Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 4

THE INCOME STATEMENT, COMPREHENSIVE INCOME, AND THE

STATEMENT OF CASH FLOWS

Overview

The purpose of the income statement is to summarize the profit-generating activities that occurred

during a particular reporting period. Comprehensive income includes net income as well as a few

gains and losses that are not part of net income and are considered other comprehensive income

items instead.

Learning Objectives

LO4-1 Discuss the importance of income from continuing operations and describe its

components.

LO4-2 Describe earnings quality and how it is impacted by management practices to manipulate

earnings.

LO4-3 Discuss the components of operating and nonoperating income and their relationship to

Lecture Outline

Part A: The Income Statement and Comprehensive Income

I. Income from Continuing Operations

A. Income from continuing operations includes the revenues, expenses, gains, and losses that

will probably continue in future periods.

1. Income tax expense always is shown as a separate expense.

II. Earnings Quality

A. Earnings quality refers to the ability of reported earnings (income) to predict a company’s

future earnings.

1. To enhance predictive value, analysts try to separate a company’s transitory earnings

B. Not all items included in operating income should be considered indicative of a company’s

permanent earnings. (T4-5)

1. Restructuring costs include costs associated with shutdown or relocation of facilities

or downsizing of operations. GAAP requires these costs to be expensed in the

III. Discontinued operations

A. Discontinued operations involve the disposal or planned disposal of a component of an

entity.

1. Discontinued operations must be reported separately, below income from continuing

operations. (T4-7)

B. What constitutes a component of an entity? (T4-8)

1. A component is any part of the company, such as an operating segment or subsidiary,

that includes operations and cash flows that can be clearly distinguished, operationally

C. Reporting discontinued operations,

1. When the component has been sold, the income effects of a discontinued operation

includes (1) the operating income or loss of the component from the beginning of the

IV. Accounting Changes

A. Accounting changes fall into one of three categories: (1) a change in an accounting

principle, (2) a change in estimate, or (3) a change in reporting entity.

B. Most voluntary changes in accounting principles are accounted for retrospectively by

revising prior years’ financial statements. (T4-11)

1. The comparative financial statements are revised.

C. A change in depreciation, amortization, or depletion method is considered to be a change

in accounting estimate that is achieved by a change in accounting principle. These

V. Correction of Accounting Errors

A. Errors discovered in the same year they are made are simply corrected by journal entry.

B. Treatment of errors discovered in a year subsequent to the year the error is made depends

VI. Earnings per Share Disclosures

A. Earnings per share (EPS) is the amount of income reported during a period for each share

of common stock outstanding.

VII. Comprehensive Income

4-4 Intermediate Accounting, 8/e

A. The purpose of the income statement is to summarize the profit-generating activities that

occurred during a particular reporting period.

B. Comprehensive income is the total change in equity for a reporting period other than from

Part B: The Statement of Cash Flows

I. Usefulness of the Statement of Cash Flows

A. The purpose of the statement of cash flows (SCF) is to provide information about cash

II. Classifying Cash Flows

A. The SCF classifies all transactions affecting cash into one of three categories: (T4-16)

1. Operating activities are inflows and outflows of cash related to the transactions

entering into the determination of net operating income. (T4-17)

a. The Direct Method

Appendix4: Interim Reporting

A. Interim reports are issued for periods of less than a year, typically as quarterly financial

statements.

B. With only a few exceptions, the same accounting principles applicable to annual reporting

are used for interim reporting.

PowerPoint Slides

A PowerPoint presentation of the chapter is available in the Connect library.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or

4-6 Intermediate Accounting, 8/e

INCOME STATEMENTS —

URBAN OUTFITTERS INC.

.

