Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Question 2–1

External events involve an exchange transaction between the company and a

Question 2–2

According to the accounting equation, there is equality between the total

Question 2–3

The purpose of a journal is to capture, in chronological order, the dual effect of a

Question 2–4

Permanent accounts represent the financial position of a company—assets,

Question 2–5

Assets are increased by debits and decreased by credits. Liabilities and equity

accounts are increased by credits and decreased by debits.

Chapter 2 Review of the Accounting Process

QUESTIONS FOR REVIEW OF KEY TOPICS

2–2 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 2–6

Revenues and gains are increased by credits and decreased by debits. Expenses

Question 2–7

The first step in the accounting processing cycle is to identify external

Question 2–8

Transaction analysis is the process of reviewing the source documents to

Question 2–9

Question 2–10

Transaction 1 records the purchase of $20,000 of inventory on account.

Question 2–11

An unadjusted trial balance is a list of the general ledger accounts and their

Answers to Questions (continued)

Question 2–12

Adjusting entries record the effect on financial position of internal events, those

Question 2–13

Closing entries transfer the balances in the temporary owners’ equity accounts to

Question 2–14

Prepaid expenses represent assets recorded when a cash disbursement creates

Question 2–15

The adjusting entry required when deferred revenues are earned is a debit to the

Question 2–16

Accrued liabilities are recorded when an expense has been incurred that will not

Answers to Questions (continued)

Question 2–17

Income statement—The purpose of the income statement is to summarize the

profit-generating activities of the company during a particular period of time. It is a

change statement that is reporting the changes in owners’ equity that occurred during

Question 2–18

A worksheet provides a means of organizing the accounting information needed

Question 2–19

Reversing entries are recorded at the beginning of a reporting period. They

Answers to Questions (concluded)

Question 2–20

The purpose of special journals is to record, in chronological order, the dual

effect of repetitive types of transactions, such as cash receipts, cash disbursements,

Question 2–21

The general ledger is a collection of control accounts representing assets,

liabilities, permanent and temporary shareholders’ equity accounts. The subsidiary

ledger contains a group of subsidiary accounts associated with a particular general

2–6 Intermediate Accounting, 8/e

Brief Exercise 2–1

Assets = Liabilities + Paid-in Capital + Retained Earnings

1. + 165,000 (inventory) + 165,000 (accounts payable)

2. – 40,000 (cash) – 40,000 (expense)

Brief Exercise 2–2

1. Inventory .................................................................. 165,000

Accounts payable ................................................. 165,000

2. Salaries expense ....................................................... 40,000

BRIEF EXERCISES

Brief Exercise 2–3

BALANCE SHEET ACCOUNTS

Cash Accounts receivable

___________________________ ___________________________

6/1 Bal. 65,000 6/1 Bal. 43,000

4. 180,000 40,000 2. 3. 200,000 180,000 4.

INCOME STATEMENT ACCOUNTS

Sales revenue Cost of goods sold

___________________________ ___________________________

0 6/1 Bal. 6/1 Bal. 0

200,000 3. 3. 120,000

Brief Exercise 2–4

1. Prepaid insurance ..................................................... 12,000

Brief Exercise 2–5

1. Insurance expense ($12,000 x 3/12) ............................. 3,000

Brief Exercise 2–6

Brief Exercise 2–7

1. Service revenue ....................................................... 4,000

Deferred service revenue ..................................... 4,000

Brief Exercise 2–8

Assets would be higher by $1,000, the amount of prepaid advertising that

expired during the month. Liabilities would be lower by $21,600 ($4,000 + 16,000 +

Brief Exercise 2–9

1. Interest receivable .................................................... 2,250

Interest revenue ($50,000 x 6% x 9/12) .................... 2,250

2–10 Intermediate Accounting, 8/e

Brief Exercise 2–10

BOWLER CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ...............................................

$325,000

Cost of goods sold .......................................

168,000

Brief Exercise 2–11

BOWLER CORPORATION

Balance Sheet

At December 31, 2016

Assets

Current assets:

Cash ...........................................................

$ 5,000

Liabilities and Shareholders' Equity

Current liabilities:

Accounts payable ......................................

$ 20,000

Salaries payable .........................................

