Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 18–10

Transactions

N 1. Sale of common stock

N 2. Purchase of treasury stock at a cost less than the original issue price

N 3. Purchase of treasury stock at a cost greater than the original issue

price

Problem 18–11

A stock dividend is the distribution of additional shares of stock to current

shareholders of the corporation. The investor receives no assets, only additional

To record the investment ($ in millions)

Investment in L&K Corporation shares ................................ 52.8

Cash (1.2 million shares x $44) ............................................... 52.8

To record the sale of shares ..........................

10% stock dividend

There is no entry for the stock dividend, but a new investment per share must be

calculated for use later when the shares are sold:

To record the sale of shares

Cash (100,000 shares x $43) ....................................................... 4.3

Investment in L&K shares (100,000 shares x $40) ................. 4.0

Gain on sale of investments (difference) .............................. .3

Problem 18–12

Part A

Requirement 1

January 2

Cash (amount received) ...................................................... 30,000,000

Requirement 2

NICKLAUS CORPORATION

Balance Sheet-Shareholders' Equity Section

March 31, 2016

Shareholders' equity

Preferred stock, $5 par, authorized 1,000,000 shares,

18–64 Intermediate Accounting, 8/e

Problem 18–12 (continued)

Part B

Requirement 1

June 30

Treasury stock ($12 x 200,000 shares) ................................ 2,400,000

Cash ............................................................................. 2,400,000

July 31

Cash ($15 x 50,000 shares) .................................................. 750,000

Requirement 2

NICKLAUS CORPORATION

Balance Sheet - Shareholders' Equity Section

September 30, 2016

Shareholders' equity

Preferred stock, $5 par, authorized 1,000,000 shares,

issued and outstanding 1,000,000 shares $ 5,000,000

Common stock, $1 par, authorized 5,000,000 shares

Problem 18–12 (continued)

Part C

Requirement 1

October 1

No entry

November 1

Retained earnings ........................................................... 540,000

December 2

Retained earnings ($10 fair value x 58,000 shares2) 580,000

Common stock dividends

Problem 18–12 (continued)

Requirement 2

NICKLAUS CORPORATION

Balance Sheet-Shareholders' Equity Section

December 31, 2016

Shareholders' equity

Preferred stock, $5 par, authorized 1,000,000 shares,

issued and outstanding 1,000,000 shares $ 5,000,000

Problem 18–12 (concluded)

