Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 2

REVIEW OF THE ACCOUNTING PROCESS

Overview

Chapter 1 explained that the primary means of conveying financial information to investors,

creditors, and other external users is through financial statements and related notes. The purpose of

Learning Objectives

LO2-1 Analyze routine economic events—transactions—and record their effects on a company’s

financial position using the accounting equation format.

LO2-2 Record transactions using the general journal format.

Lecture Outline

I. The Basic Model

A. External events involve an exchange between the company and another entity; internal

transactions do not involve an exchange transaction but do affect financial position.

B. The accounting equation underlies the process used to capture the effect of economic

events (transactions):

Assets = Liabilities + Owners' equity

2-2 Intermediate Accounting, 8/e

II. The Accounting Processing Cycle

A. Step 1. Obtain information about transactions from source documents.

B. Step 2. Transaction analysis is the process of reviewing source documents to determine

the dual effect on the accounting equation and the specific elements involved.

III. Adjusting Entries (T2-7)

A. Step 6. Record adjusting entries and post to the ledger accounts.

B. Prepayments are transactions in which the cash flow precedes expense of revenue

recognition. (T2-8)

C. Accruals involve transactions where the cash outflow or inflow takes place in a period

subsequent to expense or revenue recognition. (T2-9)

1. Accrued liabilities represent liabilities recorded when an expense has been incurred

D. Estimates often are made to comply with the accrual accounting model. (T2-10)

1. Most estimates involve either prepayments or accruals.

IV. Step 8. Prepare Financial Statements

A. The income statement (T2-12)

V. Step 9. Close the Temporary Accounts (T2-16)

A. Close the revenue accounts to income summary.

VI. Conversion from Cash Basis to Accrual Basis (T2-18)

A. Add (deduct) increases (decreases) in assets. For example, an increase in accounts

PowerPoint Slides

A PowerPoint presentation of the chapter is available in the Connect library.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or

2-4 Intermediate Accounting, 8/e

TRANSACTION ANALYSIS

➢ Each transaction is analyzed to determine its effect on the

equation and on the specific financial position elements.

1. An attorney invested $50,000 to open a law office.

An investment by the owner causes both assets and owners’ equity to increase.

2. $40,000 was borrowed from a bank and a note payable was signed.

This transaction causes assets and liabilities to increase. A bank loan increases cash

3. Supplies costing $3,000 were purchased on account.

Buying supplies on credit also increases both assets and liabilities.

Illustration 2-1

TRANSACTION ANALYSIS

(continued)

4. Services were performed on account for $10,000.

Transactions 4, 5, and 6 are revenue and expense transactions. Revenues and

5. Salaries of $5,000 were paid to employees.

6. $500 of supplies were used.

7. $1,000 was paid on account to the supplies vendor.

This transaction causes assets and liabilities to decrease.

T2-1 (continued)

2-6 Intermediate Accounting, 8/e

ACCOUNTING EQUATION FOR A CORPORATION

➢ Owners' equity for a corporation, called shareholders' equity,

is classified as either paid-in capital or retained earnings.

T2-2

ACCOUNTING EQUATION

DEBITS AND CREDITS

INCREASES AND DECREASES

Assets = Liabilities + Paid-in Capital + Retained Earnings

___________ ____________ _____________ ________________

T2-3

2-8 Intermediate Accounting, 8/e

JOURNAL ENTRIES

July 1 Two individuals each invested $30,000 in the corporation. Each

investor was issued 3,000 shares of common stock.

July 1 Borrowed $40,000 from a local bank and signed two notes. The first

note for $10,000 requires payment of principal and 10% interest in six

July 6 Purchased $2,000 of supplies for cash.

July 4-31 During the month sold merchandise costing $20,000 for $35,000 cash.

July 9 Sold clothing on account to St. Jude’s School for Girls for $3,500. The

clothing cost $2,000.

Illustration 2-6

GENERAL JOURNAL

GENERAL JOURNAL

PAGE 1

Date

Account Title and Explanation

Post

Ref.

Debit

Credit

2016

July 1

Prepaid rent

130

24,000

Cash

100

24,000

To record the payment of one year’s rent

in advance.

July 1

Furniture and fixtures

150

12,000

Cash

100

12,000

To record the purchase of furniture and

fixtures.

2-10 Intermediate Accounting, 8/e

July 4-31

Cash

100

35,000

Sales revenue

400

35,000

To record cash sales for the month.

July 4-31

Cost of goods sold

500

20,000

Inventory

140

20,000

To record the cost of cash sales.

July 20

Accounts payable

210

25,000

Cash

100

25,000

To record the payment of accounts payable.

July 20

Salaries expense

510

5,000

Cash

100

5,000

To record the payment of salaries for the

first half of the month.

