bad times, and we

assume that we will see both scenarios over the firm’s life. In addition to assuming a constant growth rate, we will

be estimating a long-term required return for the stock. By assuming these variables are constant, our price equation

for common stock simplifies to the following expression:

In this equation, the long-run growth rate (g) can be approximated by multiplying the firm’s return on assets by the

retention ratio. Generally speaking, the long-run growth rate of a firm is likely to fall between 5 and 8 percent a

year.

P 0 =

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

A B C D E F G H I J

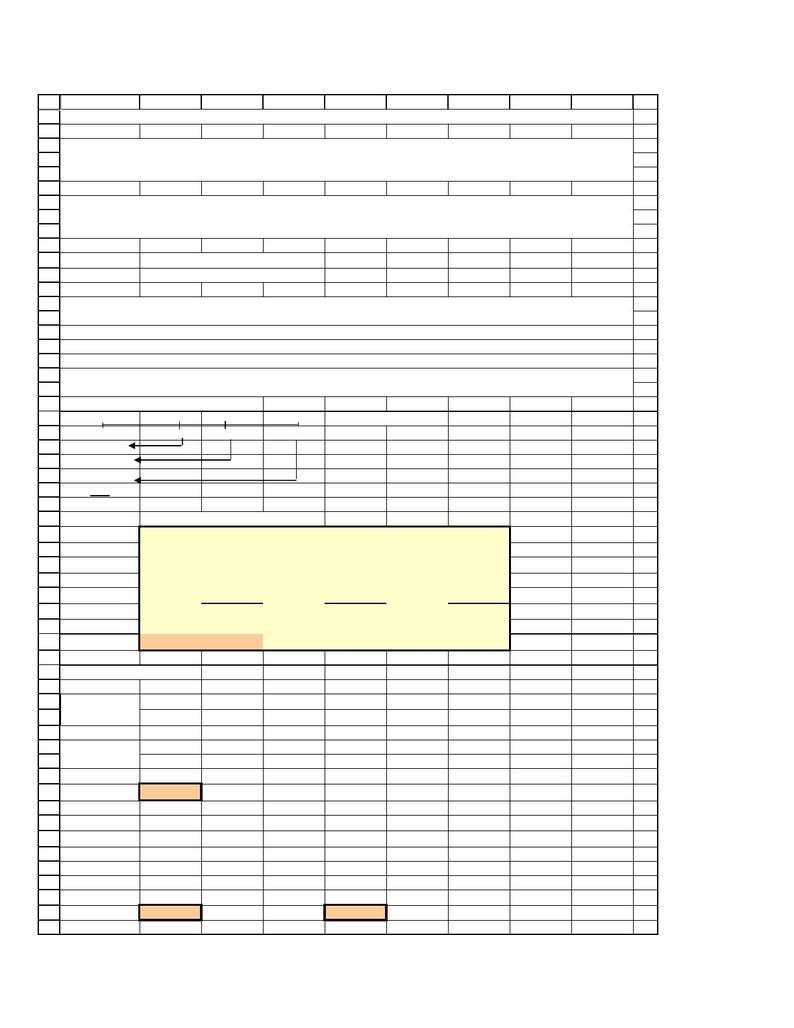

EXAMPLE: CONSTANT GROWTH

0 1 2 3 Continue to Infinty

Do =2.00 2.12 2.2472 2.3820

1.876

1.760

1.651

Etc.

??

Constant Growth Model:

D 0 = $2.00

g = 6%

r s =13.0%

D 1D 0 (1+g) $2.12

( r s – g ) ( r s – g ) 0.07

P 0 =$30.29

Stock Price 1 year from now

D 2

( r s – g )

2.2472

0.07

P1 = 32.10

Dividend Yield =

D1

C&G Yield =

P1-P0

P0P0

Dividend Yield =

2.12

C&G Yield =

$1.82

$30.29 $30.29

Dividend Yield =

7.00%

C&G Yield =

6.00%

(1.) What is the firm’s expected dividend stream over the next 3 years?

(2.) What is the firm’s current stock price?

(4.) What are the expected dividend yield, the capital gains yield, and the total return during the first year?

=

In this equation, the long-run growth rate (g) can be approximated by multiplying the firm’s return on assets by the

retention ratio. Generally speaking, the long-run growth rate of a firm is likely to fall between 5 and 8 percent a

year.

