Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

4. Mixed costs are costs that have characteristics of both a variable and a fixed cost. The high-low

method uses the highest and lowest activity levels and their related costs to estimate the variable

6. A high contribution margin ratio, coupled with idle capacity, indicates a potential for increased

income from operations if additional sales can be made. A large percentage of each additional

9. The individual products are treated as components of one overall enterprise product. These

10. Operating leverage measures the relationship between a company’s contribution margin

and income from operations. The difference between contribution margin and income fro

m

operations is fixed costs. Thus, companies with high fixed costs will normally have a high

CHAPTER 19 (FIN MAN); CHAPTER 4 (MAN)

COST BEHAVIOR AND COST-VOLUME-PROFIT ANALYSIS

DISCUSSION QUESTIONS

19-1

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

PE 19–1A (FIN MAN); PE 4–1A (MAN)

PE 19–1B (FIN MAN); PE 4–1B (MAN)

PE 19–2A (FIN MAN); PE 4–2A (MAN)

PE 19–2B (FIN MAN); PE 4–2B (MAN)

PRACTICE EXERCISES

19-2

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

PE 19–3A (FIN MAN); PE 4–3A (MAN)

PE 19–3B (FIN MAN); PE 4–3B (MAN)

PE 19–4A (FIN MAN); PE 4–4A (MAN)

PE 19–4B (FIN MAN); PE 4–4B (MAN)

PE 19–5A (FIN MAN); PE 4–5A (MAN)

Unit selling price of E: [($150 × 0.70) + ($100 × 0.30)] = $135.00

PE 19–5B (FIN MAN); PE 4–5B (MAN)

Unit selling price of E: [($50 × 0.40) + ($60 × 0.60)] = $56.00

19-3

PE 19–6A (FIN MAN); PE 4–6A (MAN)

PE 19–6B (FIN MAN); PE 4–6B (MAN)

PE 19–7A (FIN MAN); PE 4–7A (MAN)

PE 19–7B (FIN MAN); PE 4–7B (MAN)

19-4

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–1 (FIN MAN); Ex. 4–1 (MAN)

1. Fixed 9. Fixed

Ex. 19–2 (FIN MAN); Ex. 4–2 (MAN)

Ex. 19–3 (FIN MAN); Ex. 4–3 (MAN)

Ex. 19–4 (FIN MAN); Ex. 4–4 (MAN)

EXERCISES

19-5

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–5 (FIN MAN); Ex. 4–5 (MAN)

a. Fixed g. Variable

Ex. 19–6 (FIN MAN); Ex. 4–6 (MAN)

Total costs:

Supporting calculations:

a. $0.40 ($160,000 ÷ 400,000 units)

19-6

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–7 (FIN MAN); Ex. 4–7 (MAN)

The fixed cost can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of production, as

follows:

Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Highest level:

b. Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Total cost for 12,000 units:

Variable cost:

=Variable Cost per Unita.

Difference in Total Costs

Difference in Units Produced

19-7

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–8 (FIN MAN); Ex. 4–8 (MAN)

The fixed costs can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of gross-ton mile,

as follows:

Highest level:

Ex. 19–9 (FIN MAN); Ex. 4–9 (MAN)

a. Sales………………………

…

$2,750,000

b. Sales…………………………………………………

…

=

Variable Cost per

Gross-Ton Mile Difference in Gross-Ton Miles

Difference in Total Costs

$1,450,000

19-8

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–10 (FIN MAN); Ex. 4–10 (MAN)

a. Sales (in millions)…………………………………………………………………

…

$16,233

Variable costs (in millions):

c. Same-store sales increase (in millions)…………………………………

…

Ex. 19–11 (FIN MAN); Ex. 4–11 (MAN)

a. Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

$811 million

Sales – Variable Costs

Sales

b. =Contribution Margin Ratio

19-9

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–12 (FIN MAN); Ex. 4–12 (MAN)

Total Cost Variable Cost Variable Cost

(in millions) Percentage (in millions)

Cost of goods sold………………………

…

$16,151.0 × 70% = $11,305.7

Ex. 19–13 (FIN MAN); Ex. 4–13 (MAN)

a. Break-Even Sales (units) =

Fixed Costs

Unit Contribution Margin

a. Break-Even Sales (units) =

Fixed Costs

Unit Contribution Margin

19-10

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–14 (FIN MAN); Ex. 4–14 (MAN)

Ex. 19–15 (FIN MAN); Ex. 4–15 (MAN)

The cost of the promotional campaign is the fixed cost in this analysis, since

we’re trying to determine the break-even adoption rate of the campaign.