Illustration 2-7

T2-4 (continued)

GENERAL LEDGER

Cash 100 Prepaid Rent 130

Note Payable 220 Common Stock 300

T2-5

2-12 Intermediate Accounting, 8/e

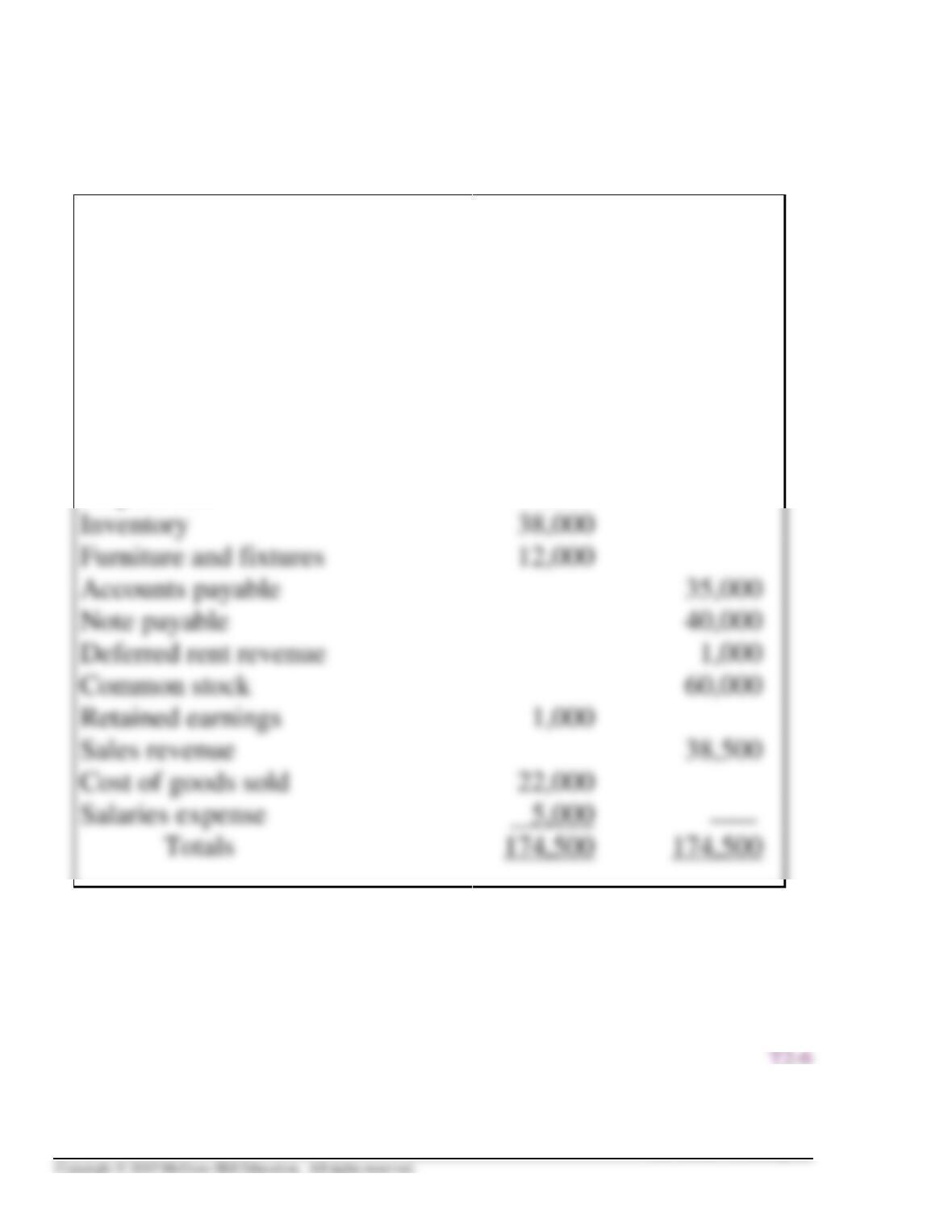

UNADJUSTED TRIAL BALANCE

DRESS RIGHT CLOTHING CORPORATION

Unadjusted Trial Balance

July 31, 2016

Account Title

Debits

Credits

Cash

68,500

Accounts receivable

2,000

Supplies

2,000

Prepaid rent

24,000

Illustration 2-9

ADJUSTING ENTRIES

➢ Even when all external transactions and events are analyzed,

journalized, and posted correctly to the appropriate ledger

accounts, some account balances will require updating.

Adjusting Entries

Prepaid Expenses Deferred Revenues

Illustration 2-10

T2-7

2-14 Intermediate Accounting, 8/e

PREPAYMENTS

Prepayments occur when the cash flow precedes either

expense or revenue recognition.

➢ PREPAID EXPENSES

To record the cost of supplies used during the month of July.

July 31

Supplies expense ................................. 800

Supplies ........................................... 800

Supplies Supplies expense

T2-8

PREPAYMENTS

(continued)

To record the cost of expired rent for the month of July.

July 31

To record depreciation of furniture and fixtures for the month of July.

July 31

Depreciation expense ......................... 200

➢ DEFERRED REVENUES

Deferred revenues represent liabilities recorded when cash is received

from customers in advance of providing a good or service.

To record the amount of deferred rent revenue recognized during July.

T2-8 (continued)