Performance Evaluation

Professor Alexander Barinov

School of Business Administration

University of California Riverside

MGT 295F Empirical Methods

Alexander Barinov (SoBA, UCR) Performance Evaluation MGT 295F Empirical Methods 1 / 37

Outline

1Performance Measures

2Performance Evaluation

3Alpha and Expense Ratio

4Example

Alexander Barinov (SoBA, UCR) Performance Evaluation MGT 295F Empirical Methods 2 / 37

Performance Measures

Appraisal Ratio

If you found a security with positive alpha, you

have to choose between outperformance and

diversification

An analogue of the Sharpe ratio, called

appraisal ratio, may help you in finding the right

trade-off

Suppose you have estimated the market

model/CAPM and have the alpha and the

volatility of the residuals

RFund −RF =αFund +βFund (RM−RF ) +

Appraisal ratio (the more the better) is α

σ

Alexander Barinov (SoBA, UCR) Performance Evaluation MGT 295F Empirical Methods 3 / 37

Performance Measures

How to Calculate Appraisal Ratio

We need to run the market model and take from there the

alpha and the “standard error” for the model

Consider Fidelity Freedom 2030 (alpha 5 bp per month,

standard deviation of the CAPM residuals 67 bp per month)

Consider also T. Rowe Price New Asia (alpha 1.17% per

month, standard deviation of the CAPM residuals 4.98% per

month)

Appraisal ratio is 0.05%

0.67%=0.075 for Freedom, 1.17%

4.98%=0.24

for New Asia

If you accept 1% extra idiosyncratic volatility, with Freedom

you will get extra 7.5 bp per month, with New Asia you will get

extra 24 bp per month – New Asia is better

Alexander Barinov (SoBA, UCR) Performance Evaluation MGT 295F Empirical Methods 4 / 37

Performance Measures

Zero-Investment Portfolios

Why we run RF−RF =α+β·(RM−RF )for a

fund, but HML =α+β·(RM−RF )(without −RF

on the left-hand side for the value minus growth

strategy?

We actually run H−RF =α+β·(E(RM)−RF )for

value and L−RF =α+β·(E(RM)−RF )for

growth and then subtract one from the other

αand βfrom HML =α+β·(RM−RF )are the

difference in αand βbetween value and growth

Same thing with other performance measures if

applied to zero-investment strategies: do not

subtract the risk-free rate or assume it is zero

Alexander Barinov (SoBA, UCR) Performance Evaluation MGT 295F Empirical Methods 5 / 37

