Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

ACCRUALS

Accruals involve transactions where the cash outflow or

inflow occurs in a period subsequent to expense or revenue

recognition.

➢ ACCRUED LIABILITIES

Accrued liabilities represent liabilities recorded when an expense has

been incurred prior to cash payment.

July 31

Salaries expense .................................. 5,500

To accrue interest expense for July on notes payable.

T2-9

Instructors Resource Manual 2-17

➢ ACCRUED RECEIVABLES

Accrued receivables involve situations when the revenue is recognized

in a period prior to the cash receipt. Assume that Dress Right loaned

August 31

T2-9 (continued)

ESTIMATES

Estimates often are made to comply with the accrual

T2-10

ADJUSTED TRIAL BALANCE

DRESS RIGHT CLOTHING CORPORATION

Adjusted Trial Balance

July 31, 2016

Account Title

Debits

Credits

Cash

68,500

Accounts receivable

2,000

Supplies

1,200

Notes payable

40,000

Deferred rent revenue

750

Salaries payable

5,500

Interest payable

333

Common stock

60,000

Retained earnings

1,000

Sales revenue

38,500

Illustration 2-12

T2-11

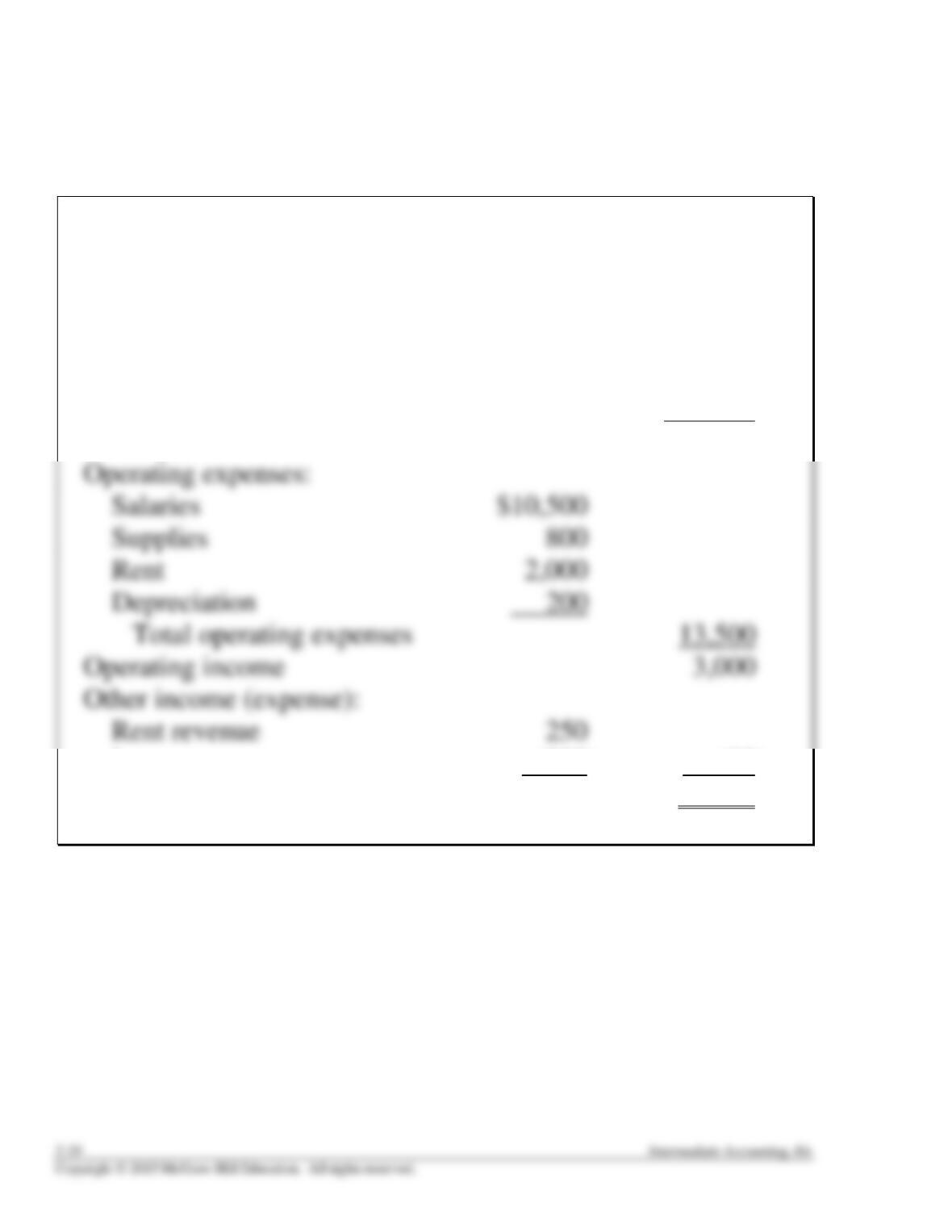

THE INCOME STATEMENT

DRESS RIGHT CLOTHING CORPORATION

Income Statement

For the Month of July 2016

Sales revenue $38,500

Cost of goods sold 22,000

Gross profit 16,500

Interest expense (333) (83)