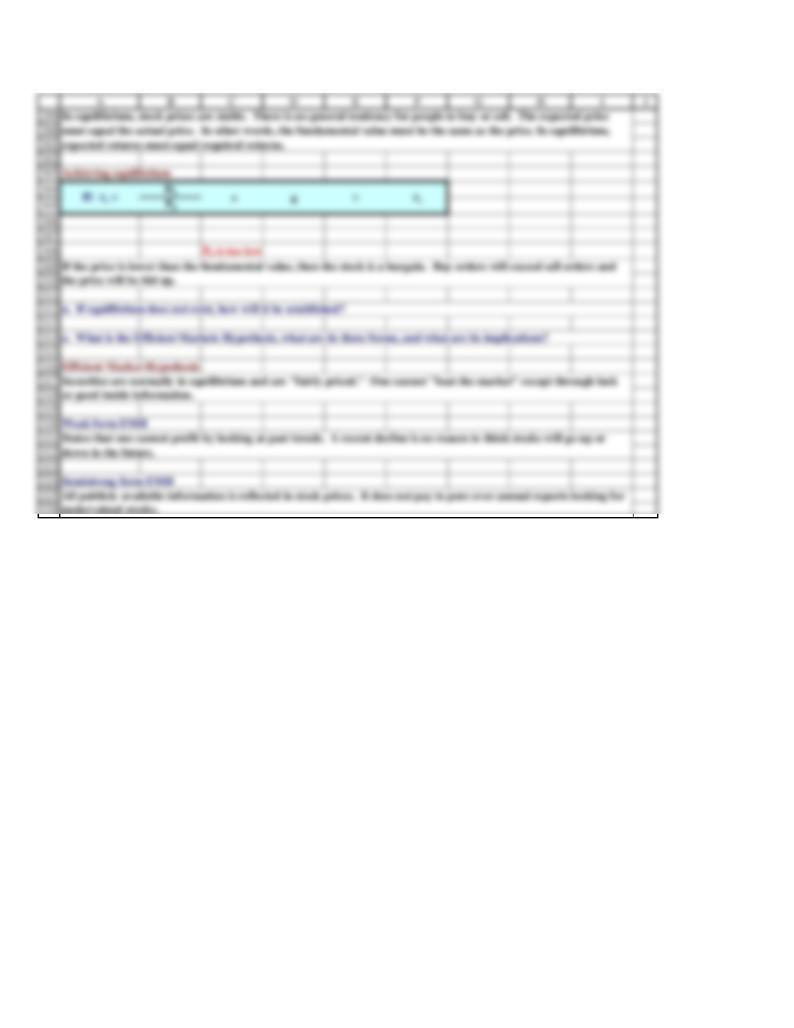

(c.) What happens if a company has a constant g which exceeds rs? Will many stocks have expected g > rs in the

short run (i.e., for the next few years)? In the long run (i.e., forever)? Answer: See Chapter 7 Mini Case Show

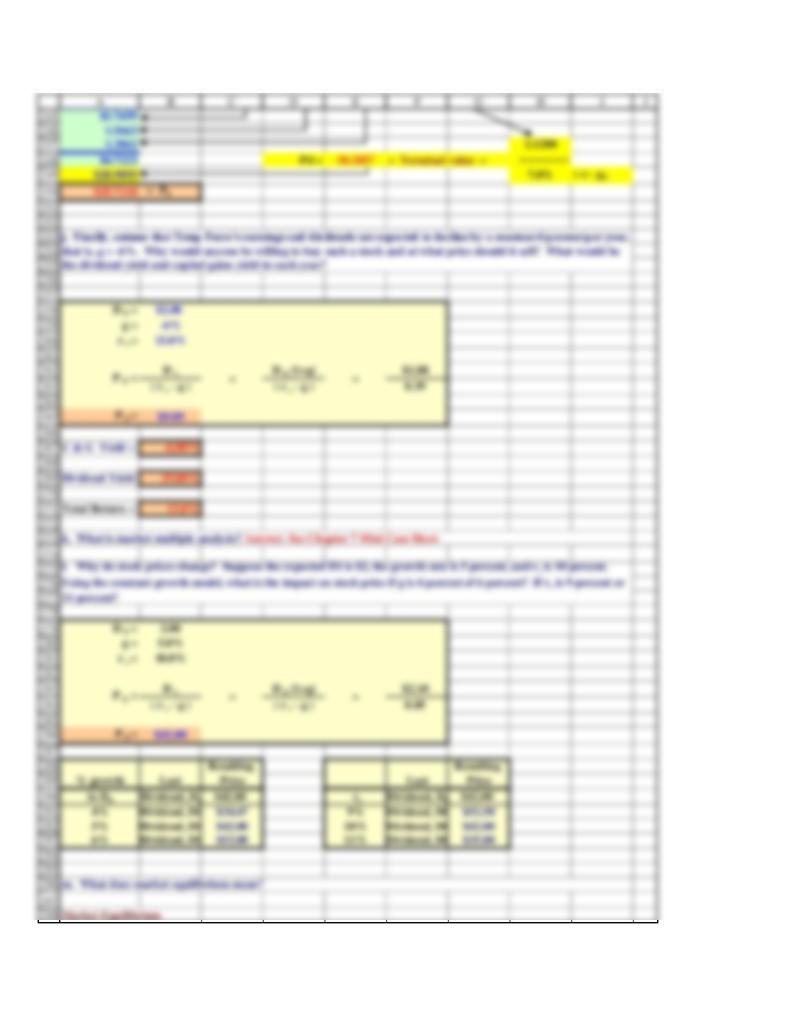

c. Assume that Temp Force has a beta coefficient of 1.2, that the risk-free rate (the yield on T-bonds) is 7 percent,

and that the market risk premium is 5 percent. What is the required rate of return on the firm’s stock?

d. Assume that Temp Force is a constant growth company whose last dividend (D0, which was paid yesterday) was

$2.00, and whose dividend is expected to grow indefinitely at a 6 percent rate.

(3.) What is the stock’s expected value 1 year from now?

P 1 =

P1 =

CAPM = rRF + b (rRF-rM)

7% + 1.2(5%) = 13%

P 0 =

=