Requirement 3

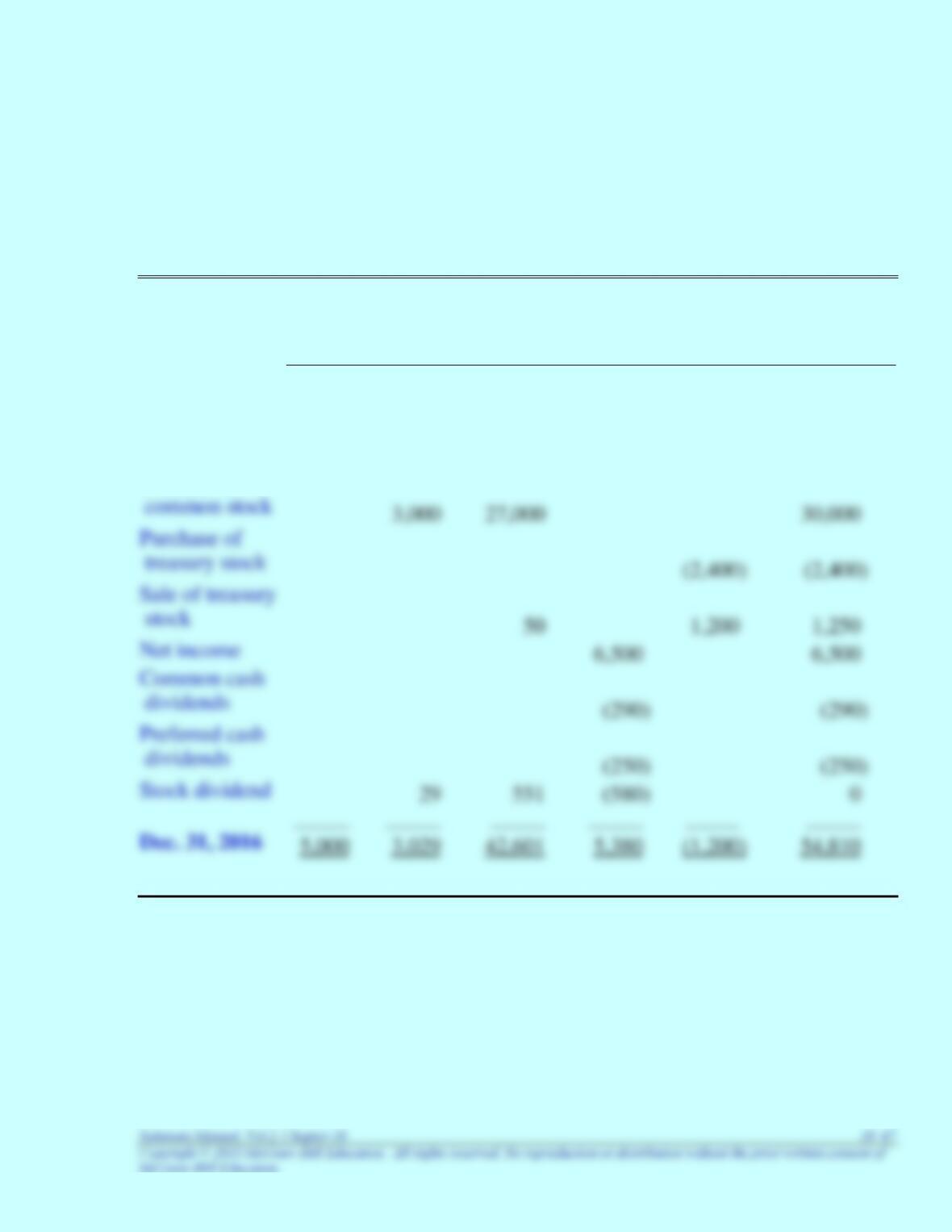

NICKLAUS CORPORATION

Statement of Shareholders’ Equity

for the Year Ended Dec. 31, 2016

($ in 000s)

Preferred

Stock

Common

Stock

Additional

Paid-in

Capital

Retained

Earnings

Treasury

Stock

Total

Share-

holders’ Equity

Jan. 2, 2016

––

––

––

––

––

––

Issuance of

preferred stock

5,000

15,000

20,000

Issuance of

18–68 Intermediate Accounting, 8/e

Problem 18–13

Requirement 1

To revalue assets:

To eliminate a portion of the deficit against available additional paid-in

capital:

Additional paid-in capital ....................................................... 60

Problem 18–13 (concluded)

Requirement 2

CHAMPION CHEMICAL CORPORATION

Balance Sheet

January 1, 2017

ASSETS

Current Assets:

Cash $ 20

LIABILITIES AND STOCKHOLDERS’ EQUITY

Liabilities $240

Stockholders’ Equity:

18–70 Intermediate Accounting, 8/e

CASES

Real World Case 18–1

Requirement 1

Assuming the shares are issued at the midpoint of the price range indicated, $14.50

Requirement 2

$ in millions

Cash (determined above) ........................................................... 398.750

