Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 18 INTERNATIONAL CAPITAL BUDGETING

ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

QUESTIONS

1. Why is capital budgeting analysis so important to the firm?

Answer: The fundamental goal of the financial manager is to maximize shareholder wealth.

2. What is the intuition behind the NPV capital budgeting framework?

Answer: The NPV framework is a discounted cash flow technique. The methodology compares

3. Discuss what is meant by the incremental cash flows of a capital project.

Answer: Incremental cash flows are denoted by the change in total firm cash inflows and cash

4. Discuss the nature of the equation sequence, Equation 18.2a to 18.2f.

Answer: The equation sequence is a presentation of incremental annual cash flows associated

with a capital expenditure. Equation 18.2a presents the most detailed expression for calculating

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

actually available for shareholders. Equation 18.2c cancels out the after-tax interest term in

18.2a, yielding a simpler formula. Equation 18.2d shows that the first term in 18.2c is generally

called after-tax net operating income. Equation 18.2e yields yet a computationally simpler

formula by combining the depreciation terms of 18.2c. Equation 18.2f shows that the first term

in 18.2e is generally referred to as after-tax operating cash flow.

5. What makes the APV capital budgeting framework useful for analyzing foreign capital

expenditures?

Answer: The APV framework is a value-additivity technique. Because international projects

6. Relate the concept of lost sales to the definition of incremental cash flow.

Answer: When a new capital project is undertaken it may compete with an existing project(s),

7. What problems can enter into the capital budgeting analysis if project debt is evaluated

instead of the borrowing capacity created by the project?

Answer: If project debt is greater (less) than the borrowing capacity created by the capital

8. What is the nature of a concessionary loan and how is it handled in the APV model?

Answer: A concessionary loan is a loan offered by a governmental body at below the normal

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

similarly converted concessionary loan payments discounted at the MNC’s normal domestic

borrowing rate. The loan payments will yield a present value less than the face amount of the

concessionary loan when they are discounted at the higher normal rate. This difference

represents a subsidy the host country is willing to extend to the MNC if the investment is made.

The benefit to the MNC of the concessionary loan is handled in the APV model via a separate

term.

9. What is the intuition of discounting the various cash flows in the APV model at specific

discount rates?

Answer: The APV model is a value-additivity technique where total value is determined by the

10. In the Modigliani-Miller equation, why is the market value of the levered firm greater than

the market value of an equivalent unlevered firm?

Answer: The levered firm has a greater market value because less money is taken from the

11. Discuss the difference between performing the capital budgeting analysis from the parent

firm’s perspective as opposed to the subsidiary’s perspective.

Answer: The goal of the financial manager of the parent firm is to maximize its shareholders’

wealth. A capital project of a subsidiary of the parent may have a positive NPV (or APV) from

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

the parent and the parent’s stockholders.

12. Define the concept of a real option. Discuss some of the various real options a firm can be

confronted with when investing in real projects.

Answer: A positive APV project is accepted under the assumption that all future operating

decisions will be optimal. The firm’s management does not know at the inception date of a

13. Discuss the circumstances under which the capital expenditure of a foreign subsidiary

might have a positive NPV in local currency terms but be unprofitable from the parent firm’s

perspective.

Answer: The project NPV might be negative from the parent firm’s perspective when it is

positive in local currency terms if all foreign cash flows cannot be legally repatriated to the

PROBLEMS

1. The Alpha Company plans to establish a subsidiary in Hungary to manufacture and sell

fashion wristwatches. Alpha has total assets of $70 million, of which $45 million is equity

financed. The remainder is financed with debt. Alpha considered its current capital structure

optimal. The construction cost of the Hungarian facility in forints is estimated at

HUF2,400,000,000, of which HUF1,800,000,and 000 is to be financed at a below-market

borrowing rate arranged by the Hungarian government. Alpha wonders what amount of debt it

should use in calculating the tax shields on interest payments in its capital budgeting analysis.

Can you offer assistance?

Solution: The Alpha Company has an optimal debt ratio of .357 (= $25 million debt/$70 million

2. The current spot exchange rate is HUF250/$1.00. Long-run inflation in Hungary is estimated

at 10 percent annually and 3 percent in the United States. If PPP is expected to hold between

the two countries, what spot exchange should one forecast five years into the future?

