Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 21–23

Direct Method

Cash Flows from Operating Activities:

Cash received from customers $672

Cash paid to suppliers (234)

21–42 Intermediate Accounting, 8/e

Exercise 21–24

Indirect Method

Cash Flows from Operating Activities:

Net income $ 91

Adjustments for noncash effects:

Depreciation expense 90

Patent amortization expense 5

Exercise 21–25

Direct Method

Cash Flows from Operating Activities:

Cash received from customers $1,332 a

Exercise 21–25 (concluded)

Calculations using summary entries:

a. Summary Entry Cash (received from customers) 1,332

Accounts receivable 12

Sales revenue 1,320

d. Summary Entry Interest expense 40

Interest payable 5

Cash (paid for interest) 35

** If a cash equivalent investment is sold for either more or less than its acquisition

cost, we have a cash flow. Suppose the cost of this investment classified as a

cash equivalent had been, say, $15.000 and was sold for $9,000, $6,000 less

Depreciation expense and patent amortization are not cash flows.

Exercise 21–26

Indirect Method

Cash Flows from Operating Activities:

Net income $182

Adjustments for noncash effects:

Depreciation expense 180

Changes in operating assets and liabilities:

Decrease in accounts receivable 12

21–46 Intermediate Accounting, 8/e

Exercise 21–27

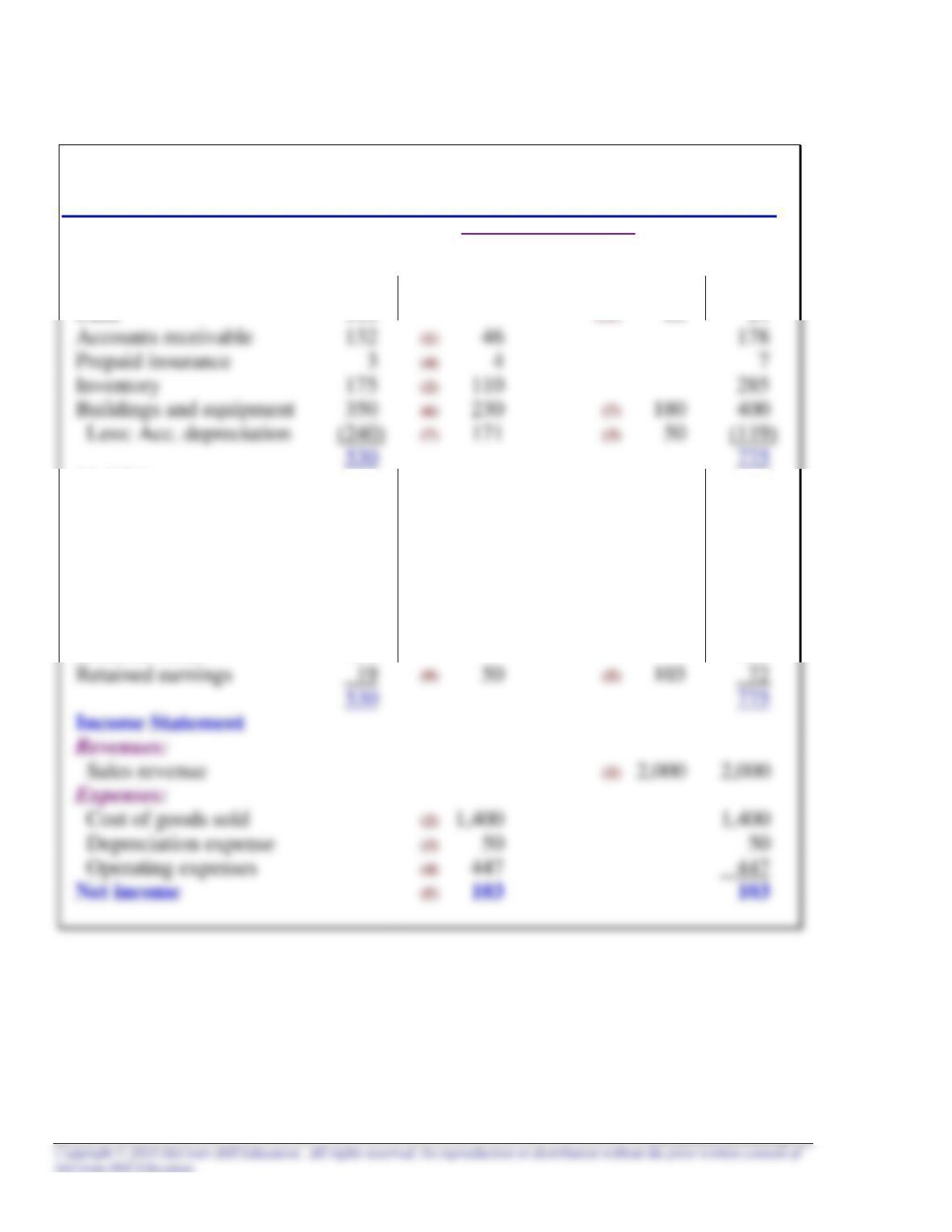

RED, INC.