12,000

2–12 Intermediate Accounting, 8/e

Brief Exercise 2–12

Sales revenue ................................................................... 850,000

Income summary ......................................................... 850,000

Income summary ............................................................. 815,000

Cost of goods sold ....................................................... 580,000

Brief Exercise 2–13

Revenues

$428,000*

Expenses:

Salaries

(240,000)

*$420,000 cash received plus $8,000 increase ($60,000 – 52,000) in amount due

from customers:

** $35,000 cash paid less $2,000 decrease in amount owed to utility company:

Exercise 2–1

Assets = Liabilities + Paid-in Capital + Retained Earnings

1. + 300,000 (cash) + 300,000 (common stock)

2. – 10,000 (cash)

+ 40,000 (equipment) + 30,000 (note payable)

EXERCISES

2–14 Intermediate Accounting, 8/e

Exercise 2–2

1. Cash .......................................................................... 300,000

Common stock ..................................................... 300,000

2. Equipment ................................................................ 40,000

5. Rent expense ............................................................ 5,000

Cash ...................................................................... 5,000

6. Prepaid insurance ..................................................... 6,000

Cash ...................................................................... 6,000

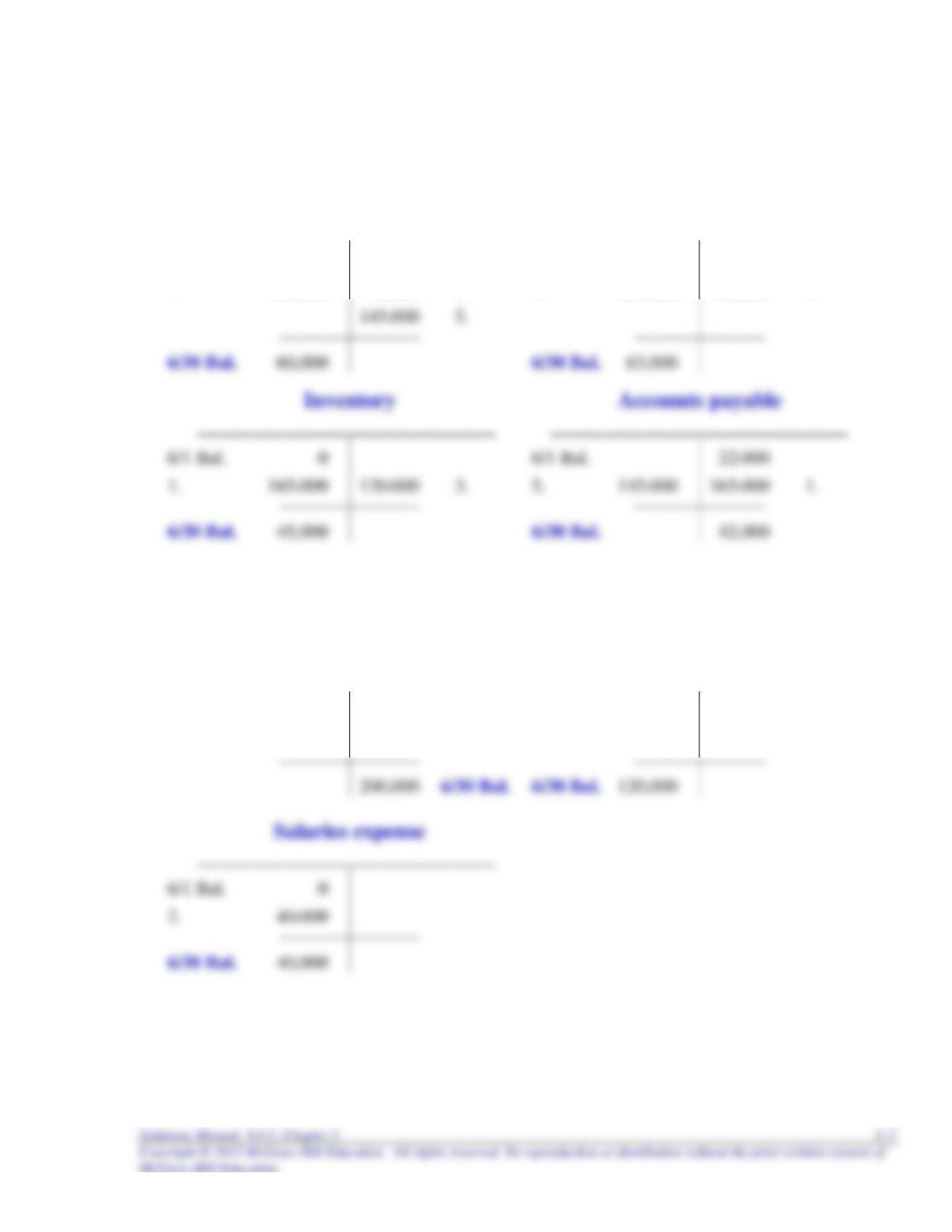

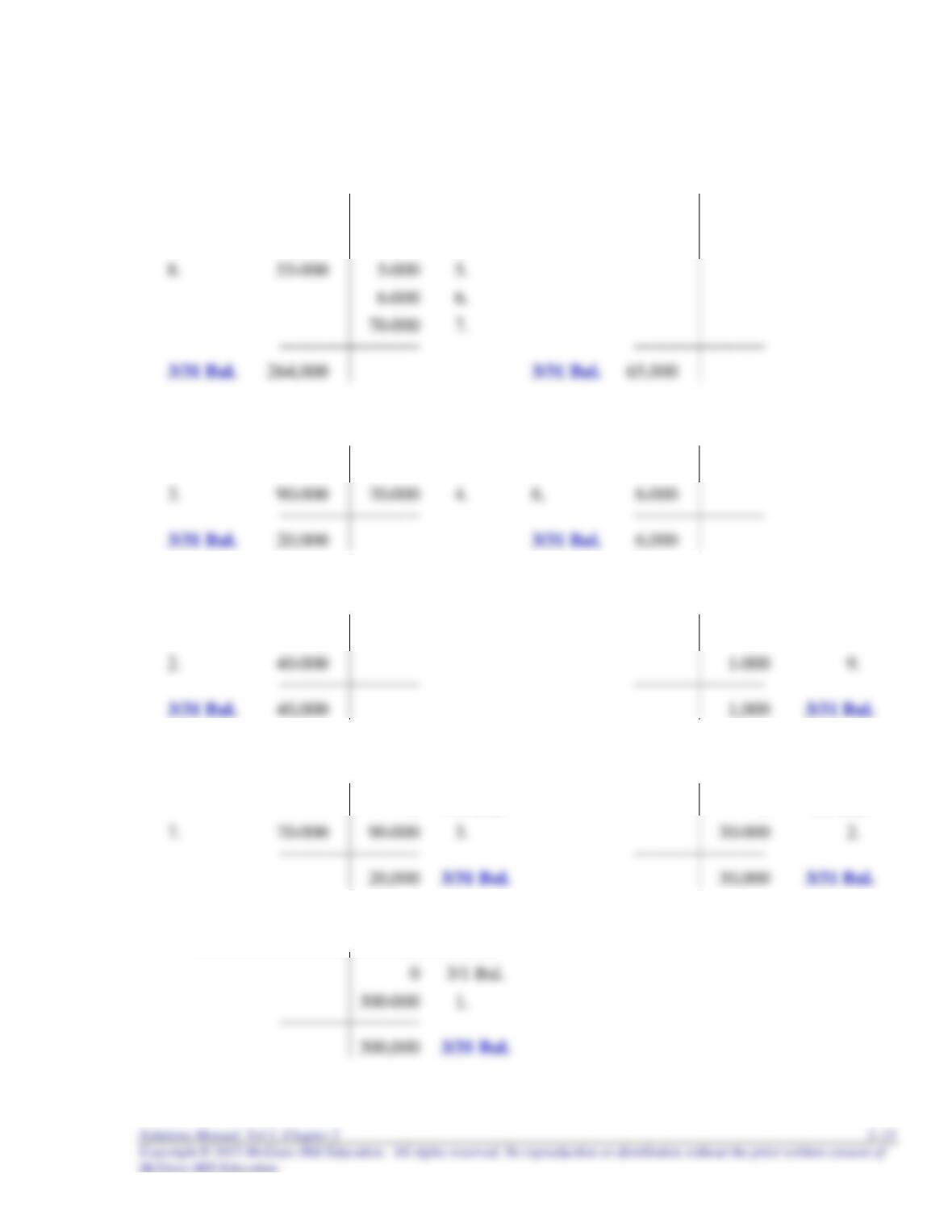

Exercise 2–3 BALANCE SHEET ACCOUNTS

Cash Accounts receivable

___________________________ ___________________________

3/1 Bal. 0 3/1 Bal. 0

1. 300,000 10,000 2. 4. 120,000 55,000 8.

Inventory Prepaid insurance

___________________________ ___________________________

3/1 Bal. 0 3/1 Bal. 0

Equipment Accumulated depreciation

___________________________ ___________________________

3/1 Bal. 0 0 3/1 Bal.

Accounts payable Note payable

___________________________ ___________________________

0 3/1 Bal. 0 3/1 Bal.

