Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 7

Long-Term Assets

REVIEW QUESTIONS

Question 7-1 (LO 7-1)

WorldCom recorded assets on the balance sheet that should have been recorded as expenses on

Question 7-2 (LO 7-1)

The two major categories for long-term assets are (1) property, plant, and equipment and (2)

intangible assets. Property, plant, and equipment include land, land improvements, buildings,

Question 7-3 (LO 7-1)

We initially record a long-term asset at its cost plus all expenditures necessary to get the asset

Question 7-4 (LO 7-1)

Recording an expense incorrectly as an asset will overstate net income on the income statement.

If University Hero initially records an expense incorrectly as an asset, expenses are understated or

Question 7-5 (LO 7-1)

Costs Little King might incur to make the land ready for its intended use include the purchase

price plus closing costs such as fees for the attorney, real estate agent commissions, title, title search,

7-2 Financial Accounting, 5e

Answers to Review Questions (continued)

Question 7-6 (LO 7-1)

We don’t depreciate land because its service life never ends. Land improvements are additional

Question 7-7 (LO 7-1)

Costs we might incur to get equipment ready for use include sales tax, shipping, delivery,

Question 7-8 (LO 7-1)

We report natural resources on the balance sheet as part of property, plant, and equipment.

Examples of natural resources include oil, natural gas, timber, and salt.

Question 7-9 (LO 7-2)

We value purchased intangible assets at their original cost plus all other costs, such as legal and

Question 7-10 (LO 7-2)

A patent is an exclusive right to manufacture a product or to use a process. A copyright is an

Question 7-11 (LO 7-2)

Goodwill is an intangible asset on the balance sheet that is recorded only when one company

acquires another company. The acquiring company records goodwill equal to the purchase price less

Question 7-12 (LO 7-3)

We capitalize a particular cost as an asset if it increases future benefits, whereas we expense a

Answers to Review Questions (continued)

Question 7-13 (LO 7-3)

We expense repairs and maintenance expenditures which maintain a given level of benefits, in

the period incurred. We capitalize as assets more extensive repairs that increase the future benefits,

Question 7-14 (LO 7-3)

If a firm successfully defends an intangible right, it should capitalize the litigation costs and

Question 7-15 (LO 7-4)

The dictionary definition of depreciation is a decrease in value of an asset, whereas the

accounting definition of depreciation is an allocation of an asset’s cost to an expense over time.

Question 7-16 (LO 7-4)

We must estimate the service life (also called useful life) of the asset as well as its residual value

Question 7-17 (LO 7-4)

The service life tells how long the company expects to obtain benefits from the asset before

Question 7-18 (LO 7-4)

Residual value, also referred to as salvage value, is the amount the company expects to receive

Question 7-19 (LO 7-4)

Straight-line creates an equal amount of depreciation each year. Double-declining-balance

Answers to Review Questions (continued)

Question 7-20 (LO 7-4)

Little King Sandwiches uses straight-line depreciation that creates an equal amount of

depreciation each year. In contrast, University Hero uses double-declining balance depreciation that

Question 7-21 (LO 7-4)

University Hero depreciates over a shorter service life (20 years) and therefore will take more

depreciation expense per year. By taking more depreciation expense per year, University Hero will

Question 7-22 (LO 7-4)

Most companies use the straight-line method for financial reporting and the Internal Revenue

Service’s prescribed accelerated method (called MACRS) for income tax purposes. Companies

Question 7-23 (LO 7-5)

No. Just as we don’t depreciate land because it has an unlimited life, we don’t amortize

intangible assets with unlimited service lives such as goodwill and most trademarks. For most other

Question 7-24 (LO 7-6)

Book value is the cost of the asset minus accumulated depreciation. We record a gain if we sell

the asset for more than book value. Similarly, we record a loss if we sell the asset for less than book

value.

Answers to Review Questions (continued)

Question 7-25 (LO 7-7)

Return on assets equals net income divided by average total assets. Return on assets indicates the

Question 7-26 (LO 7-7)

Examples of high profit margin include companies that pursue a higher profit margin through

Question 7-27 (LO 7-8)

An asset impairment occurs when the future cash flows (future benefits) that we estimate a long-

term asset will generate, fall below its book value (cost minus accumulated depreciation).

Question 7-28 (LO 7-8)

A big bath is when a company records all losses in one year to make a bad current year even

worse. By recording additional expenses in the current year, management is able to report higher

7-6 Financial Accounting, 5e

BRIEF EXERCISES

Brief Exercise 7-1 (LO 7-1)

Purchase price of land (and warehouse to be removed)

$490,000

Brief Exercise 7-2 (LO 7-1)

Purchase price

$30,000

Total cost of the bread machine

$37,500

The $600 property tax is a recurring cost that benefits the company in the current

year. The Whole Grain Bakery will report the $600 as property tax expense over

the first year.

