Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

C

CH

HA

AP

PT

TE

ER

R

1

18

8

S

Sh

ha

ar

re

eh

ho

ol

ld

de

er

rs

s’

’

E

Eq

qu

ui

it

ty

y

Overview

We turn our attention in this chapter from liabilities, which represent the creditors’ interests in

the assets of a corporation, to the shareholders’ residual interest in those assets. The discussions

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

After studying this chapter, you should be able to:

LO18-1 Describe the components of shareholders’ equity and explain how they are reported in a

statement of shareholders' equity.

LO18-2 Describe comprehensive income and its components.

accounting for shareholders’ equity.

L

Le

ec

ct

tu

ur

re

e

O

Ou

ut

tl

li

in

ne

e

Part A: The Nature of Shareholders’ Equity

I. Sources of Shareholders’ Equity

A. A company can raise money externally to fund operations in either of two ways:

1. Debt financing.

18-2 Intermediate Accounting, 8/e

2. Equity financing.

a. Creates ownership interests in the assets of the business.

B. Shareholders’ equity is created mainly by:

1. Amounts invested by shareholders – paid-in capital.

2. Amounts earned by the firm on behalf of its shareholders – retained earnings.

II. Shareholders’ Equity in Financial Statements

A. The balance sheet reports balances of shareholders’ equity accounts. (T18-2)

B. Comprehensive income, a more expansive view of the change in shareholders’ equity than

traditional net income, is the total nonowner change in equity for a reporting period.

Transactions between the corporation and its shareholders primarily include dividends and

the sale or purchase of shares of the company’s stock. Nonowner changes other than those

Part B: Paid-In Capital

I. Fundamental Share Rights

A. Usually ownership rights held by common shareholders include the right to:

1. Vote.

2. Share in profits when dividends are declared.

II. The Concept of Par Value

A. Par value has little significance other than historical.

III. Accounting for the Issuance of Shares

A. When shares are sold for cash, shareholders’ investment is allocated between stated

capital and additional paid-in capital. (T18-5)

B. At times, shares are sold for noncash consideration like a service or a noncash asset.

(T18-6)

1. The transaction should be recorded at the fair value of either the shares or the

E. Share issue costs are the costs of the legal, promotional, and accounting services

necessary to effect the sale of shares.

1. The costs reduce the net cash proceeds from selling the shares and thus paid-in

capital – excess of par.

2. Share issue costs are not recorded separately.

IV. Reacquired Shares

A. Companies sometimes reacquire shares previously sold.

1. The most common motivation is to support the market price of the shares.

2. All share repurchases are functionally the same.

3. The difference between the cash paid to buy the shares and the amount the shares

originally sold for are treated differently depending on whether that difference is

positive (credit) or negative (debit):

C. Corporations often view a share buyback as a purchase of treasury stock.

1. The cost of acquiring the shares is “temporarily” debited to the treasury stock

account.

2. We delay recording the effects on specific shareholders’ equity accounts until later

Part C: Retained Earnings

I. The Nature of Retained Earnings

A. In Part B, we studied invested capital. In Part C, we consider earned capital, usually

referred to as retained earnings. (T18-12)

II. Dividends

A. Most corporate dividends are paid in cash. At the declaration date, retained earnings is

reduced and a liability is recorded. Registered owners of shares on the date of record are

III. Stock Distributions

A. In a stock dividend, additional shares of stock are distributed to existing shareholders.

1. A stock dividend affects neither the assets nor the liabilities of the firm.

B. A stock distribution of 25% or higher is a stock split. (T18-16)

Decision-Makers’ Perspective

A. Profitability is vital to a company's long run survival.

B. The return on shareholders' equity is a popular summary measure of profitability.

1. The return on shareholders' equity is calculated by dividing net income by average

3. A common variation is the inverse – the price-earnings ratio.

D. Shareholders’ equity transactions can affect the return to shareholders.

1. When a company buys back some of its shares, the return on shareholders’ equity

goes up.

2. On the other hand, the buyback of shares uses assets, which decreases the resources

available to earn net income in the future.

E. Analysts should evaluate dividend decisions with consideration for prevailing

circumstances. Management must decide whether shareholders are better off receiving

cash dividends or having funds reinvested in the firm.

Appendix 18: Quasi-Reorganizations

A. A quasi-reorganization aids a company that experiences financial difficulties, and yet has

favorable future prospects.

1. Inflated asset values are written down.

18-6 Intermediate Accounting, 8/e

P

Po

ow

we

er

rP

Po

oi

in

nt

t

S

Sl

li

id

de

es

s

A PowerPoint presentation of the chapter is available at the textbook website.

