Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 21–2

WRIGHT COMPANY

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 30 (15) 12 42

Liabilities:

Accounts payable 35 (2) 7 28

Salaries payable 5 (3) 3 2

Interest payable 3 (5) 2 5

Statement of Income

Revenues:

Sales revenue (1) 380 380

Expenses:

Cost of goods sold (2) 130 (130)

Salaries expense (3) 45 (45)

21–62 Intermediate Accounting, 8/e

Problem 21–2 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Operating activities:

Cash inflows:

From customers (1) 382

Investing activities:

Sale of land (6) 7

Financing activities:

Repayment of notes payable (11) 30

Sale of bonds payable (12) 60

Problem 21–2 (concluded)

WRIGHT COMPANY

Statement of Cash Flows

For year ended December 31, 2016 (in $000)

Cash flows from operating activities:

Cash inflows:

From customers $382

Cash outflows:

Cash flows from investing activities:

Sale of land 7

Cash flows from financing activities:

Repayment of notes payable (30)

Sale of bonds payable 60

Net increase in cash 12

Cash balance, January 1 30

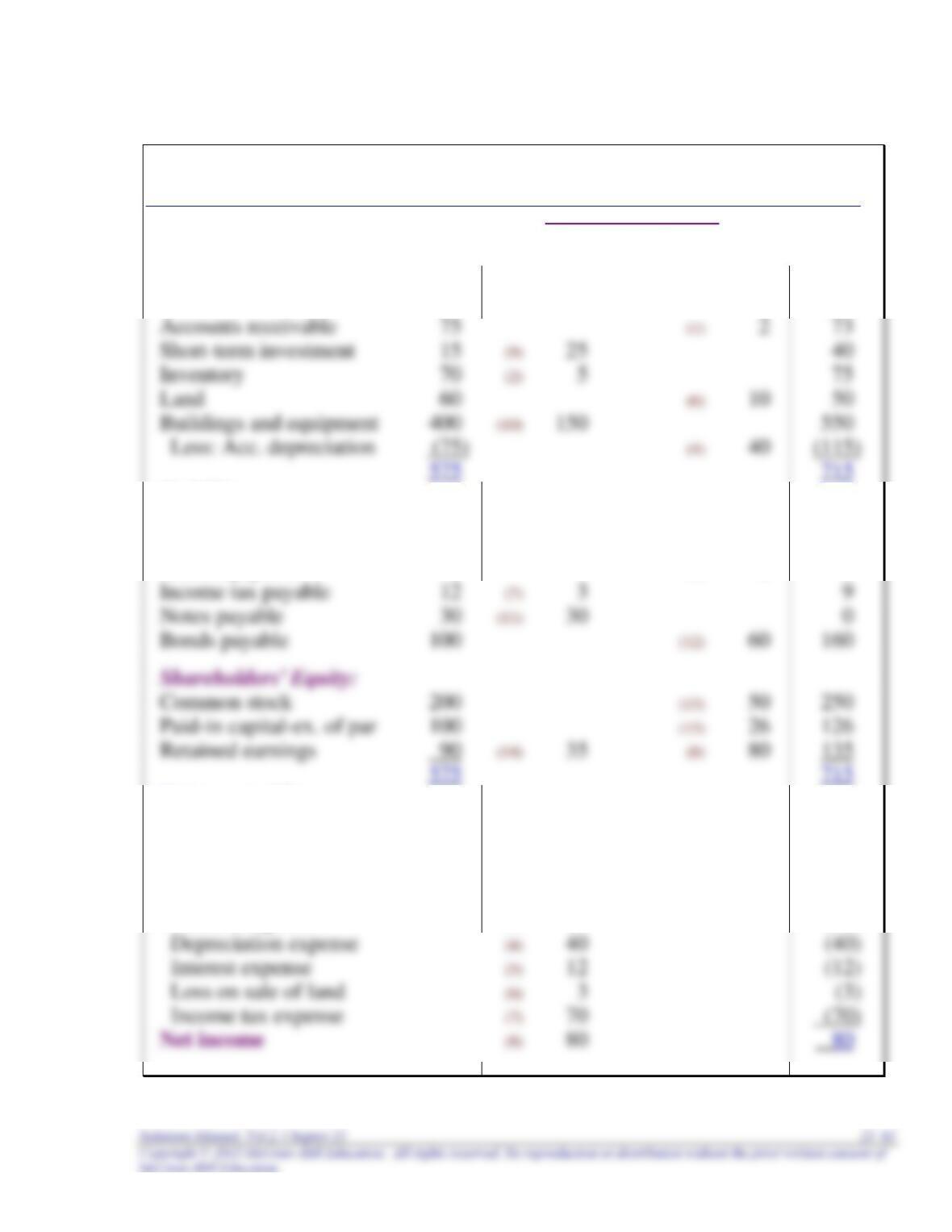

Problem 21–3

NATIONAL INTERCABLE COMPANY

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 55 (18) 14 69

Accounts receivable 164 (1) 9 173

Liabilities:

Accounts payable 45 (4) 15 30

Salaries payable 8 (5) 5 3

Shareholders' Equity:

Common stock 290 (15) 20 310

Problem 21–3 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Income

Revenues:

Sales revenue (1) 320 320

Expenses:

Cost of goods sold (4) 125 (125)

Net income (12) 22 22

21–66 Intermediate Accounting, 8/e

Problem 21–3 (continued)

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Operating activities:

Cash inflows:

From customers (1) 311

Investing activities:

Sale of long-term investment (3) 35

Sale of building parts (11) 3

Net cash flows 38

Financing activities:

Retirement of bonds payable (14) 130

Problem 21–3 (concluded)

NATIONAL INTERCABLE COMPANY

Statement of Cash Flows

For year ended December 31, 2016 ($ in millions)

Cash flows from operating activities:

Cash inflows:

From customers $311

Cash flows from investing activities:

Sale of building parts 3

Cash flows from financing activities:

Retirement of bonds payable (130)

Net increase in cash 14

Cash balance, January 1 55

Cash balance, December 31 $ 69

Noncash investing and financing activities:

Problem 21–4

DUX COMPANY

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 20 (17) 13 33

Accounts receivable 47 (1) 3 44

Liabilities:

Accounts payable 20 (3) 7 13

Salaries payable 5 (4) 3 2

Interest payable 2 (6) 2 4

Shareholders' Equity:

Common stock 200 (14) 10 210

Paid-in capital—ex. of par 20 (14) 4 24

X Noncash investing and financing activity.

Problem 21–4 (continued)

Spreadsheet for the Statement of Cash Flows (continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Income

Revenues:

Sales revenue (1) 200 200

Dividend revenue (2) 3 3

Expenses:

Cost of goods sold (3) 120 (120)

Net income (9) 25 25

Statement of Cash Flows

Operating activities:

Cash inflows:

From customers (1) 203

Net cash flows 22

Investing activities:

Sale of building (7) 7

Purchase of LT investment (10) 5

Purchase of equipment (12) 15

Net cash flows (13)

Financing activities:

Sale of bonds payable (13) 25

21–70 Intermediate Accounting, 8/e

Problem 21–4 (concluded)

DUX COMPANY

Statement of Cash Flows

For year ended December 31, 2016 ($ in 000s)

Cash flows from operating activities:

Cash inflows:

From customers $203

Cash flows from investing activities:

Sale of building 7

Purchase of long-term investment (5)

Cash flows from financing activities:

Sale of bonds payable 25

Net increase in cash 13

Cash balance, January 1 20

Cash balance, December 31 $33

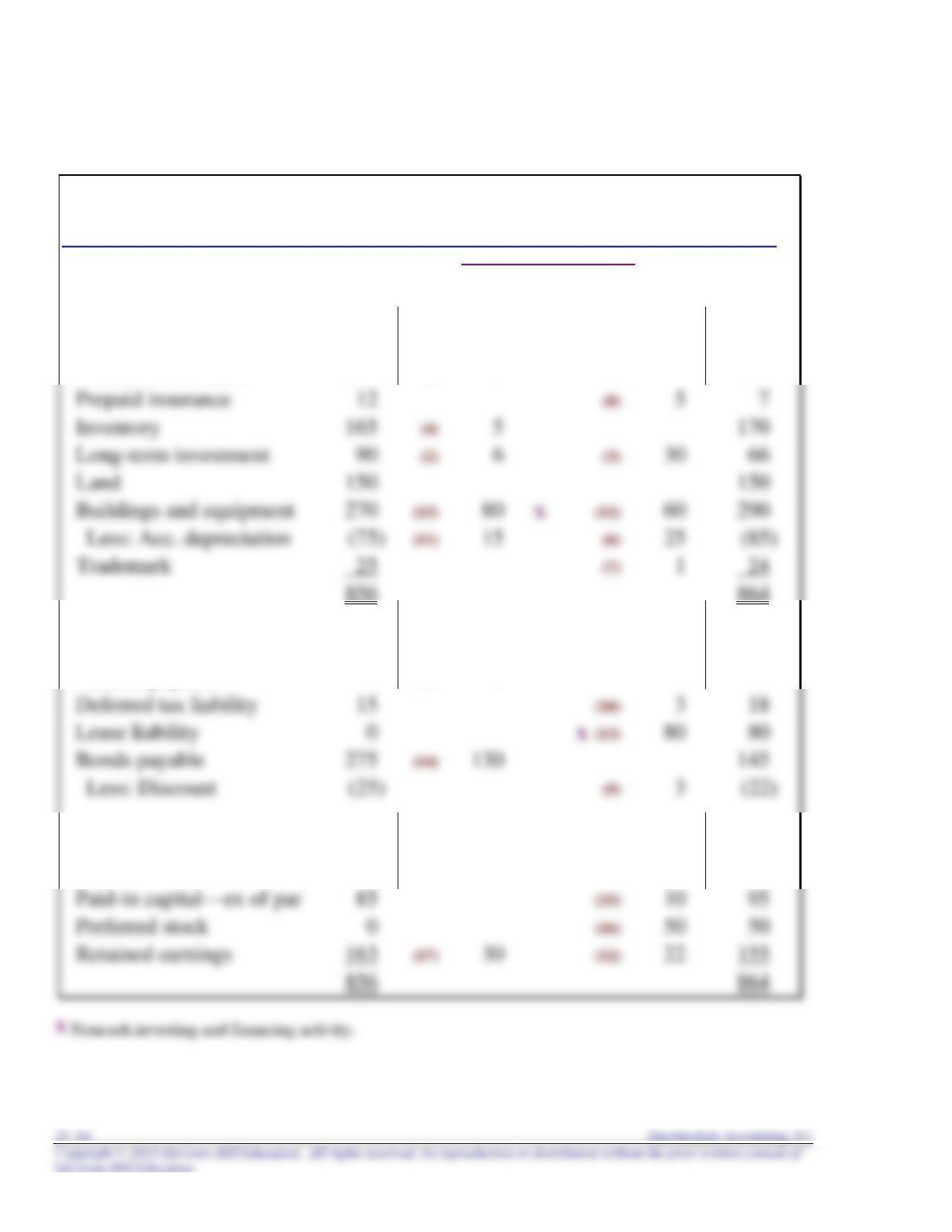

Problem 21–5

METAGROBOLIZE INDUSTRIES

Spreadsheet for the Statement of Cash Flows

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 375 (14) 225 600

Accounts receivable 450 (1) 150 600

Liabilities:

Accounts payable 450 (4) 300 750

Accrued expenses 225 (9) 75 300

Lease liability—land 0 X (2) 150 150

Shareholders' Equity:

Common stock 3,000 (12) 150 3,150

Income Statement

Revenues:

Sales revenue (1) 2,645 2,645

Gain on sale of land (3) 90 90

Expenses:

Cost of goods sold (4) 600 (600)

Problem 21–5 (continued)