3. The Beta Corporation has an optimal debt ratio of 40 percent. Its cost of equity capital is 12

percent and its before-tax borrowing rate is 8 percent. Given a marginal tax rate of 35 percent,

calculate (a) the weighted-average cost of capital, and (b) the cost of equity for an equivalent

all-equity financed firm.

4. Zeda, Inc., a U.S. MNC, is considering making a fixed direct investment in Denmark. The

Danish government has offered Zeda a concessionary loan of DKK15,000,000 at a rate of 4

percent per annum. The normal borrowing rate is 6 percent in dollars and 5.5 percent in Danish

krone. The loan schedule calls for the principal to be repaid in three equal annual installments.

What is the present value of the benefit of the concessionary loan? The current spot rate is

DKK5.60/$1.00 and the expected inflation rate is 3% in the U.S. and 2.5% in Denmark.

Solution:

Year

(t)

St

(a)

Principal

Payment

(b)

DKK

It

(c)

DKK

StLPt

(b + c)/(a)

StLPt/(1 + id)t

1

5.57

5,000,000

600,000

1,005,386

948,477

2

5.55

5,000,000

400,000

972,973

865,943

3

5.52

5,000,000

200,000

942,029

790,946

15,000,000

2,605,366

The dollar value of the concessionary loan is $2,678,574 = DKK15,000,000 ÷ 5.60. The dollar

present value of the concessionary loan payments is $2,605,366. Therefore, the present value

of the benefit of the concessionary loan is $73,208 = $2,678,574 – 2,605,366.

5. Delta Company, a U.S. MNC, is contemplating making a foreign capital expenditure in South

Africa. The initial cost of the project is ZAR10,000. The annual cash flows over the five year

economic life of the project in ZAR are estimated to be 3,000, 4,000, 5,000, 6000, and 7,000.

The parent firm’s cost of capital in dollars is 9.5 percent. Long-run inflation is forecasted to be 3

percent per annum in the U.S. and 7 percent in South Africa. The current spot foreign

exchange rate is ZAR/USD = 3.75. Determine the NPV for the project in USD by:

a. Calculating the NPV in ZAR using the ZAR equivalent cost of capital according to the Fisher

Effect and then converting to USD at the current spot rate.

b. Converting all cash flows from ZAR to USD at Purchasing Power Parity forecasted exchange

rates and then calculating the NPV at the dollar cost of capital.

Solution: The PPP forecasted ZAR/USD exchange rates are:

The two dollar NPVs are identical as they always will be under the assumption that both PPP

and the Fisher Effect hold. Note, that both parity conditions incorporate relative differences in

inflation.

c. What is the NPV in dollars if the actual pattern of ZAR/USD exchange rates is: S(0) = 3.75,

S(1) = 5.7, S(2) = 6.7, S(3) = 7.2, S(4) = 7.7, and S(5) = 8.2?

Solution:

The NPV is negative because actual exchange rates did not evolve as forecasted by PPP.

Consequently, actual NPV and forecasted NPV may be different.

6. Suppose that in the illustrated mini case in the chapter the APV for Centralia had been -

$60,000. How large would the after-tax terminal value of the project need to be before the APV

would be positive and Centralia would accept the project?

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

calculated as follows. Set

STTVT/(1+Kud)T = $60,000. This implies

TVT = ($60,000/ST)(1+Kud)T

= ($60,000/.7261)(1.11)8

= €190,431.

7. With regards to the Centralia illustrated mini case in the chapter, how would the APV change

if:

a. The forecast of

d and/or

f are incorrect?

Answer: A larger or smaller

d will not have any effect because a change will affect the

b. Deprecation cash flows are discounted at Kud instead of id?

c. The host country did not provide the concessionary loan?

MINI CASE: DORCHESTER, LTD.