Analysis Case 18–2

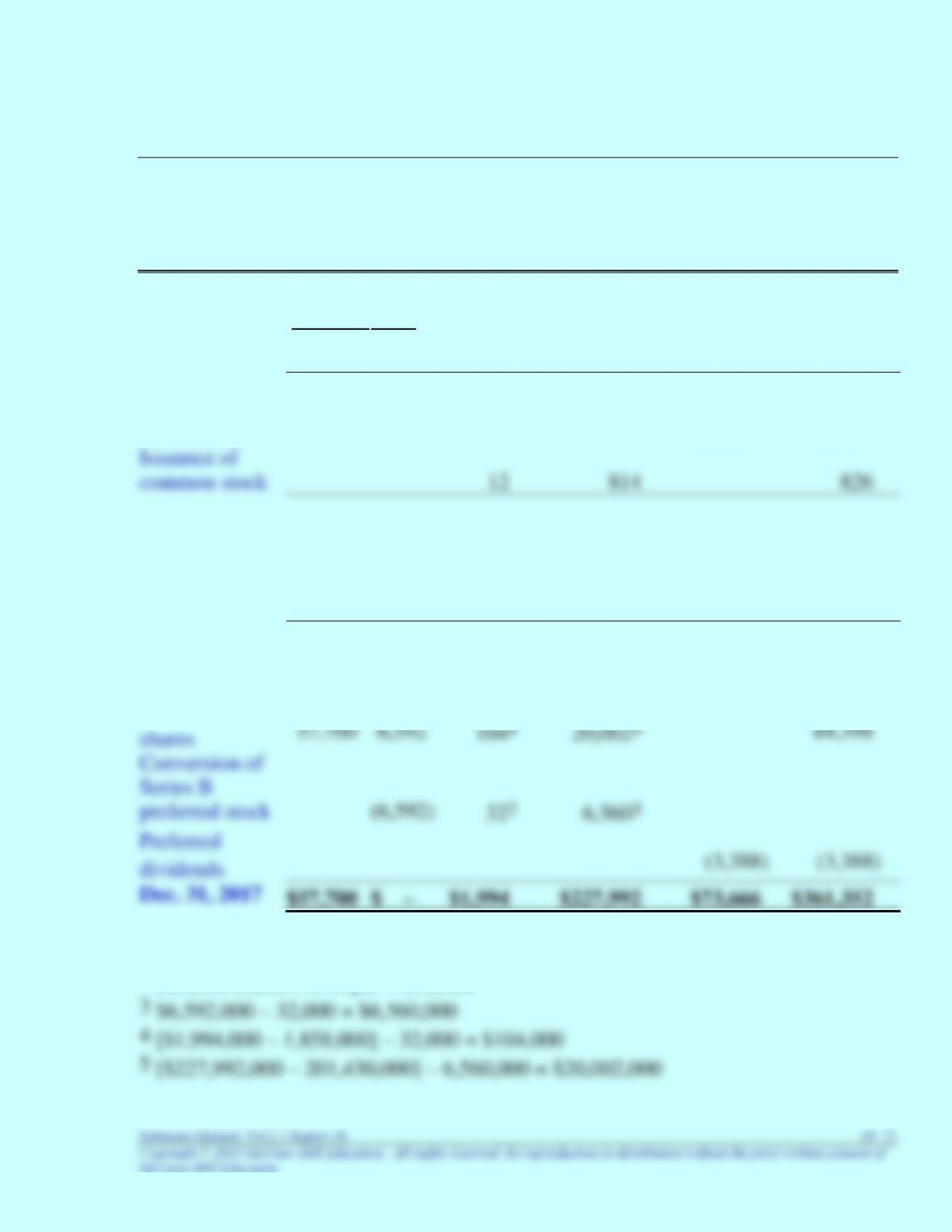

SESSEL’S DEPARTMENT STORES, INC.