Unit Contribution Margin

=Break-Even Sales (units)

Fixed Costs

19-11

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–16 (FIN MAN); Ex. 4–16 (MAN)

1Revenue per account (in millions):

2Variable cost per account (in millions, except variable cost per account):

Cost of revenue……………………………………………… $17,492 × 75% = $13,119.0

=

$16,510.5 million

X – $464.7

Revenue per Account – Variable Cost per Account

Fixed Cost

Revenue per Account – Variable Cost per Account

=33.3 million accounts

b. Break-Even =

Fixed Costs

a.

Break-Even

19-12

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–17 (FIN MAN); Ex. 4–17 (MAN)

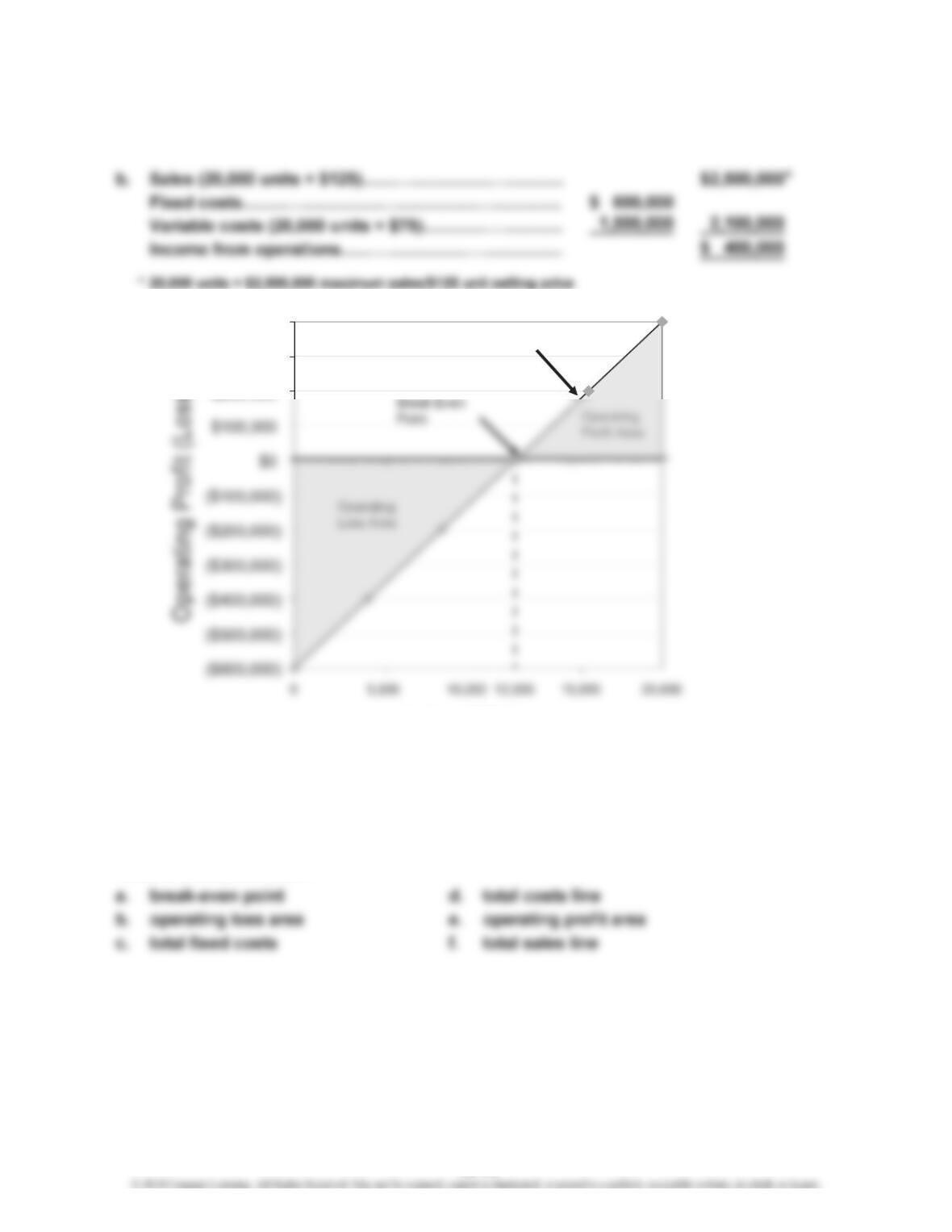

a.

$0

$500,000

$2,500,000

0 4,000 8,000 12,000 16,000 20,000

Units of Sales

Break-

Even Point

Operating

Profit Area Total Sales Line

Operating

Loss Area

$600,000

19-13

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–18 (FIN MAN); Ex. 4–18 (MAN)