Net income $2,917

Illustration 2-13

T2-12

THE BALANCE SHEET

DRESS RIGHT CLOTHING CORPORATION

Balance Sheet

At July 31, 2016

Assets

Current assets:

Cash $ 68,500

Accounts receivable 2,000

Supplies 1,200

Liabilities and Shareholders’ Equity

Current liabilities:

Accounts payable $ 35,000

Salaries payable 5,500

Deferred rent revenue 750

Illustration 2-10

T2-14

THE STATEMENT OF CASH FLOWS

DRESS RIGHT CLOTHING CORPORATION

Statement of Cash Flows

For the Month of July 2016

Cash Flows from Operating Activities:

Cash inflows:

From customers $ 36,500

Cash Flows from Investing Activities:

Purchase of furniture and fixtures (12,000)

Cash Flows from Financing Activities:

Issue of common stock $ 60,000

Net increase in cash $68,500

Illustration 2-15

T2-14

THE STATEMENT OF SHAREHOLDERS' EQUITY

DRESS RIGHT CLOTHING CORPORATION

Statement of Shareholders' Equity

For the Month of July 2016

Total

Common Retained Shareholders’

Stock Earnings Equity

Illustration 2-16

T2-15

THE CLOSING PROCESS

To close the revenue accounts to income summary

Sales revenue .............................................. 38,500

To close the expense accounts to income summary

Income summary ........................................ 35,833

Cost of goods sold .................................. 22,000

Income Summary

To close income summary to retained earnings

Income summary ........................................ 2,917

Retained earnings .................................... 2,917

T2-16

POST-CLOSING TRIAL BALANCE

DRESS RIGHT CLOTHING CORPORATION

Post-Closing Trial Balance

July 31, 2016

Account Title

Debits

Credits

Cash

68,500

Accounts receivable

2,000

Supplies

1,200

Prepaid rent

22,000

T2-17

CONVERSION FROM CASH TO ACCRUAL

Converting from cash to accrual income:

➢ Add (deduct) increases (decreases) in assets. For example, an increase in

accounts receivable means that the company recognized more revenue

The Krinard Cleaning Services Company maintains its records on the cash basis,

with one exception. The company reports equipment as an asset and records

January 1, 2016 December 31, 2016

Accounts receivable $16,000 $25,000

Prepaid expenses 7,000 4,000

Accrual net income is $68,500, determined as follows:

Cash-basis net income $63,000

Illustration 2-18

T2-18

Instructors Resource Manual 2-27

Copyright © 2015 McGraw-Hill Education. All rights reserved.

Suggestions for Class Activities

1. Spreadsheet Activities

2. Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, analysis and judgment skills.

Communication Skills. In addition to Communication Case 2-3, Judgment Cases 2-1 and 2-2 can

Assignment Chart

Learning Est. time

Questions Objective(s) Topic (min.)

2-1

1

External and internal events

5

2-2

1

Dual effect of transactions on financial position

5

2-9

3

Posting

5

2-10

2

Journal entries

5

2-11

3,5

Trial balance

5

2-12

4

Adjusting entries

5

2-13

7

Closing entries

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

2-1

1

Transaction analysis

10

2-2

2

Journal entries

10

2-3

3

T-accounts

15

Learning Est. time

Exercises Objective(s) Topic (min.)

2-1

1

Transaction analysis

15

2-2

2

Journal entries

15

2-3

3

T-accounts and trial balance

15

2-11

5

Adjusting entries

15

2-12

6,7

Financial statements and closing entries

20

2-13

7

Closing entries

10

2-14

7

Closing entries

10

CPA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

1

The effect of a transaction on the accounting

equation

3

Learning Est. time

Problems Objective(s) Topic (min.)

2-1

2,3

Accounting cycle through unadjusted trial

balance

40

2-2

2,3

Accounting cycle through unadjusted trial

40

Star Problems

Learning Est. time

Cases Objective(s) Topic (min.)

Judgment Case 2-1

4,8

Cash versus accrual; adjusting entries

20