Consolidated Statements of Income

(In thousands, except per share data)

Fiscal Year Ended January 31

2014

2013

2012

Net sales

$3,086,608

$2,794,925

$2,473,801

Cost of sales

1,925,266

1,763,394

1,613,265

Gross profit

1,161,342

1,031,531

860,536

Illustration 4-2

SINGLE-STEP INCOME STATEMENT

➢ An advantage of the single-step format is its simplicity.

MAXWELL GEAR CORPORATION

Income Statement

For the Year Ended December 31, 2016

Revenues and gains:

Sales ............................................................................

$573,522

Interest and dividends .................................................

26,400

Interest .........................................................................

14,522

Total expenses and losses ......................................

405,422

Income before income taxes ..........................................

200,000

Illustration 4-3

T4-2

4-8 Intermediate Accounting, 8/e

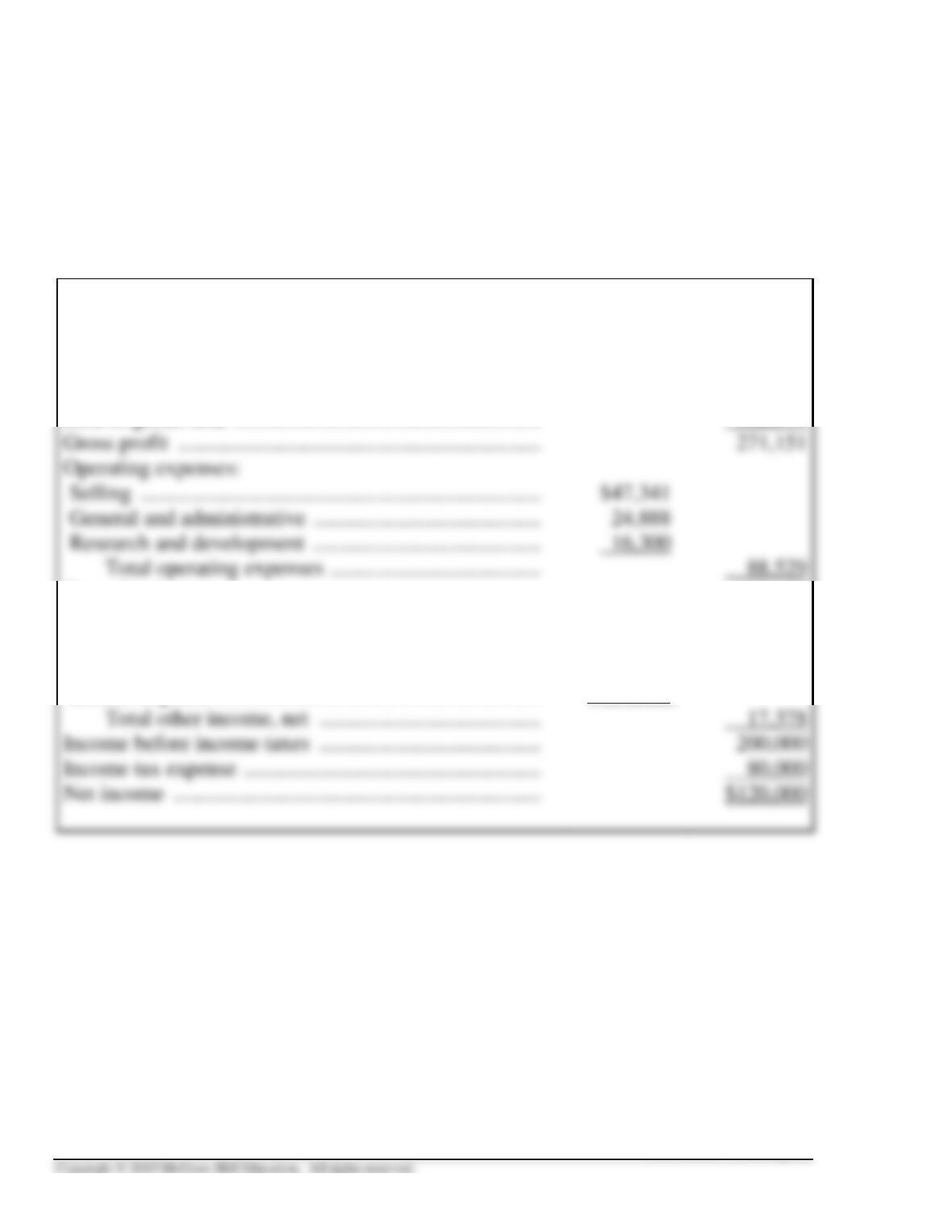

MULTIPLE-STEP INCOME STATEMENT

➢ An advantage of the multiple-step format is that it separately

reports operating and nonoperating activities.

MAXWELL GEAR CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ................................................................

$573,522

Cost of goods sold .........................................................

302,371

Operating income ..........................................................

182,622

Other income (expense):

Interest and dividend revenue ......................................

26,400

Gain on sale of investments ..........................................

5,500

Interest expense ............................................................

(14,522)