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 110 (11) 86 24

Liabilities:

Accounts payable 100 (2) 13 87

Accrued expenses payable 11 (4) 5 6

Notes payable 0 (8) 50 50

Bonds payable 0 (10) 160 160

Shareholders' Equity:

Common stock 400 400

Exercise 21–27 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Operating activities:

Cash inflows:

Financing activities:

Issuance of note payable (8) 50

Exercise 21–27 (concluded)

RED, INC.

Statement of Cash Flows

For year ended December 31, 2016 ($ in millions)

Cash flows from operating activities:

Cash inflows:

From customers $1,954

Cash flows from investing activities:

Purchase of equipment (230)

Cash flows from financing activities:

Issuance of note payable 50

Issuance of bonds payable 160

Exercise 21–28

$ in millions

Pension expense (given) 82

Plan assets (expected return) 90

PBO ($112 service cost + $51 interest cost) 163

21–50 Intermediate Accounting, 8/e

Exercise 21–29

Requirement 1

The specific citation that specifies the guidelines for cash equivalents is FASB ASC

Requirement 2

Specifically, the guidelines are:

Cash Equivalents

Cash equivalents are short-term, highly liquid investments that have both of the

following characteristics:

Generally, only investments with original maturities of three months or less qualify

under that definition. Original maturity means original maturity to the entity holding

the investment. For example, both a three-month U.S. Treasury bill and a three-year

Exercise 21–30

The FASB Accounting Standards Codification represents the single source of

authoritative U.S. generally accepted accounting principles. The specific citation for

each of the following items is:

1. Disclosure of interest and income taxes paid if the indirect method is used:

3. Disclosure of noncash investing and financing activities:

21–52 Intermediate Accounting, 8/e

Exercise 21–31

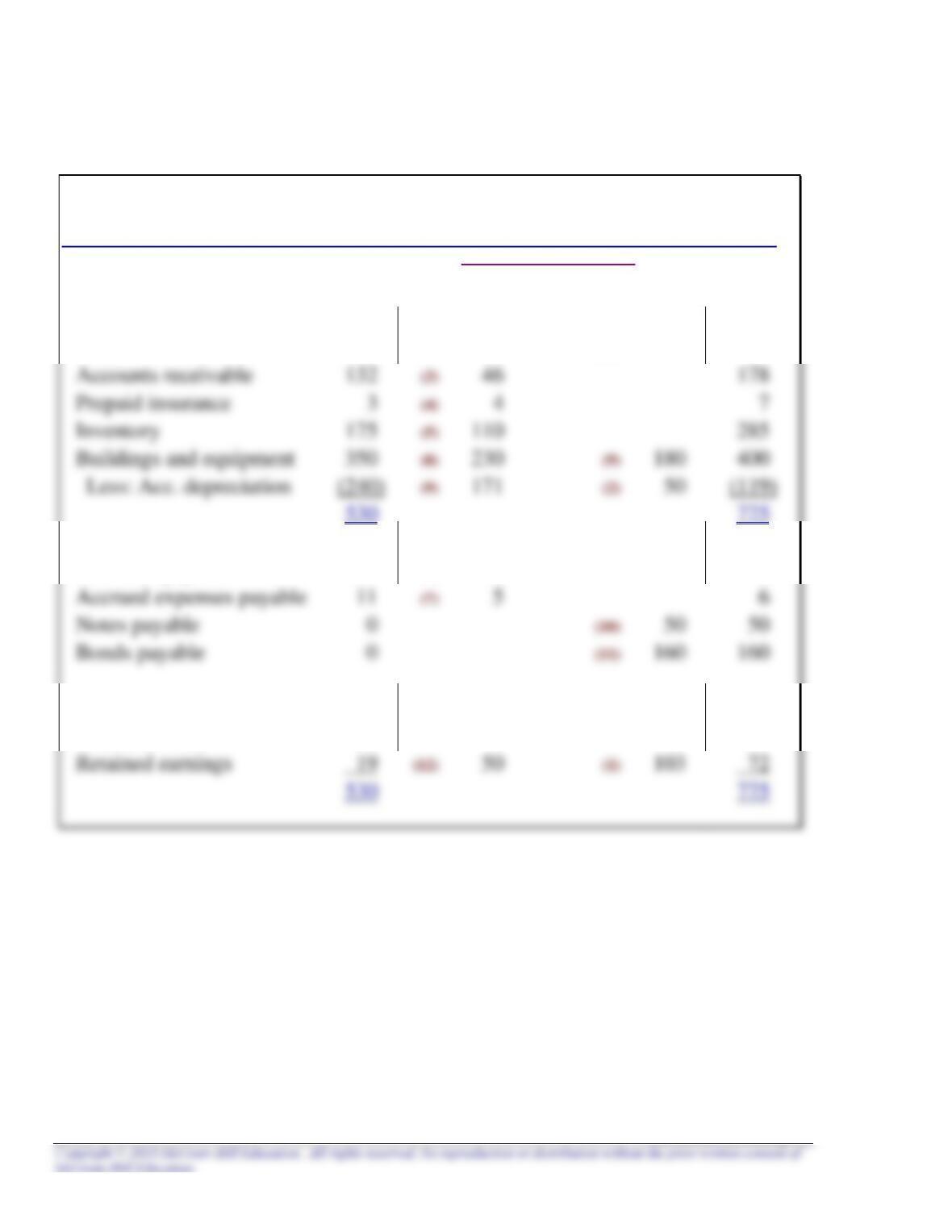

RED, INC.

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 110 (13) 86 24

Liabilities:

Accounts payable 100 (6) 13 87

Shareholders' Equity:

Common stock 400 400

Exercise 21–31 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Net income (1) 103

Adjustments for noncash effects:

Depreciation expense (2) 50

Increase in accounts receivable (3) 46

Investing activities:

Purchase of equipment (8) 230

Sale of equipment (9) 9

Net cash flows (221)

Financing activities:

Issuance of note payable (10) 50

Exercise 21–31 (concluded)

RED, INC.

Statement of Cash Flows

For year ended December 31, 2016 ($ in millions)

Cash flows from operating activities:

Net income $ 103

Adjustments for noncash effects:

Depreciation expense 50

Cash flows from investing activities:

Purchase of equipment (230)

Cash flows from financing activities:

Issuance of note payable 50

Net decrease in cash (86)