Statement of Shareholders’ Equity

For the Years Ended December 31, 2017, 2016, and 2015

($ in 000s)

Preferred

Series A

Stock

Series B

Common

Stock

Additional Paid-

in

Capital

Retained

Earnings

Total

Share-

holders’

Equity

Dec. 31, 2014

$ –

$ –

$1,288

$ 88,468

$19,178

$108,934

Net income

13,494

13,494

Dec. 31, 2015

1,300

89,282

32,672

123,254

Net income

12,126

12,126

Issuance of

common stock

558

112,148

112,706

Dec. 31, 2016

1,858

201,430

44,798

248,086

Net income

32,2561

32,256

Issuance of

1 [$73,666,000 – 44,798,000] + 3,388,000 = $32,256,000

2 320,000 shares x $.10 par = $32,000

Communication Case 18–3

This case encourages students to consider the larger question of the factors that

differentiate whether financial instruments qualify for recognition as liabilities or part

of equity. It also requires them to carefully consider the profession’s definitions of

those elements. You may wish to suggest to your students that they consult FASB

ASC 480: “Distinguishing Liabilities from Equity” (previously SFAS No. 150,

Accounting for Certain Financial Instruments with Characteristics of both Liabilities

and Equity), and the FASB’s Preliminary Views on phase two of that project, which

Arguments brought out in IAS 32 cited above include the following:

Classification as Liability or Equity

The fundamental principle of IAS 32 is that a financial instrument should be classified

as either a financial liability or an equity instrument according to the substance of the

Case 18–3 (continued)

A financial instrument is an equity instrument only if (a) the instrument includes no

contractual obligation to deliver cash or another financial asset to another entity and

(b) if the instrument will or may be settled in the issuer's own equity instruments, it is

either:

Illustration – preference shares

If an enterprise issues preference (preferred) shares that pay a fixed rate of dividend

and that have a mandatory redemption feature at a future date, the substance is that

Arguments brought out in FASB documents cited above include the following:

Basic Ownership Approach—The Board’s Preliminary View

The underlying principle of the basic ownership approach is that claims against the

entity’s assets are liabilities (or assets) if they reduce (or enhance) the net assets

available to the owners of the entity. Under the approach, an instrument would be

classified as equity if it is a basic ownership instrument. A basic ownership instrument

18–74 Intermediate Accounting, 8/e

Case 18–3 (concluded)

Ownership-Settlement Approach

Under the ownership-settlement approach, an entity would classify instruments based

on the nature of their return and their settlement requirements (or lack thereof). The

following three types of instruments would be classified as equity:

1. Basic ownership instruments

An indirect ownership instrument has the following characteristics:

1. It is not perpetual

2. Its terms link its value to the price of a basic ownership instrument and cause its

If an instrument has one or more equity outcomes and one or more nonequity

outcomes, it would be separated into an equity component and a nonequity

component. Examples of instruments that would be separated are convertible debt and

puttable stock. The nonequity component of a separated instrument would be initially

Research Case 18–4

Requirement 1

Cisco reports accumulated other comprehensive income in its balance sheet as a

component of shareholders’ equity as follows:

($ in millions)

Shareholders' equity: 2013 2012

Preferred stock

Requirement 2

Cisco relies on FASB ASC 220–10–45–8: “Comprehensive Income–Overall–Other

Presentation Matters” when reporting comprehensive income. Cisco reports a separate

statement of comprehensive income.

45–8 An entity shall display comprehensive income and its components in a financial

statement that is displayed with the same prominence as other financial statements that

constitute a full set of financial statements. This Subtopic does not require a specific

Case 18–4 (continued)

Requirement 3

Comprehensive income is a more expansive view of the change in shareholders’

equity than traditional net income. It is the total nonowner change in equity for a

reporting period. In fact, it encompasses all changes in equity other than from

The first of these—components of comprehensive income created during the

reporting period—can be reported either (a) as an extension of the income statement

or (b) in a separate statement, immediately following the income statement.

($ in millions)

Net income $xxx

Other comprehensive income:

Net unrealized holding gains (losses) on investments (net of tax)† $ x

† Changes in the fair value of some equity securities.

‡ Gains and losses due to revising assumptions or market returns differing from expectations,

and prior service cost from amending the plan (described in Chapter 17).