Dorchester Ltd., is an old-line confectioner specializing in high-quality chocolates. Through

its facilities in the United Kingdom, Dorchester manufactures candies that it sells throughout

Western Europe and North America (United States and Canada). With its current

manufacturing facilities, Dorchester has been unable to supply the U.S. market with more than

225,000 pounds of candy per year. This supply has allowed its sales affiliate, located in Boston,

to be able to penetrate the U.S. market no farther west than St. Louis and only as far south as

Atlanta. Dorchester believes that a separate manufacturing facility located in the United States

would allow it to supply the entire U.S. market and Canada (which presently accounts for 65,000

pounds per year). Dorchester currently estimates initial demand in the North American market

at 390,000 pounds, with growth at a 5 percent annual rate. A separate manufacturing facility

would, obviously, free up the amount currently shipped to the United States and Canada. But

Dorchester believes that this is only a short-run problem. They believe the economic

development taking place in Eastern Europe will allow it to sell there the full amount presently

shipped to North America within a period of five years.

Dorchester presently realizes £3.00 per pound on its North American exports. Once the

U.S. manufacturing facility is operating, Dorchester expects that it will be able to initially price its

product at $7.70 per pound. This price would represent an operating profit of $4.40 per pound.

Both sales price and operating costs are expected to keep track with the U.S. price level; U.S.

inflation is forecast at a rate of 3 percent for the next several years. In the U.K., long-run

inflation is expected to be in the 4 to 5 percent range, depending on which economic service

one follows. The current spot exchange rate is $1.50/£1.00. Dorchester explicitly believes in

PPP as the best means to forecast future exchange rates.

The manufacturing facility is expected to cost $7,000,000. Dorchester plans to finance this

amount by a combination of equity capital and debt. The plant will increase Dorchester’s

borrowing capacity by £2,000,000, and it plans to borrow only that amount. The local

community in which Dorchester has decided to build will provide $1,500,000 of debt financing

for a period of seven years at 7.75 percent. The principal is to be repaid in equal installments

over the life of the loan. At this point, Dorchester is uncertain whether to raise the remaining

debt it desires through a domestic bond issue or a Eurodollar bond issue. It believes it can

borrow pounds sterling at 10.75 percent per annum and dollars at 9.5 percent. Dorchester

estimates its all-equity cost of capital to be 15 percent.

The U.S. Internal Revenue Service will allow Dorchester to depreciate the new facility over a

seven-year period. After that time the confectionery equipment, which accounts for the bulk of

the investment, is expected to have substantial market value.

Dorchester does not expect to receive any special tax concessions. Further, because the

corporate tax rates in the two countries are the same--35 percent in the U.K. and in the United

States--transfer pricing strategies are ruled out.

Should Dorchester build the new manufacturing plant in the United States?

Suggested Solution to Dorchester Ltd.

Summary of Key Information

The before-tax nominal contribution margin per unit at t=1 is $4.40(1.03)t-1.

It is assumed that Dorchester will be able to sell one-fifth of the 290,000 pounds of candy it

presently sells to North America in Eastern Europe the first year the new manufacturing facility

is in operation; two-fifths the second year; etc.; and all 290,000 pounds beginning the fifth year.

The contribution margin on lost sales per pound in year t equals £3.00(1.045)t.

Terminal value will initially be assumed to equal zero.

The marginal tax rate,

, is the U.K. (or U.S.) rate of 35%.

Dorchester will borrow $1,500,000 at the concessionary loan rate of 7.75% per annum.

Optimally, Dorchester should borrow the remaining funds it needs, £1,000,000, in pounds

sterling because according to the Fisher equation, the real rate is less for borrowing pounds

sterling than it is for borrowing dollars:

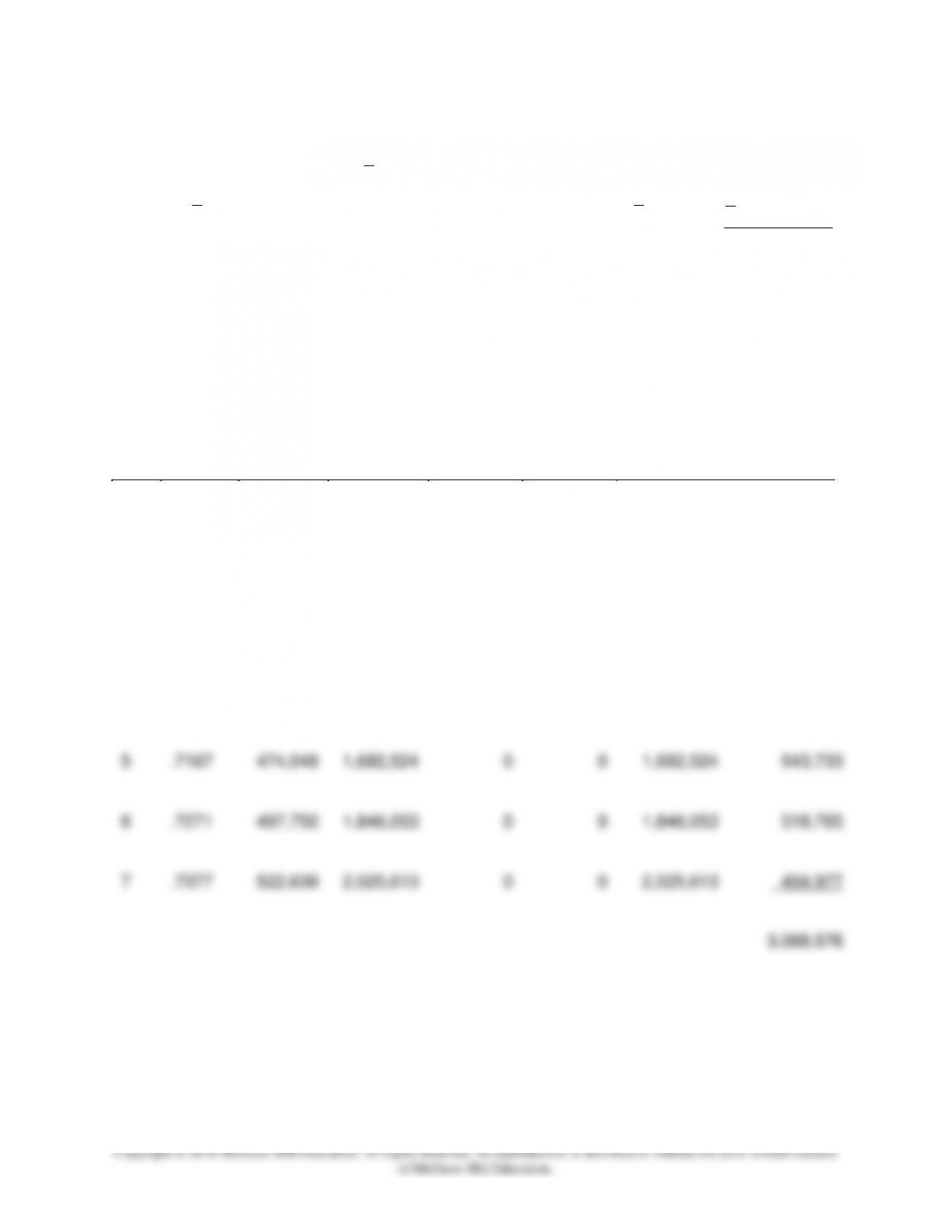

Calculation of the Present Value of the After-Tax Operating Cash Flows

Year

(t)

t

S

Quantity

t

S

x

Quantity

x $4.40

x (1.03)t-1

Quantity

Lost

Sales

Quantity

Lost

Sales

x £3.00

x (1.045)t

tt

SOCF

)

K

+(

)-(

OCF

St

ud

t

t

1

1

(a)

£

(b)

£

(a + b)

£

£

1

.6764

390,000

1,160,702

(232,000)

(727,320)

433,382

244,955

2

.6863

409,500

1,273,673

(174,000)

(570,037)

703,636

345,832

3

.6963

429,975

1,397,548

(116,000)

(397,126)

1,000,422

427,566

4

.7064

451,474

1,533,373

(58,000)

(207,498)

1,325,875

492,748

5

.7167

474,048

1,682,524

0

0

1,682,524

543,733

6

.7271

497,750

1,846,053

0

0

1,846,053

518,765

7

.7377

522,638

2,025,613

0

0

2,025,613

494,977

3,068,576

Calculation of the Present Value of the Depreciation Tax Shields

Year

(t)

t

S

Dt

)

i

+(

D

St

d

t

t

1

$

£

1

.6764

1,000,000

213,761

2

.6863

1,000,000

195,837

3

.6963

1,000,000

179,404

4

.7064

1,000,000

164,340

5

.7167

1,000,000

150,552

6

.7271

1,000,000

137,911

7

.7377

1,000,000

126,340

1,168,146

Calculation of the Present Value of the Concessionary Loan Payments

Year

(t)

t

S

(a)