Cash balance, January 1 110

Cash balance, December 31 $ 24

Exercise 21–32

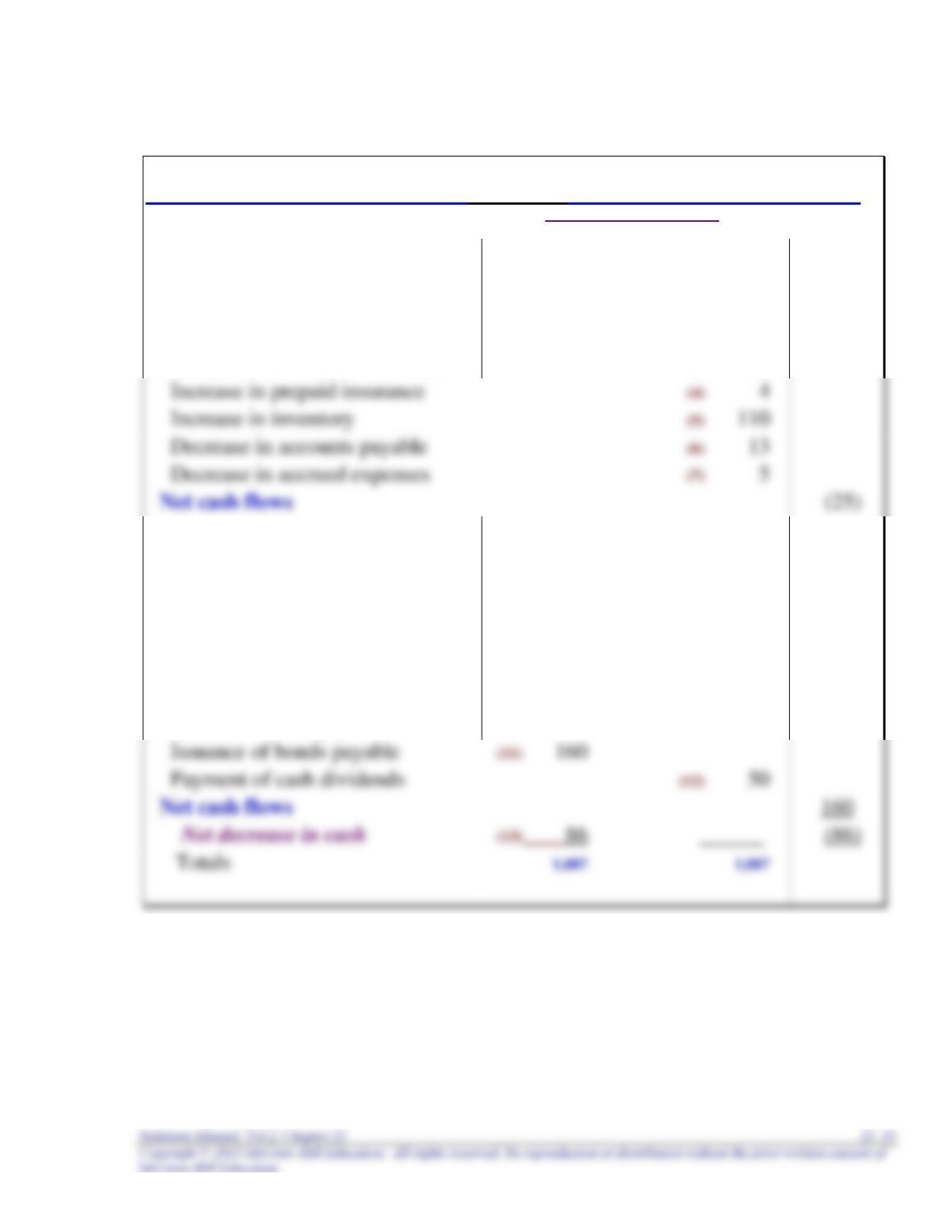

BALANCE SHEET ACCOUNTS

Cash (Statement of Cash Flows)

______________________________________________________

86

Operating Activities:

From customers (1) 1,954 1,523 (2) To suppliers

456 (4) For expenses

Accounts Receivable Prepaid Insurance

______________________ ______________________

46 4

________ ________

(1) 46 (4) 4

Inventory Buildings and Equipment

21–56 Intermediate Accounting, 8/e

Exercise 21–32 (continued)

Accrued Expenses Payable Notes Payable

______________________ ______________________

5 50

________ ________

(4) 5 50 (8)

INCOME STATEMENT ACCOUNTS

Sales Cost of Goods Sold

______________________ ______________________

2,000 1,400

________ ________

2,000 (1) (2) 1,400

Net Income (Income Summary)

Exercise 21–32 (concluded)

RED, INC.

Statement of Cash Flows

For year ended December 31, 2016 ($ in millions)

Cash flows from operating activities:

Cash inflows:

Cash flows from investing activities:

Purchase of equipment (230)

Sale of equipment 9

Net cash flows from investing activities (221)

Cash flows from financing activities:

Issuance of note payable 50

Net decrease in cash (86)

Cash balance, January 1 110

21–58 Intermediate Accounting, 8/e

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

1. b. The two gains are not cash flows. Proceeds from the sale of equipment are

4. a. Dividends paid to stockholders are considered cash flows relating to

5. d. Dividends paid is not a component of cash flow from investing; it is a

6. a. Cash flows from operations using the indirect method are computed by

taking net income plus noncash expenses (e.g., depreciation) less gains from

7. c. IFRS allows companies to report cash outflows for interest and dividends as

either operating or financing cash flows.

8. b. U.S. GAAP requires that interest received and interest payments be reported

CMA Exam Questions

1. d. A statement of cash flows should report as operating activities all

transactions and other events not classified as investing or financing

2. a. Investing activities include the lending of money and the collecting of those

loans, and the acquisition, sale, or other disposal of securities that are not

cash equivalents and of productive assets that are expected to generate

3. c. Net operating cash flow may be determined by adjusting net income.

Depreciation is an expense not directly affecting cash flows that should be

added back to net income. The increase in accounts payable is added to net

21–60 Intermediate Accounting, 8/e

PROBLEMS

Problem 21–1

Classifications

+ I Investing activity (cash inflow)

Transactions

Example + I 1. Sale of land.

+ F 2. Issuance of common stock for cash.

– F 3. Purchase of treasury stock.

N 4. Conversion of bonds payable to common stock.

X 11. Issuance of stock dividend.

N 12. Payment of property dividend.

– F 13. Payment of cash dividends.

+ F 14. Issuance of short-term note payable for cash.

+ F 15. Issuance of long-term note payable for cash.

– I 16. Purchase of marketable securities (“available for sale”).