entropy

Article

A Risk-Free Protection Index Model for Portfolio

Selection with Entropy Constraint under

an Uncertainty Framework

Jianwei Gao * and Huicheng Liu

School of Economics and Management, North China Electric Power University, Beijing 102206, China;

lhuicheng@ncepu.edu.cn

*Correspondence: gaojianwei111@sina.com; Tel.: +86-10-6177-3151

Academic Editor: Kevin H. Knuth

Received: 21 December 2016; Accepted: 15 February 2017; Published: 21 February 2017

Abstract:

This paper aims to develop a risk-free protection index model for portfolio selection based

on the uncertain theory. First, the returns of risk assets are assumed as uncertain variables and subject

to reputable experts’ evaluations. Second, under this assumption, combining with the risk-free interest

rate we define a risk-free protection index (RFPI), which can measure the protection degree when the

loss of risk assets happens. Third, note that the proportion entropy serves as a complementary means

to reduce the risk by the preset diversification requirement. We put forward a risk-free protection

index model with an entropy constraint under an uncertainty framework by applying the RFPI,

Huang’s risk index model (RIM), and mean-variance-entropy model (MVEM). Furthermore, to solve

our portfolio model, an algorithm is given to estimate the uncertain expected return and standard

deviation of different risk assets by applying the Delphi method. Finally, an example is provided to

show that the risk-free protection index model performs better than the traditional MVEM and RIM.

Keywords: portfolio selection; risk free protection index; entropy constrain; uncertain variable

1. Introduction

Portfolio selection focuses on the optimal allocation of one’s wealth to obtain maximum profitable

return under minimum risk control. Since Markowitz [

1

] first proposed the classic mean-variance

model (MVM), many researchers have suggested new methods or elements to get numerous variants

of the MVM for portfolio selection (e.g., minimum-variance model [

2

], mean-variance-skewness

model [

3

], mean-semivariance model [

4

]). Their research can be regarded as the extension to the

classic portfolio theory which is based on probability and statistics theory. The security returns are

all assumed to be random variables and their expected value and variance are obtained from the

sample of available historical data. Considering the complexity of the security market in the real world,

the non-uniqueness of randomness as a kind of uncertainty and the lack of enough historical data

to reflect the future performances of security returns in some real life cases, many scholars began to

regard security returns as fuzzy variables which rely on experienced experts’ evaluations instead of

historical data. Thus, fuzzy portfolio optimization theory is developed and has been mainly studied

based on following three methods: (i) Fuzzy set theory [

5

]; (ii) Possibility measure [

6

,

7

]; (iii) Credibility

measure [8–10].

However, paradoxes arise when fuzzy variables are utilized to describe the subjective estimations

of security returns in the above three methods [

11

]. For instance, if a security return is regarded as

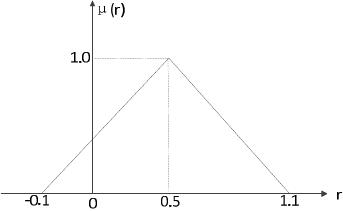

a fuzzy variable, then it can be characterized by a membership function. We suppose that a security

return is the triangular fuzzy variable

ξ= (−

0.1, 0.5, 1.1

)

(see Figure 1). Based on the membership

function, it is easy to obtain that

Pos{ξ=0.5}=

1 (or

Cr{ξ=0.5}=

0.5), which means that the

Entropy 2017,19, 80; doi:10.3390/e19020080 www.mdpi.com/journal/entropy

Entropy 2017,19, 80 2 of 12

security return is exactly 0.5 with belief degree 1 in possibility measure (or 0.5 in credibility measure).

However, this is unreasonable because the degree belief of exactly 0.5 should be almost zero.

In addition, we also get from the possibility theory that

Pos{ξ6=0.5}=Pos{ξ=0.5}=

1

(or

Cr{ξ6=0.5}=Cr{ξ=0.5}=

0.5. It implies that the two events of the return being exactly

0.5 and not being exactly 0.5 have the same degree belief both in possibility measure and credibility

measure, and they are equally likely to happen. This conclusion is contradictory and unacceptable to

our judgment.