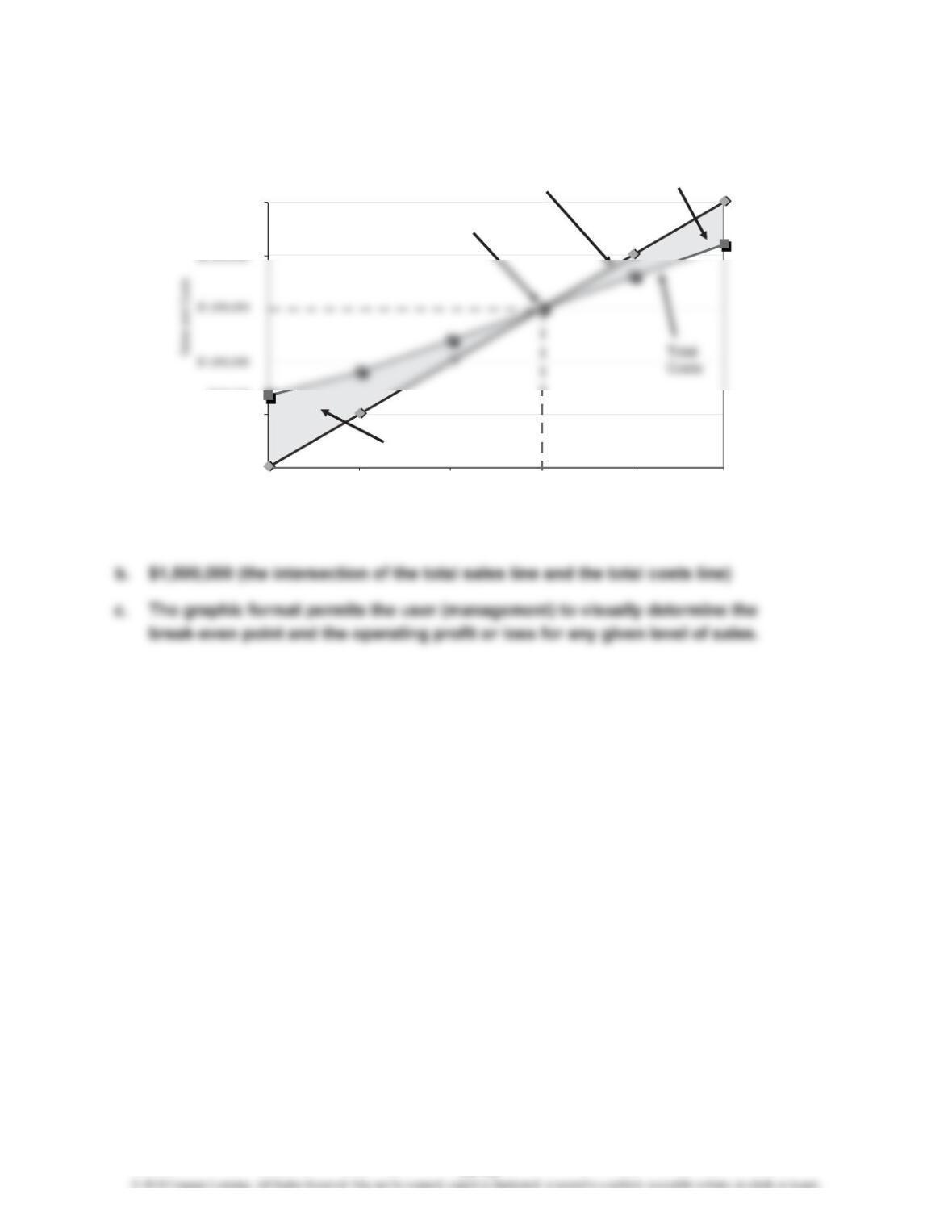

a. $600,000 (total fixed costs)

c.

d. 12,000 units (the intersection of the profit line and the horizontal axis)

Ex. 19–19 (FIN MAN); Ex. 4–19 (MAN)

Cost-volume-profit chart

$200,000

$300,000

$400,000

Units of Sales

Profit Line

19-14

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–20 (FIN MAN); Ex. 4–20 (MAN)

Profit-volume chart

a. break-even point

Ex. 19–21 (FIN MAN); Ex. 4–21 (MAN)

a. Unit Selling Price of E = ($90 × 40%) + ($105 × 60%)

19-15

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–22 (FIN MAN); Ex. 4–22 (MAN)

a. Unit contribution margin of overall product (E):

Unit selling price of E [(20% × $1,000) + (80% × $200)]………………………

…

$360

Fixed costs of the New York City to George Town, Grand Cayman round-trip flight:

Fuel………………………………………………

…

$10,400

Break-even sales (units) of overall product:

Ex. 19–23 (FIN MAN); Ex. 4–23 (MAN)

a. (1) Margin of Safety (dollars) = Sales – Sales at Break-Even Point

b. The break-even point (S) is determined as follows:

Break-Even Sales (dollars) = Total Fixed Costs + Total Variable Costs (at Break-Even)

Break-Even Sales (dollars) = Total Fixed Costs + 60% Break-Even Sales (dollars)

=Fixed Costs

Unit Contribution Margin