Principal

Payment

(b)

$

It

(c)

$

tt

SLP

(a) x (b + c)

£

tt

dt

SLP

(1+i)

£

1

.6764

214,286

116,250

223,574

201,873

2

.6863

214,286

99,643

215,449

175,654

3

.6963

214,286

83,036

207,025

152,402

4

.7064

214,286

66,429

198,297

131,808

5

.7167

214,286

49,821

189,286

113,605

6

.7271

214,286

33,214

179,957

97,523

7

.7377

214,286

16,607

170,330

83,346

1,500,000

956,211

)

i

+(

d

1=t

Calculation of the Present Value of the Interest Tax Shields

from the $1,500,000 Concessionary Loan

Year

(t)

t

S

(a)

It

(b)

$

tt

SI

(a x b x

)

£

tt

dt

SI

(1+i)

£

1

.6764

116,250

27,521

24,850

2

.6863

99,643

23,935

19,514

3

.6963

83,036

20,236

14,897

4

.7064

66,429

16,424

10,917

5

.7167

49,821

12,497

7,501

6

.7271

33,214

8,452

4,581

7

.7377

16,607

4,288

2,098

84,357

Calculation of the Present Value of the Interest Tax Shields from the £1,000,000 Bond Issue

Year

(t)

Outstanding

Loan

Balance

Principal

Payment

Interest

Payment

)

i

+(

It

d

t

1

£

£

£

£

1

1,000,000

0

107,500

33,973

2

1,000,000

0

107,500

30,675

3

1,000,000

0

107,500

27,698

4

1,000,000

0

107,500

25,009

5

1,000,000

0

107,500

22,582

6

1,000,000

0

107,500

20,390

7

1,000,000

1,000,000

107,500

18,411

178,738

Without considering the terminal value of the project, the APV of the project is negative:

Dorchester should not go ahead with its plans to build a manufacturing plant in the U.S. unless

the terminal value is likely to be large enough to yield a positive APV. The terminal value of the

Since the terminal value is expected to be substantial, and the initial cost of the project is

$7,000,000, it appears likely that the terminal value will be sufficient to yield a positive APV.

Thus, Dorchester should go ahead with its plans to build a manufacturing plant in the U.S.

MINI-CASE: STRIK-IT-RICH GOLD MINING COMPANY

The Strik-it-Rich Gold Mining Company is contemplating expanding its operations. To do so it

will need to purchase land that its geologists believe is rich in gold. Strik-it-Rich’s management

believes that the expansion will allow it to mine and sell an additional 2,000 troy ounces of gold

per year. The expansion, including the cost of the land, will cost $2,500,000. The current price

of gold bullion is $1,400 per ounce and one-year gold futures are trading at $1,484 =

$1,400(1.06). Extraction costs are $1,050 per ounce. The firm’s cost of capital is 10%. At the

current price of gold, the expansion appears profitable: NPV = ($1,400 – 1,050) x 2,000/.10 -

$2,500,000 = $4,500,000. Strik-it-Rich’s management is, however, concerned with the

possibility that large sales of gold reserves by Russia and the United Kingdom will drive the

price of gold down to $1,100 for the foreseeable future. On the other hand, management

believes there is some possibility that the world will soon return to a gold reserve international

monetary system. In the latter event, the price of gold would increase to at least $1,600 per

ounce. The course of the future price of gold bullion should become clear within a year. Strik-it-

Rich can postpone the expansion for a year by buying a purchase option on the land for

$250,000. What should Strik-it-Rich’s management do?

Suggested Solution to Strik-it-Rich Gold Mining Company

There is considerable risk in expanding operations at the present time, even though the NPV

a relatively small amount to have the opportunity to postpone the decision until additional

information is learned. Obviously, Strik-it-Rich’s management will only invest if the NPV is

positive. The risk-neutral probability of gold increasing to $1,600 per ounce is:

Since this amount is substantially in excess of the $250,000 cost of the purchase option on the

land, Strik-it-Rich’s management should definitely take advantage of the timing option it is

confronted with to wait and see what the price of gold is in one year before it makes a decision

to expand operations.