Brief Exercise 7-3 (LO 7-1)

Estimated

Fair

Value

Allocation

Percentage

Amount of

Basket

Purchase

Recorded

Amount

Building

$400,000

$400,000/$480,000 = 83.33% (= 5/6)

× $450,000

$375,000

Brief Exercise 7-4 (LO 7-2)

(in millions)

Purchase price

$19.0

Brief Exercise 7-5 (LO 7-2)

Salaries for R&D

$540,000

The $27,000 in patent filing and related legal costs are recorded to the patent

intangible asset account.

Brief Exercise 7-6 (LO 7-3)

(1)

Expense in the period incurred.

(2)

Capitalize and depreciate over the service life of the asset.

Brief Exercise 7-7 (LO 7-3)

$240,000

Betty Foods can capitalize legal fees only for the successful defense.

Brief Exercise 7-8 (LO 7-4)

The company controller’s approach to measuring depreciation is based on the

dictionary definition of depreciation – decrease in value of an asset. Depreciation in

Brief Exercise 7-9 (LO 7-4)

Year

2021

($45,000 – $6,000)

=

3,900 x 4/12

=

10

Brief Exercise 7-10 (LO 7-4)

1. Straight-line

2. Double-declining-balance

Brief Exercise 7-11 (LO 7-4)

Straight-line

Depreciation

expense

=

$50,000 – $10,000

=

$5,000

8 years

7-10 Financial Accounting, 5e

Brief Exercise 7-12 (LO 7-5)

Brief Exercise 7-13 (LO 7-6)

Sale amount

$16,000

Less:

Brief Exercise 7-14 (LO 7-6)

Sale amount

$25,000

Brief Exercise 7-15 (LO 7-6)

Debit

Credit

Loss

8,000

Accumulated Depreciation

12,000

Brief Exercise 7-16 (LO 7-6)

Debit

Credit

Equipment (Delivery Truck)

31,000

Brief Exercise 7-17 (LO 7-6)

Debit

Credit

Equipment

22,000

Brief Exercise 7-18 (LO 7-7)

Net income

=

20%

($840,000 + $930,000) 2

Brief Exercise 7-19 (LO 7-8)

Step 1: Test for Impairment

The long-term asset is not impaired since future cash flows ($38 million) are

Brief Exercise 7-20 (LO 7-8)

Step 1: Test for Impairment

The long-term asset is impaired since future cash flows ($32 million) are less

EXERCISES

Exercise 7-1 (LO 7-1)

Purchase price of land (and building to be removed)

$1,000,000

Title insurance

3,000

Exercise 7-2 (LO 7-1)

Purchase price

$75,000

Sales tax

6,000

Shipping

1,000

Exercise 7-3 (LO 7-1)

Estimated

Fair Value

Allocation

Percentage

Amount of

Basket Purchase

Recorded

Amount

Land

$175,000

$175,000/$700,000 = 25%

X $600,000

$150,000

Exercise 7-4 (LO 7-1, 7-4)

1. Land is not depreciated. However, depreciation on the building is tax-

2. If the true allocation should have been 20% to land and 80% to building, then

the allocation of 10% to land and 90% to building, for the express purpose of

reducing taxes, is not ethical. Who is harmed? The government is clearly

Exercise 7-5 (LO 7-2)

Debit

Credit

Legal Fees Expense

9,000

Exercise 7-6 (LO 7-2)

(amounts in millions)

Exercise 7-7 (LO 7-2)

1. Patent costs capitalized

2. Expense items on income statement

Basic research to develop the technology

$3,900,000

Exercise 7-8 (LO 7-2, 7-4)

List A

List B

__f_ 1. Depreciation

a. Exclusive right to display a word, a symbol, or an

Exercise 7-9 (LO 7-3)

1.

Equipment

$250,000

2.