Illustration 4-4

T4-3

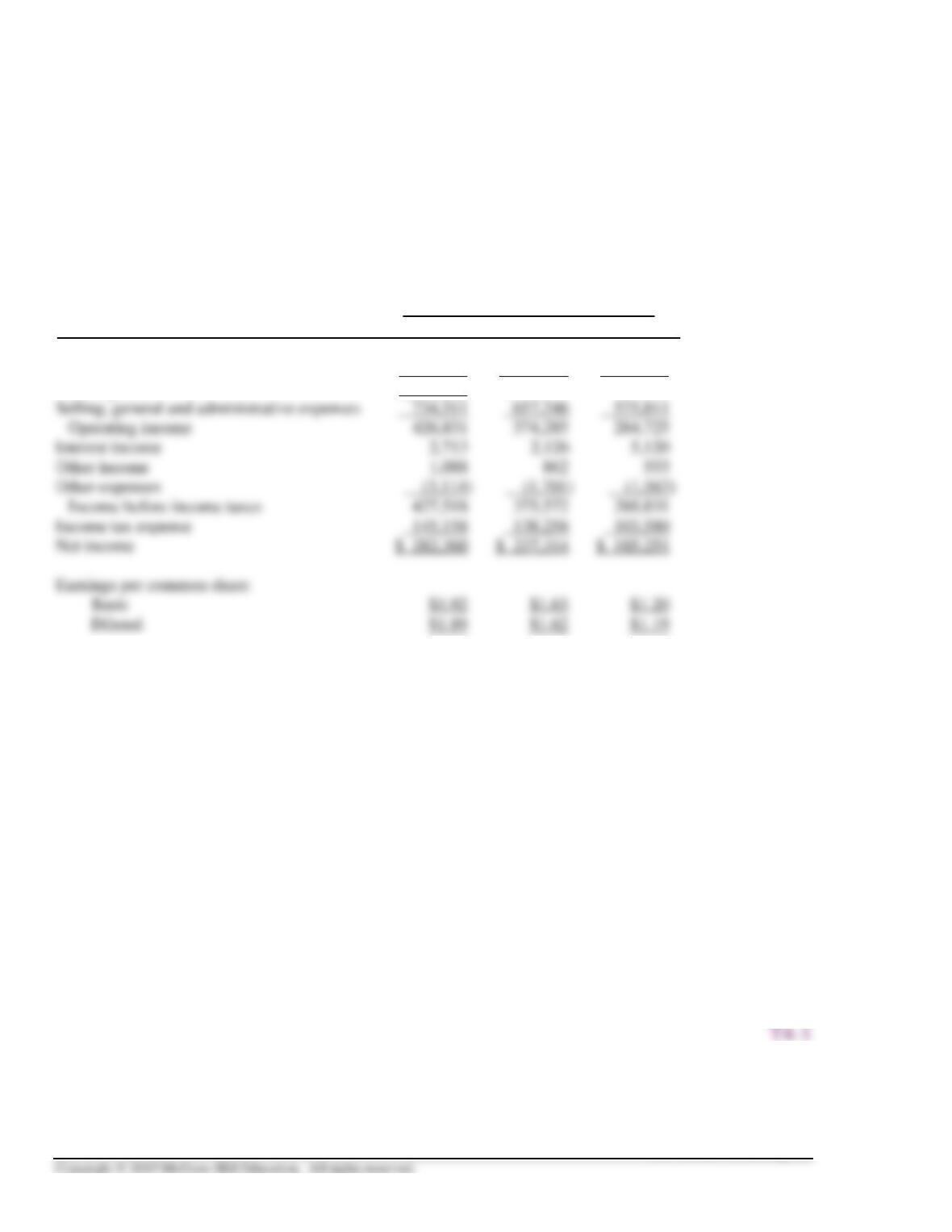

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Income Statement Presentation. There are more similarities than

differences between income statements prepared according to U.S. GAAP

and those prepared applying international standards. Some of the

differences are:

• International standards allow expenses to be classified either by

function (e.g., cost of goods sold, general and administrative, etc), or

by natural description (e.g., salaries, rent, etc.). SEC regulations

require that expenses be classified by function.

T4-4

4-10 Intermediate Accounting, 8/e

OPERATING INCOME AND EARNINGS QUALITY

Income Statements – GameStop Corp.

Income Statements (in part)

($ in millions)

Year Ended

February 1,

2014

February 2,

2013

Net sales

$9,039.5

$8,886.7

Cost of sales

6,378.4

6,235.2

Illustration 4-5

NONOPERATING INCOME AND EARNINGS

QUALITY

➢ Some nonoperating items have generated considerable

Income Statements – Intel Corporation

Income Statements (in part)

Years Ended December 30

(in millions)

2000

1999

Illustration 4-6

T4-6

4-12 Intermediate Accounting, 8/e

DISCONTINUED OPERATIONS

► Discontinued operations must be reported separately, below

income from continuing operations.

Income from continuing operations before income taxes XXX

➢ The income tax effect of discontinued operations is included in

the separate presentation rather than as part of the amount

T4-7

4-14 Intermediate Accounting, 8/e

DISCONTINUED OPERATION

► A component is any part of the company, such as an operating

segment or subsidiary, that includes operations and cash flows

that can be clearly distinguished, operationally and for

