Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 20-3

This is a change in accounting principle.

($ in millions)

Common stock ($1 par x 4 million shares retired)......................... 4

UMC applies the new way of reporting reacquired shares retrospectively; that is,

to all prior periods as if it always had used that method. In other words, all financial

statement amounts for individual periods affected by the change and that are included

20–22 Intermediate Accounting, 8/e

Exercise 20-4

Requirement 1

($ in millions)

Investment in equity securities ($48 million – 31 million) ........... 17

Retained earnings (investment revenue from the equity method) 17

Requirement 2

Financial statements would be recast to reflect the equity method for each year

Requirement 3

When a company changes from the equity method, no adjustment is made to the

book value of the investment. Instead, the equity method is simply discontinued,

Exercise 20-5

Requirement 1

Access FASB Accounting Codification

Requirement 2

The specific citation that describes the guidelines for how to account for a change

Requirement 3

35-33 An investment in common stock of an investee that was previously

accounted for on other than the equity method may become qualified for use of the

equity method by an increase in the level of ownership (that is, acquisition of

Exercise 20-6

The FASB Accounting Standards Codification represents the single source of

1. Reporting most changes in accounting principle:

”

2. Disclosure requirements for a change in accounting principle:

3. Illustration of the application of a retrospective change in the method of

accounting for inventory:

Exercise 20-7

Requirement 1

($ in millions)

Inventory (additional amount due

Requirement 2

2016 2015

Income before income taxes $10.0 $8.0

20–26 Intermediate Accounting, 8/e

Exercise 20-7 (continued)

Requirement 3

Besides net income, which was reported in 2015 as $3 million ($5 million less tax)

and now revised to $4.8 million, other amounts that would be revised to reflect

accounting by the FIFO costing method are:

Earnings per share

The reason for the credit to deferred tax liability requires you to reflect back on

what you learned about accounting for income taxes. The reason is that an

accounting method used for tax purposes cannot be changed retrospectively for

Exercise 20-7 (concluded)

Requirement 4

In the retained earnings column of the comparative statements of shareholders’

equity, the beginning balance of 2015 retained earnings is revised to include any

adjusted as follows (not required):

Millington Supplies

Statement of Shareholders’ Equity

For the Years Ended Dec. 31, 2016 and 2015

($ in millions)

Common

Stock

Additional

Paid-in

Capital

Retained

Earnings

Total

Shareholders’

Equity

Balance at Jan. 1

9.0*

Net income

4.8

Exercise 20-8

Requirement 1

To record the change: ($ in millions)

Retained earnings (cost of goods sold higher; 2015 net income lower) 6

Inventory (cost of goods sold higher; inventory lower) .............. 6

Requirement 2

Flay is unable to apply the LIFO cost method retrospectively. It does, however,

have sufficient information to apply the new method prospectively beginning in 2015.

Requirement 3

($ in millions) 2016 2015 2014

Exercise 20-9

Requirement 1

To record the change: ($ in millions)

Retained earnings ($23 million plus $7 million) .......................... 30

Inventory (cost of goods sold higher; inventory lower) ............... 30

Requirement 2

If it is impracticable to revise all specific years reported, a change is applied

retrospectively as of the earliest year practicable. Wolfgang has information that

would allow it to revise all assets and liabilities on the basis of LIFO for 2015 in its

Requirement 3

($ in millions) 2016 2015 2014

20–30 Intermediate Accounting, 8/e

Exercise 20-10

Requirement 1

In general, we report voluntary changes in accounting principles retrospectively.

However, a change in depreciation method is considered a change in accounting

estimate resulting from a change in accounting principle. In other words, a change in

Requirement 2

Asset’s cost $2,560,000

Accumulated depreciation to date (given) (1,801,000)

Adjusting entry (2016):

Depreciation expense (calculated above) .......................... 200,000

Exercise 20-11

Requirement 1

In general, we report voluntary changes in accounting principles retrospectively.

However, a change in depreciation method is considered a change in accounting

estimate resulting from a change in accounting principle. In other words, a change in

Requirement 2

Asset’s cost $800,000

Accumulated depreciation to date ($160,000 x 2) (320,000)

Adjusting entry:

Depreciation expense (calculated above) .......................... 240,000

Accumulated depreciation ....................................... 240,000

Not required:

Exercise 20-12

Requirement 1

April 1, 2016

Cash ........................................................................................ 36,000

Receivable—royalty revenue ............................................ 31,000

Royalty revenue ................................................................ 5,000

Requirement 2

The fact that more royalty revenue was received in April than anticipated in

Exercise 20-13

1. This is a change in estimate.

To revise the liability on the basis of the new estimate:

Exercise 20-14

Requirement 1

Accrued liability and expense

Warranty expense (3% x $3,600,000) ............................................... 108,000

Requirement 2

Actual expenditures (summary entry)

Estimated warranty liability ($50,000 – 23,000) ........................ 27,000

Exercise 20-15

Requirement 1

A deferred tax liability is established using the currently enacted tax rate for the

($ in millions)

Income tax expense (to balance)................................................ 10

Requirement 2

When a company revises a previous estimate, prior financial statements are not

Exercise 20-16

Requirement 1

This is a change in accounting estimate.