Break-Even Sales (units)

19-16

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 19–24 (FIN MAN); Ex. 4–24 (MAN)

Ex. 19–25 (FIN MAN); Ex. 4–25 (MAN)

a. Beck Inc.:

b. Beck Inc.’s income from operations would increase by 100% (5.0 × 20%),

Appendix Ex. 19–26 (FIN MAN); Appendix Ex. 4–26 (MAN)

=

Contribution Margin

Income from Operations

Operating Leverage

19-17

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Appendix Ex. 19–27 (FIN MAN); Appendix Ex. 4–27 (MAN)

a.

Sales $4,440,000

Variable cost of goods sold:

Computations:

Variable cost of goods manufactured: $3,120,000 – $132,000 = $2,988,000

Units Sold = Units Manufactured – Units in Ending Inventory

b. Absorption costing income from operations…………………………………

…

$1,656,000

Note: The difference between the two income numbers can be reconciled

as follows:

RHYS COMPANY

Income Statement—Variable Costing

For the Month Ended July 31, 2014

19-18

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Appendix Ex. 19–28 (FIN MAN); Ex. 4–28 (MAN)

a.

Sales $7,450,000

Cost of goods sold:

Computations:

Unit cost of ending inventory:

Total cost of goods manufactured:

b. Note: The difference between the two income numbers can be reconciled

as follows:

TUDOR MANUFACTURING CO.