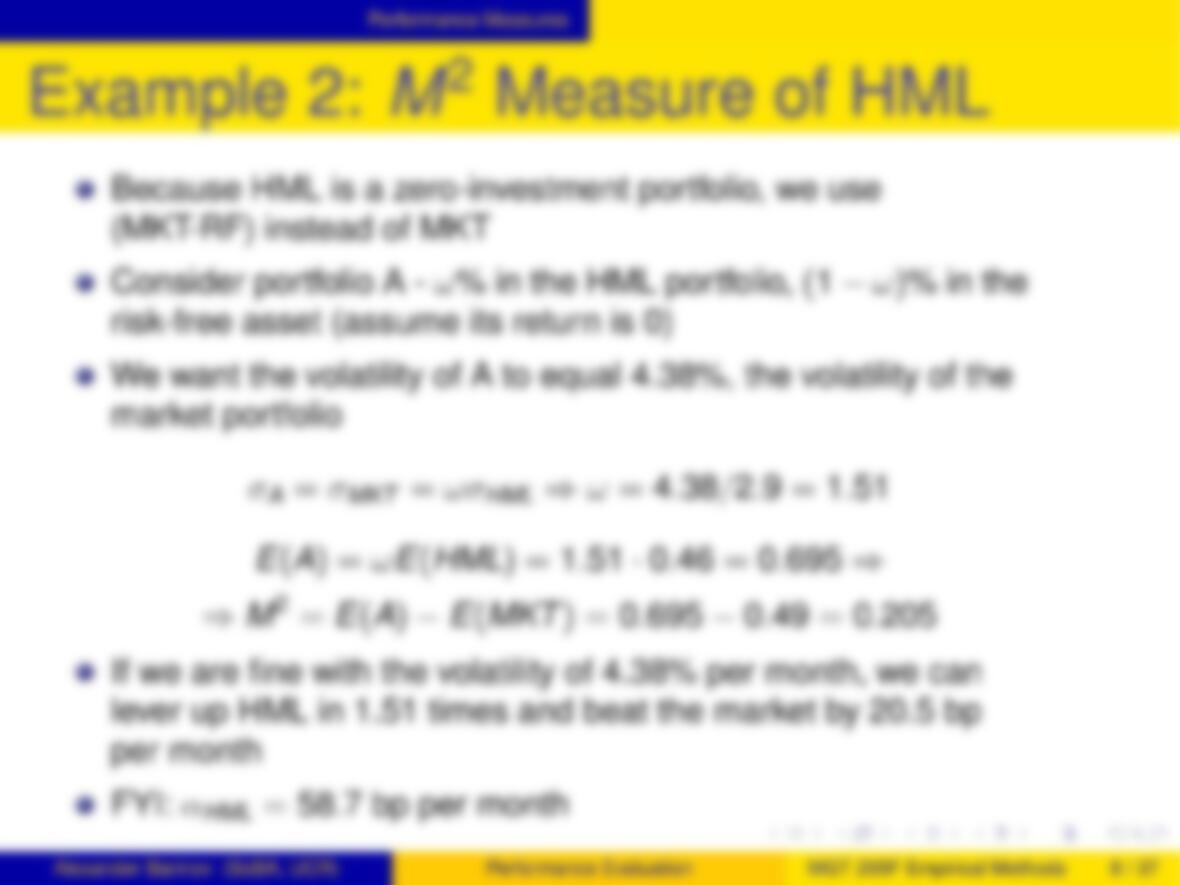

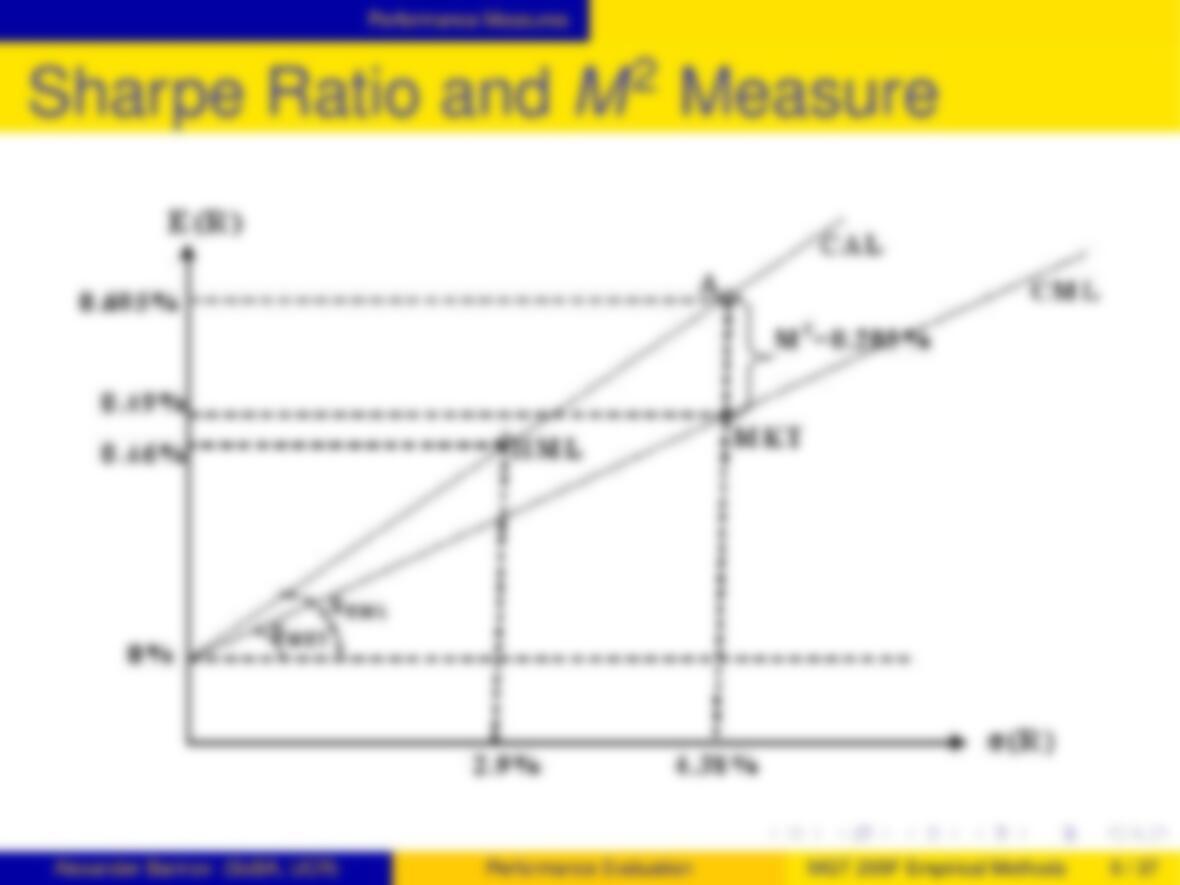

Performance Measures

Example 1: Sharpe Ratio of HML

Sample: August 1963 – December 2006

Market portfolio has average excess return

0.49% per month, standard deviation 4.38%

HML portfolio has average return 0.46% per

month, standard deviation 2.9%

SMKT =RMKT −RF

σMKT

=0.49

4.38 =0.11

SHML =RHML

σHML

=0.46

2.9=0.16

HML beats the market on the reward-to-risk

ratio by 42% – HML is a better investment

Alexander Barinov (SoBA, UCR) Performance Evaluation MGT 295F Empirical Methods 6 / 37

Performance Measures

Example 1: Sharpe Ratio of HML

Put it in words: “With MKT, you get extra 11 bp per

month if you increase the standard deviation of your

position by 1% per month; with HML you will get extra

16 bp per month for the same thing”