Requirement 2

When an estimate is revised as new information comes to light, accounting for the

Requirement 3

$800,000 Cost

$160,000 Old annual depreciation ($800,000 ÷ 5 years)

20–36 Intermediate Accounting, 8/e

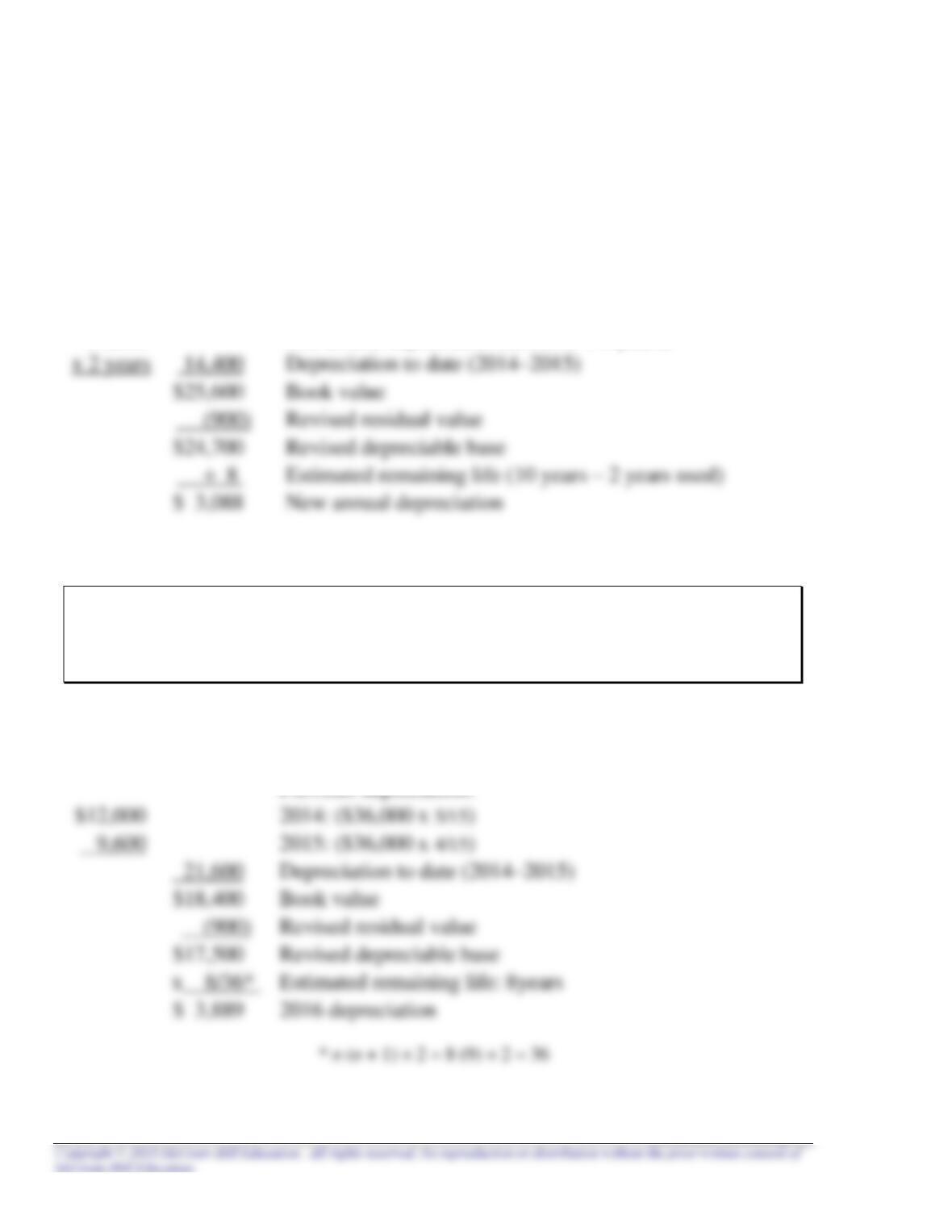

Exercise 20-17

Requirement 1

Depreciation expense (determined below) .. 3,088

Accumulated depreciation .................. 3,088

Calculation of annual depreciation after the estimate change:

$40,000 Cost

$7,200 Old annual depreciation ($36,000 ÷ 5 years)

Requirement 2

Depreciation expense (determined below) .. 3,889

Accumulated depreciation................... 3,889

Calculation of annual depreciation after the estimate change:

$40,000 Cost

Exercise 20-18

EP 1. Change from declining balance depreciation to straight-line.

E 2. Change in the estimated useful life of office equipment.

R 7. Including in the consolidated financial statements a subsidiary acquired

several years earlier that was appropriately not included in previous

years.

Exercise 20-19

Requirement 1

The 2014 error caused 2014 net income to be understated, but since 2014 ending

Analysis: U = Understated

O = Overstated

2014 2015

Beginning inventory → Beginning inventory U

Plus: net purchases Plus: net purchases

Exercise 20-19 (concluded)

However, the 2015 error has not yet self-corrected. Both retained earnings and

inventory still are overstated as a result of the second error.

Analysis: U = Understated

O = Overstated

2015

Beginning inventory

Requirement 2

Retained earnings (overstatement of 2015 income) ........................ 150,000

Requirement 3

The financial statements that were incorrect as a result of both errors (effect of

Exercise 20-20

1. Error discovered before the books are adjusted or closed in 2016.

2. Error not discovered until early 2017.