DISCONTINUED OPERATIONS —

When the component has been sold

➢ When the component has been sold, the income effects of a

discontinued operation includes:

1. Operating income or loss (revenues, expenses, gains and losses)

2. Gain or loss on disposal.

The Duluth Holding Company has several operating divisions. In October 2016, management

decided to sell one of its divisions that qualifies as a separate component according to generally

Duluth’s income statement for the year 2016, beginning with income from continuing

operations, would be reported as follows:

Income from continuing operations $22,350,000

Illustration 4-7

T4-9

4-16 Intermediate Accounting, 8/e

DISCONTINUED OPERATIONS —

When the component is considered held for sale

➢ When the component is considered held for sale, the income

effects of a discontinued operation includes:

1. Operating income or loss (revenues, expenses, gains and losses)

The Duluth Holding Company has several operating divisions. In October of 2016, management

decided to sell one of its divisions that qualifies as a separate component according to generally

accepted accounting principles. On December 31, 2016, the end of the company’s fiscal year, the

Duluth’s income statement for 2016, beginning with income from continuing operations, would

be reported as follows:

Income from continuing operations $22,350,000

Discontinued operations:

Illustration 4-8

T4-10

CHANGE IN ACCOUNTING PRINCIPLE

► Most voluntary changes in accounting principles are

► The steps used to account for changes are as follows:

1. The comparative financial statements are revised.

► A change in depreciation, amortization, or depletion method

is considered to be a change in accounting estimate that is