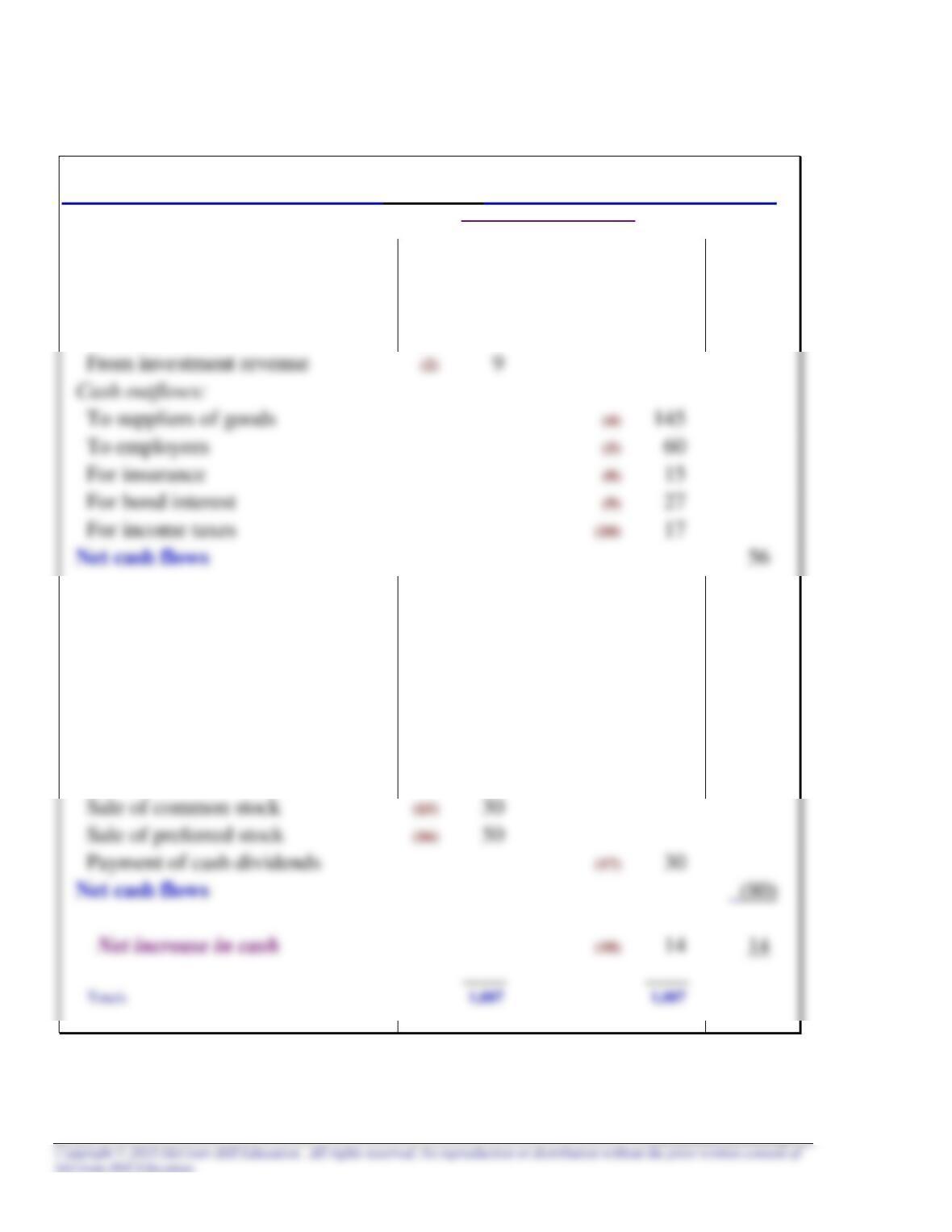

Spreadsheet for the Statement of Cash Flows

(continued)

Dec.31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Operating activities:

Cash inflows:

From customers (1) 2,495

Financing activities:

Payment of cash dividends (13) 450

Net cash flows (450)

Net increase in cash (14) 225 225

Totals 8,155 8,155

Problem 21–5 (concluded)

METAGROBOLIZE INDUSTRIES

Statement of Cash Flows

For year ended December 31, 2016 ($ in 000)

Cash flows from operating activities:

Cash inflows:

From customers $2,495

Cash flows from investing activities:

Purchase of equipment (900)

Cash flows from financing activities:

Payment of cash dividends (450)

Net cash flows from financing activities (450)

Net increase in cash 225

21–74 Intermediate Accounting, 8/e

Problem 21–6

Requirement 1

a. Summary Entry Cash (received from customers) 155

Accounts receivable 5

Sales revenue 150

d. Summary Entry Interest expense 6

Discount on bonds payable 3

Cash (paid for interest) 3

Depreciation expense, bad debt expense, the gain on sale of equipment, and the loss

on sale of land are not cash outflows.

Problem 21–6 (concluded)

Requirement 2

Cash Flows from Operating Activities:

Cash received from customers $155

Cash paid to suppliers (87)

Problem 21–7

Cash Flows from Operating Activities:

Cash received from customers $316a

Cash increase from sale of cash equivalents 2b

a. Summary Entry Cash (received from customers) 316

b.

The gain on sale of cash equivalents indicates that total cash increased as a result of

converting cash in one form (say a $10 million treasury bill) to cash in another form

(checking account)*:

Summary Entry Cash [checking account] 12

[*Any other example you think of that involves a gain on sale of cash equivalents would work as well.]

c. Summary Entry Cost of goods sold 120

Inventory 12

Problem 21–7 (concluded)

f. Summary Entry Insurance expense 20

Prepaid insurance 4

Cash (paid for insurance ) 16

21–78 Intermediate Accounting, 8/e

Problem 21–8

Direct Method

Cash Flows from Operating Activities:

Cash received from customers $692

Cash paid to suppliers (103)

Net cash flows from

operating activities $350

Indirect Method

Cash Flows from Operating Activities:

Net income $ 88

Adjustments for noncash effects:

Depreciation expense 123

Changes in operating assets and liabilities:

Increase in accounts receivable (108)

Decrease in inventory 104

Problem 21–9

Direct Method

Cash Flows from Operating Activities:

Cash received from customers $926

Cash paid to suppliers (384)

Indirect Method

Cash Flows from Operating Activities:

Net income $ 40

Adjustments for noncash effects:

Depreciation expense 190

Inventory loss 12

Changes in operating assets and liabilities:

Decrease in accounts receivable 26

Problem 21–10

1. Cash received from customers $306

2. Cost of goods sold $180

3. ? in salaries payable Increase