Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 21–11

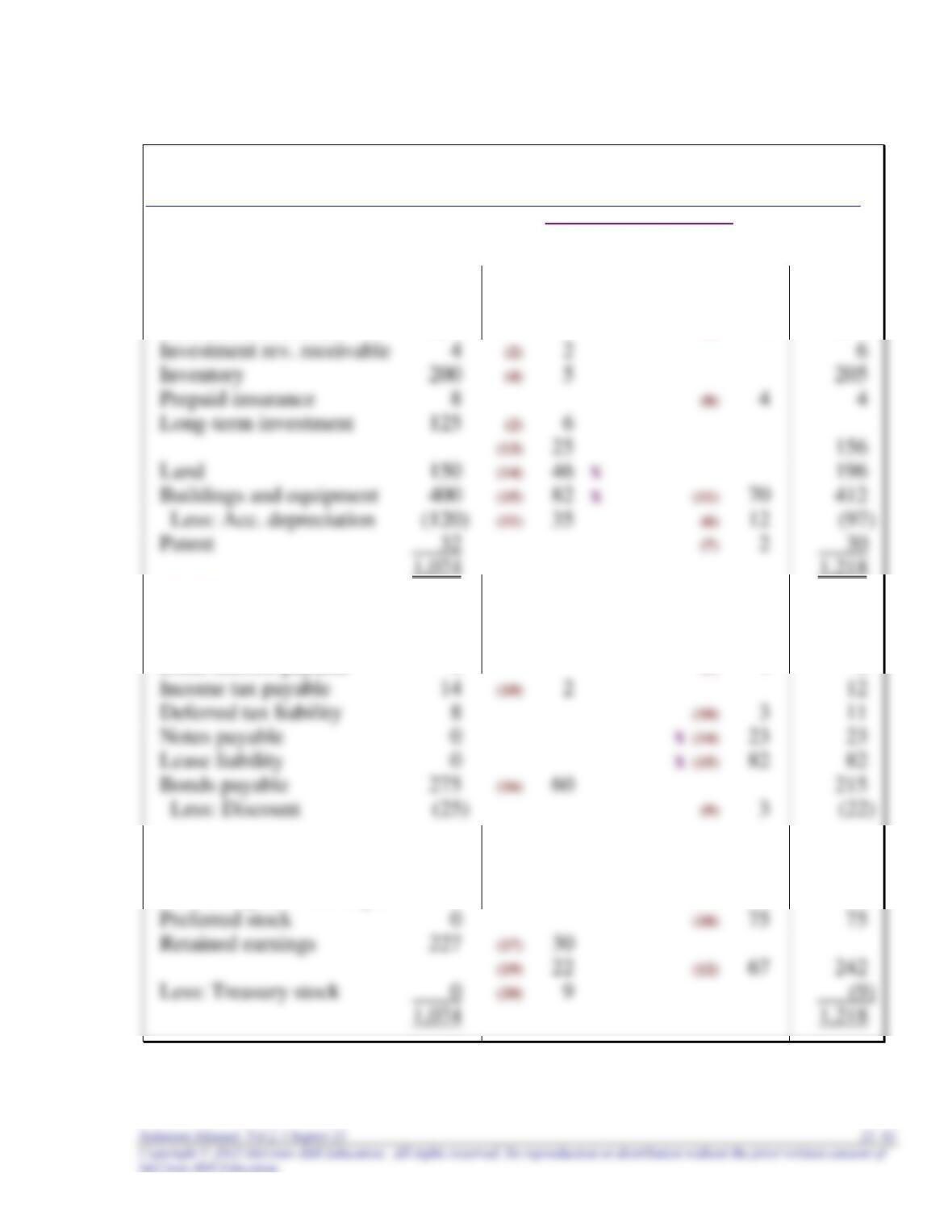

ARDUOUS COMPANY

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 81 (21) 35 116

Accounts receivable 194 (1) 4 190

Liabilities:

Accounts payable 65 (4) 15 50

Salaries payable 11 (5) 5 6

Bond interest payable 4 (9) 4 8

Shareholders' Equity:

Common stock 410 (17) 20 430

Paid-in capital—ex. of par 85 (17) 10 95

21–82 Intermediate Accounting, 8/e

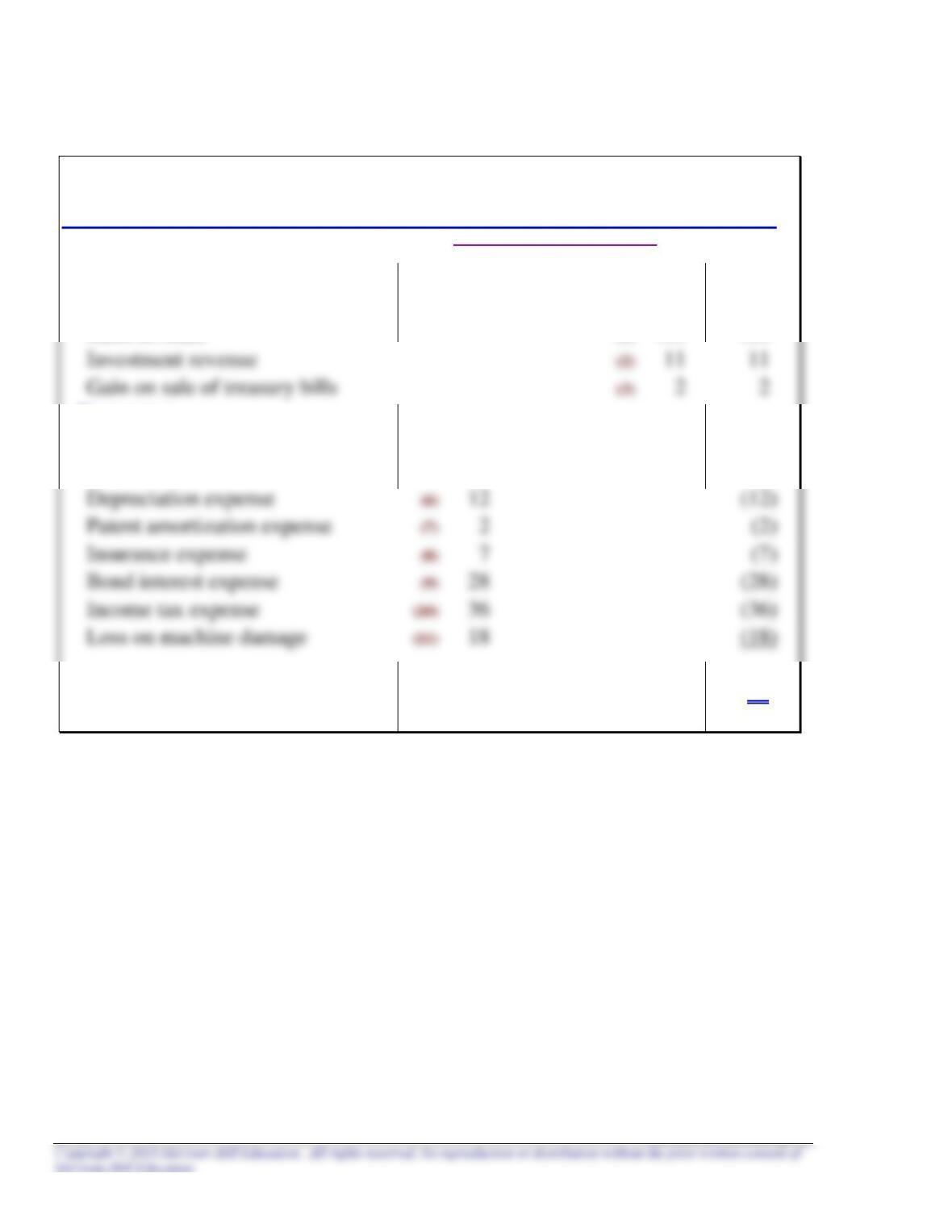

Problem 21–11 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Income

Revenues:

Sales revenue (1) 410 410

Expenses:

Cost of goods sold (4) 180 (180)

Salaries expense (5) 73 (73)

Net income (12) 67 67

X Noncash investing and financing activity.