Income Statement—Absorption Costing

For the Month Ended June 30, 2014

19-19

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

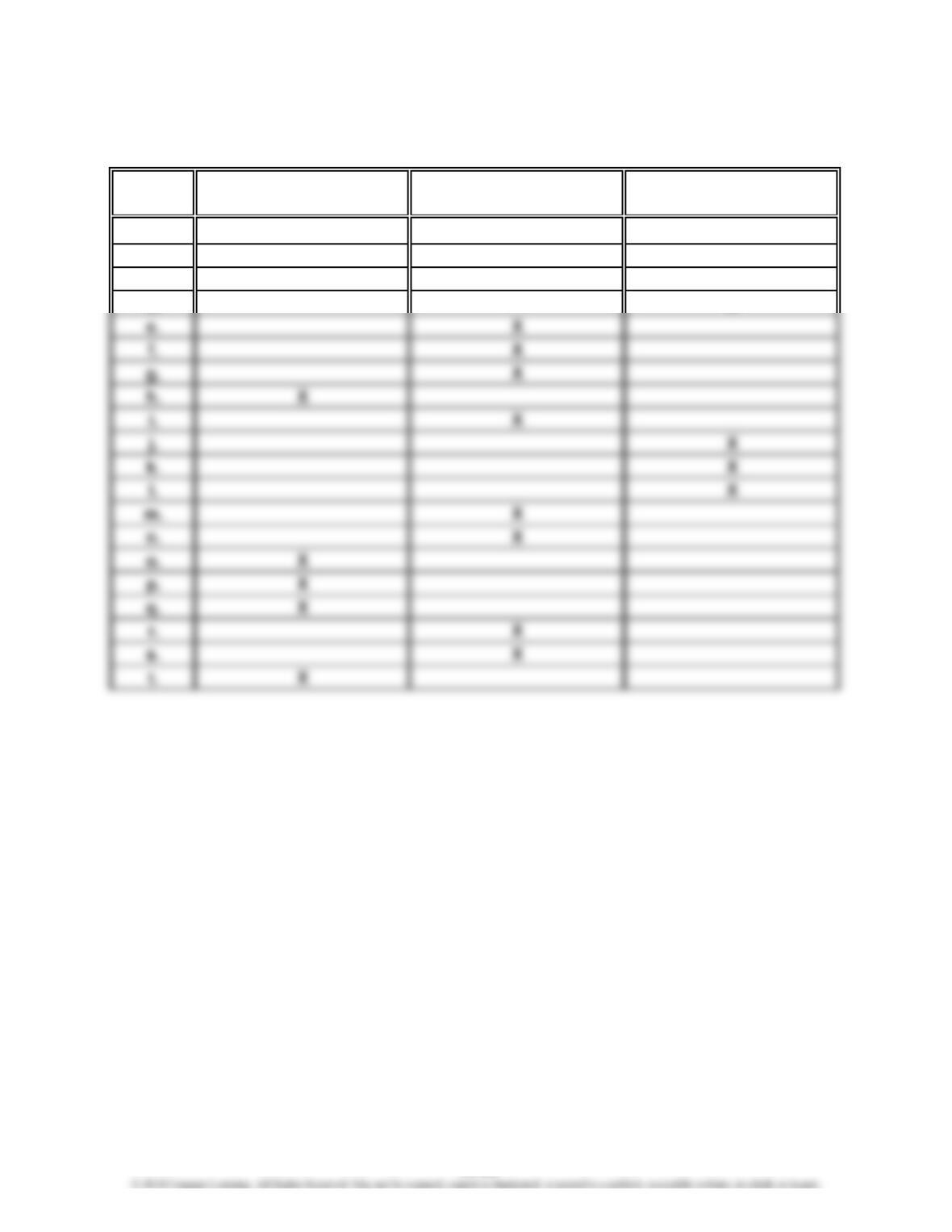

Prob. 19–1A (FIN MAN); Prob. 4–1A (MAN)

Fixed Variable Mixed

Cost Cost Cost Cost

a. X

b. X

c. X

d. X

PROBLEMS

19-20