Common stock

___________________________

2–16 Intermediate Accounting, 8/e

Exercise 2–3 (concluded)

INCOME STATEMENT ACCOUNTS

Sales revenue Cost of goods sold

___________________________ ___________________________

0 3/1 Bal. 3/1 Bal. 0

Rent expense Depreciation expense

___________________________ ___________________________

3/1 Bal. 0 3/1 Bal. 0

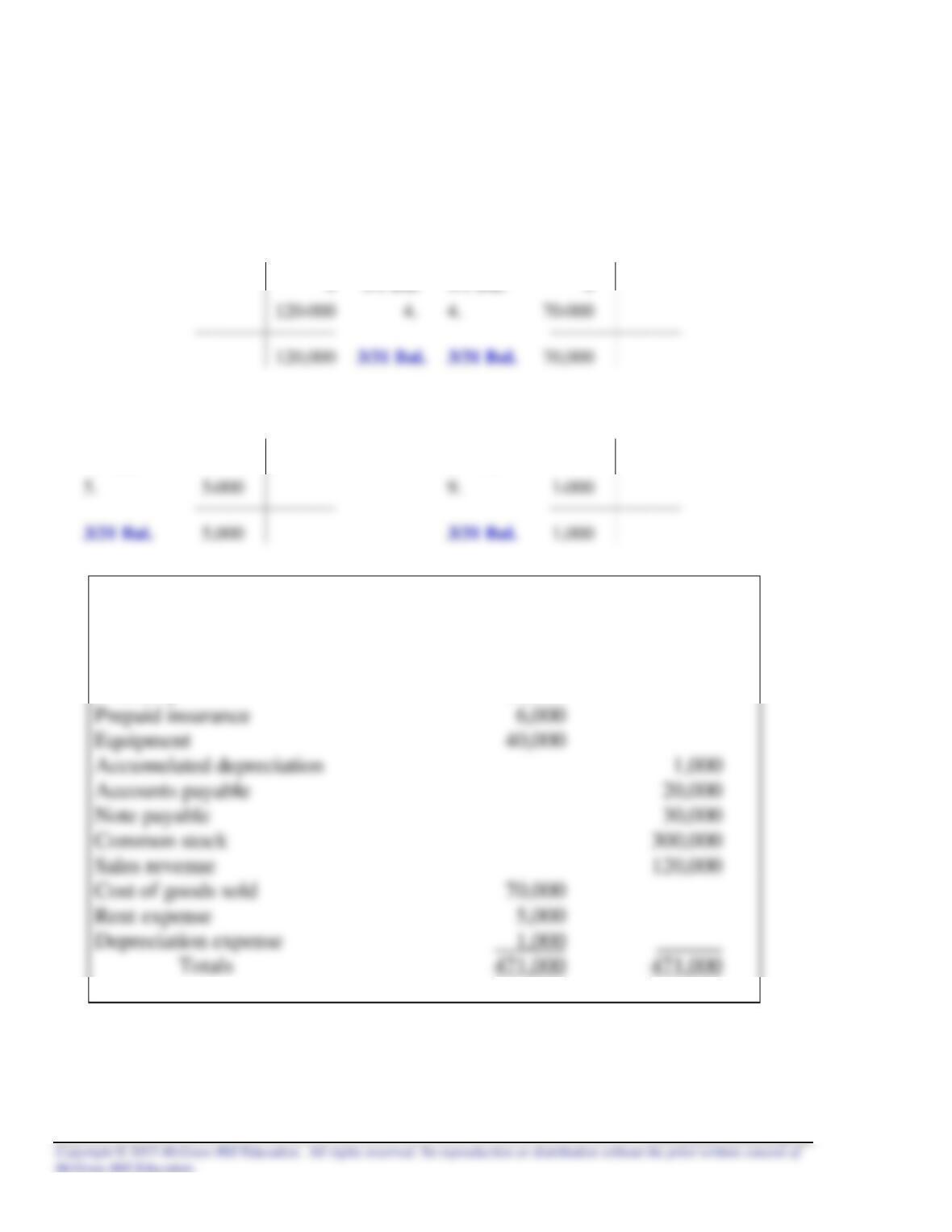

Account Title

Debits

Credits

Cash

264,000

Accounts receivable

65,000

Inventory

20,000

Exercise 2–4

1. Cash ...................................................................... 500,000

Common stock ................................................... 500,000

2. Furniture and fixtures ........................................... 100,000

Cash.................................................................... 40,000

Note payable ..................................................... 60,000

5. Rent expense ......................................................... 6,000

Cash.................................................................... 6,000

6. Prepaid insurance ................................................. 3,000

Cash.................................................................... 3,000

