Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 21 The Statement of Cash Flows Revisited

QUESTIONS FOR REVIEW OF KEY TOPICS

Question 21–1

Every cash flow eventually affects the balance of one or more accounts in the

Question 21–2

The informational value of the presentation is enhanced if the cash flows are

Question 21–3

No, an investment in Treasury bills need not always be classified as a cash

equivalent. A guideline—not a rule—for cash equivalents is that these investments

21–2 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 21–4

Transactions that involve merely transfers from cash to cash equivalents such as

the purchase of a three-month Treasury bill, or from cash equivalents to cash such as

Question 21–5

"Cash flows from operating activities" are both inflows and outflows of cash that

Question 21–6

The generalization that "cash flows from operating activities" report all the

Answers to Questions (continued)

Question 21–7

"Cash flows from investing activities" are both outflows and inflows of cash due to

the acquisition and disposition of assets. This classification includes cash payments to

acquire (1) property, plant, and equipment and other productive assets; (2)

Question 21–8

The payment of cash dividends to shareholders is classified as a financing activity,

Answers to Questions (continued)

Question 21–9

A statement of cash flows reports transactions that cause an increase or a decrease

1. Acquiring an asset by incurring a debt payable to the seller.

2. Acquiring an asset by entering into a lease agreement.

Question 21–10

The acquisition of a building purchased by issuing a mortgage note payable in

Question 21–11

Perhaps the most noteworthy item reported on an income statement is net

income—the amount by which revenues exceed expenses. The most noteworthy item

Answers to Questions (continued)

Question 21–12

The spreadsheet entries shown in the two "changes" columns, which separate the

beginning and ending balances, explain the increase or decrease in each account

Question 21–13

If sales revenue is $200,000, this does not necessarily mean that $200,000 cash

was received from customers. Amounts reported on the income statement usually do

Question 21–14

When an asset is sold at a gain, the gain is not reported as a cash inflow from

21–6 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 21–15

When determining the amount of cash paid for income taxes, an increase in the

Question 21–16

When using the indirect method of determining net cash flows from operating

activities, the net cash increase or decrease from operating activities is derived

Question 21–17

When using the indirect method of determining net cash flows from operating

Answers to Questions (continued)

Question 21–18

Either the direct method or the indirect method is permitted, but the FASB strongly

encourages companies to report "cash flows from operating activities" by the direct

Question 21–19

The direct and indirect methods are alternative approaches to deriving net cash

Question 21–20

Question 21–21

U.S. GAAP designates cash outflows for interest payments and cash inflows from

interest and dividends received as operating cash flows. Dividends paid to

shareholders are classified as financing cash flows. IFRS permits more flexibility.

Companies can report interest and dividends paid as either operating or financing cash

21–8 Intermediate Accounting, 8/e

BRIEF EXERCISES

Brief Exercise 21–1

Summary Entry ($ in millions)

Cash (received from customers) 38

Brief Exercise 21–2

Summary Entry ($ in millions)

Brief Exercise 21–3

Summary Entry ($ in millions)

Cost of goods sold 25

Inventory 6

Brief Exercise 21–4

Summary Entry ($ in millions)

Salaries expense 17

Brief Exercise 21–5

($ in millions)

Interest expense (10% x 1/2 x $380) 19

21–10 Intermediate Accounting, 8/e

Brief Exercise 21–6

($ in millions)

Interest expense (10% x 1/2 x $380) 19

Agee would report the cash inflow of $380 million from the sale of the bonds as a

cash inflow from financing activities in its statement of cash flows.

Brief Exercise 21–7

Merit would report the cash inflow of $41 million from the borrowing as a cash inflow

from financing activities in its statement of cash flows.

*December 31, 2016

Interest expense (7% x outstanding balance) ... 2,870,000

Brief Exercise 21–8

($ in millions)

Cash ......................................................... 35

Gain on sale of land (difference) ............ 13

21–12 Intermediate Accounting, 8/e

Brief Exercise 21–9

Cash Flows from Investing Activities:

Proceeds from sale of marketable securities $30

Brief Exercise 21–10

Cash Flows from Financing Activities:

Sale of common shares $40

Brief Exercise 21–11

Net income $90

Adjustments for noncash effects:

Depreciation expense 3

Loss on sale of equipment 2

Brief Exercise 21–12

Net income $60

Adjustments for noncash effects:

Amortization expense 2

EXERCISES

Exercise 21–1

Example F 1. Sale of common stock

I 2. Sale of land

F 3. Purchase of treasury stock

O 4. Merchandise sales

F 13. Payment of a cash dividend

I 14. Purchase of building

I 15. Collection of nontrade note receivable (principal amount)