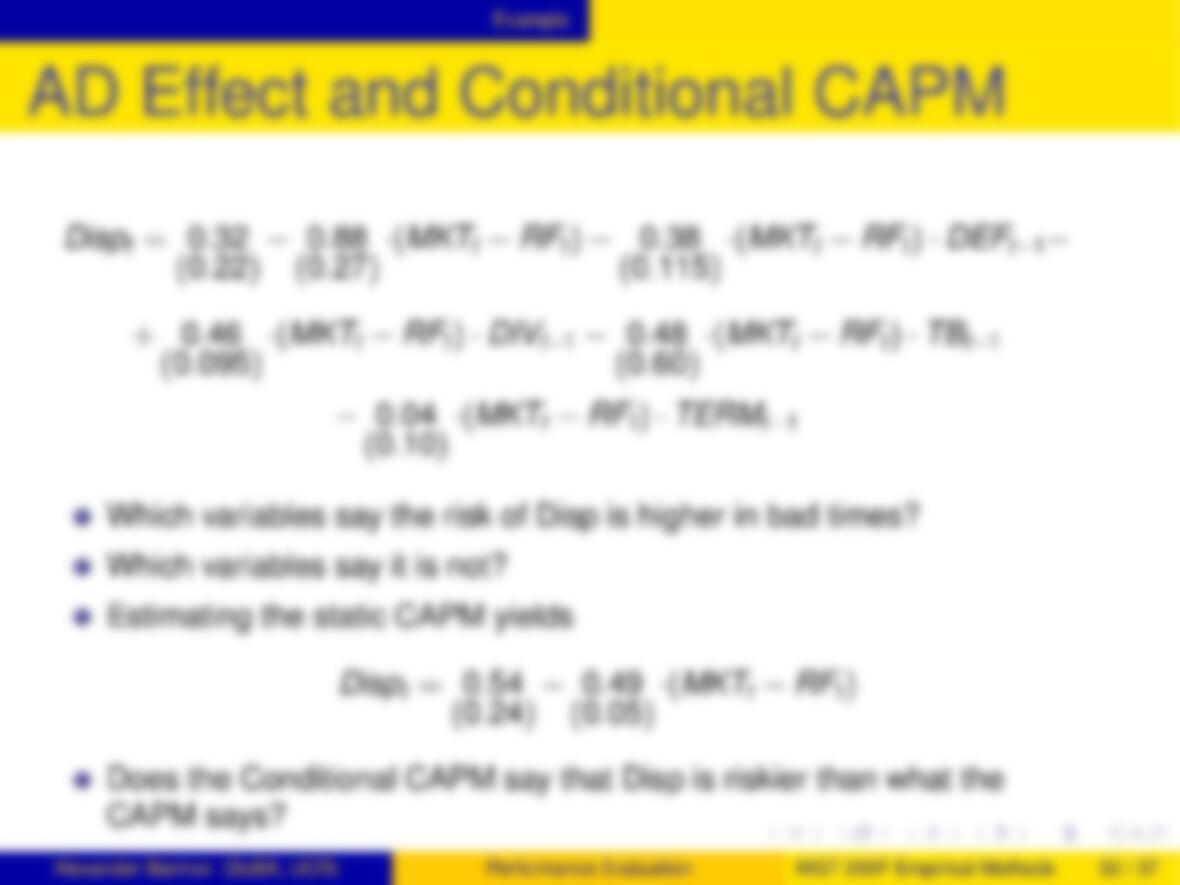

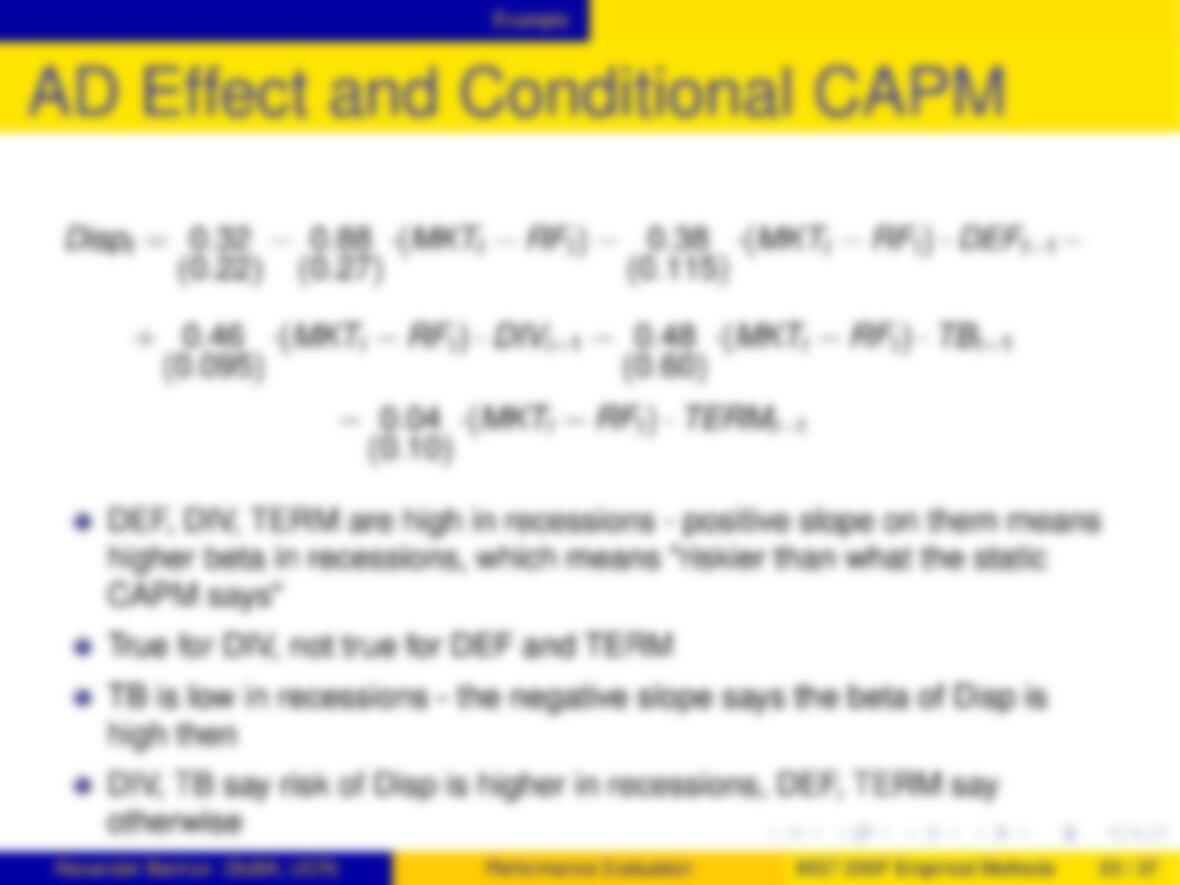