Entropy 2017, 19, 80 2 of 12

membership function, it is easy to obtain that P s = 0.5} = 1ο{

ξ

(or Cr = 0.5} = 0.5{

ξ

),which means that

the security return is exactly 0.5 with belief degree 1 in possibility measure (or 0.5 in credibility

measure). However, this is unreasonable because the degree belief of exactly 0.5 should be almost

zero. In addition, we also get from the possibility theory that P s 0.5} = P s = 0.5} = 1ο{ξ≠ ο{ξ (or

Cr 0.5} = Cr = 0.5} = 0.5{

ξ

≠{

ξ

. It implies that the two events of the return being exactly 0.5 and not

being exactly 0.5 have the same degree belief both in possibility measure and credibility measure,

and they are equally likely to happen. This conclusion is contradictory and unacceptable to our

judgment.

Figure 1. Membership function of a security return

()

=0.1, 0.5, 1.1ξ −.

To deal with the above situation, Liu [12–15] proposed an uncertain measure and further

developed the uncertainty theory, which has been used in various areas (e.g., insurance, medical

care, environment and education) especially in the study of portfolio optimization [16–19]. Qin, et al.

[20] first studied mean-variance model in the uncertain environment. Zhu [21] considered a

continuous-time uncertain portfolio optimization problem. Liu and Qin [22] proposed a mean

semi-absolute deviation model for uncertain portfolio selection. Different from the above studies on

risk measurement, some scholars took the risk-free interest rate into consideration in the uncertain

portfolio optimization. Huang [23] first put forward a risk index model, Huang and Qiao [24]

modeled the multi-period problem, Huang and Ying [11] further considered the portfolio adjusting

problem. These studies proved that the above-mentioned paradoxes can be solved when the

uncertain variable is used to describe human imprecise estimations of security returns [11,24].

However, we find that these researchers usually focused on the weight of risk assets for

uncertain portfolio selection problem and ignored the protective screening function of risk-free

asset. As a result, the capital allocation is usually too centralized or decentralized. In this paper, we

study the portfolio selection problem under the framework of the uncertainty theory. In particular,

we extend the work of Huang, et al. [11,23,24] by proposing a risk-free protection index model with

entropy constraint for portfolio selection problem. Firstly, to introduce the protective screening

function of risk-free asset in guaranteeing the expected return of portfolio selection as the loss of risk

assets happens at a certain confidence level, we put forward a risk-free protection index (RFPI).

Secondly, considering that the Mean-variance selection framework without entropy constraint may

result in concentrative allocation, we further add proportion entropy constraint to the RFPI model to

meet the preset diversification requirement, which can prevent the concentrative allocation. Finally,

we propose a risk-free protection index model with proportion entropy constraint for portfolio

selection problem under uncertainty framework. The RFPI model can evaluate the protection made

by risk-free asset when the risk assets happen to lose at a certain confidence level, i.e., it can measure

the protective effect of risk-free asset on risk assets.

The rest of the paper is organized as follows: Section 2 introduces the knowledge about

uncertain variables and entropy constraint in finance. In Section 3, we first present RIM for uncertain

portfolio and the MVEM for diversified fuzzy portfolio. Then we further propose a risk-free

protection index model with entropy constraint in uncertainty environment and give an algorithm

to solve the portfolio selection model. Illustrative example is given in Section 4. Section 5 draws the

conclusion.

Figure 1. Membership function of a security return ξ=(−0.1, 0.5, 1.1).

To deal with the above situation, Liu [

12

–

15

] proposed an uncertain measure and further

developed the uncertainty theory, which has been used in various areas (e.g., insurance, medical

care, environment and education) especially in the study of portfolio optimization [

16

–

19

].

Q

in, et al. [20]

first studied mean-variance model in the uncertain environment. Zhu [

21

] considered

a continuous-time uncertain portfolio optimization problem. Liu and Qin [

22

] proposed a mean

semi-absolute deviation model for uncertain portfolio selection. Different from the above studies on

risk measurement, some scholars took the risk-free interest rate into consideration in the uncertain

portfolio optimization. Huang [

23

] first put forward a risk index model, Huang and Qiao [

24

] modeled

the multi-period problem, Huang and Ying [

11

] further considered the portfolio adjusting problem.