I 16. Loan to another firm

Exercise 21–2

Requirement 1

($ in millions)

Inventory

_______________________________________

Beginning balance 90

Goods purchased 303 300 Cost of goods sold

Requirement 2

Summary Entry ($ in millions)

Cost of goods sold 300

21–16 Intermediate Accounting, 8/e

Exercise 21–3

($ in millions)

Situation Sales Accounts Cash received

revenue receivable from

customers

increase

(decrease)

1 100 -0- 100

2 100 5 95

3 100 (5) 105

3. Summary Entry Cash (received from customers) 105

Exercise 21–4

Situation Sales Accounts Cash received

revenue receivable from

customers

increase

(decrease)

1 200 -0- 200

2 200 10 190

2. Summary Entry Cash (received from customers) 190

3 200 10 190

3. Summary Entry Cash (received from customers) 210

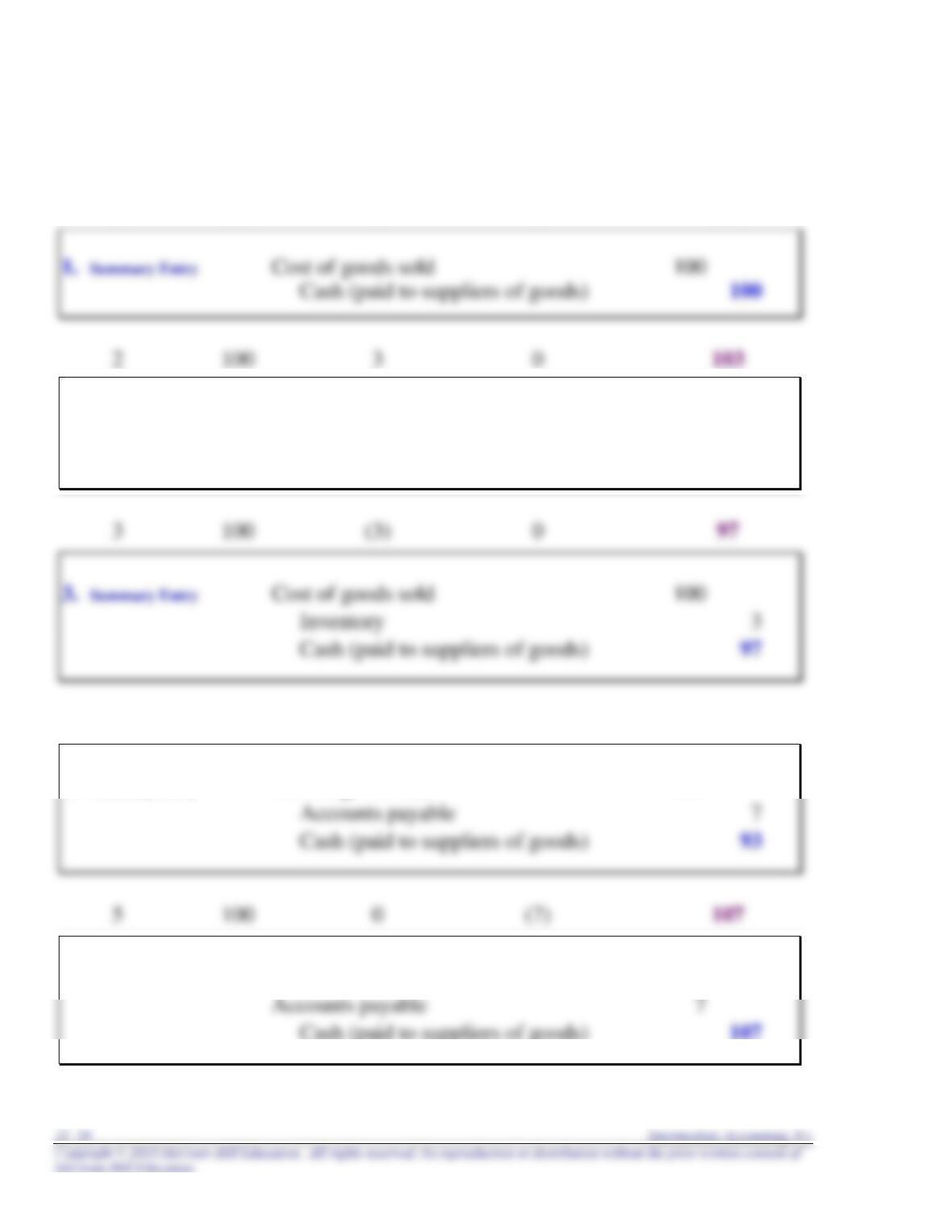

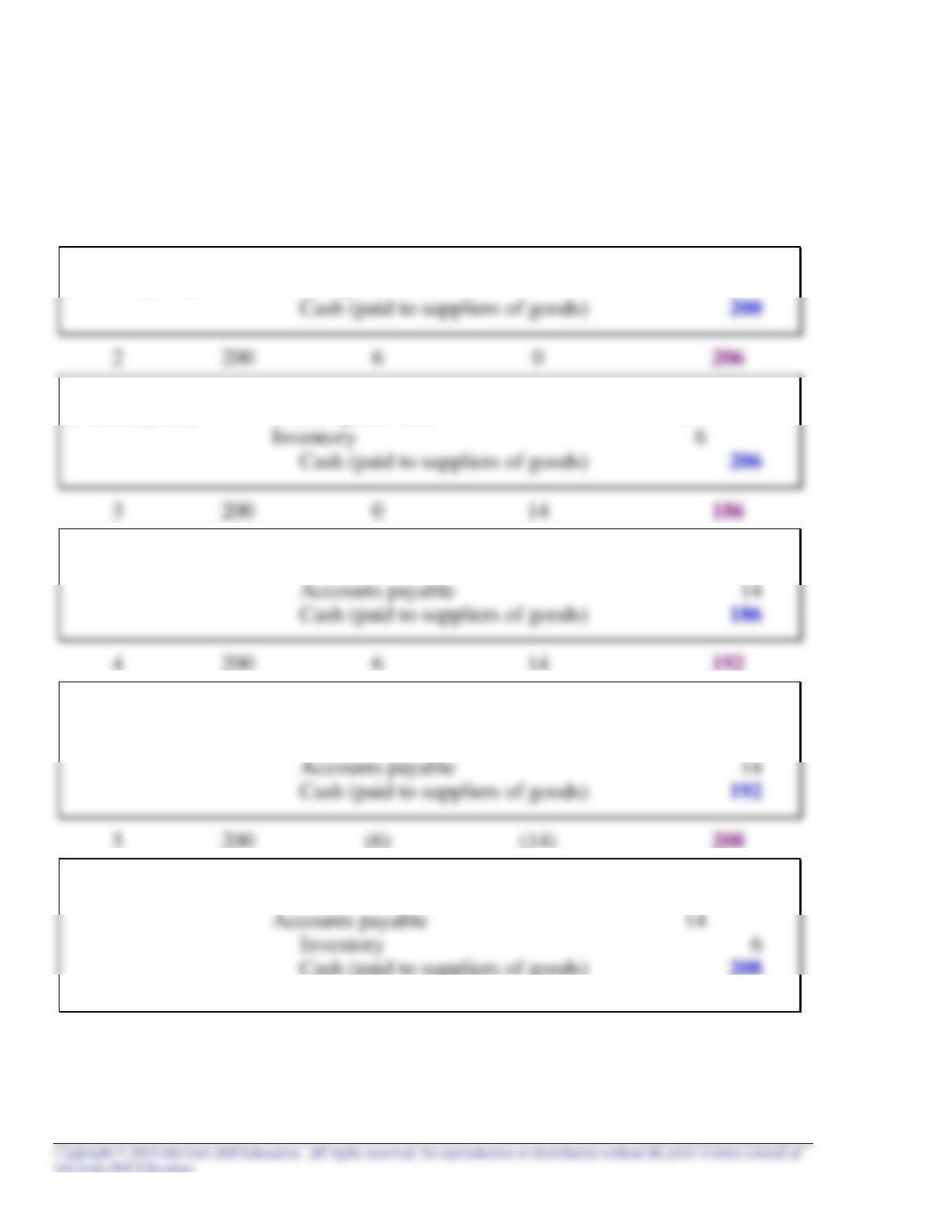

Exercise 21–5

Cost of Accounts Cash paid to

Situation goods sold Inventory payable suppliers

increase (decrease) increase (decrease)

1 100 0 0 100

2. Summary Entry Cost of goods sold 100

Inventory 3

Cash (paid to suppliers of goods) 103

4 100 0 7 93

4. Summary Entry Cost of goods sold 100

5. Summary Entry Cost of goods sold 100

Exercise 21–5 (concluded)

Cost of Accounts Cash paid to

Situation goods sold Inventory payable suppliers

increase (decrease) increase (decrease)