T

Te

ea

ac

ch

hi

in

ng

g

T

Tr

ra

an

ns

sp

pa

ar

re

en

nc

cy

y

M

Ma

as

st

te

er

rs

s

The following can be reproduced on transparency film as they appear here, or

SHAREHOLDERS’ EQUITY

❖ Shareholders’ equity accounts represent the ownership

interests of shareholders. Shareholders’ equity is a residual

❖ Ownership interests of shareholders arise primarily from

two sources – (1) amounts invested by shareholders in the

T18-1

18-8 Intermediate Accounting, 8/e

Exposition Corporation

Balance Sheet ($ in millions)

December 31, 2016

Assets

[$3,000]

Liabilities

[$1,000]

Shareholders’ equity

PAID-IN CAPITAL:

Capital stock (par):

Preferred stock, 10%, $10 par,

Additional Paid-in Capital:

Paid-in capital – excess of par, common 260

Paid-in capital – excess of par, preferred 50

RETAINED EARNINGS 1,670

ACCUMULATED COMPONENTS OF COMPREHENSIVE INCOME:

Unrealized gains (losses) on investment securities (85)

Unrealized net loss on pensions (75)

COMPREHENSIVE INCOME

❖ Encompasses all changes in equity other than from transactions with

owners.

• Components of comprehensive income created during the reporting

period can be reported either (a) as an additional section of the

income statement, (b) as part of the statement of shareholders’ equity,

or (c) as a separate statement in a disclosure note:

($ in millions)

Net income $xxx

Other comprehensive income:

Net unrealized holding gains (losses) on investments (net of tax)† $ x

† Changes in the fair value of some securities.

‡ Gains and losses due to revising assumptions or market returns differing from expectations

and prior service cost from amending the plan (described in Chapter 17).

§ When a derivative designated as a cash flow hedge is adjusted to fair value, the gain or loss is