Problem 21–11 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Operating activities:

Cash inflows:

From customers (1) 414

From investment revenue (2) 3

Net cash flows 82

Investing activities:

Sale of machine components (11) 17

Net cash flows (31)

Financing activities:

Retirement of bonds payable (16) 60

Sale of preferred stock (18) 75

Net increase in cash (21) 35 35

Totals 1,313 1,313

Problem 21–11 (concluded)

ARDUOUS COMPANY

Statement of Cash Flows

For year ended December 31, 2016 ($ in millions)

Cash flows from operating activities:

Cash inflows:

From customers $414

From investment revenue 3

Cash flows from investing activities:

Sale of machine components 17

Purchase of long-term investment (25)

Purchase of land (23)

Net cash flows from investing activities (31)

Cash flows from financing activities:

Retirement of bonds payable (60)

Sale of preferred stock 75

Noncash investing and financing activities:

Acquired $82 million building by 15-year lease.

Problem 21–12

Requirement 1

Retirement of common shares ($ in millions)

Common stock (5 million shares x $1 par per share) ............................... 5

Paid-in capital—excess of par ($22 – 5 – 2) .................................. 15

Net income closed to retained earnings

Income summary .............................................................................................. 88

Retained earnings (given) ........................................................ 88

Declaration of a cash dividend

Retained earnings (given) ............................................................ 33

Declaration of a stock dividend

Retained earnings (given) ............................................................ 20

21–86 Intermediate Accounting, 8/e

Problem 21–12 (concluded)

Requirement 2

BRENNER-JUDE CORPORATION

Statement of Retained Earnings

FOR THE YEAR ENDED DECEMBER 31, 2016

($ in millions)

Balance at January 1 $ 90

Deductions:

Retirement of common stock (2)

Problem 21–13

Amount Category

1. Cash collections from customers (direct method). $145,0001 O

2. Payments for purchase of property, plant, and

1 Summary Entry

Cash (received from customers) 145,000

Accounts receivable ($34,000 – 24,000) 10,000

Sales revenue (given) 155,000

2Property, Plant, & Equipment

________________________________________________________________

Beginning balance 247

3 Summary Entry

Cash (sale of equipment) 31,000

Accumulated depreciation (determined below) 22,000

P, P, & E (given) 40,000

Gain on sale of equipment (given) 13,000

Accumulated Depreciation

21–88 Intermediate Accounting, 8/e

Problem 21–13 (concluded)

4 Summary Entry

Retained earnings (determined below) 15,000

Retained Earnings

_______________________________________________________________

91 Beginning balance

5 Summary Entry

Bonds payable (determined below) 17,000

Cash 17,000

Bonds Payable

Problem 21–14

SURMISE COMPANY

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 40 (16) 5 45

Liabilities:

Accounts payable 32 (7) 15 17

Accrued liabilities 10 (9) 12 (2)

X Noncash investing and financing activity.

Problem 21–14 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Operating activities:

Net income (1) 50

Adjustments for noncash effects:

Net cash flows 40

Investing activities:

Purchase of LT investment (10) 40

Net cash flows (40)

Financing activities:

Issuance of note payable (12) 35

Problem 21–14 (concluded)

SURMISE COMPANY

Statement of Cash Flows

For year ended December 31, 2016 ($ in millions)

Cash flows from operating activities:

Net income $ 50

Adjustments for noncash effects:

Depreciation expense 22

Cash flows from investing activities:

Purchase of long-term investment (40)

Net cash flows from investing activities (40)

Cash flows from financing activities:

Issuance of note payable 35

Net increase in cash 5

Cash balance, January 1 40

Cash balance, December 31 $45

21–92 Intermediate Accounting, 8/e

Problem 21–15

Part A: Assuming both companies use current GAAP, not applying the proposed

Accounting Standards Update for lease accounting described in the Chapter

15 Supplement.

Requirement 1

Digital would report the cash inflow of $28,329,472 from the sale of the bonds as a