6 100 3 7 96

6. Summary Entry Cost of goods sold 100

Inventory 3

7. Summary Entry Cost of goods sold 100

Inventory 3

8. Summary Entry Cost of goods sold 100

Accounts payable 7

9. Summary Entry Cost of goods sold 100

21–20 Intermediate Accounting, 8/e

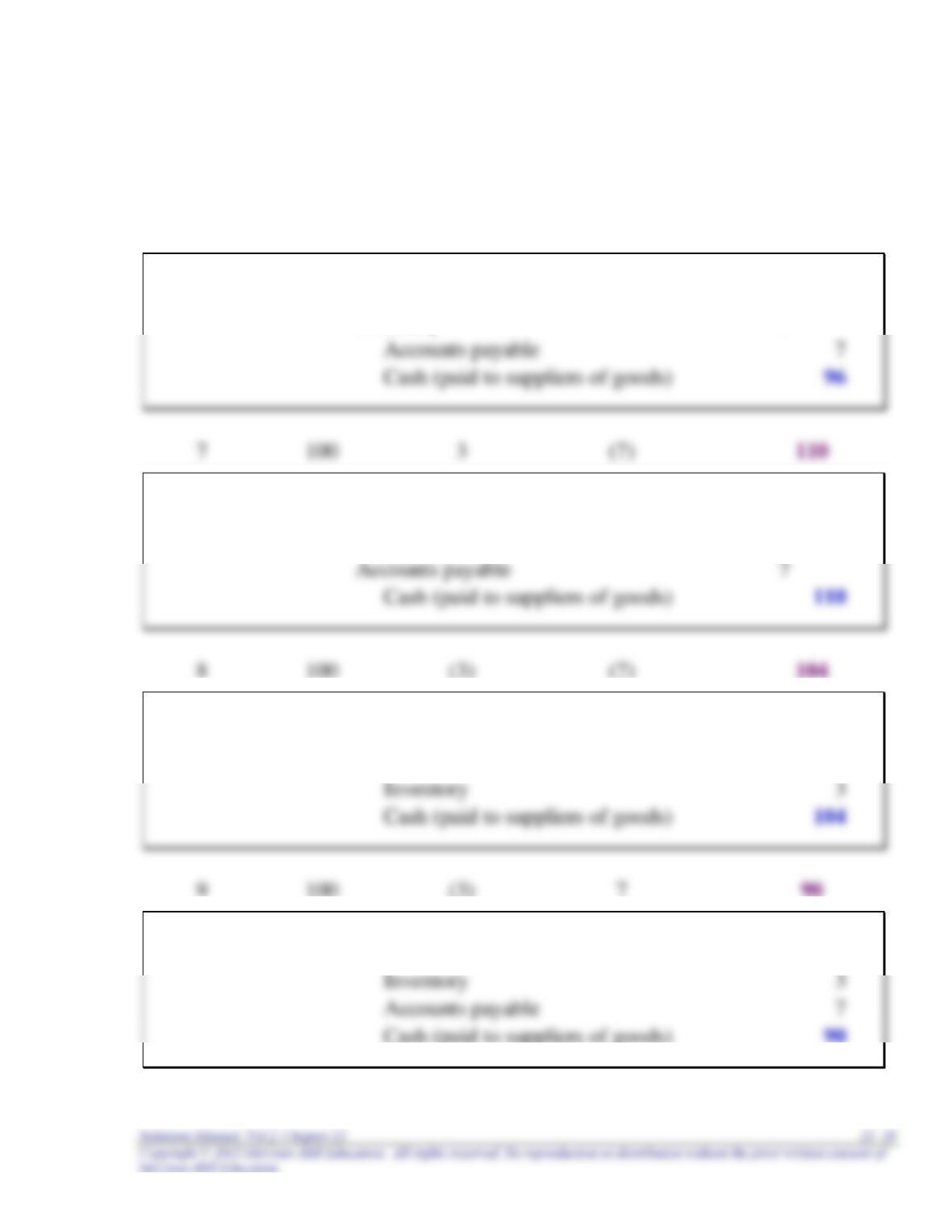

Exercise 21–6

Cost of Accounts Cash paid to

Situation goods sold Inventory payable suppliers

increase increase

(decrease) (decrease)

1 200 0 0 200

1. Summary Entry Cost of goods sold 200

2. Summary Entry Cost of goods sold 200

3. Summary Entry Cost of goods sold 200

4. Summary Entry Cost of goods sold 200

Inventory 6

5. Summary Entry Cost of goods sold 200