These studies proved that the above-mentioned paradoxes can be solved when the uncertain variable

is used to describe human imprecise estimations of security returns [11,24].

However, we find that these researchers usually focused on the weight of risk assets for uncertain

portfolio selection problem and ignored the protective screening function of risk-free asset. As a result,

the capital allocation is usually too centralized or decentralized. In this paper, we study the portfolio

selection problem under the framework of the uncertainty theory. In particular, we extend the work of

Huang, et al. [

11

,

23

,

24

] by proposing a risk-free protection index model with entropy constraint for

portfolio selection problem. Firstly, to introduce the protective screening function of risk-free asset in

guaranteeing the expected return of portfolio selection as the loss of risk assets happens at a certain

confidence level, we put forward a risk-free protection index (RFPI). Secondly, considering that the

Mean-variance selection framework without entropy constraint may result in concentrative allocation,

we further add proportion entropy constraint to the RFPI model to meet the preset diversification

requirement, which can prevent the concentrative allocation. Finally, we propose a risk-free protection

index model with proportion entropy constraint for portfolio selection problem under uncertainty

framework. The RFPI model can evaluate the protection made by risk-free asset when the risk assets

happen to lose at a certain confidence level, i.e., it can measure the protective effect of risk-free asset on

risk assets.

The rest of the paper is organized as follows: Section 2introduces the knowledge about uncertain

variables and entropy constraint in finance. In Section 3, we first present RIM for uncertain portfolio

and the MVEM for diversified fuzzy portfolio. Then we further propose a risk-free protection index

model with entropy constraint in uncertainty environment and give an algorithm to solve the portfolio

selection model. Illustrative example is given in Section 4. Section 5draws the conclusion.

Entropy 2017,19, 80 3 of 12

2. Knowledge about Uncertain Variables and the Entropy Constraint

To use uncertain variables to describe the security returns and consider the portfolio selection

problem with an entropy constraint, this section first introduces some necessary knowledge about

uncertain variables, and then presents an entropy constraint to finance.

2.1. The Expected Value, Variance and Distribution of an Uncertain Variable

Liu [

12

,

13

] presented an uncertain variable and an uncertain measure. We suppose that

Γ

is

a nonempty set,

ζ

is a

σ

-algebra over

Γ

, each element

Λ∈ζ

is an event, and

M{Λ}

is the occurrence

possibility measure of Λ. The function Mis called an uncertain measure if it satisfies four axioms:

(i)

Axiom 1: (Normality) M{Γ}=1;

(ii)

Axiom 2: (Self-duality) M{Λ}+M{Λc}=1;

(iii)

Axiom 3: (Countable subadditivity) M∞

∪

i=1

Λi≤

∞

∑

i=1

M{Λi}for every event {Λi};

(iv)

Axiom 4: (Product measure) Let

(Γk

,

ζk

,

Mk)

be uncertain spaces for

k=

1, 2,

···

,

n

, then product

uncertain measure is M=M1∧M2∧··· ∧ Mn.

Let

M

be an uncertain measure. The triplet

(Γ

,

ζ

,

M)

is called an uncertainty space. An uncertain

variable is a measurable function

ξ

:

(Γ,ζ,M)→ <

, i.e., the Borel set

B

:

{ξ∈B}={γ∈Γ|ξ(γ)∈B}

is an event. Then the uncertain distribution is defined as Φ(x) = M{ξ≤x},Φ:< → [0, 1].

The expected value is defined as

E[ξ]=Z∞

0M{ξ≥r}dr −Z0

−∞M{ξ≤r}dr. (1)

and its variance is defined as

V[ξ] = E[(ξ−E[ξ])2]. (2)

If ξand ηare independent uncertain variables with finite expected values, then it holds that

E[aξ+bη] = aE[ξ] + bE[η], for∀a,b∈ <. (3)

An uncertain variable ξis named as the normal uncertain variable if it satisfies

Φ(x)=1+expπ(e−x)

√3σ−1

,x∈ <, (4)

which is denoted by

N(e,σ)

with the mean value

e

and standard variance

σ

. The inverse function can

be written as [13]

Φ−1(α) = e+√3σ

πln α

1−α, (5)

where

α∈(

0, 1

)

and

Φ−1(α)

is the inverse function of

Φ

. Furthermore, we can calculate, for a linear

uncertain variable ξ~L(a,b)[23], the expected value is (a+b)/2 and variance is (b−a)2/12.