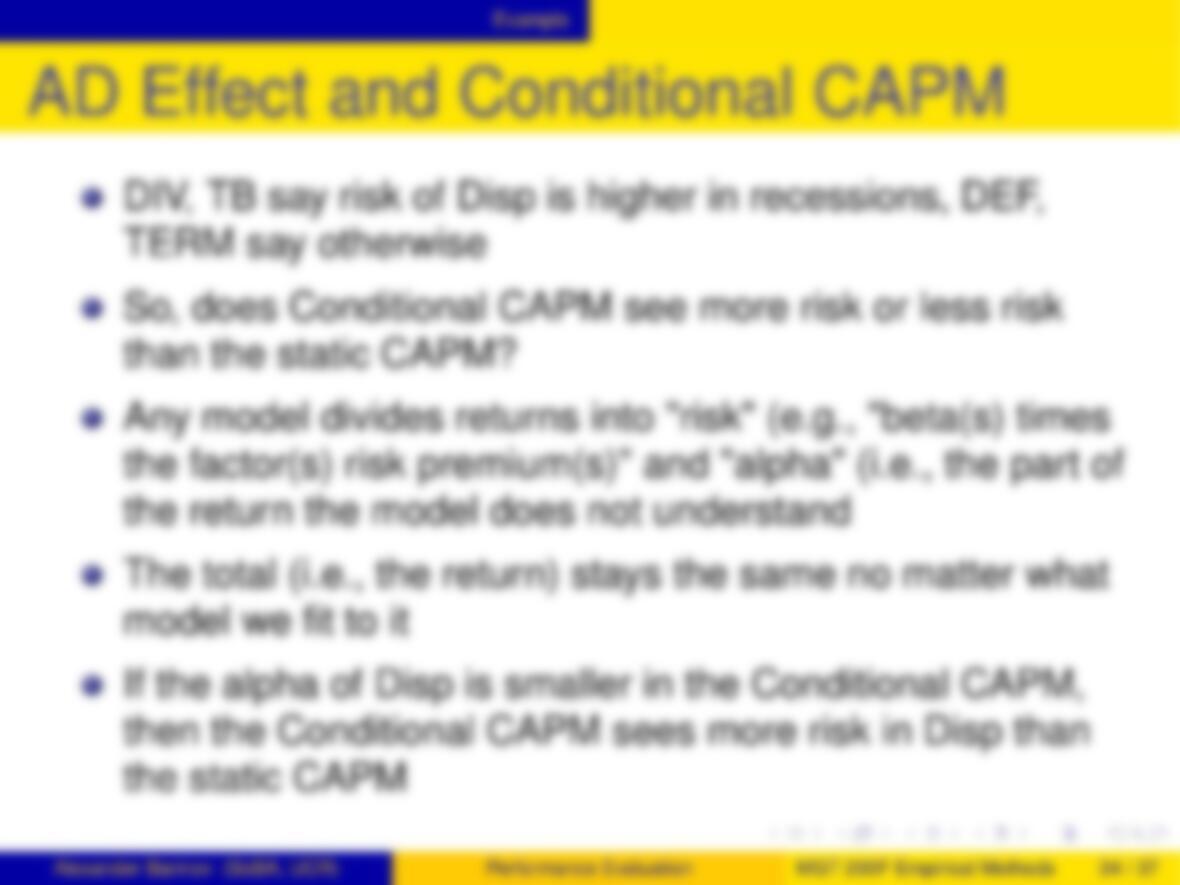