7. Accounts payable ................................................. 120,000

Cash.................................................................... 120,000

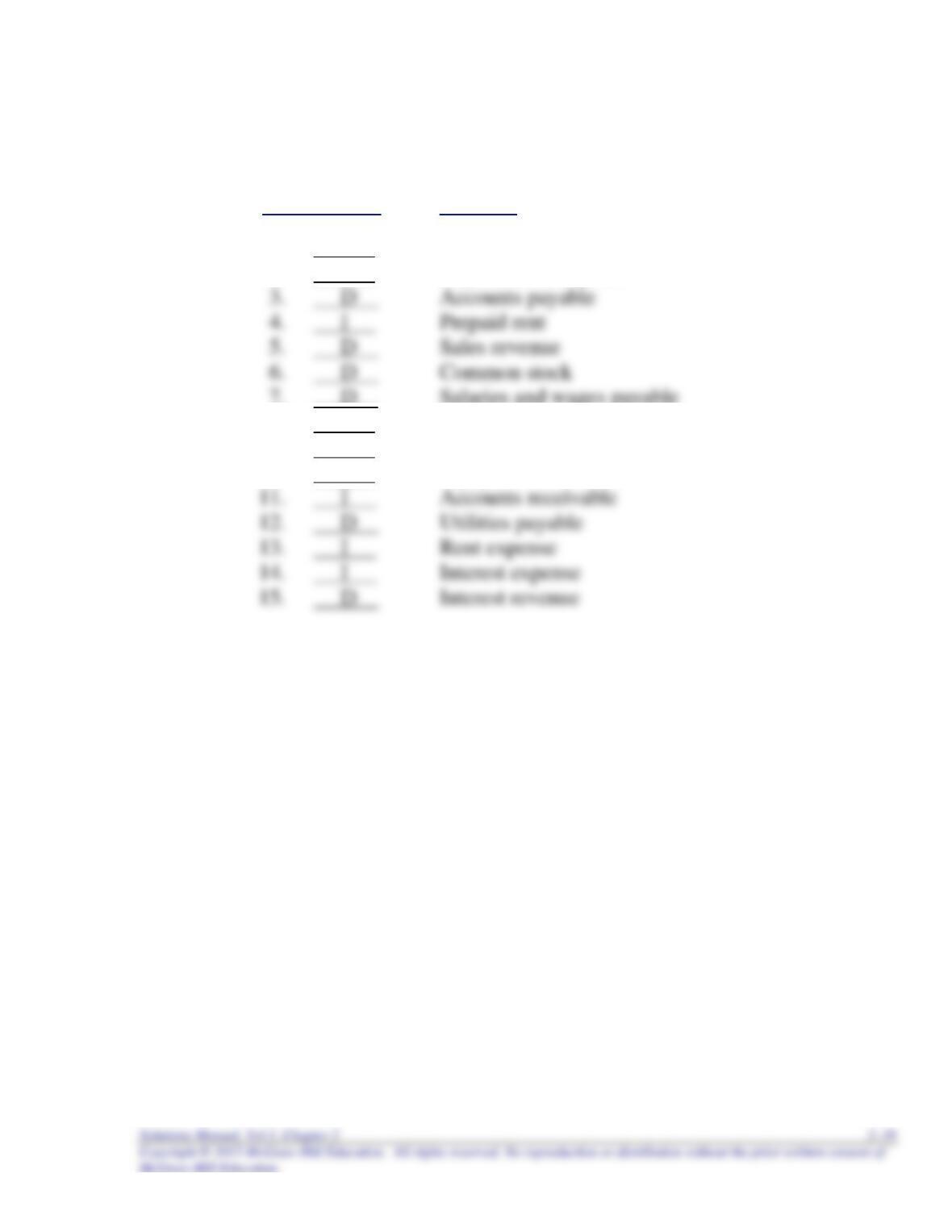

Exercise 2–5

List A List B

k 1. Source documents a. Record of the dual effect of a transaction in

debit/credit form.

f 5. Unadjusted trial balance e. Determine the dual effect on the accounting

equation.

b 6. Adjusting entries f. List of accounts and their balances before

recording adjusting entries.

h 7. Adjusted trial balance g. List of accounts and their balances after

recording closing entries.

Exercise 2–6

Increase (I) or

Decrease (D) Account

1. I Inventory

2. I Depreciation expense

7. D Salaries and wages payable

8. I Cost of goods sold

9. I Utility expense

10. I Equipment

Exercise 2–7

Account(s) Account(s)

Debited Credited

Example: Purchased inventory for cash 3 5

1. Paid a cash dividend. 10 5

2. Paid rent for the next three months. 8 5

3. Sold goods to customers on account. 4,16 9,3

Exercise 2–8

1. Prepaid insurance ($12,000 x 30/36) .............................. 10,000

Insurance expense .................................................. 10,000

2. Depreciation expense ................................................. 15,000