2.2. Entropy Constraint

Numerous portfolio selections operate problematically in practice [

25

]. Then, to avoid putting

excessive weights on only a few assets and reduce the impact of estimation error associated with

parameters of the moments of security returns, several diversity constraints have been introduced

and added to previous portfolio selection models. For example, Philippatos and Wilson [

26

] first used

entropy as a measurement of the uncertainty in portfolio selection. Usta and Kantar [

3

] presented

a mean-variance-skewness entropy measure for a multi-objective portfolio selection. Lin [

27

] put

forward a canonical form for diversity entropy constraint. Zhou et al. [

28

] introduced the application

Entropy 2017,19, 80 4 of 12

of entropy in finance. Zhou et al. [

29

] established a mean-variance hybrid-entropy model. Huang [

30

]

developed an entropy method to solve the diversified fuzzy portfolio problem. These studies imply

that entropy is a more general measure of risk than variance and it can be calculated from non-metric

data for it has nothing to do with the assumption of symmetric probability distributions [

26

]. This paper

will introduce Shannon’s entropy [3] in the portfolio selection constraints as follows.

Suppose that investment proportion in the i-th securities is denoted by

xi

(

xi≥

0,

for i=1, 2, ··· ,n). Then

H(x)=−

n

∑

i=1

xiln xi(6)

is named as the proportion entropy. Furthermore, it is obvious to see that

(Hmax =ln n,i f xi≡1

n,f or i =1, 2, ···n,

Hmin =0, i f xi=1or xj=0, j6=i,f or j =1, 2, ···n,

and the larger the absolute value (the greater the value of proportion entropy), the more diversely the

assets can be allocated to the alternative securities.

3. Risk-Free Protection Index Model with Entropy for an Uncertain Portfolio

In this section, we present the RIM for an uncertain portfolio and the MVEM for a diversified

fuzzy portfolio in Section 3.1. Furthermore, we propose a risk-free protection index model with

entropy constraint in uncertainty environment in Section 3.2 and give an algorithm to solve the model

in Section 3.3.

Figure 3. The relationship between RFPI and the expected return rates.

Figure 4. The relationship between RFPI and VaRU.

possible correlation effect among i-th securities in today’s highly related markets and the return

rates of i-th securities don’t completely subject to normal uncertain distribution. Thus, we can take

both the co-variance of a pair of assets in the model and abnormal uncertain distribution or other

kinds of distributions into account in the future research. In addition, we can extend our portfolio

selection problem to multi-objective portfolio problems and also add the crisp forms of the proposed

model in the further study.

Acknowledgments: The author acknowledges the support from Natural Science Foundation of China under

Grant Nos. 71271083, 71671064, and Humanities and Social Science Fund Major Project of Beijing under Grant

No. 15ZDA19 and Fundamental Research Funds for Central Universities under Grant No. 2016XS70.

Author Contributions: Jianwei Gao and Huicheng Liu conceived and designed the experiments. Huicheng Liu

performed the experiments and contributed analysis tools. Jianwei Gao wrote the paper.

Conflicts of Interest: The authors declare no conflict of interest.

References

1. Markowitz, H. Portfolio selection. J. Finance 1952, 7, 77–91.

2. Huang, X.X. Portfolio Analysis: From Probabilistic to Credibilistic and Uncertain Approaches; Springer-Verlag:

Berlin/Heidelberg, Germany, 2010.

3. Usta, I.; Kantar, Y.M. Mean-variance-skewness-entropy measures: A multi-objective approach for

portfolio selection. Entropy 2011, 13, 117–133.

4. Grootveld, H.; Hallerbach, W. Variance vs. downside risk: Is there really that much difference? Eur. J.

Oper. Res. 1999, 114, 304–319.