Building

$750,000

Exercise 7-10 (LO 7-4)

1. Straight-line

2. Double-declining-balance

Depreciation

expense

=

$29,500 – $3,500

=

$2,600

10 years

7-18 Financial Accounting, 5e

Exercise 7-11 (LO 7-4)

Requirement 1

Straight-line

Requirement 2

Double-declining-balance

Calculation

End-of-Year Amounts

Year

Beginning

Book Value

X

Depreciation

Rate*

=

Depreciation

Expense

Accumulated

Depreciation

Book

Value**

Requirement 3

Activity-based

Calculation

End-of-Year Amounts

Year

Miles

Used

X

Depreciation

Rate*

=

Depreciation

Expense

Accumulated

Depreciation

Book

Value**

** $36,000 cost minus accumulated depreciation

Exercise 7-12 (LO 7-4)

Year

2021

($18,000 – $2,000)

=

$3,200 x 9/12

=

5 years

Exercise 7-13 (LO 7-4)

Year

Exercise 7-14 (LO 7-4)

Cost of the equipment

$19,000

Less: Accumulated depreciation (Years 1 and 2)

(8,000)*

Exercise 7-15 (LO 7-4)

($21,500 – $2,500)

=

$0.19/mile

100,000

7-20 Financial Accounting, 5e

Exercise 7-16 (LO 7-5)

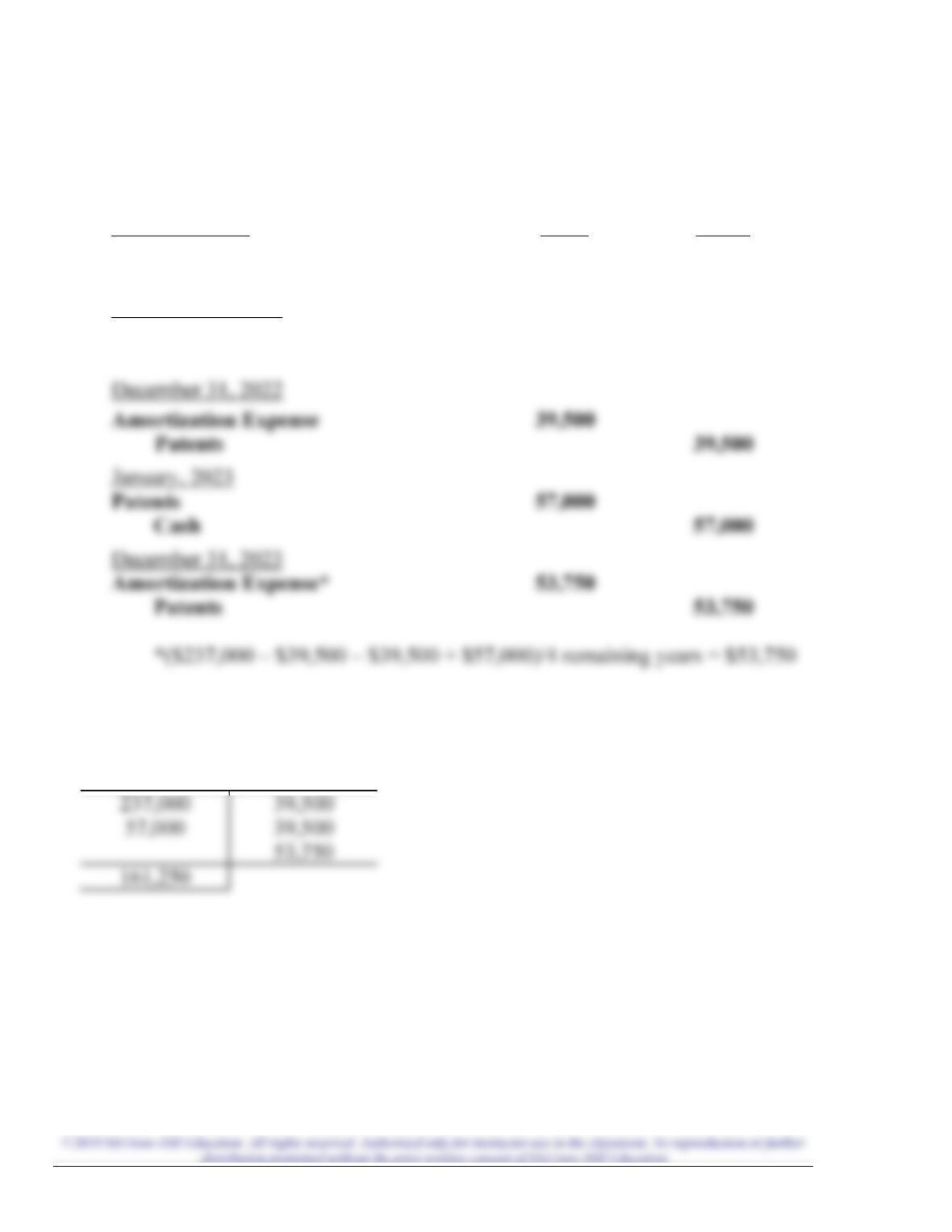

Requirement 1

January 1, 2021

Debit

Credit

Patents

237,000

Cash

237,000

December 31, 2021

Amortization Expense

39,500

Patents

39,500

Requirement 2

Balance in the Patents account

Patents