T18-3

18-10 Intermediate Accounting, 8/e

STATEMENT OF SHAREHOLDERS' EQUITY

T18-4

SHARES SOLD FOR CASH

❖ When shares are sold for cash, the capital stock account

(usually common or preferred) is credited for the amount

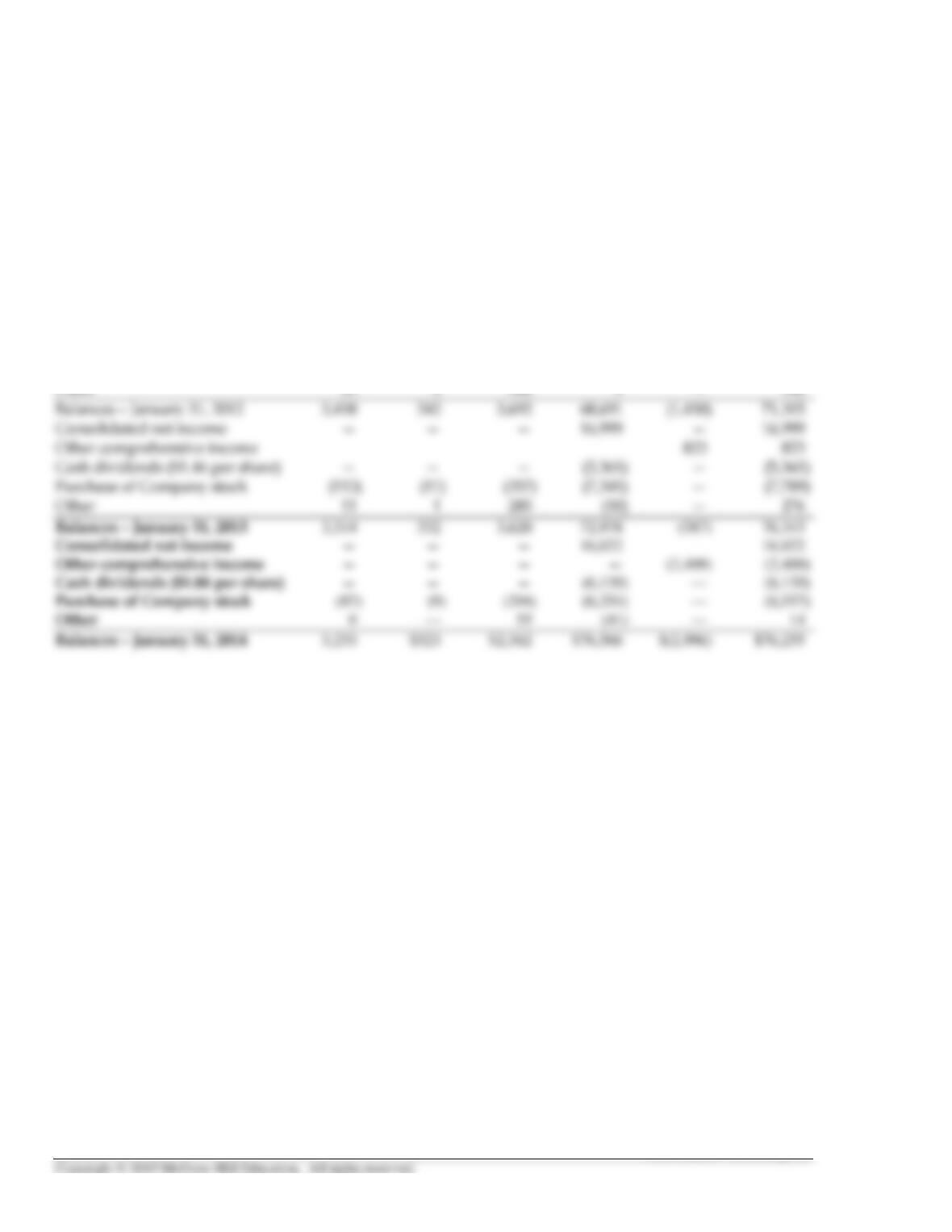

Wal-Mart Accum. Total

Capital in Other Walmart

Common Excess of Retained Compr. Sh/Hdrs’

(In millions, except per share amounts) Shares Stock Par Value Earnings Income Equity

Balances – February 1, 2011 3,516 $352 $3,577 $63,967 $646 $68,542

Consolidated net income — — — 15,699 — 15,699

Other comprehensive income — — — — (2,056) (2,056)

Cash dividends ($1.46 per share) — — — (5,048) — (5,048)

Purchase of Company stock (113) (11) (229) (5,930) — (6,170)

Other 15 1 344 3 — 348

❖ The entire proceeds from the sale of nopar stock are deemed

stated capital and recorded in the stock account.

T18-5

18-12 Intermediate Accounting, 8/e

SHARES SOLD FOR NONCASH CONSIDERATION

❖ Occasionally, a company might issue its shares for

consideration other than cash. It is not uncommon for a new

DuMont Chemicals issues 1 million of its common shares, $1

par per share, in exchange for a custom-built factory for which

no cash price is available. Today’s issue of the Wall Street

Journal lists DuMont’s stock at $10 per share:

($ in millions)

T18-6

MORE THAN ONE SECURITY

SOLD FOR A SINGLE PRICE

❖ More than one security might be sold for a single price. The

cash received usually is the sum of the separate market values

AP&P issues 4 million of its common shares, $1 par per share,

and 4 million of its preferred shares, $10 par, for $100 million.

Today’s issue of the Wall Street Journal lists AP&P’s common

at $10 per share. There is no established market for the preferred

shares:

($ in millions)

Cash ......................................................................... 100

❖ If the total selling price is not equal to the sum of the two

T18-7

18-14 Intermediate Accounting, 8/e

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Use of the term “reserves” and other terminology differences. Shareholders’

equity is classified under IFRS into two categories: Share capital and “reserves.” The

term reserves is considered misleading and thus is discouraged under U.S. GAAP.

Here are some other differences in equity terminology:

U.S. GAAP IFRS

Capital stock: Share capital:

Common stock Ordinary shares

Preferred stock Preference shares

COMPARISON OF SHARE RETIREMENT AND

TREASURY STOCK ACCOUNTING

– SHARE BUYBACKS

American Semiconductor’s balance sheet included the following:

Shareholders' Equity ($ in millions)

Common stock, 100 million shares at $1 par ............ $ 100

Retirement Treasury Stock

Reacquired 1 million of its common shares

Case 1: Shares repurchased at $7 per share

Common stock ($1 par x 1 million sh) 1 Treasury stock (cost) ............. 7

OR

Case 2: Shares repurchased at $13 per share

Common stock ($1 par x 1 million sh) 1 Treasury stock (cost) .............. 13

T18-9

18-16 Intermediate Accounting, 8/e

COMPARISON OF SHARE RETIREMENT AND

TREASURY STOCK ACCOUNTING

– SUBSEQUENT SALE OF SHARES

American Semiconductor sold 1 million shares after reacquiring shares at $13 per

share (Case 2 in Illustration 18-10)

Retirement Treasury Stock

Case A: Shares sold at $14 per share

Cash ................................... 14 Cash ............................................ 14

OR

Case B: Shares sold at $10 per share

Cash ................................... 10 Cash ............................................ 10

T18-10

REPORTING SHARE BUYBACKS IN THE

BALANCE SHEET

❖ Formally retiring shares restores the balances in both the Common

stock account and Paid-in capital – excess of par to what those

balances would have been if the shares never had been issued at all.

o Any net increase in assets resulting from the sale and

Shares Treasury

Retired Stock

Shareholders’ Equity ($ in millions)

Paid-in capital:

Common stock, 100 million shares at $1 par $ 99 $ 100