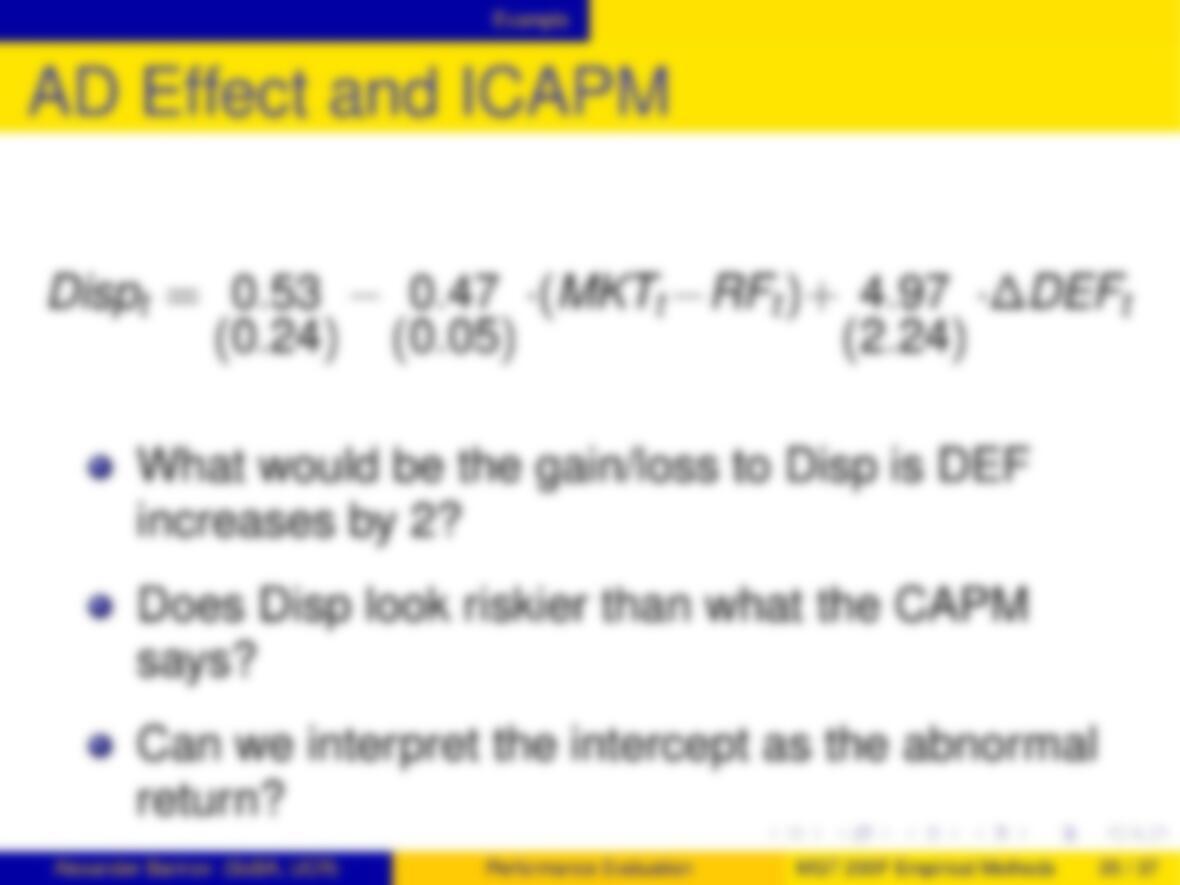

You do not need to subtract RF from HML, because