June 30, 2016*

Interest expense (6% x $28,329,472) ...................... 1,699,768

December 31, 2016**

Interest expense (6% x [$28,329,472 + 99,768]) ..... 1,705,754

Discount on bonds payable (difference) ......... 105,754

Problem 21–15 (continued)

Requirement 2

Calculation of the present value of lease payments

$391,548 x 15.32380t = $6,000,000

(rounded)

t Present value of an annuity due of $1: n = 20, i = 3% (from Table 6)

Midsouth would report the $6,000,000* investment in the switching equipment and its

financing with a capital lease as a significant noncash investing and financing activity

Calculations:

September 30, 2016*

Leased equipment (calculated above) .............................. 6,000,000

December 31, 2016**

Interest expense (3% x [$6 million – 391,548]) ................ 168,254

Problem 21–15 (continued)

Requirement 3

Digital would report the $6,000,000* direct financing lease of the switching

equipment as a significant noncash investing activity (acquiring one asset and

disposing of another) in the disclosure notes to the financial statements.

Calculations:

September 30, 2016*

Lease receivable (PV of lease payments) .......................... 6,000,000

Inventory of equipment (lessor’s cost) ......................... 6,000,000

December 31, 2016**

Cash (rental payment) ....................................................... 391,548

Problem 21–15 (continued)

Requirement 4

MDS would report the $6,000,000* sales-type lease of the switching equipment

as a significant noncash activity in the disclosure notes to the financial

statements.

The $783,096 ($391,548* + 391,548**) cash lease payments is considered to be

Note: By the indirect method of reporting cash flows from operating activities,

the $1,000,000 (sales revenue: $6,000,000 – cost of goods sold:

The $168,254 interest revenue that increased net income actually did

increase cash [the interest portion of the $783,096 ($391,548 x 2) cash

Noncash adjustments to convert net income to cash flows from

operating activities:

Increase in lease receivable ........................... ($6,000,000)

21–96 Intermediate Accounting, 8/e

Problem 21–15 (concluded)

Calculations:

September 30, 2016*

Lease receivable (present value) ....................................... 6,000,000

December 31, 2016**

Cash (rental payment) ....................................................... 391,548

Problem 21–15 (continued)

Part B: Assuming both companies use the proposed Accounting Standards

Update for lease accounting described in the Chapter 15 Supplement.

Requirement 1

Digital would report the cash inflow of $28,329,472 from the sale of the bonds as a

June 30, 2016*

Interest expense (6% x $28,329,472) ...................... 1,699,768

December 31, 2016**

Interest expense (6% x [$28,329,472 + 99,768]) ...... 1,705,754

Problem 21–15 (continued)

Requirement 2

Calculation of the present value of lease payments

Midsouth would report the $6,000,000* investment in the switching equipment and its

financing with a lease as a significant noncash investing and financing activity in the

disclosure notes to the financial statements.

The $783,096 ($391,548* + 391,548**) cash lease payments are divided into the

interest portion and the principal portion. The interest portion, $168,254, from

Calculations:

September 30, 2016*

Right-of-use equipment (calculated above) ...................... 6,000,000

Lease payable (calculated in above) .............................. 6,000,000

December 31, 2016**

Interest expense (3% x [$6 million – 391,548]) ................. 168,254

Lease payable (difference) ............................................... 223,294

Cash (rental payment) ................................................... 391,548

Problem 21–15 (continued)

Requirement 3

A lessor classifies its cash receipts from lease payments as operating activities

in its statement of cash flows after initially reporting its acquisition of a lease

receivable and derecognition of the leased asset as a supplemental noncash

Calculations:

September 30, 2016*

Lease receivable (PV of lease payments) ......................... 6,000,000

Inventory of equipment (lessor’s cost) ........................ 6,000,000

December 31, 2016**

Cash (rental payment)....................................................... 391,548

21–100 Intermediate Accounting, 8/e

Problem 21–15 (concluded)

Requirement 4

MDS would report the $6,000,000* lease of the switching equipment as a

noncash transaction in the disclosure notes to the financial statements.

Calculations:

September 30, 2016*

Lease receivable (present value) ....................................... 6,000,000

December 31, 2016**

Cash (rental payment) ....................................................... 391,548